Research Report Analysis: SOX Surges 88% in Single Quarter, Yet JPMorgan Signals Deleveraging

TechFlow Selected TechFlow Selected

Research Report Analysis: SOX Surges 88% in Single Quarter, Yet JPMorgan Signals Deleveraging

For investors, what truly needs to be closely watched over the next two months is the capital expenditure guidance during earnings season and the pace of storage price hike realization; this is the real switch determining whether positions will reverse.

Written by: Rita

TechFlow Insights

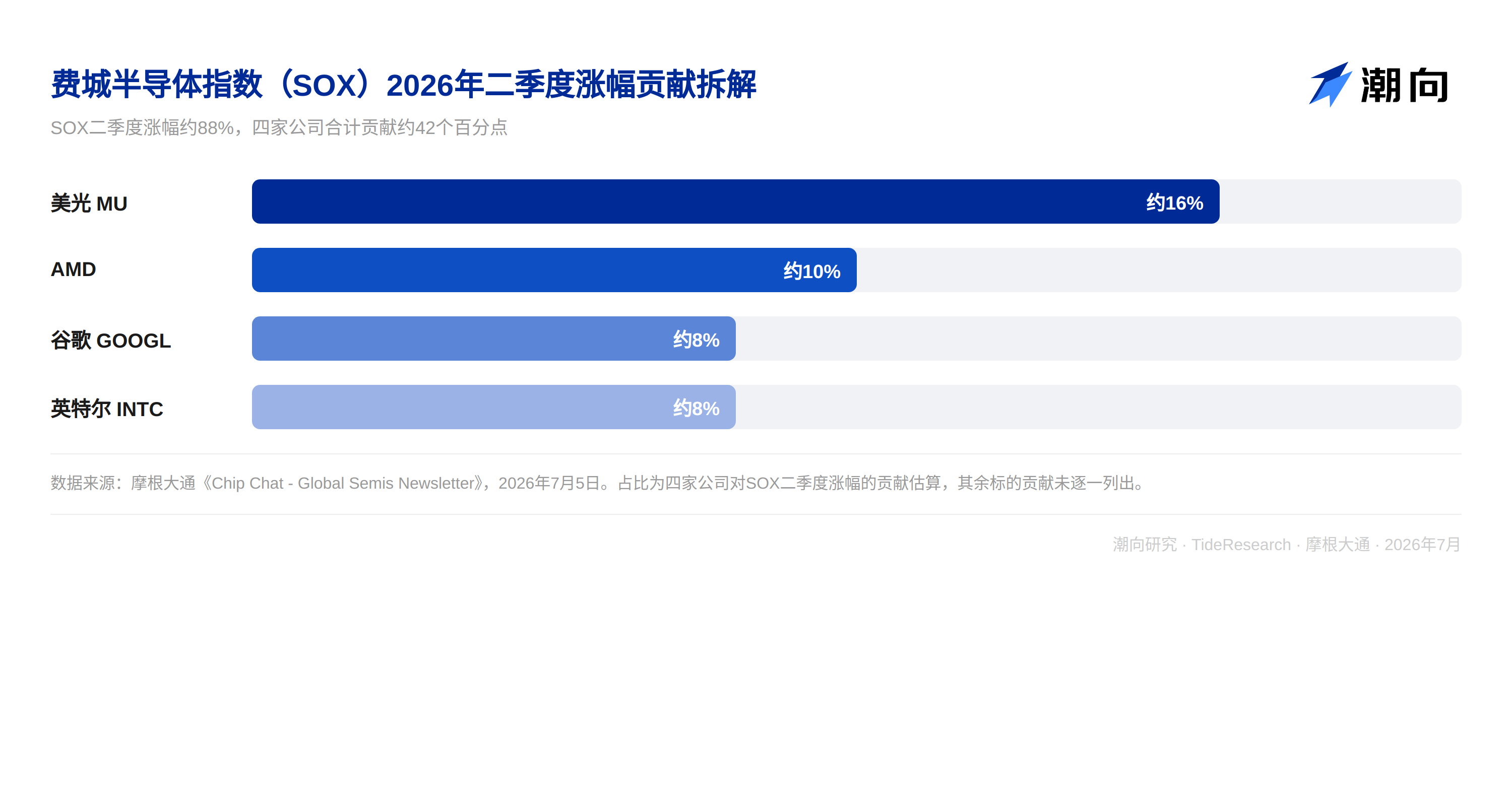

Q2 just concluded, and the Philadelphia Semiconductor Index (SOX) surge approached 88%, creating the strongest single-quarter performance since the index's inception. Micron, AMD, Google, and Intel contributed approximately 16%, 10%, 8%, and 8% of the momentum respectively, accounting for nearly half of the strength in this rally. J.P. Morgan Global Market Strategist Nikolaos Panigirtzoglou gave an unwelcome judgment in the latest issue of Chip Chat Global Semiconductor Weekly Report: the nearly stable outperformance of semiconductors relative to hyperscale cloud providers has continued since last September, which looks somewhat unsustainable in the long run, unless earnings realization and AI monetization speed truly catch up, or cloud providers' capital expenditure growth rate indeed slows down.

