Guosen Securities Research Report Interpretation: Global Energy Storage Enters China-US-Europe Tri-Polar Resonance Cycle, Commercial and Industrial Energy Storage Growth Rate Outperforms Front-of-the-Meter Energy Storage

TechFlow Selected TechFlow Selected

Guosen Securities Research Report Interpretation: Global Energy Storage Enters China-US-Europe Tri-Polar Resonance Cycle, Commercial and Industrial Energy Storage Growth Rate Outperforms Front-of-the-Meter Energy Storage

Energy storage has already upgraded from ancillary facilities for new energy to an independent power infrastructure sector.

By: Rita

TechFlow Guide

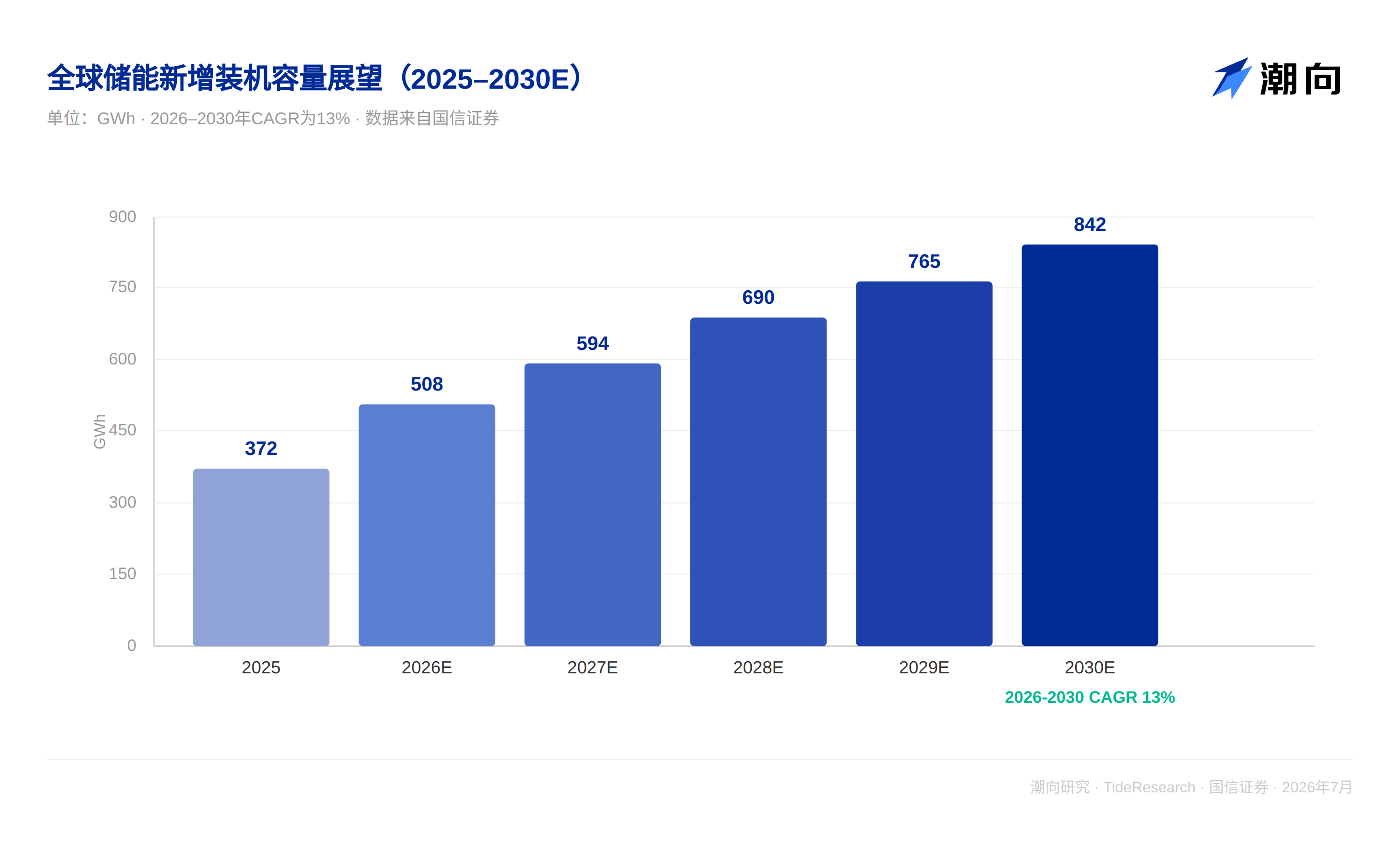

The global energy storage market is bidding farewell to the stage of single policy-driven growth. Guosen Securities' latest research report judges that from 2026 to 2030, global newly added energy storage installed capacity will grow from 508GWh to 842GWh, with a CAGR of 13%, corresponding to output value growing from 533.9 billion yuan to 839.5 billion yuan. The three major markets of China, the United States, and Europe are expanding simultaneously, while emerging markets such as the Middle East, Southeast Asia, and Australia are accelerating follow-up due to power shortages. Energy storage has upgraded from new energy supporting facilities to an independent power infrastructure track.

