Bitget UEX Daily Report | US-Iran Talks Stalemate, Inflation Concerns Weigh Heavily on Markets; US Equities Pull Back from Record Highs, Energy Prices Push Up Bond Yields

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | US-Iran Talks Stalemate, Inflation Concerns Weigh Heavily on Markets; US Equities Pull Back from Record Highs, Energy Prices Push Up Bond Yields

Overall, short-term macroeconomic and geopolitical factors dominate, while long-term structural opportunities in AI and the energy transition remain key areas of focus.

I. Top News

Federal Reserve Updates

Leadership Transition at the Fed: Powell to Serve as Acting Chair

- On May 15, the Federal Reserve announced that current Chair Jerome Powell would serve as “Acting Chair” until Kevin Warsh formally assumes the role—a move consistent with standard leadership transition protocols.

- Market attention has shifted to policy continuity under the new chair, especially amid persistent inflationary pressures. Market impact: Uncertainty during the transition period may amplify short-term volatility; investors are reassessing the likelihood of rate cuts under the new leadership in a high-oil-price environment—broad easing expectations have already significantly receded.

International Commodities

U.S.-Iran Stalemate Continues; Shipping Disruption in the Strait of Hormuz Pushes Energy Prices Higher

- U.S.-Iran negotiations remain deeply divided; Trump warned Iran it must act swiftly or face harsher consequences. The UAE and Saudi Arabia reported drone attacks, further escalating regional tensions.

- Crude oil prices surged sharply, with WTI approaching or exceeding $105 per barrel—driving up global inflation expectations. Market impact: Energy supply shortage risks triggered a sharp rise in bond yields; investor pricing of a “higher-for-longer” interest-rate regime intensified, while equity market risk appetite weakened.

Macroeconomic Policy

U.S. Treasury Yields Approach Record Highs; Inflation Concerns Dominate Market Sentiment

- The 30-year U.S. Treasury yield neared 5%—a two-decade high—while the 10-year yield rose significantly; Jeffrey Gundlach of DoubleLine Capital stated that a rate cut at the Fed’s next meeting is “simply impossible.”

- Initial progress was achieved in U.S.-China trade consultations—including consensus on tariffs, establishment of a joint council, and advancement on agricultural market access. Market impact: Elevated inflation expectations combined with geopolitical risks weighed on risk assets, while offering relative support to precious metals and energy-related sectors.

II. Market Recap

Commodities & FX Performance

- Spot Gold: –1.08%, ~$4,488/oz.

- Spot Silver: –1.84%, ~$74.45/oz.

- WTI Crude Oil: +1.38%, driven by concerns over disruption in the Strait of Hormuz, rising to $103/bbl.

- Brent Crude Oil: +1.12%, at $110/bbl.

- U.S. Dollar Index: +0.13%, strengthening to 99.37.

Cryptocurrency Performance

- BTC: –1.31%, ~$77,000; trading sideways amid dual pressure from geopolitical and macroeconomic headwinds—short-term sentiment weighed down by risk aversion.

- ETH: –3.2%, ~$2,100; tracking broader market trends with elevated volatility.

- Total Crypto Market Cap: –1.1%, at $2.65 trillion.

- Liquidations: ~$659 million liquidated in the past 24 hours, with $590 million in long positions.

