BUIDL and Aladdin, BlackRock's Hidden Main Thread Penetrating On-Chain Finance

TechFlow Selected TechFlow Selected

BUIDL and Aladdin, BlackRock's Hidden Main Thread Penetrating On-Chain Finance

When DeFi's collateral and risk benchmark belong to the same giant.

Written by: Thejaswini M A

Compiled by: Saoirse, Foresight News

In a game, the venue holds supreme weight. Teams win and lose, and the trophy changes hands every year. But if you own the arena and set the rules of competition, then no matter who ultimately wins the championship, every match plays out on your turf, and everyone must pay you rent.

This is the layout BlackRock is currently making in the crypto field. However, when mentioning BlackRock, most people only think of ETFs. BlackRock launched a Bitcoin ETF, absorbing tens of billions of dollars in funds. Media outlets around the world competed to report that the traditional finance giant was finally making a major entry into the crypto industry. This description is not false, but the ETF is merely a bait.

An ETF is just a trading product. Investors can buy and sell it; it is no different from the rest of the index funds in a brokerage account. Even if the BlackRock Bitcoin ETF disappears tomorrow, the crypto market will continue to operate as usual without suffering any fundamental damage. Today, we focus on dismantling the real core: the entire BUIDL layout strategy.

BUIDL: Seemingly Safe Underlying Collateral, Hiding Centralized Shackles

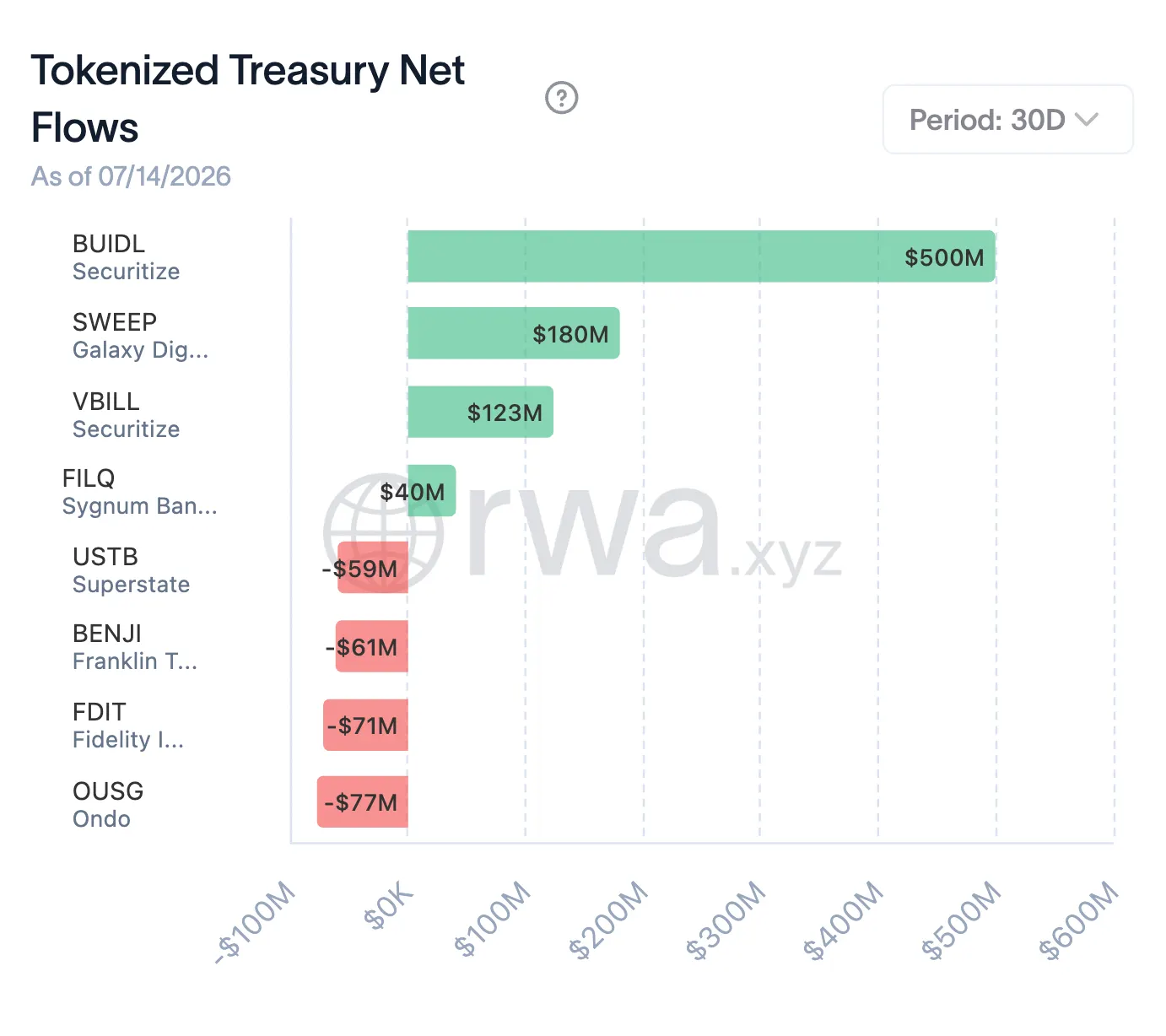

BUIDL is a tokenized money market fund launched by BlackRock. The underlying assets are short-term US Treasury bonds and cash. The assets are split into on-chain tokens, allowing holders to earn yields directly. The product launched in 2024 with an initial size of approximately $2.5 billion. At first glance, the volume is not large, but it is evolving into a force not to be underestimated.

BUIDL holds Treasury bonds as underlying assets; the assets themselves belong to top-tier safe assets. The risk does not lie in the underlying target, but in the permission rules for asset entry and exit: BUIDL is a permissioned asset. Only wallets approved by BlackRock and its partner Securitize can hold or transfer them; whitelist permissions are completely controlled by BlackRock. Investors can only redeem during specified periods according to terms set by BlackRock. Whether BlackRock's compliance department actively marks an address or regulators pressure them, BlackRock has the right to freeze wallets and suspend redemptions.

Ordinary crypto tokens can be transferred freely at any time without intervention; but BUIDL carries the risk of a single entity shutting down liquidity. This is the root of the risk; all products built on top of BUIDL will inherit this hidden danger together.

