Galaxy Creates Another New Concept "Inference Capital Market", 10,000-Word Research Report Targets AI Compute Financialization

TechFlow Selected TechFlow Selected

Galaxy Creates Another New Concept "Inference Capital Market", 10,000-Word Research Report Targets AI Compute Financialization

The previous ICM "Internet Capital Market" narrative has already caused me massive losses.

Author: Lucas Tcheyan (Galaxy Digital Vice President of Research)

Compiled by: TechFlow

TechFlow Editor's Note: Galaxy Digital's latest research report outlines the complete landscape of the "Inference Capital Market"—from GPU futures contracts soon to be launched on ICE and CME, to Venice turning inference access rights into tradable perpetual assets (DIEM), to Pearl and Ambient subsidizing inference costs with "Proof of Useful Work," and USD.AI lending for GPU hardware using stablecoin deposits. Inference is replacing training as the dominant force driving GPU demand, and the financial layer surrounding it is just beginning to take shape.

Introduction

The "On-chain Inference Capital Market" describes a system taking shape: a set of networks, protocols, infrastructure, and applications that liberate AI model inference from centralized APIs controlled by frontier labs and hyperscale cloud providers like OpenAI and Anthropic, coordinating and settling on-chain, and building a financial layer on top. Users can send prompts to GPU operator networks coordinated by crypto token incentives, and in certain configurations, obtain cryptographic or economic guarantees regarding output correctness and privacy.

This category has attracted increasing attention in 2026. Inference—processing new data with trained AI models to generate outputs—has surpassed training as the dominant share of global GPU demand. Meanwhile, autonomous agents have emerged as a new class of inference consumers: they pay programmatically and operate without human intervention.

Over the past few years, decentralized GPU markets, inference protocols, payment channels, tokenization, capital formation tools, and on-chain liquidity have each had their moment in the spotlight. The new change is that these primitives are converging into a single integrated system—an inference capital market. As inference is increasingly used for all work, this market is expected to find growing demand. On-chain experiments are unfolding around truly productive and economically meaningful activities, with demand coming not just from the crypto space.

Caption: Complete landscape of the Inference Capital Market

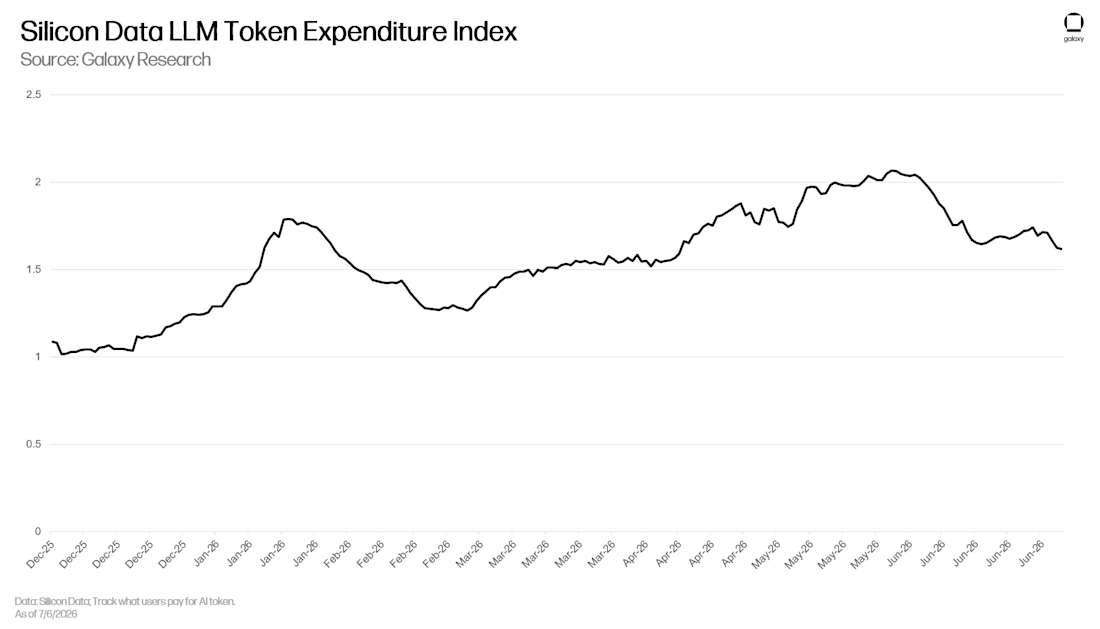

Several forces are driving this convergence. GPU usage is decisively shifting from training to inference, and open-weight models are catching up to frontier models at the "good enough" task level. This allows previously expensive tasks to be routed to the cheapest service providers—whether through crypto channels or not. Growing inference demand is also driving users to creatively seek compute sources. Citadel recently released a report showing that token spending measured by the Silicon Data LLM Index is declining, reflecting users shifting to cheaper models. (AI tokens—units AI companies use to price services—should not be confused with crypto tokens.)

Caption: Token spending trends tracked by the Silicon Data LLM Index

Companies like Coinbase, Microsoft, and AirBnB have recently also begun shifting to using open-source models, primarily Chinese models. OpenRouter's recent funding also proves growing market demand for diversified model access, which makes inference more economical. This is partly a result of supply constraints—chip shortages make marginal inference costs higher.

Caption: Illustration of inference supply constraints

The second force is financialization. The普及 of AI and its intelligence as input for almost all tasks is creating demand for its commoditization and financialization. More teams are thinking about how to turn AI compute into a tradable asset incorporated into a broader financial layer. Early frameworks for an inference capital market are emerging, financializing AI hardware and capacity, with the goal of assembling them into a complete market.

GPU Index and Futures Markets

Before diving into the on-chain inference capital market, one must first understand the larger market being developed off-chain—GPU futures.

Estimates for AI infrastructure investment vary widely. Morgan Stanley predicts global data center capital expenditure of about $2.9 trillion by 2028 (excluding power investment), with about $2.5 trillion related to AI. McKinsey estimates data centers will need $6.7 trillion in global capital expenditure by 2030, with $5.2 trillion for AI processing facilities and $1.5 trillion for traditional IT; its AI scenarios range from $3.7 trillion for constrained demand to $7.9 trillion for accelerated demand. Goldman Sachs estimates AI infrastructure capital expenditure of about $7.6 trillion between 2026 and 2031, covering compute, data centers, and power. Regardless of the exact numbers, these predictions consistently show: compute/hardware is the largest expenditure category, accounting for 55% to 67%.