What's more worth watching in the report is positioning rather than price. Crowded long positions in hardware and semiconductors once outperformed crowded short positions by nearly 40 percentage points in June, the strongest performance in at least four years. Hedge funds' overall return in June reached 4.2%, cumulative year-to-date 11.1%. But entering July, momentum factor positions have retreated about 17% from the high on June 22, signs of deleveraging are beginning to appear, net selling has occurred for three consecutive days in the North America direction, and overall US stock positioning has fallen from the 60th percentile at the end of May to around the 40th percentile at the end of June.

Up 88% in a Quarter, What Are Institutions Worried About

The same divergence can be seen in the options market. Throughout the second quarter, the phenomenon of individual stocks and options becoming more expensive simultaneously was rare, also one of the most profitable trades this season. Investors bought volatility in the storage and memory sectors while selling volatility in hyperscale cloud providers. J.P. Morgan believes the market has already priced quite a lot of AI optimism into long-term options in advance; these options currently appear expensive, and this forms the natural hidden danger of this round of semiconductor trades.

The derivatives trading desk, which usually only discusses macroeconomics and hardly touches individual stock positions, gave specific advice this time: buy two-month puts, sell six-month calls. The targets directly point to memory, storage, optical communication, and semiconductor equipment, these AI-benefiting sectors with the largest gains earlier. Once such teams enter the field to make specific targets, it is itself a signal.

Divergence Hides in Details, Specific Numbers for ASML and Storage

Divergence at the individual stock level is clearer than macro narratives. Regarding ASML, buy-side models are already modeling 2028 Earnings Per Share (EPS) of 60 to 65 euros. J.P. Morgan analyst Sandeep Deshpande's figures are 54.4 euros for 2027 and 64.4 euros for 2028. The core controversy has shifted from whether to hold ASML to what can drive the stock price higher. The answer points to whether EUV equipment demand from 2027 to 2028 can be verified. The market is currently modeling around 90 to 100 units for 2027 and around 110 units for 2028. Any statement lower than these numbers may cause expectations to fluctuate.

Capital expenditure forecasts for storage and foundry directions have also been revised upward. J.P. Morgan raised the storage capital expenditure forecast from FY26 to FY28 from $300 billion to $450 billion. Tokyo Electron is listed as the top choice, reasoning that its share in DRAM etching equipment is expanding, and Yen pricing gives it more room for price increases relative to US peers. Regarding TSMC, the market expects N3 pricing to increase by 10% in 2027. The high end of the gross margin guidance range for Q2 is 67.5%, but buy-side investors are generally betting on the higher figure of 68% to 69%. The storage sector is also diverging internally. Kioxia's 10-day implied volatility has surged above 150, Samsung is close to 130, but hard drive targets like Western Digital have instead become the institutional long preference. SanDisk is one of the targets with the largest decline within the month, falling over 23%.

Similar pricing divergence can also be seen in the European list. Besides ASML, Infineon is given a buy-side range of 3.6 to 4.75 euros for 2028 EPS. STMicroelectronics' target price was raised to 71.5 euros, corresponding to 2028 EPS of 3.68 to 4.48 euros under three scenarios. Nokia continues to be bullish by J.P. Morgan after retracing about 20% from its high, reasoning that the market underestimated the visibility of realization for its AI network business. Looking at these numbers together, the divergence between buy and sell sides for ASML is the most direct. The sell side gives 54.4 to 64.4 euros, while the buy side has already modeled 60 to 65 euros. Ratings for STMicroelectronics and Infineon are relatively stable, but the buy-side expectation range for Infineon's 2028 EPS is also more optimistic than the company's guidance, indicating that the trust the market places in advance regarding the realization for these European names is greater than the guidance provided by the companies themselves.

TechFlow Perspective

The signal most easily overlooked in this weekly report is that the derivatives trading desk, which usually only looks at macroeconomics, rarely gave specific short volatility suggestions targeting storage, optical communication, and semiconductor equipment. Once such teams start entering the field to judge individual stock directions, it usually means market divergence on short-term trends is large enough to require options hedging; simple addition or reduction of positions is no longer sufficient. Another contradiction is also worth dissecting. Buy-side modeling for ASML and STMicroelectronics 2028 EPS is generally higher than the sell side, betting on capital expenditure confirmation and capacity utilization realization. Once foundry or storage customers' capital expenditure guidance falls short of expectations, the room for retreat in such priced-in optimistic expectations is not small. J.P. Morgan's own strategists also admit that the continuous outperformance of semiconductors relative to hyperscale cloud providers from last September to now has appeared somewhat unsustainable, unless earnings realization speed truly accelerates. For investors, what truly needs close monitoring in the next two months is capital expenditure guidance during earnings season and the rhythm of storage price increase realization. This is the real switch for whether positions reverse or not.

Disclaimer

This article is a compilation and interpretation by TechFlow Research of third-party brokerage research reports. The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the brokerage analysts, representing only their affiliated institution's stance, not representing the views of TechFlow Research, nor constituting any investment advice.

The market carries risks; decisions must be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News