TSMC CoPoS's "Glass Myth": Three Illusions Personally Debunked by Core Supply Chain Insiders

TechFlow Selected TechFlow Selected

TSMC CoPoS's "Glass Myth": Three Illusions Personally Debunked by Core Supply Chain Insiders

Glass substrates are not a scam; it's just that the market has prematurely hyped the 2030 industrialization story into the certainty of 2026.

By: ChaoXiang Research

Over the past month, the sexiest narrative in the global semiconductor market has been "TSMC CoPoS + Glass Substrate".

At the shareholders' meeting on June 4, TSMC hinted that the pilot production line has been built. On June 11, slides leaked from the Japan JPCA Show revealed collaboration with Ibiden and Innolux to verify glass core carriers. On June 16, cooperation details were officially disclosed. A series of signals injected into the market like catalysts sent Taiwan tech stocks, A-share glass substrate concepts, and even Corning ($GLW) across the ocean into a collective state of frenzy.

On July 3, cold water arrived.

Anger from the Supply Chain

The Taiwan tech media "Tech Taiwan" published an exclusive report based on interviews with multiple core figures in the TSMC CoPoS supply chain. The interviewees' emotion was not "clarification," but "anger." Some said their "blood pressure spikes" every time they saw false rumors in the market, while others straightforwardly said they were "furious."

There are only two core pieces of information they want to correct: TSMC's first-generation CoPoS likely did not adopt glass substrates in its technical route; TSMC never considered glass interposers.

These two pieces of information fundamentally contradict the "glass substrate as the core of CoPoS" narrative that has flooded the market over the past month.

SemiWiki simultaneously reposted this exclusive report with a straightforward title, "Why TSMC's First-Generation CoPoS May Be Glass-Free".

The report also disclosed that Samsung Electro-Mechanics (SEMCO), Toppan, and other Japanese and Korean substrate manufacturers have joined the R&D race for glass core substrates and recently began submitting engineering samples to TSMC. In other words, supply chain competition for glass core substrates is indeed heating up, but this is "preparation for war" rather than "going live."

What Exactly Did the Market Confuse?