Nowadays, BUIDL is gradually becoming the collateral on which on-chain finance relies to build. What this article explores is precisely this silent takeover of underlying sovereignty.

Penetration and Implementation: Stablecoins and Exchange Margins Successively Access BUIDL

First, let's look at Ethena and USDe. USDe is currently the third-largest synthetic dollar stablecoin by market cap. Ethena also issues another dollar token, USDtb, over 90% of whose reserve assets are BUIDL. Whenever the market fluctuates violently and the USDe mechanism is under pressure, USDtb is the shock absorber it relies on to buffer risk. In other words, BlackRock's Treasury bond assets are already located at the underlying layer of the top dollar assets in the crypto market.

A few weeks ago, the layout went a step further. Ethena issued various stablecoins via white-label for third-party enterprises, and BUIDL became the core reserve asset for these customized stablecoins, running through the entire product line.

Objectively clarify the dependency relationship: During stable market periods, USDe rarely uses BUIDL. USDe mainly relies on crypto assets superimposed with short futures to build reserves, with only about 7% of funds allocated to conventional stablecoins (including USDtb). USDe's circulation scale is as high as $6 billion, but only $65 million to $80 million of own reserves are reserved to defend against losses. When carry trade yields disappear, the meager own buffer funds are insufficient to cope with risks, and Ethena can only transfer funds into this Treasury bond fund on a large scale to seek shelter.

In times of crisis, BlackRock assets will become the final load-bearing cornerstone. The most dangerous situation is nothing other than: waiting until the market crashes, only to discover that the control over the underlying assets is in someone else's hands.

Since April, OKX's institutional large clients can use BUIDL as trading margin to secure positions. The tokens are custodied by Standard Chartered, and idle margin can continue to generate Treasury bond yields. It is the first time that a traditional large bank of such scale has participated in such crypto business. Idle margin becomes an interest-bearing asset, and this asset is precisely the BUIDL issued by BlackRock.

Aladdin Lists USDe: Controlling Full Market Risk Data and Pricing Power

A few weeks ago, BlackRock integrated USDe into the Aladdin system.

Aladdin is BlackRock's self-developed risk management platform, used to monitor various investment portfolios and simulate potential risks. Do not mistake BlackRock's integration of USDe as supporting the crypto industry. The real purpose is to use this system to grab data inside the on-chain financial system, risk exposure structures, and operational logic, all summarized into BlackRock's own data hub.

