Latest Portfolio Adjustment Analysis of the U.S. “Version Son”: 20% Position Possibly Invested in Anthropic; $9 Billion Short Position on NVIDIA; Focus Shifts to Power and Memory Sectors

TechFlow Selected TechFlow Selected

Latest Portfolio Adjustment Analysis of the U.S. “Version Son”: 20% Position Possibly Invested in Anthropic; $9 Billion Short Position on NVIDIA; Focus Shifts to Power and Memory Sectors

The best long-term position isn’t necessarily the hottest chip company.

Compiled & Translated by TechFlow

Speakers: Josh Kale, Marketing, Anthropic AI; Ejaaz Ahamadeen, Former Product Manager, Coinbase

Podcast Source: Limitless Podcast

Original Title: Leopold Aschenbrenner Says “No More Stocks!”

Air Date: June 17, 2026

Key Takeaways

Leopold Aschenbrenner—widely regarded as one of the world’s most aggressive AI investors—is simultaneously running a ~$9 billion notional short position in public markets on NVIDIA, ASML, and Oracle, while reallocating capital toward power, memory, data center networking, and deeper AI infrastructure and model assets such as Anthropic. The hosts argue this does not signal an AI bubble bursting, but rather a sector rotation—away from “chip-first” infrastructure trades toward “power-, network-, and data-center-construction-first.” This shift gains increasing market significance following NVIDIA’s recent $25 billion bond issuance and Anthropic’s soaring valuation.

Key Insights Summary

Leopold’s Core Trading Logic

- “The classic ‘pick-and-shovel’ trade in AI has become overcrowded—and Leopold’s recent positioning shifts clearly signal that.”

- “His view isn’t that AI infrastructure has peaked, but rather that certain layers within the infrastructure stack—especially semiconductors and traditional high-flying names—have become excessively crowded.”

- “If the question is where capital flows next, there are two answers. First and most direct: toward the next genuine infrastructure bottleneck—power, memory, and data center networking. Second: toward that mysterious investment revealed just weeks ago.”

- “He’s consistently invested in highly infrastructure-oriented assets—both optical companies and power-related firms.”

- “If he’s cautious on NVIDIA, capital flows to power and memory; simultaneously, he wants to invest directly into the ‘mine’ itself—not just keep buying ‘shovels.’ Anthropic is his preferred mine.”

Signals from NVIDIA’s Financing

- “The issue isn’t whether NVIDIA will continue generating profits—but why a company with exceptionally high margins and substantial cash on hand would borrow another $25 billion externally.”

- “When a company repurchases shares aggressively and hikes dividends dramatically in the same month it borrows money, it clearly isn’t borrowing due to cash shortage. A more plausible explanation is that cheap funding is available—and AI’s financing playbook is undergoing a subtle shift.”

The Next Wave of AI Infrastructure Upside

- “The real bottleneck is no longer just GPUs—it’s power, memory, data center networking, and the physical capability to build these things at scale.”

- “Even with unlimited capital, you cannot build data centers fast enough, ramp memory chip capacity quickly enough, or expand grids, power lines, and related infrastructure instantly. There simply aren’t enough skilled workers on the ground—and permitting, regulation, and bureaucratic processes stand in the way.”

- “Whoever can physically build data centers will capture the profits.”

Optical Modules, Copper, and Fiber

- “As GPU scale increases, copper traces heat up, energy loss rises, and efficiency plummets—making fiber the logical next upgrade path.”

- “Copper remains virtually the only material people genuinely want for high-bandwidth, short-distance transmission. Only when it becomes unsuitable—e.g., over longer distances or under excessive thermal load—does the industry shift to fiber. Hence, current demand for both copper and fiber is exceptionally strong.”

- “Copper futures have surged recently—because everyone needs it. It’s the foundational material for high-bandwidth, short-distance transmission; fiber represents the next stage.”

- “Copper remains the most critical material for short-distance, high-bandwidth transmission—but once distance lengthens or heat intensifies, fiber becomes mandatory.”

- “Capital will next flow to infrastructure companies that sound unglamorous.”

Why Energy Is the Safest Bet

- “I’ve long favored energy because even if AI demand slows, energy remains a global necessity—and that demand will only rise.”

- “The single trend that rises across all scenarios is our growing need for energy, electricity, and power. These are the companies I’m most willing to hold long-term.”

- “What I most want to follow are companies Jensen Huang is investing in—and whose logic overlaps with Leopold’s. Right now, my closest proxy is Marvell.”

- “The best long-term positions may not be the hottest chip stocks—but rather power infrastructure assets that remain indispensable across any macro scenario.”

Leopold’s AI Portfolio

Josh Kale:

Leopold Aschenbrenner—a 24-year-old AI specialist investor—is now widely viewed by markets as the world’s top AI investor. Rumor has it his fund’s notional position size exceeds $20 billion. A month ago, when we reviewed Ejaaz’s post, the fund stood at $13.7 billion—effectively doubling each quarter.

We’ve now obtained several important new developments in his latest investment moves. In our last episode, we discussed his portfolio—and what surprised many was his short position on a company nearly everyone knows: NVIDIA, the world’s highest-valued, most AI-hyped stock. Many struggle to understand why he’d place a >$9 billion short bet on such a company.