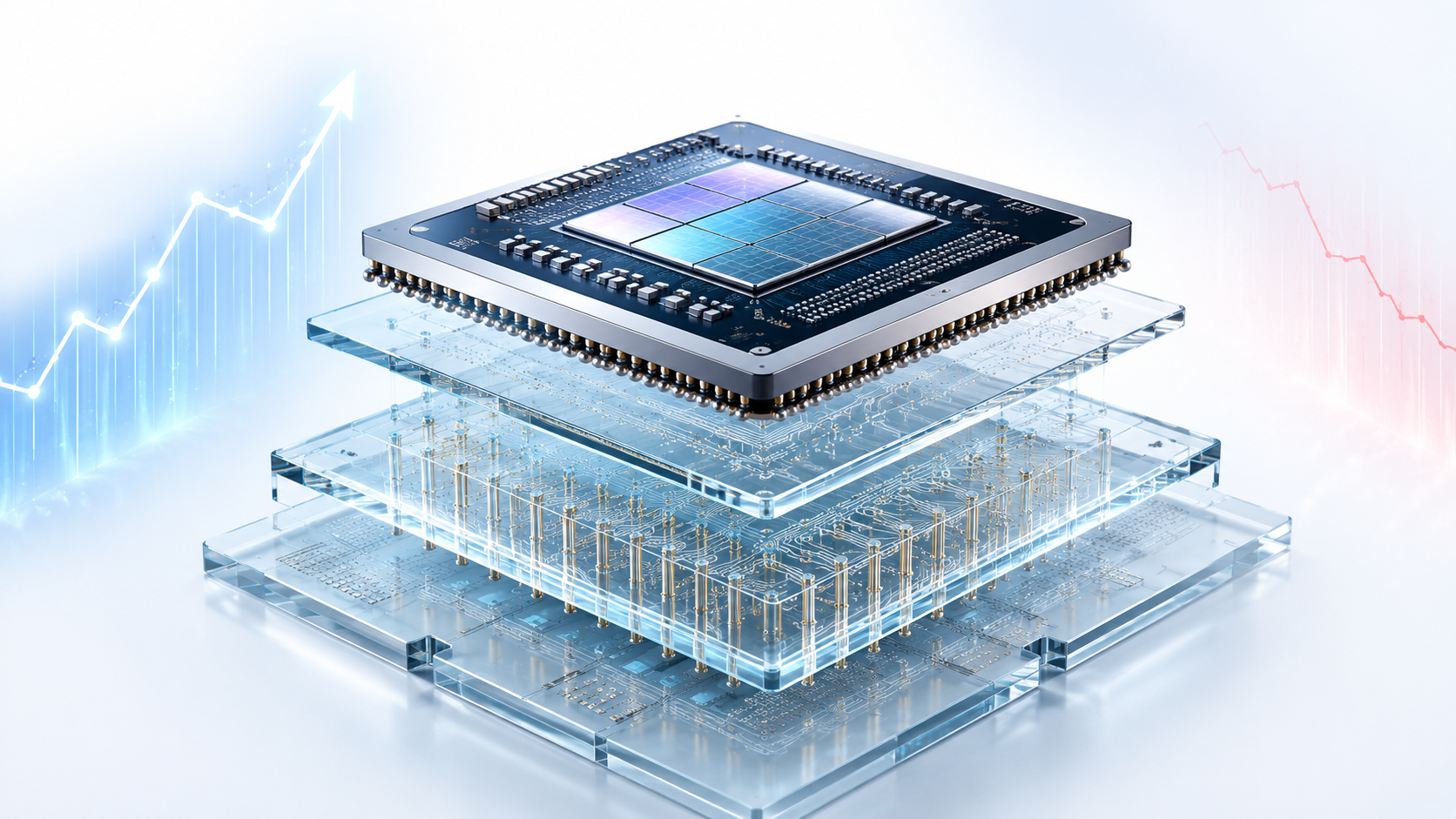

The reason this news is damaging lies in the fact that most market participants cannot distinguish that the word "glass" in packaging appears in three completely different positions, corresponding to three completely different technical routes, value amounts, and introduction timelines.

Glass Carrier (Glass Carrier) is a temporary support plate that holds the chip and RDL through the manufacturing process and is then removed, not remaining in the final product. This is like scaffolding at a construction site—removed once the building is complete. CoPoS is indeed using 310×310mm glass carriers, which all sources confirm, but this glass has low value and is not the thing the market is hyping.

Glass Core Substrate (Glass Core Substrate) is the carrying substrate at the bottom layer of the packaging structure, located below the interposer, responsible for mechanical support and connection to the PCB. Ming-Chi Kuo's industry survey on June 11 described its structure: glass as the core layer, covered top and bottom with ABF build-up layers, forming a sandwich structure. The technical challenges of TGV (Through Glass Via) drilling and copper filling refer to this layer. This is the high-value segment the market is truly hyping, and also the object of verification in the collaboration between TSMC, Ibiden, and Innolux.

Glass Interposer (Glass Interposer) is located between the chip and the packaging substrate, undertaken by the silicon interposer in the traditional CoWoS architecture, responsible for high-speed interconnection between GPU and HBM. Some understand CoPoS as "using glass to replace the silicon interposer," but Ming-Chi Kuo explicitly listed this common error on June 11: "CoPoS adopts a glass interposer" is the most typical market misinterpretation. In the CoPoS architecture, this interconnection role is jointly undertaken by the RDL layer on the chip side and the TGV/ABF build-up layer on the glass core carrier side. TSMC has never placed glass in the interposer position.

Three types of glass, three positions, three completely different investment logics. The market stirred them into a mess, then slapped a unified label on this mess: "Glass Substrate Concept Stocks."

Cross-Verification: What Do Various Sources Say?

Arranging the key sources from the past month, a clear timeline emerges.

TSMC CEO C.C. Wei confirmed at the shareholders' meeting on June 4 that the CoPoS pilot production line has been built, and production is expected to reach a considerable scale in 2-3 years. This statement points to 2028-2029.

Ming-Chi Kuo gave a more specific judgment on June 11: CoPoS is expected to mass produce in the second half of 2028, and NVIDIA's Feynman AI chip may be the first adopter. He described in detail the two usage positions of glass in CoPoS, temporary carriers and glass core substrates, and corrected three common misconceptions.