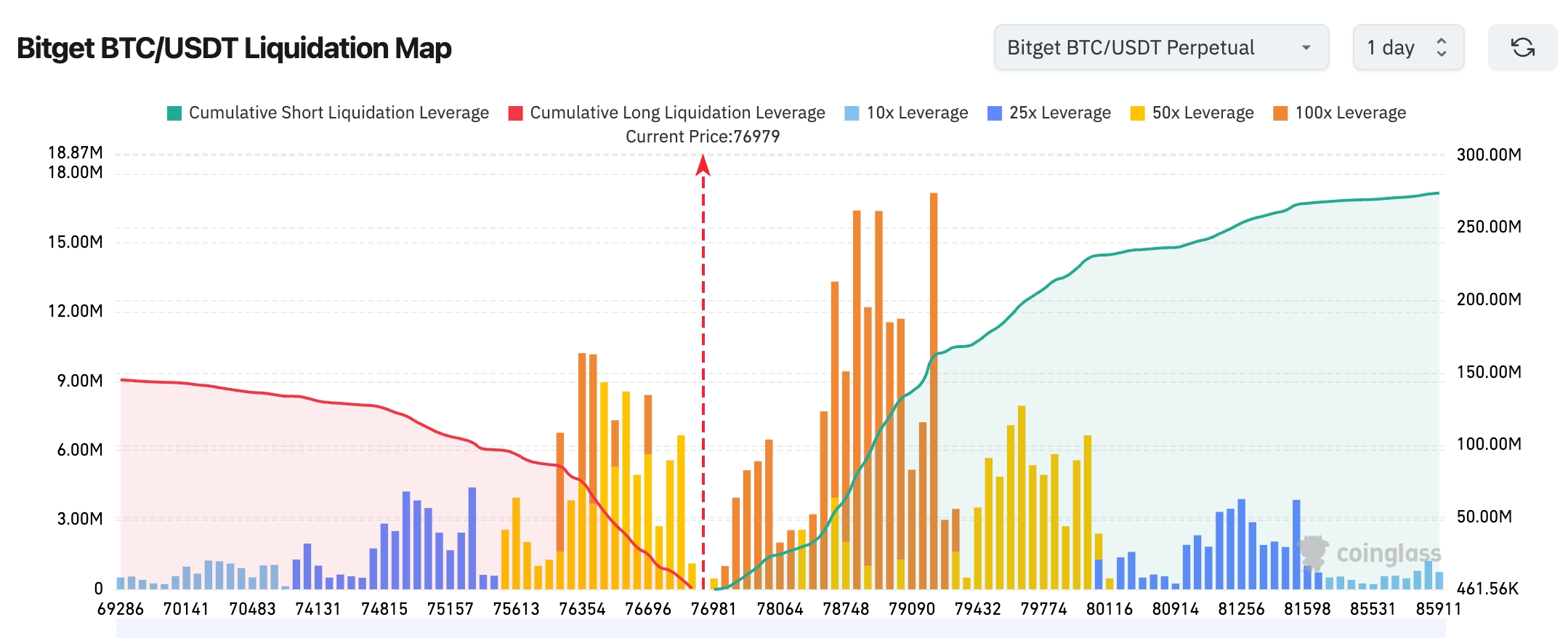

- Bitget BTC/USDT Liquidation Map: Near current price, resistance zones above correspond to dense liquidation clusters; downside support levels warrant caution around concentrated long positions.

- Spot ETF Net Flows: With BTC currently trading near $76,979, a large cluster of highly leveraged short positions lies between $78,700–$79,500. Further upside could trigger cascading short covering and amplify upward momentum. Conversely, a break below $76,000–$77,000—where long leverage is densely concentrated—may spark short-term long liquidation and deeper pullbacks.

U.S. Equity Index Performance

- Dow Jones Industrial Average: –1.07%, closing at 49,526.11; pullback from highs driven primarily by inflation concerns.

- S&P 500: –1.24%, at 7,408.50; retreating from record highs.

- Nasdaq Composite: –1.54%, at 26,225.14; tech stocks notably under pressure.

Tech Giants’ Performance

- Microsoft (MSFT): $414.23, –0.68%.

- Apple (AAPL): $300.23, +0.68%.

- NVIDIA (NVDA): $225.32, –4.42%.

- Meta (META): $614.23, –0.68%.

- Amazon (AMZN): $264.10, –1.15%.

- Google (GOOGL): $396.78, –1.07%.

