Bitget UEX Daily Report | Trump’s Visit to China; Wessel Approved as Fed Chair; PPI Hits Record High, Rate Hike Expectations Rise

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Trump’s Visit to China; Wessel Approved as Fed Chair; PPI Hits Record High, Rate Hike Expectations Rise

Overall, the market is in a window where policy uncertainty and event-driven factors are intertwined, and volatility may remain elevated.

I. Top News

Federal Reserve Updates

Kevin Warsh officially confirmed by the Senate as next Fed Chair

- On Wednesday local time, the Senate approved Kevin Warsh’s appointment as the next Federal Reserve Chair by a vote of 54 in favor and 45 opposed, succeeding current Chair Jerome Powell, whose term expires on May 15. This appointment concludes a months-long, highly contested selection process that began in summer 2025. Markets are closely watching for continuity in monetary policy under Warsh; near-term Fed decisions are likely to maintain a cautious stance, though longer-term uncertainty may amplify bond market volatility. The timing coincides with President Trump’s visit to China, underscoring the sensitivity of global central bank policy trajectories amid high-level U.S.-China engagement—and is expected to exert medium-term influence on USD and risk-asset pricing.

International Commodities

OPEC monthly report shows April crude output hit lowest level since 1990

- OPEC’s overall daily production plunged 1.727 million barrels month-on-month to 18.98 million barrels in April; Saudi Arabia accounted for roughly half the decline, with its output falling cumulatively by 42% to 6.32 million barrels per day—the lowest since the Gulf War;

- Supply contraction combined with geopolitical factors pushed oil prices higher in the short term;

- Analysts note this round of production cuts reinforces market expectations of a tight supply-demand balance, sustaining upward pressure on crude prices—though global demand slowdown remains a key downside risk.

Macroeconomic Policy

U.S. April PPI surges 6% YoY—highest since 2022—fueling rate-hike bets

- April PPI rose 1.4% MoM and 6% YoY, driven by sharp increases in energy and transportation costs; services-sector inflation reached a four-year high;

- The 30-year Treasury auction yield rose to 5.046%, the first time above 5% since the 2007 financial crisis; auction results were relatively weak;

- Pricing models now assign nearly a 50% probability to one rate hike within 2026; unexpectedly persistent inflation could force the Fed to delay rate cuts—or even pivot toward tightening—pressuring both bond and equity markets’ risk sentiment.

II. Market Recap

Commodities & FX Performance

- Spot gold: +0.13%, at ~$4,695/oz;

- Spot silver: +0.06%, at ~$87.50/oz;

- WTI crude: +0.21%, at ~$97.70/bbl;

- Brent crude: +0.08%, at ~$103.80/bbl;

- U.S. Dollar Index: edged higher to 98.457; strong PPI data and the new Fed Chair appointment boosted safe-haven USD buying.

Cryptocurrency Performance

- BTC: -1.27%, trading near $79,670; PPI-driven rate-hike concerns triggered a brief dip below $78,000 before modest recovery—remaining in a high-range consolidation;

- ETH: -0.58%, trading near $2,269;

- Total crypto market cap: -1.2% to $2.74 trillion;

- Liquidations: ~$375 million liquidated in past 24 hours, including ~$310 million long positions;