On June 16, Ming-Chi Kuo further interpreted the slides leaked from TSMC at the Japan JPCA Show and proposed a key judgment: In CoPoS, the importance of oS (substrate) is higher than CoP (panel). CoP solves production efficiency and cutting economics, it is a "very good optimization option" (very-nice-to-have); oS solves warpage and durability, it is a "necessity" (must-have). He positioned the glass core carrier as TSMC's "must have" and pointed out that besides NVIDIA, two US clients have already expressed high interest.

TrendForce's research report on June 17 gave a key time difference ignored by the market: the mass production node for CoPoS itself is pilot production in 2027 and mass production in the second half of 2028; but the commercial scale production of glass core substrates "may not be until after 2030."

This means there is a 1-2 year window between the mass production of CoPoS and the introduction of glass core substrates. In this window, the first generation of CoPoS is entirely likely to continue using traditional organic substrates as a transition solution.

Tech Taiwan's supply chain leak on July 3 aligns perfectly with TrendForce's timeline.

$GLW: Is the Plunge a Coincidence or a Omen?

Corning ($GLW) plummeted 13.3% in a single day on July 1, and fell another 10.8% on July 2, sliding all the way from a 52-week high of $271.78 to about $197. Over the past year, this stock has risen 391%, with a TTM P/E ratio exceeding 105 times.

It needs to be pointed out that Tech Taiwan's report was published on July 3, later than GLW's two-day plunge. The direct triggering factors for GLW's recent decline are more likely: passive buying exit triggered by FTSE Russell index reclassification, large-scale selling by executives in June (cashing out over $54 million within three months), and profit-taking triggered by the extremely stretched valuation itself.

But narrative-level risks are accumulating. Corning has been labeled by the market as "AI Glass Substrate." Institutions predict 2026 to be the first year of glass substrate commercialization, with a global market size of about $18.6 billion, and the compound growth rate may reach 67% after 2028. If the first generation of CoPoS does not use glass core substrates at all, then the realization time for the parts of these predictions strongly bound to CoPoS will be significantly delayed. For a stock with a PE over 100 times, the difference in pricing between delaying realization by one year and by two years could be 30% or even more.

At the same time, it needs to be seen that Corning has strong business support outside of semiconductor packaging: the optical communication business benefits from fiber optic demand in AI data centers, recently securing a multi-year fiber optic supply agreement with Amazon; its "Glass Bridge" optical interconnect component cuts into the CPO (Co-Packaged Optics) track. These business lines are a different matter from CoPoS glass substrates. GLW's valuation bubble is its own problem and cannot be simply attributed to the "glass substrate narrative bursting."

What Is This News Really Saying?

Setting aside emotional expressions, the signal conveyed by Tech Taiwan's report is actually much milder than it appears on the surface.

It did not say "glass substrates are a scam." Quite the opposite, manufacturers such as Samsung Electro-Mechanics and Toppan are submitting engineering samples of glass core substrates to TSMC, which itself indicates that the industrialization process is accelerating.

What it says is: "One step later than you thought."

The core value of the first generation of CoPoS lies in "squaring the circle," increasing the material utilization rate of 12-inch circular wafers from less than 70% to over 90% for square panels. This itself does not depend on glass. Glass core substrates solve warpage and signal integrity issues, allowing CoPoS to run better on ultra-large size packaging, but are not a prerequisite for "whether it can run."

For investors, what really needs to be split are three completely different logics: glass temporary carriers are already in use, low value, do not constitute an investment theme; the equipment supply chain for CoPoS panel-level packaging is in the 2026-2027 verification period, highest certainty, is the most direct benefit segment in the near term; the introduction cycle of glass core substrates spans 2028-2030, highest value, but TGV yield remains a chokehold problem, belonging to medium-to-long term layout.

The market's problem is not looking in the wrong direction, but discounting 2030 revenue into 2026 stock prices. In the semiconductor business, the gap between pricing two years early and realizing one year late is enough to kill a significant rise. Conversely, when the market compresses the timeline too short due to panic, those who understand the real rhythm can find better entry positions.

Fear and greed are always two sides of the same coin. This coin is now flipping in the air.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News