BlackRock uses this to figure out the leverage levels of various parties in the market, accurately predicting at which point price declines will trigger large-scale forced liquidations. Once a sell-off market trend starts, BlackRock knows in advance how the dominoes will fall one by one. Even if crypto project founders believe they are operating independent protocols, ultimately they have to adopt BlackRock's exclusive model to measure risk.

USDC, the second-largest stablecoin with a market cap of approximately $78 billion, also has the vast majority of its cash reserves managed by funds under BlackRock.

The complete risk chain has already taken shape: traders hold USDe, USDe risk buffering relies on USDtb, and the vast majority of USDtb's underlying is BUIDL; traders also use USDe for collateralized lending, starting a new round of speculation. Collateral is hidden in the underlying foundation, with various leveraged loans stacked layer upon layer on top. All market participants default to the underlying assets being able to be redeemed stably and freely. Once the underlying asset channel closes, everyone will encounter a liquidity crisis simultaneously.

History Repeats: BlackRock's Mature Playbook for Achieving Monopoly Through Underlying Infrastructure

Ethena's cooperation has the highest exposure, but several other exchanges have also successively accepted various tokenized Treasury bonds as margin, including BlackRock's BUIDL and competing products such as Franklin Templeton. At this stage, BUIDL is the largest target in the track. Funds naturally gather towards assets with optimal liquidity, continuous funds flow into head products, and the Matthew Effect continues to strengthen.

BlackRock has long replicated this playbook and has succeeded repeatedly. Index funds were ordinary in the early years, regarded as "plain water products" in investment. BlackRock relied on iShares index funds to sweep the global market. Today, the three index giants BlackRock, Vanguard, and State Street have become major shareholders of nearly 90% of S&P 500 component companies. They do not need to stand in front of the stage; they only need to take root in the underlying layer and wait for massive funds to continuously pour in.

At the operational level, Aladdin repeats the same story. This risk control system covers asset scales exceeding $20 trillion, accounting for approximately one-tenth of total global financial assets. A large number of financial institutions competing with BlackRock still pay to use this system for risk control. It equals competitors relying on BlackRock's algorithms to assess their own safety bottom lines, allowing BlackRock to see through all the market's cards.

The 2008 financial crisis and the 2020 COVID bond crisis fully exposed potential conflicts of interest: the US government entrusted BlackRock twice to dispose of crisis assets and execute market rescue plans, and a large amount of rescue funds ultimately flowed into BlackRock's own products. Issuing underlying collateral assets on one hand, and operating asset pricing risk control systems on the other — this is precisely the pattern BlackRock now wants to build in the crypto industry.

Ultimate Vision: Becoming the Underlying Operating System of the Crypto World

If various tokenized dollars continue to use BUIDL as underlying reserves in the future, DeFi continuously deposits funds here, and market risks are uniformly handed over to Aladdin for calculation and pricing, BlackRock will become the underlying operating system of the crypto world.

Why is this matter far more important than ETFs? ETFs and collateral have essential differences. ETFs only represent investment demand: investors buy if bullish and sell if bearish; trading behavior does not impact the foundation of the entire system. Collateral is the exact opposite. Once various stablecoins and lending protocols choose BUIDL as underlying support, wanting to withdraw will be exceptionally difficult. Withdrawing underlying collateral means dismantling all lending and leveraged positions built on top of this asset, easily inducing a systemic collapse. Therefore, the market will passively continue the status quo, not daring to easily replace the underlying cornerstone. ETFs can be liquidated at any time, but no one dares to rashly remove the foundation while the entire system is operating normally.

Currently, it is still in the early stage. BUIDL with a scale of $2.5 billion is negligible compared to the over $300 billion stablecoin market volume; the stablecoin market share is mostly occupied by Tether and Circle. Measured by current data, BlackRock does not yet count as the market foundation.

Realistic Trade-offs on Both Sides

Optimistic perspective: Multiple collapses in the history of the crypto industry had their root cause in inferior tokens collateralizing each other. Building synthetic dollars based on US Treasury bonds custodied by globally renowned institutions can reduce risks and enhance industry credibility.