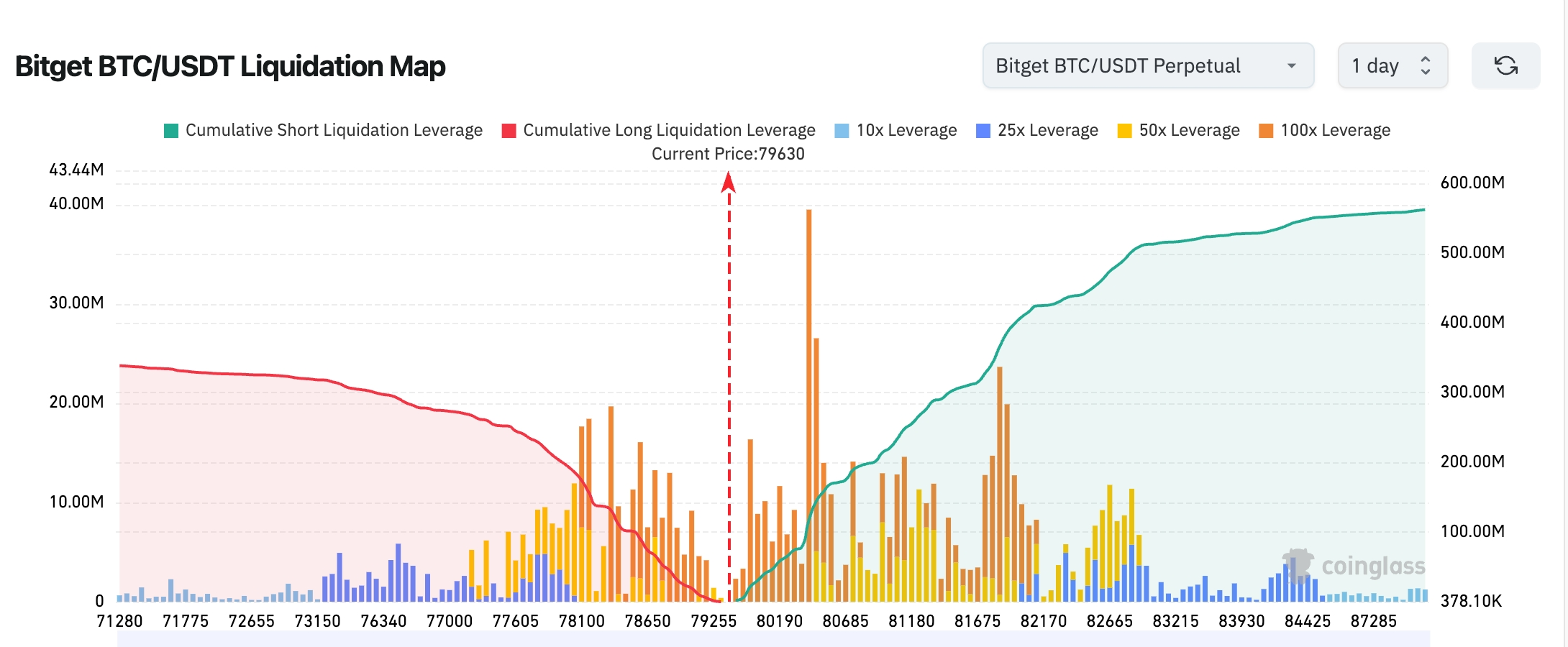

- Bitget BTC/USDT liquidation heatmap: Current BTC price ~$79,630; clear long/short liquidation boundary visible; heavy concentration of high-leverage short liquidations between $80,000–$82,000—further upside could trigger cascading short squeezes. Long liquidations cluster near $78,000, but total volume remains significantly lower than short-side exposure, suggesting a near-term “liquidity sweep upward” structure.

- Spot ETF net flows: BTC spot ETFs saw ~$346 million net outflow yesterday; ETH spot ETFs saw ~$14 million net outflow;

- BTC inflows/outflows: ~$212 million net outflow from spot markets yesterday; ~$802 million net outflow from derivatives markets.

U.S. Equity Index Performance

- Dow Jones: -0.14%, at 49,693.20—dragged down by defensive sectors, continuing modest correction;

- S&P 500: +0.58%, at 7,444.25—reaching a new all-time high, led by tech and growth stocks;

- Nasdaq: +1.20%, at 26,402.34—also hitting a new record high, driven primarily by a strong rebound in chip stocks.

Tech Giants’ Highlights

- NVIDIA (NVDA): +2.29%, at ~$226—AI demand remains robust;

- Google (GOOGL): +3.94%, at ~$402—strong performance across search and cloud businesses;

- Apple (AAPL): +1.38%, at ~$298—stable hardware ecosystem;

- Microsoft (MSFT): -0.63%, at ~$415—short-term profit-taking;

- Amazon (AMZN): +1.62%, at ~$270—dual momentum from e-commerce and cloud services;

- Meta (META): +2.26%, at ~$616—ad revenue exceeded expectations;

- Tesla (TSLA): +2.73%, at ~$436—confidence boosted by autonomous driving progress. Overall, six of the “Magnificent Seven” rose, with AI remaining the dominant theme—NVIDIA and Google leading gains.