These predictions are difficult because there are unknowns on both the supply and demand sides. One is demand elasticity—if cheaper compute is reinvested into larger models and broader deployments rather than saved, efficiency gains will expand usage rather than shrink bills. Another is the effective lifespan of chips, with depreciation estimates ranging from 3 to 7 years. Although more powerful chips are released every year, which should theoretically push old chips toward obsolescence, those "relics" continue to retain value. Severe supply constraints keep old hardware useful; they can also serve lower-tier models. The result is continuous capital flowing into a volatile asset—precisely the condition for pricing, hedging, and financing markets to begin forming.

"The work of procuring compute is compared to the drug market—you have a 'guy,' and you call when you need product."

In a sense, these markets already exist, just not in standardized form. Large buyers are already locking in future compute privately—from hourly rentals to multi-year reserved contracts (GPU-style offtake agreements), to bilateral deals between suppliers and largest customers, typically priced through opaque, relationship-driven negotiations. Frontier labs like OpenAI sell tokens in bulk, hyperscale cloud providers reserve capacity among themselves, and neoclouds forward purchase from clouds and brokers because supply falls short of demand. Baseten, one of the world's largest inference operators, compares today's compute procurement to the drug market—you have a "guy," and you call when you need product. Companies profiting from opacity—brokers and large holders—have little reason to give it up for transparent screens and a few basis points of efficiency gain. Similar vested interest resistance helped kill attempts to establish liquefied natural gas exchanges over a decade. GPU futures are emerging on this fragmented basis as a standardized layer for transferring price risk, but not yet as a substitute for capacity allocation methods.

For futures markets to operate, an accurate index is needed as a contract reference. For compute, this is harder than for standardized commodities. A "GPU hour" makes no sense without specifying chip model, memory and network configuration, region, and whether it is on-demand or reserved. Electricity, bandwidth, and LNG also had similar underlying commodity differences before becoming liquid markets. The solution is the same: define grades and reference prices, rather than requiring every unit to be identical. Crude oil is priced based on WTI and Brent, natural gas based on Henry Hub.

Caption: Analogy between GPU indices and commodity benchmarks

GPUs are converging toward a similar structure. Ornn (a Galaxy portfolio company) has released a compute price index based on real-time trading data. Silicon Data daily publishes H100, A100, and B200 leasing indices on the Bloomberg Terminal, normalizing pricing data from different configurations, suppliers, and regions into a single benchmark. Compute Desk is also building in the same direction. In Ornn's framework, these indices are more like SOFR (Secured Overnight Financing Rate) than its notorious predecessor LIBOR. Each index is constructed based on extensive actual trading data in the market, rather than expert panel estimates, tracking not a single GPU, but the market price of a defined set of compute.

This anchoring based on real-world transactions makes heterogeneity manageable. Indices do not need any two GPU hours to be identical, only enough real transactions to calculate a representative price. But it faces a problem crude oil does not: a barrel of standard WTI does not change, while GPU benchmarks decay as chips iterate from H100 to H200, B200, GB200, and then Rubin, forcing reference standards to be rewritten every generation. Fragmentation exacerbates this problem—AMD, Google TPU, Amazon Trainium, hyperscale self-developed chips, and sovereign chips分散 demand across incompatible silicon. Persistent benchmarks become harder to maintain.

The second point of contention is settlement method. Labs hedging compute budgets or trading desks making directional bets may only want pure price exposure; for them, a contract paying the difference based on the index is the entire purpose. But neoclouds needing real chips to serve customers need capacity itself. Futures launched so far are cash-settled, because price hedging demand is easiest to standardize—most commodity futures are cash-settled for the same reason. Physical delivery is possible but harder to provide, as it requires further standardization and specificity. There is also a view that this order is reversed—with supply controlled by few sellers, cash settlement based on weak indices is easy to manipulate; commodities usually require physical delivery or a working cash-and-carry mechanism for prices to converge on reality first.

The market also needs participants with real reasons to trade on both sides, not just speculators making directional bets. Natural buyers are companies whose costs are tied to compute and wish to lock in costs—AI labs, application companies, neoclouds that have committed capacity downstream and need to secure inputs. Natural sellers are companies holding GPU inventory but uncertain about future use—hyperscale cloud providers, large GPU holders, and brokers. Lenders providing financing for GPU procurement need the same reference prices, because debt secured by depreciating hardware must have a marking benchmark. Speculators and proprietary trading firms add liquidity on top. The main structural tension in the current market is: most sellers want to sell long-term contracts, while buyers want to buy short-term contracts—sellers want to lock in revenue, buyers want flexibility.

Despite these challenges, early signs of a more mature GPU market are beginning to appear. Prediction market platform Kalshi has already launched markets for specific GPU prices. ICE (parent company of the NYSE, collaborating with Ornn) and CME (collaborating with Silicon Data) have announced plans to launch GPU futures within the coming year. "Compute as a commodity" is about to become reality.

On-chain Inference Capital Market

Models and inference suppliers are essentially token factories. They accept raw input—GPUs, and refine it into output in the form of tokens. GPU hours are becoming increasingly standardized through GPU indices, but the token layer above is far from developed, with one model's tokens priced completely differently from another's. But this layer is taking shape. China's three major state-owned telecom operators have begun retailing inference as a metered utility, selling standardized monthly token packages, much like mobile data plans. Amazon is reportedly beginning to pay Anthropic based on consumed tokens rather than previously promised compute hours. The Shanghai Futures Exchange is said to be in early design of AI token futures, as a counterpart to the GPU contracts being built by CME and ICE on the input side.