- Tesla (TSLA): $422.24, –4.75%.

Summary: Most mega-cap tech names faced downward pressure; Microsoft held up relatively well due to its defensive characteristics. Rising inflation expectations and higher Treasury yields jointly pressured growth stock valuations, prompting some sector rotation.

Sector Rotation Highlights

Energy / Oilfield Services Sector: Strong rally, driven by sharp oil price gains.

- Key stocks: ExxonMobil (XOM) up ~4.07%; Chevron (CVX) up ~2.39%; Schlumberger (SLB) stable; Halliburton (HAL) outperformed.

- Catalysts: U.S.-Iran negotiation stalemate heightened concerns over supply disruptions in the Strait of Hormuz, amplifying global energy shortage risks and boosting crude prices—benefiting the entire upstream-to-midstream value chain.

Tech / Semiconductor Sector: Notable decline.

- Key stocks: Micron Technology (MU) down 6.62%; Intel (INTC) down 6.18%.

- Catalysts: AI investment enthusiasm temporarily dampened by high inflation, rising Treasury yields, and tightening rate expectations—prompting profit-taking and sector rotation.

Precious Metals Mining Sector: Broadly weaker (average stock declines of 2–5%).

- Catalyst: A stronger U.S. dollar and rising yields pressured non-yielding assets.

III. Deep Dive: U.S. Equity Analysis

1. SpaceX – IPO Listing Plans Overview: Elon Musk’s SpaceX has accelerated its IPO process, targeting pricing on June 11 and Nasdaq listing on June 12, with an estimated valuation of ~$1.75 trillion and planned fundraising of ~$75 billion—potentially among the largest IPOs in U.S. capital markets history. BlackRock and other institutions are reportedly considering participation in a $5–10 billion subscription. Market Interpretation: Institutional investors broadly view aerospace and satellite internet (Starlink) as beneficiaries of long-term structural growth—especially amid expanding global satellite communications demand and accelerating commercialization of the space economy. This IPO is not merely a capital event but could reshape market valuation frameworks for “hard-tech” mega-caps. However, the high valuation has also drawn concerns regarding profitability and execution risks; potential fund reallocation effects merit attention—some investors may rebalance away from Tesla and other Musk-linked assets to accommodate the new listing. Investment Takeaway: Significant liquidity and valuation volatility are likely in the early phase; best suited for long-term strategic allocation by investors confident in the space economy and satellite infrastructure themes—not for short-term speculation.

2. Samsung Electronics – Strike Risk Overview: Samsung Electronics faces its first-ever large-scale strike threat. Labor and management resumed “last-chance” negotiations on May 18, with strong warnings issued by the Korean government. The union insists on launching an 18-day strike starting May 21, demanding improved profit-sharing. Markets have already priced in negative expectations. Market Interpretation: As the world’s largest memory chip manufacturer, supply-chain disruption fears have triggered notable share price weakness and dragged down the broader semiconductor sector. If the strike materializes, daily losses could reach hundreds of millions of dollars—and potentially exacerbate global chip shortages, particularly amid surging AI compute demand. This event highlights dual challenges confronting tech giants: labor cost pressures and geopolitical supply-chain fragility—resonating strongly with the current high-rate, high-inflation environment. Investment Takeaway: Short-term semiconductor sector volatility will intensify; investors should closely monitor negotiation outcomes—the success or failure of talks will directly affect industry supply-demand balance and pricing power for related U.S.-listed supply-chain firms.