Sector Highlights

Semiconductor/Chip Sector up >2%

- Key names: NVIDIA +2.29%; Cisco surged ~19% after hours;

- Catalyst: Significant AI order upgrades combined with accelerating global compute demand continue to justify sector re-rating.

Chinese ADRs rebounded collectively >7%

- Key name: 21Vianet +25%+;

- Catalyst: Strategic investor participation and improved U.S.-China high-level dialogue expectations lifted risk sentiment.

III. In-Depth U.S. Stock Analysis

1. Cisco (CSCO) – AI Orders Surge, Guidance Beats Expectations

Event Summary: Cisco reported Q4 revenue of $15.8 billion and adjusted EPS of $1.06—both slightly above consensus. Its Q1 FY25 revenue guidance of $16.7–16.9 billion exceeds market expectations by 5.6–6.8%. Annual AI orders from hyperscale cloud providers are now projected at $9 billion—up 80% from prior guidance—with $5.3 billion already secured. The company also announced a restructuring plan involving ~4,000 layoffs to sharpen strategic focus on AI. Market Interpretation: Analysts widely view Cisco’s AI transition as successful; the substantial order upgrade highlights its leadership in data center networking, sending shares up nearly 19% after hours. Investment Takeaway: The AI capex cycle remains in early stages; Cisco’s restructuring accelerates strategic alignment, enhancing long-term growth visibility—monitor upcoming AI order execution closely.

2. Cerebras Systems (CBRS) – IPO Pricing Repeatedly Raised, Valuation Nears $49 Billion

Event Summary: AI chipmaker Cerebras’ IPO has drawn overwhelming demand—over 20x oversubscribed—driving expected pricing to $185/share, well above its prior $150–160 range. The company has already raised both its price range and share count; valuation is poised to approach $49 billion. Arm and SoftBank previously attempted acquisition but were rebuffed. Market Interpretation: Wall Street is extremely bullish on AI infrastructure chip demand; Cerebras’ unique wafer-scale engine technology has garnered strong institutional interest. Investment Takeaway: Amid AI compute shortages, Cerebras’ listing may become a new benchmark for the semiconductor sector—short-term enthusiasm is high, but secondary-market volatility warrants close attention.

3. AMD – 13F Filing Reveals Quantum & Semiconductor Investment Strategy

Event Summary: AMD’s latest 13F filing shows significant增持 of Marvell Technology and entry into quantum computing—expanding its AI and advanced-node footprint. Market Interpretation: Analysts believe this bolsters AMD’s competitiveness in data centers and HPC, differentiating it from NVIDIA. Investment Takeaway: Through strategic investments in frontier technologies, AMD is positioned to capture long-term AI and quantum-computing tailwinds—track its ecosystem expansion closely.

IV. Crypto Project Updates

1. According to Cointelegraph, Société Générale will deploy EURCV and USDCV—euro- and dollar-backed stablecoins—on the Canton Network via its digital asset subsidiary SG-FORGE, targeting tokenized collateral, repo financing, and institutional settlements.

2. Prediction market Polymarket’s monthly trading volume fell ~8.9% to $10.2 billion in April—the first sequential decline since last August. Rival Kalshi posted a ~13% increase to $14.8 billion.

3. Mike Selig, newly appointed Chair of the U.S. Commodity Futures Trading Commission (CFTC), stated the agency stands ready to regulate emerging financial frontiers during his tenure. His Innovation Task Force is actively advancing initiatives to establish clear regulatory and compliance pathways for blockchain, AI, prediction markets, and other next-generation financial innovations—aiming to attract projects to build and operate in the U.S.