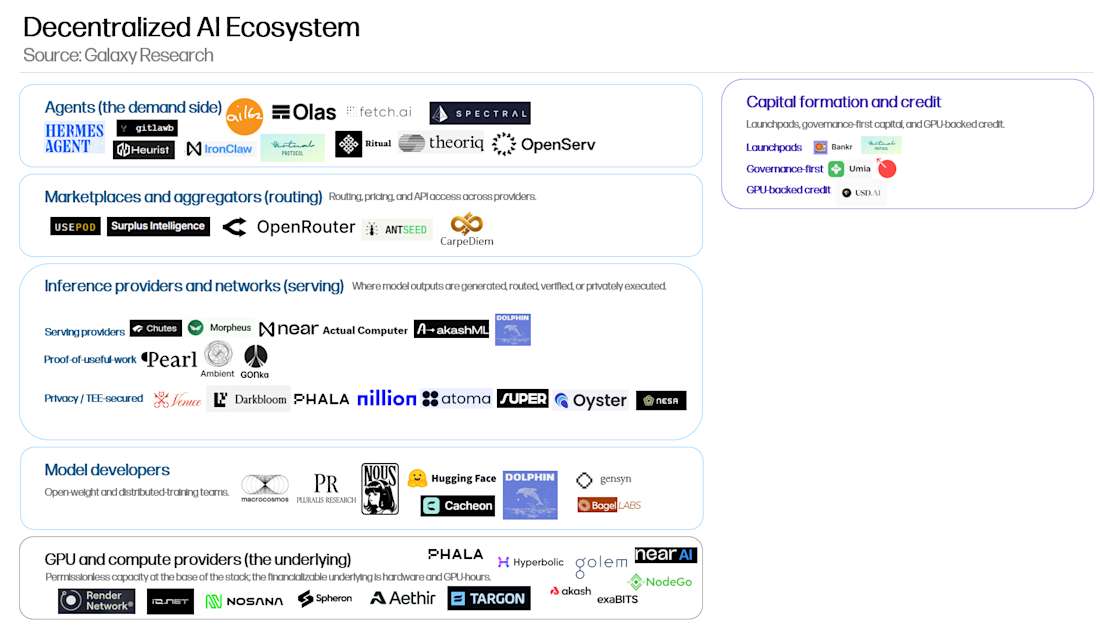

The crypto space is building its own version. These on-chain inference capital markets are built on existing crypto-AI primitives such as GPU suppliers and decentralized model developers, while incorporating emerging verticals such as agent payment standards and tokenized inference markets. The ecosystem has spanned multiple chains and execution environments, but development is particularly concentrated on Base and Solana, thanks to their mature developer and user bases.

Caption: On-chain Inference Capital Market Ecosystem Map

At the core are inference suppliers and networks—projects that turn prompts into outputs. Surrounding them are layers that make inference useful, accessible, and financializable: model developers, GPU and compute suppliers, routers and markets, agents and applications, payment channels, capital formation infrastructure. These peripheral layers are important because they either create inference demand, supply inference input, or turn inference usage into something that can be paid for, financed, routed, or owned.

Many of these products are not crypto-exclusive and have off-chain counterparts. At the top of the stack, agent frameworks like Hermes and Ironclaw can alternately fetch inference services from frontier labs or on-chain suppliers like Venice. Models from decentralized developers like Nous Research can be accessed on OpenRouter. GPU suppliers are permissionless, open-source counterparts to hyperscale clouds and data centers, usually much smaller in scale. Agent payment protocols like x402 and MPP can pay for OpenAI or Anthropic subscriptions just as conveniently as for Venice. Programmatic settlement is becoming standard rather than a crypto-exclusive advantage—OpenAI and Visa recently announced their own agent payment infrastructure.

Unique components appear on the financialization side, where crypto changes how inference is owned, priced, and financed. Financialized inference attracts a series of on-chain projects that use blockchain payment channels and tokenization to turn inference activities into tradable assets. This comes in three forms:

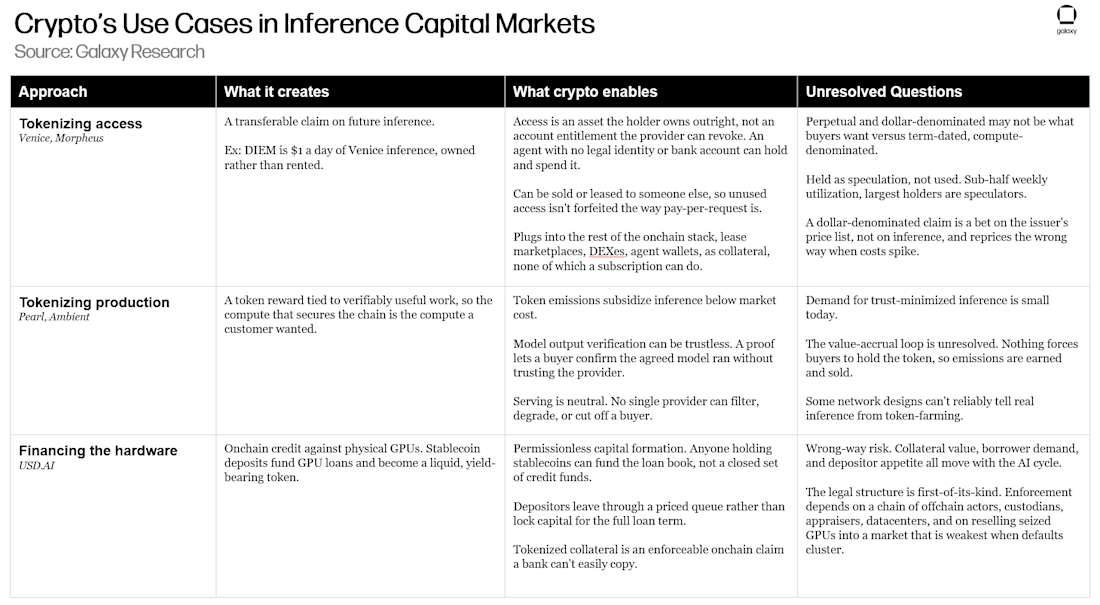

Inference service suppliers like Venice and Morpheus tokenize inference access rights, turning claims on future inference into something holders can hold, price, and resell.

Proof of Useful Work projects like Pearl and Ambient tokenize inference production, paying tokens for work serving inference.

Credit suppliers like USD.AI do something different. They do not tokenize inference itself, but provide financing for the hardware required to run inference, funding underlying GPUs and data centers with stablecoin deposits.

Together, these components constitute the on-chain inference capital market.

Inference Suppliers

The inference supplier layer is the core of the entire stack. This is where decentralized inference most directly resembles traditional AI API markets. Users or developers select models, send prompts, pay per token or per request or via subscription, and then receive outputs. The simplest version looks like using APIs from OpenRouter, Together AI, Fireworks, or frontier labs. The difference is that crypto-native suppliers may source capacity from decentralized GPU networks, accept stablecoin or token payments, provide access to open or uncensored models, include privacy guarantees, or attach tokenized access rights to usage.