Domestic: Shifting from Subsidy Dependence to Market Pricing

China's energy storage newly added capacity in 2025 was 66GW and 189GWh, a year-on-year increase of 73%. Among them, front-of-the-meter storage added 179GWh, accounting for 95%, and commercial and industrial storage added 10.5GWh, accounting for 5%, a year-on-year increase of 40%. The report points out that the key to this round of growth is "Document No. 136" promoting energy storage to shift from new energy supporting attributes to independent power market entities, while "Document No. 114" established the capacity electricity price mechanism at the institutional level. In terms of revenue structure, domestic front-of-the-meter storage has currently built a diversified profit model of "capacity base plus spot flexibility plus ancillary service increment". Capacity compensation policies have been implemented in many places. Projects where capacity electricity prices have been implemented generally achieve an all-investment internal rate of return of 7% to 9%, a return level rarely seen in the past era of relying on mandatory storage configuration. Electricity price mechanism reforms have also opened up space for commercial and industrial storage. The full implementation of the peak electricity price mechanism coupled with the deepening of the spot market has continued to widen the peak-valley price spread in areas with concentrated commercial and industrial loads. However, the report also gives a forecast that China's installed capacity CAGR from 2026 to 2030 will be only 8%, far lower than the 73% growth rate in 2025. The growth center under a high base is naturally falling back.

United States: AIDC Forces Grid Acceleration, Energy Storage Becomes a Necessity

US energy storage installation is dominated by front-of-the-meter storage. In 2025, new energy storage added 57GWh, a year-on-year increase of 29%, of which front-of-the-meter storage was 51GWh, accounting for 90%. On June 18, the US Federal Energy Regulatory Commission issued a directive requiring the six major grid operators to open a "fast lane" for grid connection for large electricity consumers such as data centers, while clarifying that grid connection supporting costs are borne by the electricity consumers themselves, forcing the load side to configure flexible regulation resources locally. This means that if data centers want to access the grid faster, energy storage is almost the only realistic option, because it can achieve millisecond-level regulation, directly cope with extreme fluctuations in computing load, and simultaneously meet multiple requirements for power supply reliability and grid demand response. Coupled with the "Big and Beautiful" Act extending the energy storage investment tax credit to 2036, projects starting construction before the end of 2033 can enjoy a 100% credit ratio, dropping to 75% and 50% in 2034 and 2035 respectively. The phase-out rhythm is obviously smoother than the arrangement for wind and photovoltaic power to fully exit in 2027. The policy certainty for US front-of-the-meter storage is obviously stronger than other markets.

Europe: Tripartite Agreement Writes 2030 Targets into Policy Documents

The European energy storage market structure is more balanced. In 2025, newly added capacity was about 27GWh, a year-on-year increase of 24%. Among them, front-of-the-meter storage was 16.3GWh accounting for 60%, household storage 9.8GWh accounting for 36%, and commercial and industrial storage 3.6GWh accounting for 13%. The year-on-year growth rates for commercial and industrial and front-of-the-meter storage reached 62% and 83% respectively. On June 26, the EU signed the "EU Energy Storage Tripartite Agreement", joining member states, industrial enterprises, and financial institutions to form a combined force to support the 2030 target of 200GW energy storage installed capacity. It clarified that the EU needs to add 30 to 35GW of energy storage from 2026 to 2028, the proportion of energy storage meeting peak power demand needs to double from 5% to 10%, and 22 member states simultaneously issued national energy storage deployment commitments. Commercial and industrial storage is the steepest market segment in this agreement. Newly added capacity is expected to jump from 9GWh in 2026 to 24GWh in 2028, and the proportion of commercial and industrial storage to renewable energy installed capacity will increase from 5% to 20%.

Emerging Markets: Power Shortage is the Most Primitive Driving Force

Australia launched a 2.3 billion AUD household storage subsidy plan in May this year. Eligible households can receive up to 4,000 AUD in installation subsidies. At the same time, net metering policies in various states are gradually phasing out, and PV feed-in tariffs continue to decrease, jointly pushing up household storage penetration. In the Middle East, Saudi Arabia's "Vision 2030" plans for renewable energy installed capacity to reach 120GW, and the UAE plans for new energy to account for 44%. High-proportion desert PV grid connection is generating mandatory storage configuration demand. At the same time, Middle East data center construction is accelerating, and energy storage has the dual value of backup power and peak-valley arbitrage. In Southeast Asia, Vietnam and Thailand have already issued mandatory storage configuration policies for new energy projects. Weak grid infrastructure further amplifies the alternative value of energy storage. The common point of these markets is that energy storage is an indispensable patch for grid stability.

Looking at the three major markets together makes it more intuitive. In terms of newly added installed capacity in 2025, China's 189GWh far exceeds the US's 57GWh and Europe's 27GWh, but the growth rhythm in the next five years is reversing: China's CAGR from 2026 to 2030 is only 8%, the US can reach 21% on a North American basis, Europe is 10%, and global commercial and industrial storage runs at the forefront of all market segments with a CAGR of 22%.

TechFlow Perspective

The CAGR given in the report is actually quietly cooling down. China fell from 73% in 2025 to 8% from 2026 to 2030, and the global total growth rate is only 13%. This is somewhat misaligned with the wording of "high prosperity", more like a transition period for the industry from explosive expansion to regular growth. The 22% compound growth rate of commercial and industrial storage is almost twice that of front-of-the-meter storage at 13%, and also significantly faster than household storage at 9%. This means that in the next few years, those truly running out excess returns may not be traditional large storage leaders, but companies better at distributed generation and channel penetration. The nine target companies listed in the report span the full chain of large storage, household storage, and commercial and industrial storage, with wide coverage. However, for ordinary investors, clarifying which market segment beta they are buying may be more important than remembering the "Outperform" rating itself. In addition, the report classifies the Middle East, Southeast Asia, and Australia uniformly as emerging market increments, but the policy implementation intensity and grid construction speed in these regions vary greatly. Whether mandatory storage configuration policies can be implemented as scheduled is the variable that truly determines whether this increment can be realized.

Disclaimer

This article is a compilation and interpretation of third-party securities research reports by TechFlow Research. The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the securities analyst, represent only the position of their affiliated institution, do not represent the views of TechFlow Research, and do not constitute any investment advice.

The market has risks, decisions need to be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News