4. BitGo data shows “conviction buyers” now hold nearly 4 million BTC—an increase of 300% since end-2025. At the current ~$80,000 price, this “conviction capital” totals ~$320 billion.

5. Metaplanet—the largest corporate Bitcoin holder in Japan—has postponed its preferred stock listing. CEO Simon Gerovich cited Japan’s underdeveloped preferred stock market, regulatory requirements tying dividends to sustainable cash flow, and the company’s planned monthly dividend frequency—far exceeding Japan’s typical annual or semi-annual practice—as primary reasons.

6. Per The Block, Fidelity International launched FILQ—the first tokenized fund—representing its existing multi-billion-dollar institutional liquidity fund on-chain, offering 24/7 trading. Moody’s assigned FILQ its highest possible short-term rating: AAA-mf.

7. The U.S. Senate confirmed Kevin Warsh as Federal Reserve Chair by a 54–45 vote. Warsh had previously been confirmed by the Senate on May 12 for a 14-year term as a Fed Governor. With today’s (May 13) Chair confirmation, he will formally assume office upon completion of White House procedural formalities, succeeding Chair Powell whose term ends this Friday (May 15).

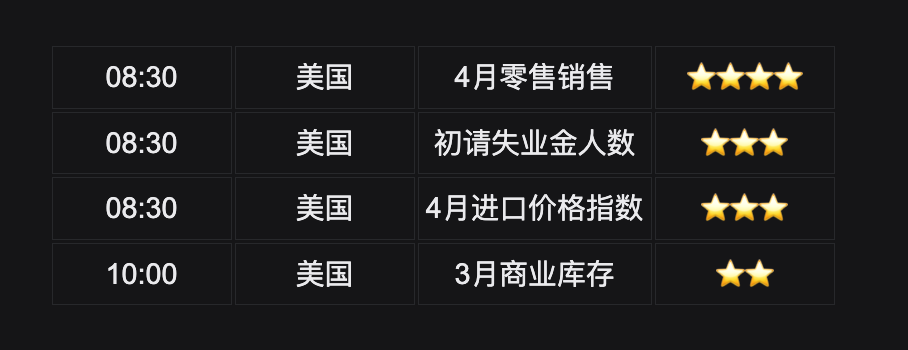

V. Today’s Market Calendar

Data Release Schedule

Key Event Preview

May 14 (Thursday)

- President Trump’s visit to China; U.S. government invited CEOs from NVIDIA, Apple, ExxonMobil, Boeing, and others to accompany him; ★★★★★

- U.S. equities: Applied Materials (AMAT) reports earnings after market close; Cerebras Systems expected to list on Nasdaq;

- New York Fed President John Williams speaks (Eastern Time afternoon); watch for latest comments on inflation and policy path.

May 15 (Friday)

- Powell’s term as Fed Chair ends; Warsh expected to succeed;

- 13F institutional holdings filing deadline—Berkshire Hathaway, Duan Yongping, and others to disclose latest U.S. equity positions.

*This week’s core themes include Powell’s departure/Warsh’s succession, U.S. CPI/PPI data, Trump’s China visit, and earnings from Circle, Oklo, AMAT, etc.—expect heightened volatility.

Institutional Views:

Goldman Sachs and other major banks point out that April’s hotter-than-expected PPI data, combined with the Fed Chair transition, have lifted near-term rate-hike odds to ~50%, sustaining upward pressure on Treasury yields and weighing on risk assets. Yet Trump’s China visit signals potential U.S.-China relations easing, which could alleviate trade friction concerns—benefiting global supply chains and tech stocks. Longer term, OPEC’s steep production cuts support oil prices; gold retains portfolio allocation appeal as a safe haven. While crypto markets face short-term headwinds, institutional ETF holdings show no signs of mass withdrawal, and BTC’s ~$78,000 level remains a strong technical support zone—monitor upcoming retail sales data for further Fed policy clues. Overall, markets sit at an inflection point where policy uncertainty and event-driven catalysts intersect—volatility is likely to remain elevated.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute investment advice. Data herein may contain inherent discrepancies; always refer to real-time market data for accuracy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News