Caption: Inference Supplier Landscape

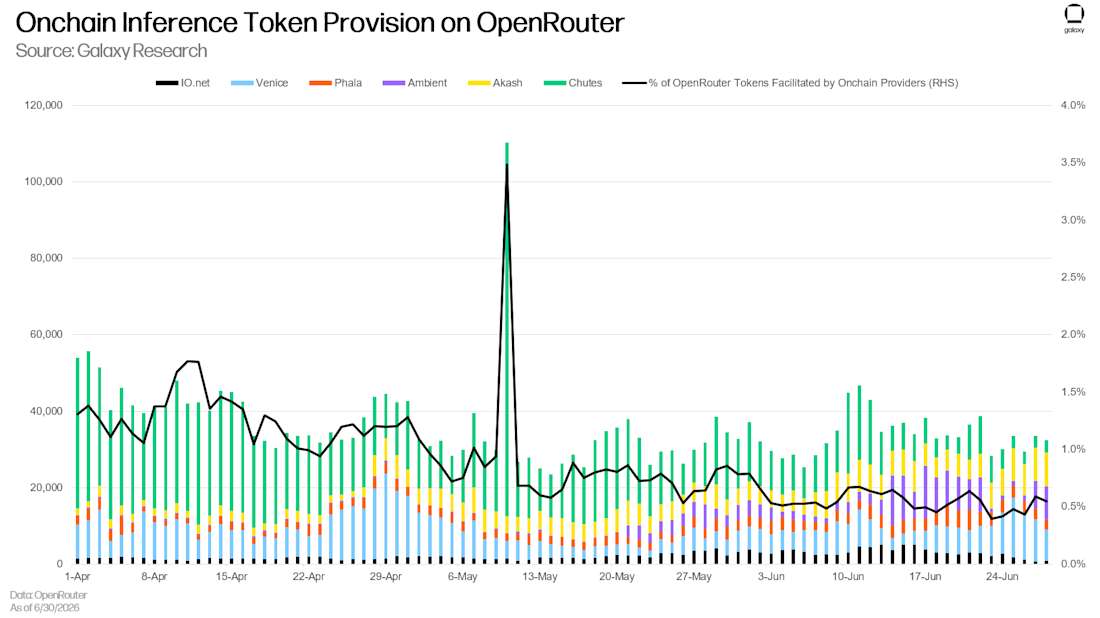

OpenRouter is one of the most favorable venues for on-chain inference. Demand there is priced per token, and users can freely switch suppliers on any request—this is exactly the environment where cheaper or faster suppliers should take share. Over the past three months, tokens processed by on-chain suppliers accounted for 0.5%-1% of OpenRouter's daily total, while total tokens processed by OpenRouter continued to grow explosively. This shows some initial traction outside the crypto-native community, but still only a small fraction of total usage, indicating these suppliers cannot yet compete with mature centralized products, whether due to insufficient distribution, relative cost, or other factors.

But OpenRouter represents only part of total token usage. For example, Venice reported that on June 23, all its access points processed 100 billion tokens, 10 times the amount it processed on OpenRouter. Looking only at OpenRouter usage cannot reflect overall traction at the project level; on-chain inference suppliers are trying various methods to build stable customer bases. Some are specific functions—Venice actively promotes privacy as a differentiating feature, allowing users not to worry about suppliers retaining, checking, leaking, censoring, or being forced to disclose sensitive information when using inference. Chutes and AkashML allow anyone to connect GPUs to their network and monetize idle compute, attempting to lower costs. While these features may help suppliers win some share, they can largely be replicated by centralized suppliers and may not be sufficient to gain meaningful market share.

Where on-chain products can truly establish differentiation is in mechanisms that financialize inference—turning access rights into assets buyers can own, hold, and resell, rather than subscriptions that can only be consumed.

Venice: Tokenized Inference Ownership

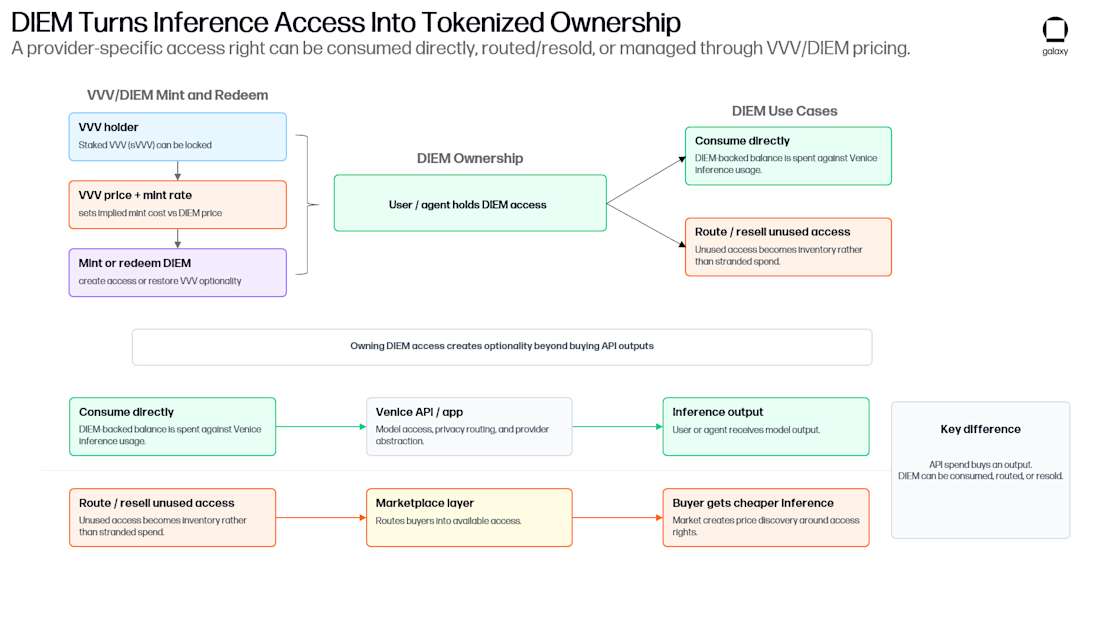

Venice, founded by crypto industry veteran and serial entrepreneur Erik Voorhees, has gone furthest in turning inference access rights into ownable assets. It runs a dual-token system—VVV and DIEM—packaging claims on future inference into something holders can mint, own, and resell.

VVV acts as the project's "capital asset." It does not represent ownership of the Venice platform—Venice has its own separate equity (in June, Venice completed a $65 million Series A financing, reaching unicorn valuation)—but holders theoretically benefit from the project's success. Most directly, part of Venice revenue is used to buy back and burn VVV. Buyback and burn comes in two ways: discretionary burn funded from general revenue, and programmatic burn routing a fixed proportion of every new subscription to buyback and burn. To date, 42% of VVV has been burned.

VVV also has utility. Any amount can be staked to receive annual VVV emissions, or staking 100 VVV unlocks a Pro subscription. But its most interesting use is its relationship with DIEM—Venice's "compute asset." Holders lock staked VVV to mint DIEM, each DIEM permanently granting $1 of Venice inference credits. Holding 100 DIEM gives $100 of API credits, applicable to all models on the Venice platform, valid permanently (or at least as long as Venice is operating).

The staked VVV required per DIEM follows a curve set by Venice, rising exponentially as DIEM supply approaches Venice's controlled target, because each DIEM is a perpetual one-dollar-per-day liability on Venice's books. Supply is now close to that target, so the rate has climbed from about 90 VVV/DIEM at launch to hundreds now. This suppresses issuance, meaning early minters obtained DIEM at a VVV price far below what anyone can obtain now. While VVV is locked to back DIEM, stakers retain only 80% of regular VVV staking yield, with the other 20% flowing to Venice. Locking can only be released by burning DIEM, so minters who have sold DIEM must reacquire DIEM on the market to redeem VVV—incurring losses if the price has risen.