3. Microsoft – Gates Foundation Exit Overview: The Bill & Melinda Gates Foundation Trust fully exited its remaining ~7.7 million shares of Microsoft stock (valued at ~$3.2 billion) in Q1—ending a decades-long holding position. Bill Gates himself retains a substantial personal stake, while other institutions—including Bill Ackman’s Pershing Square—significantly increased positions during the same period. Market Interpretation: This exit reflects the foundation’s charitable funding and portfolio diversification needs—not a bearish view on Microsoft’s fundamentals. Microsoft remains dominant in AI (Copilot), cloud computing (Azure), and enterprise markets, and its continued high capital expenditure underscores long-term growth commitment. Institutional views are divergent: sellers provided liquidity; buyers bet on valuation attractiveness—illustrating typical institutional positioning dynamics for mature tech giants operating in a high-valuation environment. Investment Takeaway: Institutional flows do not alter Microsoft’s core AI+cloud growth trajectory; focus instead on quarterly earnings for validation of AI monetization progress—not isolated actions by one foundation.

4. Tesla – Model Y Price Increase Overview: Tesla raised prices on select mid- and high-trim U.S. Model Y variants for the first time in nearly two years: Premium RWD and AWD trims each increased by $1,000; Performance trim rose by $500; base model unchanged. Market Interpretation: This reflects pricing optimization amid mounting raw material, logistics, and operational cost pressures—and tests consumer willingness to pay for EVs in a high-oil-price environment. Amid intensifying competition and demand segmentation, Tesla uses premium-trim price hikes to restore margins, while keeping the entry-level variant stable to maintain sales volume thresholds. This strategy correlates positively with rising energy prices—but warrants caution regarding potential macro slowdown impacts on discretionary consumption. Investment Takeaway: Monitor upcoming delivery data and margin evolution; pricing flexibility will be key to sustaining competitive advantage in the evolving landscape—best suited for investors focused on Tesla’s long-term EV and energy ecosystem strategy.

IV. Cryptocurrency Project Updates

1. According to Blockaid monitoring, its vulnerability detection system identified an ongoing attack on the Verus-Ethereum cross-chain bridge (verus.io), resulting in approximately $11.58 million in losses.

2. Binance Research’s weekly chart analysis highlights four on-chain signals converging on the same conclusion: supply is tightening and selling pressure has been exhausted.

– Long-term dormancy: Nearly 60% of BTC supply has remained unmoved for over one year—far above the 27% level seen in 2012. Dormancy peaked at 69.5% in January 2024 following approval of spot Bitcoin ETFs and remains near historic highs.

– SLRV indicator: The Short-Term vs. Long-Term Holder Value Ratio has plunged deep into historical bottom territory, signaling subdued market sentiment. Long-term holders dominate supply, while short-term speculators have largely exited. Historically, every cycle bottom coincided with this ratio entering similar zones.

– Exchange balances: Having peaked at 17.6% during the pandemic, exchange-held BTC has now declined to 15.0%—with ~500,000 BTC permanently removed from exchanges. Seller supply has dropped to a six-year low.

– STH MVRV indicator: Since November 2024, BTC’s Short-Term Holder MVRV has spent most of its time below 1.0—gradually exhausting seller pressure. It has now rebounded to 1.0, indicating short-term holders are beginning to accumulate unrealized gains again. Given profit accumulation remains in early stages, renewed selling pressure is unlikely to emerge immediately—historically, this configuration often precedes sustained recoveries.

3. CryptoBriefing reported that Iran launched Hormuz Safe, its state-backed digital maritime insurance platform, offering shipping insurance for vessels transiting the Persian Gulf and Strait of Hormuz—with settlements in Bitcoin and other cryptocurrencies. Iranian authorities estimate that capturing a meaningful share of the Persian Gulf maritime insurance market could generate over $10 billion in revenue. Hormuz Safe aims to bypass SWIFT and Western intermediaries, reducing reliance on traditional financial infrastructure. Its biggest hurdle is international recognition—shipowners, trading companies, or port authorities engaging with the platform risk triggering secondary sanctions.

4. TsLombard noted that central banks globally may tighten policy only modestly in response to oil price shocks, making aggressive monetary tightening unlikely. In the U.S., the Fed is unlikely to implement any near-term tightening—any such action would almost certainly be deferred until 2027 at the earliest.