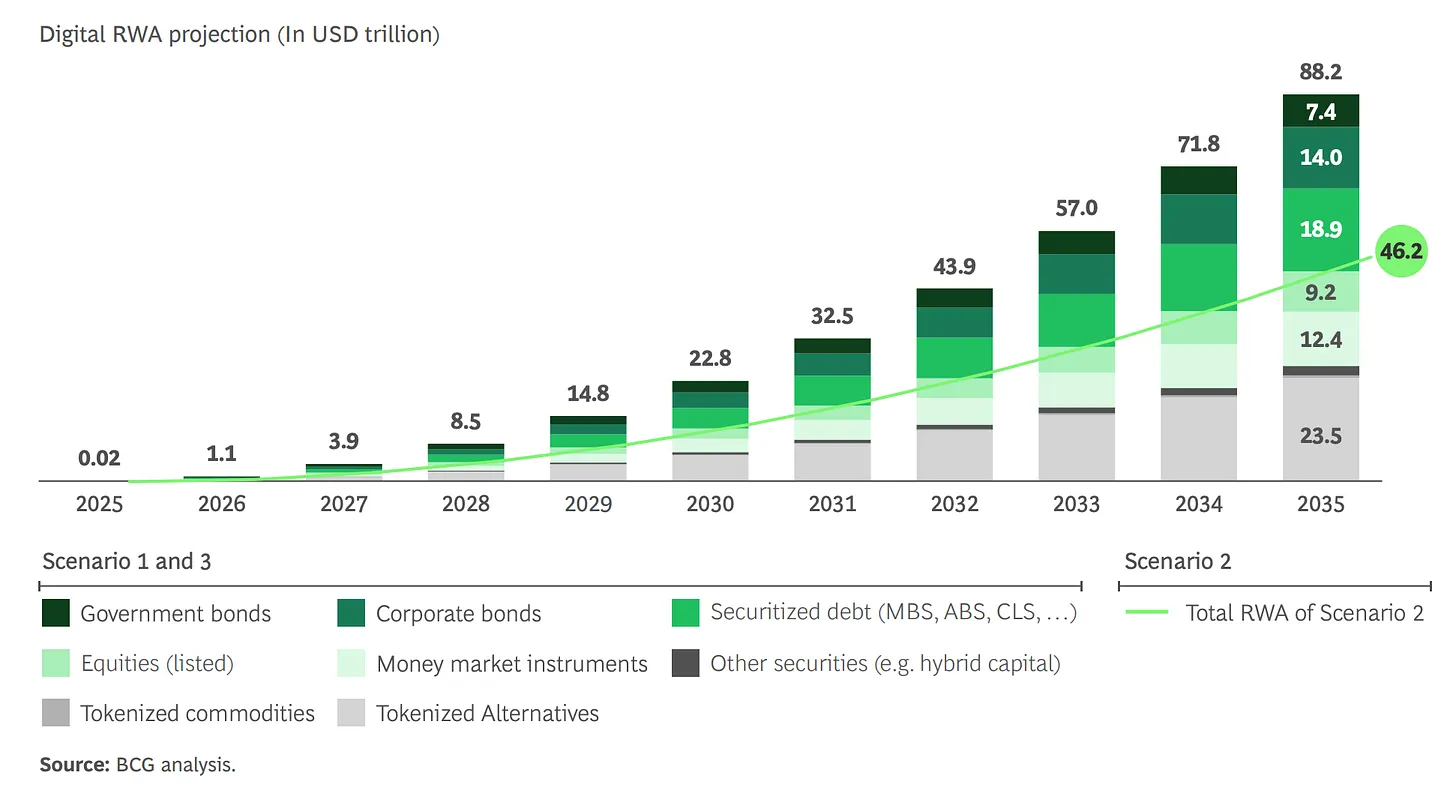

Warning perspective: First, the evaluation standard should not only look at asset scale, but also at the layer where the asset resides. Compared to assets with huge volume but no one relying on them, underlying assets with smaller scale but deeply bound by dozens of upper-layer products have greater influence. Boston Consulting predicts that the tokenized real-world asset market is expected to reach $16 trillion in the 2030s, and BUIDL is seizing the underlying base position. Second, this is an exchange of power: exchanging for asset stability, handing over underlying control rights. Stable yields are visible intuitively, but the risks of power concession are difficult to detect in the short term. And BUIDL from start to finish is a permissioned asset that follows BlackRock rules, relies on whitelist access, and has redemption permissions centrally controlled.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News