Caption: Dual-token mechanism of VVV and DIEM

These two tokens reinforce each other. DIEM can only be minted by locking staked VVV, so rising DIEM demand pulls VVV out of circulating supply, giving it utility beyond speculation. Conversely, DIEM benefits from Venice's growth. The more useful and widely used the platform is, the more valuable the transferable claim on its daily access becomes. DIEM holders do not just own resalable inference—they hold a position tied to Venice's success.

Broader products are driving tokenomics even when users never touch crypto. The Venice team says most users are not crypto-native, and many do not care about tokens. But when they subscribe, buy credits, or use the platform, these activities still drive VVV buyback and burn and demand for Venice inference. Tokenomics sits downstream of the product, rather than replacing it. Venice is not a crypto token looking for an AI use case, but an AI product that routes part of usage and access rights to a tokenized inference market.

Caption: Venice Inference Usage Growth Trend

Venice's DIEM is unique in ownership. It lets users own the inference they consume, rather than renting it.

DIEM is an experiment in how to tokenize and deliver inference access. Its uniqueness lies in ownership—letting users own the inference they consume, rather than renting it. Buyers paying per request get nothing after inference is used up, while holders of tokenized access rights own an asset they can retain, transfer, or sell. This opens several use cases:

Because claims are tradable, holders with uneven demand can retain baseline access, selling or renting out unneeded days, recouping costs directly lost in pay-per-request models. Agents can directly hold DIEM, giving them a permissionless, ownable inference balance. Trades can be instant sales via Aerodrome, or fixed-term leases via markets like Surplus, UsePod, AntSeed, CarpeDiem, etc.

Another example the Venice team often cites: users buy DIEM, use it for one day of inference, and sell it the next day. If the price is flat, inference is effectively free. If the price rises, the user even profits. The reverse also applies—if the price falls, holders' losses may far exceed the cost of buying inference directly. For some users, this means they can speculate on inference prices while consuming inference.

DIEM can also provide cost certainty. A business or agent with stable predictable demand can use DIEM to lock in its compute costs—the logic is the same as multi-year cloud reserved contracts. It does not know what $1 of inference will buy in two years, but can lock it in now. At a DIEM price of $1,270 on July 7, one DIEM is about four years of one-dollar-per-day credits, so buyers prepay about three and a half years of perpetual cash flow. The question is, buying this certainty means holding a volatile, dollar-denominated perpetual asset—this is exactly contrary to the certainty buyers want. Priced as a perpetual commitment, DIEM implies a double-digit discount rate on Venice's continued service capability, and the value of this claim depends entirely on how long Venice can continue servicing.

This mechanism is still early, with real flaws:

Tokenized inference is most useful for issuers who need to pull demand forward and raise capital. Labs with the best models and real pricing power have little incentive to tokenize, as this sacrifices price discrimination between customers, breakage revenue (unused credits), and flexibility to reprice.

DIEM has no maturity date for holders to recover principal, nor is it backed by collateral or reserves—unlike GPU-backed loans discussed below. It is an open-ended bet that Venice will still provide that $1 years later; if not, there is no covenant or recourse.

DIEM is a claim on what Venice decides $1 of inference can buy, not a claim on a fixed amount of inference. Venice sets token prices for each model, which may fluctuate with demand and availability. The risk is not only the direction of market price, but also discretion between Venice and holders. Models becoming cheaper should mean $1 buys more, but holders only see this if Venice passes the savings down.

Caption: Erik Voorhees's Venice is the project that has gone furthest in turning inference access rights into ownable assets. (YouTube/ReasonTV, CC BY 3.0)

The deeper question is: is this perpetual, dollar-denominated form of DIEM the exposure inference buyers want, or do they prefer a claim with a term, priced in compute or tokens, or both.

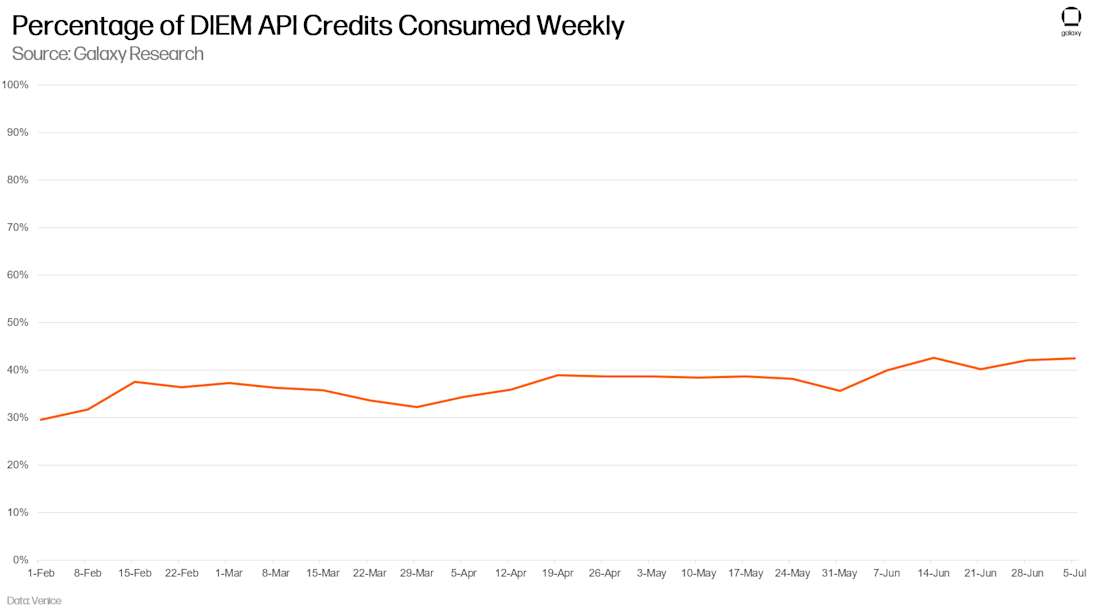

Caption: DIEM Usage Rate and Holder Distribution

Currently DIEM is mainly held as a speculative asset, rather than for inference access—less than 50% of issued amount is used for inference weekly. Venice's own materials call DIEM a "range-bound perpetual asset," dividing buyers into API users, VVV holders extracting value without selling VVV, and speculators arbitraging the spread. The latter two categories make up the largest share of holders. The closest centralized analogy is OpenAI's Scale Tier: prepaid commitment for model throughput calculated per token/minute, purchased for a fixed term. But Scale Tier is not ownable inference—it is account-bound, non-transferable internal capacity on the OpenAI platform. DIEM's advantage is exactly the opposite: it can be held, resold, and combined with the rest of the crypto inference stack. Better tools might combine Scale Tier's term and compute pricing, plus DIEM's ownership and transferability.