5. Tokens including ZRO, KAITO, and PYTH face major token unlocks this week, with PYTH’s unlock valued at ~$95.5 million.

6. CryptoQuant analyst Axel Adler observed that Bitcoin has recently tested the $82,000 level three times—each time failing to sustain the breakout. Data shows that during each rally, the STH-SOPR indicator rose toward 1.0 before weakening again—indicating short-term holders consistently locked in profits rather than holding through rallies.

Axel Adler noted that $82,000 is not only a critical technical resistance level but also a significant behavioral sell zone. This level currently coincides with Bitcoin’s 200-day moving average (200D SMA). Until the 7-day STH-SOPR SMA sustains above 1.0 for multiple days *and* BTC closes decisively above its 200D SMA on the daily chart, rallies may continue to be treated as selling opportunities.

At the macro level, escalating Middle East tensions continue suppressing market risk appetite. Impacted by Iran-related conflict, rising oil prices, and expectations of “higher-for-longer” rates, U.S. equities closed lower across the board on Friday. WTI crude futures rose over 4%, and the 10-year Treasury yield climbed to ~4.6%—a yearly high.

V. Today’s Market Calendar

Data Release Schedule

Key Event Preview

May 18 (Monday)

- U.S.-Israel reportedly set to restart strikes against Iran as early as this week ★★★★★

- U.S. Earnings: Baidu (BIDU) reports pre-market;

- G7 Finance Ministers and Central Bank Governors Meeting;

- Samsung Electronics labor-management enters second round of post-mediation talks (critical negotiations to avert strike) ★★★★★

May 19 (Tuesday)

- U.S. Weekly ADP Employment Change (week ending May 2);

- Google I/O 2026 Developer Conference (May 19–20); ★★★★★

- Russian President Putin’s state visit to China (May 19–20); ★★★★★

May 20 (Wednesday)

- NVIDIA (NVDA) reports Q1 earnings after market close (the absolute highlight of the week) ★★★★★

- SpaceX may file IPO prospectus as early as Wednesday, targeting June 12 listing ★★★★★

- U.S. Weekly EIA Crude Oil Inventory Report (week ending May 15);

- Other key U.S. earnings: Lowe’s (LOW), Analog Devices (ADI), Target (TGT), Intuit (INTU), GDS (GDS).

May 21 (Thursday)

- Fed releases minutes from April 28–29 FOMC meeting (Powell’s final minutes; signal for Warsh era) ★★★★★

- U.S. Weekly Initial Jobless Claims (week ending May 16);

- U.S. May S&P Global Manufacturing & Services PMI Preliminary Readings;

- Key U.S. earnings: Walmart (WMT), NIO (NIO), NetEase (NTES), Vipshop (VIPS) report pre-market;

May 22 (Friday)

- U.S. May University of Michigan Consumer Sentiment Index Final Reading.

*This week’s top U.S. equity catalysts: NVIDIA’s pivotal earnings (key test for AI rally sustainability), Fed meeting minutes (signal of Powell’s tenure end), Google I/O developer conference, SpaceX’s potential IPO filing, plus major earnings from Walmart and several Chinese tech/consumer names. Macro data and corporate events are exceptionally dense—expect pronounced market volatility.

Institutional Views:

Goldman Sachs and other institutions point to “Iran risk叠加 interest-rate storm” as the greatest current market threat. Growth expectations are already optimistic, while tail-risk pricing for geopolitics remains insufficient—if the Strait of Hormuz closure extends, it would force energy repricing and extreme volatility. An inflation-constrained Fed has limited room for easing, and equity market volatility thresholds have risen post-rally; investors should prepare for heightened uncertainty. Overall, near-term macro and geopolitical factors dominate, while long-term opportunities remain anchored in AI and energy transition themes.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute investment advice. Data herein may contain unavoidable inaccuracies—please refer to real-time market data for accuracy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News