For Venice, every DIEM in circulation is $1 of compute it must service and can never sell to others—a liability. This is why it uses revenue to buy back tokens, not to appease holders.

VVV and DIEM are not meant to mimic Venice equity instruments. They were initially as a bootstrapping mechanism to build the platform user base. Today, their value comes from the compute claims they provide. VVV holders, through mintable DIEM, own a perpetual claim on Venice inference—the more Venice grows and its compute becomes valuable, the more valuable this claim becomes. For Venice, every DIEM in circulation is $1 of compute it must service and cannot sell to others—a liability—this is why it uses revenue to buy back tokens. One side owns the claim and wants it to appreciate, the other bears the obligation and wants to manage it. This shared position on Venice compute—rather than any equity interest—is the aligning force, and an interesting attempt at VVV as a utility token mechanism to build an inference business.

Tokenized Inference Production

Venice tokenizes inference access rights, while Proof of Useful Work networks tokenize inference production itself—subsidizing the cost of serving inference with token emissions. Proof of Work guides networks by paying token rewards to people solving arbitrary puzzles—this is how Bitcoin is secured, and why it wastes energy on other things. Proof of Useful Work replaces that puzzle with real inference, so the same compute securing the chain also produces something customers are willing to pay for. Pearl and Ambient are two running attempts, built on opposite designs.

Pearl

Pearl Network is a Layer-1 blockchain forked from the Bitcoin codebase, retaining Bitcoin's UTXO model and difficulty adjustment mechanism, but replacing the SHA-256 hashing algorithm with matrix multiplication—the core operation in AI inference and training. Pearl's claim is that the same matrix multiplication serving customer inference can simultaneously serve as a mining attempt.

When an AI model answers a prompt, the underlying reality is multiplying two large grids of numbers—this is matrix multiplication. Pearl lets miners take these exact grids, slightly scrambling them by adding a layer of random numbers, then multiplying the scrambled version. Multiplying scrambled grids is heavy computation, and this computation is submitted to the mining race. During operation, intermediate results are continuously checked against the difficulty target. If below, the miner wins the block—same rules as Bitcoin, except the work being tested is real model serving computation, not useless hashing in standard mining. After multiplication is complete, a fast final step subtracts the random layer back, leaving the exact inference result the customer wants. So the single multiplication act produces two things simultaneously: real AI output and the chance to win block rewards.

Two design choices make this "killing two birds with one stone" feasible. Pearl is released as a plugin for vLLM—a popular software AI companies already use, suppliers can enable directly without rebuilding systems. Because winning entries must be public for network verification, Pearl wraps them with zero-knowledge proofs, so customer prompts and suppliers' proprietary model weights remain hidden. Overhead is small. Pearl reports running models its way adds 0.5% to 10% extra work, and in its release tests on Llama-3.3-70B, the Pearl version ran as fast or faster than the standard version, because the team's re-engineering of core computation happened to be more efficient than the standard version in certain configurations.

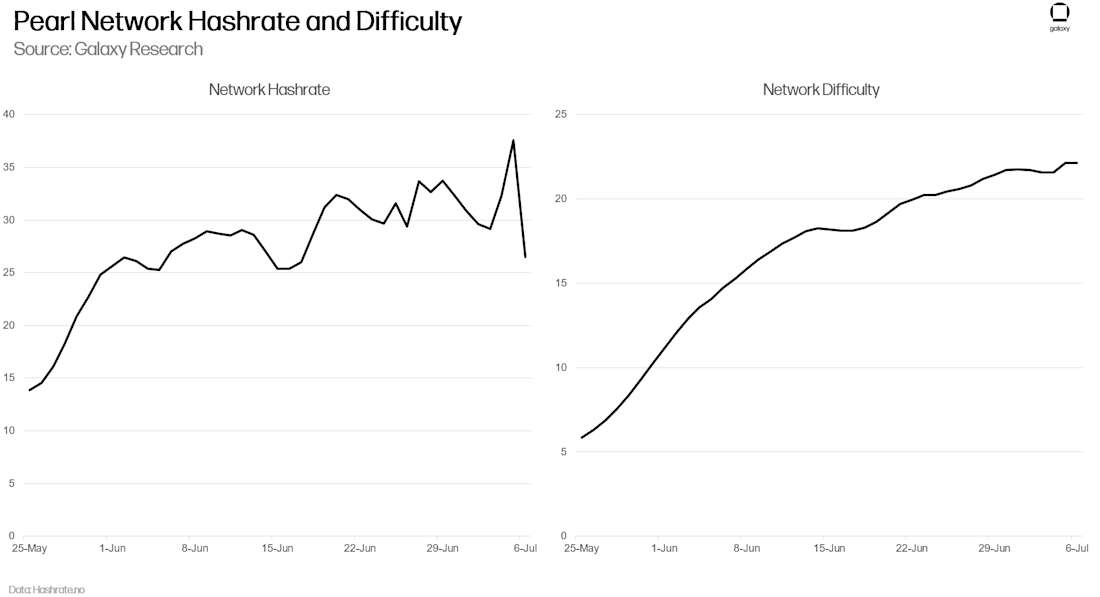

Caption: Pearl Network Compute Growth Trend

As one of the earliest networks combining Proof of Work and inference, Pearl attracted strong miner interest after launch, with compute rising rapidly. But the protocol cannot distinguish useful computation (computation serving real inference requests) from useless computation, because the computation is valid regardless of whether customers want the results. Pearl's whitepaper assumed this, incorporating a group of miners running useless computation purely to earn block rewards in its assumptions. Pearl's launch confirmed this—early mining boom drove rapid compute climb, with almost none serving real inference.

However, there are increasing signs of real-world traction. Most notably, in May Pearl announced a partnership with Together.ai—one of the leading inference and compute suppliers—launching an inference endpoint priced more than 25% lower than Together's standard rate, with the discount funded by Pearl token rewards earned on the same compute. Pearl's dual-use design only produces useful work when real paid inference demand drives compute. Without that demand, block rewards only attract speculative miners, resulting in just a different form of Bitcoin-like Proof of Work, without productive output.

Ambient

Ambient made opposite design choices to Pearl. Instead of letting miners run arbitrary models, it standardizes the entire network to a large open-weight model, and builds consensus around verifying that model's outputs.

Pearl lets miners compete through brute force—everyone racing to solve the same problem—Ambient lets miners compete through auction. Users or agents post an inference task with a deadline and price—essentially "complete this in X minutes, I pay Y"—miners bid to undertake. Winning miners run the query on the network model, posting a bond (forfeited if not delivered on time), guaranteeing quality and speed commitments. A group of randomly selected validators—priority weighted by history of useful work rather than staked capital—then checks the results. Because miners serve many different tasks simultaneously, rather than everyone fighting for one block, the network avoids bottlenecks in traditional Proof of Work. The entire system is a Solana fork, replacing staking with useful work, aiming to run at Solana-level speeds.

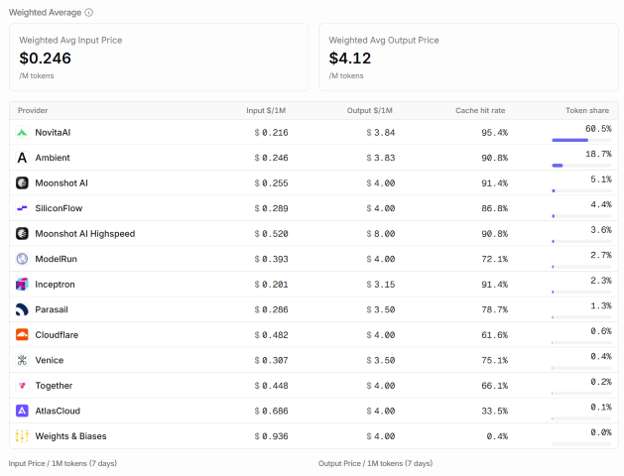

Caption: Ambient is the second cheapest supplier for Kimi K2.7 model input and output tokens on OpenRouter

Auctions are also the mechanism making Ambient inference pricing competitive. Ordinary API suppliers must recover the full cost of serving requests from user payments. Ambient miners can be paid twice for the same unit of work: once from payment by the user or agent who won the task, and once from protocol rewards for verified useful work. Because miners compete on tasks with clear price and latency targets, they should bid at net cost minus expected token rewards, rather than total cost before deduction. In effect, token emissions subsidize the supply side, and auctions force most subsidies to pass to the demand side in the form of cheaper inference. The key difference from general mining subsidies is: rewards attach to tasks someone posts and pays for. If the mechanism works, emissions buy not just compute, but cheaper, verified inference—this attracts more usage, gives miners more work, and strengthens support for network token demand.

Caption: Design Comparison between Ambient and Pearl

This auction is also why Ambient claims to have solved the problem Pearl did not. In Pearl, miners can earn block rewards by running matrix multiplication regardless of whether customers want the output—this is why the network attracted compute not serving real demand. In Ambient, miners only earn tokens by winning tasks someone posted and paid for, so mining and serving real inference are the same act by design.

Ambient also takes a unique approach to inference output verification. If a miner claims to have run your query on the agreed model, how do you know it didn't secretly switch to a cheaper, lower-quality model to save costs? This is a real problem even for today's centralized suppliers—they have been accused of quietly lowering model quality to cut costs. Ambient's answer leverages a characteristic of how language models work. When models generate text, every step produces logits—raw numerical scores for all possible next words before selecting one. This string of scores is actually the fingerprint of which exact model is thinking, and can be hashed into a short number to check.

To check a miner who generated an output of thousands of tokens, validators do not need to rerun the entire task. It picks a random point in the text, asks the miner to provide the fingerprint at that point, then only runs the model at that location to generate one token to see if its fingerprint matches. One token of work confirms thousands. This is similar to Bitcoin—producing work is expensive but checking is cheap. Ambient claims this keeps verification cost overhead around 0.1%, compared to about 10 to 1,000 times overhead for zero-knowledge proof methods other projects attempt.

How "Useful" is Proof of Useful Work Really?

What distinguishes these projects from other decentralized compute projects is: the work securing the chain is the work customers want. When this mechanism works, one unit of energy buys both security and a sellable product. Mining is a second revenue stream on hardware suppliers are already running, and output is verifiable enough for agents to buy inference without trusting suppliers won't lower model quality or cut access.

If there is not enough real demand, block rewards alone can attract miners, and Proof of Work networks are filled with compute serving no customers—formally useful but substantively useless.

Beyond technical challenges, there are two issues between promise and realization. The first is demand. Decentralized inference networks are competing with centralized suppliers and plain GPU rentals—both cheaper, faster, and without attached crypto tokens. To win, there must be buyers wanting trust-minimized forms of inference—verifiable, censorship-resistant, neutral, with no suppliers able to run away. The slice of demand willing to pay for this today is still small, but if these projects prove the ability to provide consistent stable inference at lower cost, or if trust in centralized AI is eroded, it may expand rapidly. Pearl's launch is a warning. Without enough real demand, block rewards alone can attract miners, and networks are filled with compute serving no customers—formally useful but substantively useless.

Caption: Challenges Facing Proof of Useful Work

The second issue is token value accrual. Each project promises a flywheel: real usage drives demand for its crypto tokens → tokens fund mining rewards securing the network → supports more usage. But none have closed it. Mining mints tokens, miners sell to cover costs, but nothing on the demand side forces buyers to acquire tokens, because consuming the actual product—inference or proofs—mostly does not require large-scale use of crypto tokens. Pearl's inference can be paid in dollars, and its proposed future market where tokens will buy compute is itself an admission the loop does not yet exist. Ambient postponed the release of its tokenomics, and did not say whether inference will be priced in tokens. So every token is earned and sold, rather than used.

Most likely, these networks will use their tokens as native payment channels for inference—the obvious way to close the loop. Paired with emission subsidies letting them provide inference below market price, this strategy could be compelling. Cheaper inference attracts real usage, and if payment must be in tokens, usage becomes token demand. But the flywheel only turns positively if adoption持续,organic token demand eventually exceeds emission selling pressure.

AI Inference Hardware Financing

Venice tokenizes inference access rights, Pearl and Ambient tokenize inference production, and below them, a different on-chain market is emerging: financing GPUs required for inference runs. This is the clearest case in this report of crypto doing what it does best—it works precisely because it does not mint tokens or try to guide demand for tokens. It raises capital in conventional ways to collateralize hardware, funneling stablecoin deposits into loans for operators buying GPUs, and repaying depositors from lease cash flows.

The largest operators have already financed their equipment clusters through bank credit lines, asset-backed securitization, and private credit. CoreWeave's billions of dollars in GPU-backed debt is a typical case. Smaller neoclouds are harder—they own hardware, hold contract cash flows supporting loans, but lack the balance sheet, treasury functions, and lender relationships needed to obtain loans quickly. USD.AI lends to them. Depositors fund loans, lease income repays loans, and interest returns to depositors as yield. There are three things banks are hard to match: openness to anyone holding stablecoins on the lender side, rather than closed credit funds; every loan becoming a composable on-chain instrument that can be staked, traded, or used as collateral elsewhere; collateral claims represented on-chain, while still relying on traditional legal enforcement.

Caption: USD.AI Operating Mechanism

USD.AI runs on two tokens. Depositors mint USDai—a synthetic dollar backed by PayPal's PYUSD (PYUSD is in turn backed by U.S. Treasuries and cash). USDai does not pay yield, aiming to maintain liquidity and composability. To earn yield, depositors stake it as sUSDai, whose value grows as positions receive rewards. Yield comes from two places: active loan interest paid by GPU borrowers, and Treasury yield on idle reserves during deployment intervals. With the loan book at about half of reserves, staking yield is about 8%, with the protocol target reaching 10%-15% as more capital is deployed.

Caption: USD.AI Loan Process

The difficulty in lending against physical GPUs as collateral is how to enforce claims when borrowers default. USD.AI once recorded each financed GPU as an ERC-721 NFT, describing it as a legal title instrument under Uniform Commercial Code Article 7, with borrowers holding machines under a bailee arrangement, and NFTs as collateral. It called this framework CALIBER. The protocol later abandoned it, finding it created too much commercial friction. Now NFTs represent loan records—they carry terms of service and route repayments on-chain, but do not themselves transfer legal claims to collateral. Enforcement proceeds through conventional off-chain loan documents, with physical recovery still relying on the operational stack any hardware lender would rely on: physical inspection, proof of installation, collateral monitoring, lien filing, and data center or custodian cooperation. This enforcement path and the protocol's broader model have not undergone full distressed asset recovery testing.

A liquid token backed by 3-year amortization loans has asset-liability mismatch. Most RWA credit protocols mask it by promising instant redemption, then collapse under pressure—USD0++'s depeg is an example. USD.AI does not promise instant exit. Redemptions are liquidated over a 30-day cycle, based on amortized principal, first-come-first-served. The protocol will not liquidate a running loan to fund withdrawals. A pricing queue borrowing from Flashbots MEV-Boost design covers the top, letting redeemers wanting to skip the queue bid for priority, with fees routed to waiting holders. Loan terms are similar to CMBS: 70%-80% loan-to-value ratio, borrower reserves covering about three months of debt service, liquidation after two missed payments, hardware insured, monitored, and recoverable via specialized partners.

USD.AI belongs in this report because it connects the credit layer with the pricing layer. Lenders financing GPUs must mark their collateral according to some standard: how fast hardware depreciates, how much it can sell for in forced sale, what advance ratio is safe, how to hedge residual value. Compute indices and forming futures give lenders this reference, and lenders in turn provide real credit exposure, giving those prices use beyond speculation. GPU lenders need to know not the spot lease price on a given day, but how much this machine can resell for when the loan defaults—liquid indices and futures curves can ultimately determine this.

Caption: Connection between GPU Credit and Compute Pricing Layer

USD.AI states about 95% of its loan book is secured by long-term offtake contracts rather than spot leases, so borrowers' debt service ability depends more on counterparties pre-committing to capacity than on daily lease prices. Two things now stand between that risk and depositors. The protocol de-risks each loan quickly—70%-80% loan-to-value ratio plus pre-funded three months debt service reserves brings effective LTV at issuance down to over 60. USD.AI says about one-quarter to one-third of loans are repaid in the first year, so it recovers much exposure before hardware value drops significantly. Fast depreciation—usually feared—is favorable to lenders as long as amortization outruns it. Second, every new loan now comes with Barkr value loss insurance, its AI-driven collateral valuation guaranteed and reinsured by Munich Re (reinsurer with A+/AA- rating). If a loan defaults and collateral sells below Barkr's assessed value, the difference is paid to the protocol. Given the 80% LTV cap, USD.AI describes this as full coverage on outstanding debt.

Insurance changes risk but does not eliminate it. It passes residual value risk to a strong counterparty, but also concentrates new dependence on Barkr's valuation model and reinsurance continuing effectiveness—coverage and USD.AI's off-chain enforcement have not been tested by a real wave of defaults. Loans still amortize over 3 years, versus claimed 7-year effective life, faster hardware cycles will narrow this gap. The difference from months ago is, a distressed liquidation is now borne by the insurer first, before falling on depositors.

Conclusion

Caption: Inference Capital Market Overview and Outlook

Currently, the inference capital market—on-chain and off-chain—is still small relative to the AI industry's growth. For on-chain products to scale, they must prove the advantages they introduce are sustainable and lasting.

Those advantages are clear. Tokenized access rights (Venice) turn claims on inference into bearer assets holders can retain, resell, lease, or hand to agents, rather than subscriptions bound to an account a supplier can revoke. Proof of Useful Work (Pearl and Ambient) subsidizes inference with token emissions to below market cost, and makes outputs verifiable, letting buyers pay without trusting suppliers won't swap models. Financing (USD.AI) turns illiquid GPU credit into composable instruments anyone holding stablecoins can fund and exit, faster than the traditional credit industry. Under all three, the entire stack is permissionless and programmatic—this is the form most naturally suited for consumers like agents that may drive most demand for on-chain capital market inference. Crypto is used where ownership, neutrality, composability, and capital access matter.

Resistance to adoption is not small. No one has connected real demand for compute with real demand for crypto tokens. Production networks mint tokens and sell them, using emissions to fund below-market inference—emissions are sold immediately after being earned. Trading of tokenized access rights is based more on speculation on issuers than usage, DIEM is mainly held by speculators, priced as a bet on Venice rather than inference. Financing is the exception—the only form with real customers: neoclouds needing capital and having cash flows to repay—so its yield comes from served demand, rather than tokens minted to guide interest. So far, the financial layer has been more successful at attracting speculative capital than generating self-sustaining, usage-driven demand.

The true advantage of the on-chain inference capital market in continuous AI infrastructure lies not in competing with established enterprises in what they do best—serving inference at low cost at scale. But in forming capital and reaching markets traditional finance is too slow, too small, or incapable of serving. This is the pattern crypto keeps rediscovering—it rarely wins on products, exchanges, models, or applications themselves, but it repeatedly becomes the fastest way to build financial layers around these, whether pricing assets, fragmentation, financing, or settlement.

Inference is the latest and largest instance. A trillion-dollar asset class is assembling in real time, and the market structure for compute as a financial asset—indices, futures, credit, tokenized capacity—barely exists yet. This absence is opportunity. The financing layer works today because it is the first part of this structure to find real demand, and the rest of the stack is a bet: the same advantages will extend upward as compute itself financializes.

Inference markets may take years to mature, but the financial layer built around them is forming now.

Update (July 15): The section on USD.AI has been updated to reflect changes in the protocol regarding enforcement of claims on defaulted loans.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News