Now we have a potential explanation. NVIDIA is raising capital—not through equity, but via debt. On the surface, this seems illogical: why would a company of NVIDIA’s scale and profitability raise another $25 billion in cash—just completed? Today, we’ll tie Leopold’s portfolio to this question: Why has he earned so much? What’s he watching next? And what does NVIDIA’s financing truly mean?

Ejaaz Ahamadeen:

Let’s start with some background. Leopold Aschenbrenner was previously a researcher at OpenAI. Roughly one-and-a-half to two years ago, he raised a fund—initially quite small, around $200 million, as I recall. But according to his most recent 13F filing, the fund’s publicly disclosed holdings now total $13.7 billion.

So naturally, the market wants to know: What positions has he taken? What’s his core investment thesis? Where will his next big trade land? To grasp this, first understand that until about a month ago, Leopold remained extremely bullish on the entire AI sector—particularly the “pick-and-shovel” logic, i.e., GPU and upstream hardware suppliers like NVIDIA.

But roughly a month ago, the market noticed he wasn’t particularly bullish on semiconductors. He remains bullish on memory and power—the true bottlenecks—and possibly on new cloud providers—but notably avoids the world’s most valuable company: NVIDIA. More specifically, he holds ~$9 billion in bearish positions across NVIDIA, ASML, Oracle, and other firms widely seen as core AI infrastructure beneficiaries.

The Logic Behind Shorting NVIDIA

Ejaaz Ahamadeen:

Once this emerged, many grew concerned—fearing an AI bubble burst. After all, on the surface, NVIDIA’s GPUs are still selling briskly, and demand shows no clear weakening. So where’s the problem?

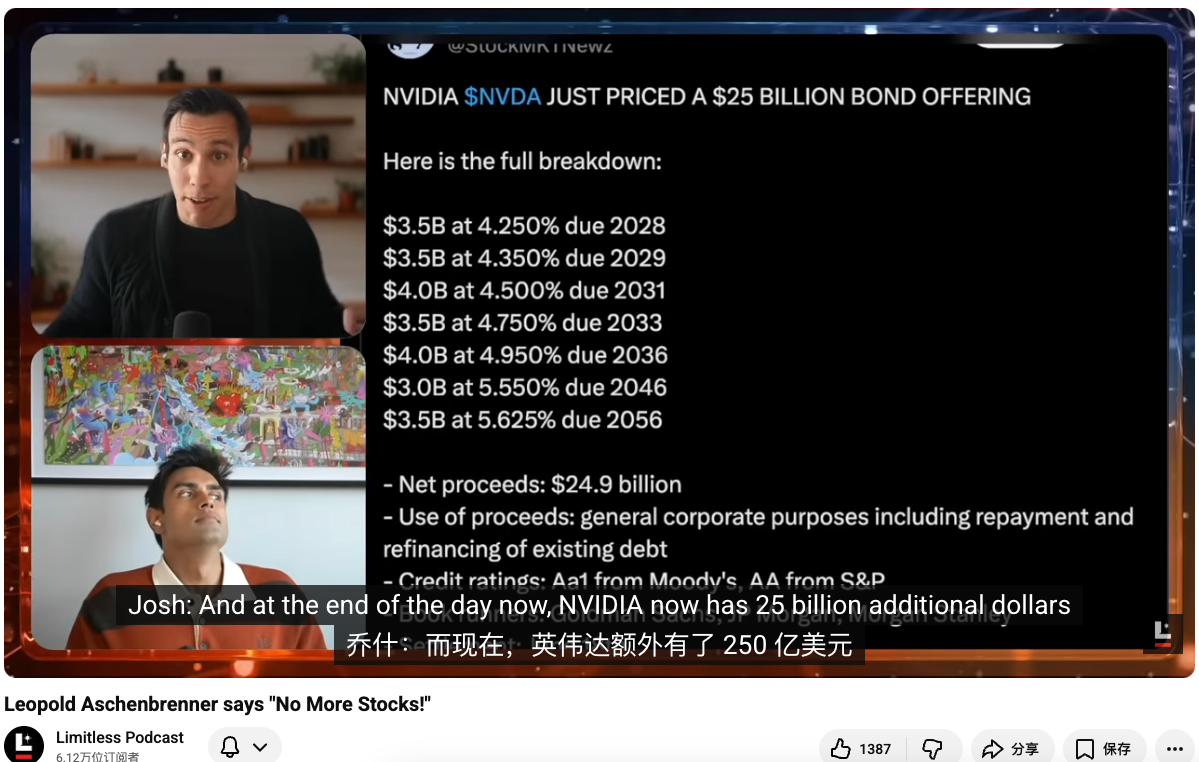

We later uncovered several new clues—the most critical being NVIDIA’s recent $25 billion bond issuance. This means it’s not merely deploying its own balance sheet cash but adding external leverage. So the question arises: why would the world’s most profitable, highest-margin, strongest-cash-flow company borrow $25 billion externally?

Josh Kale:

Initially, they planned to raise $20 billion—but expanded to $25 billion, with oversubscription exceeding 3x. Last episode, we noted: don’t worry about bubbles yet—these firms, though capital-intensive, generate sufficient revenue to theoretically self-fund expansion using their own balance sheets.

Yet this marks NVIDIA’s first notable off-balance-sheet financing since 2021—not tapping its own cash. Its current cash balance stands at ~$12+ billion. Viewed together, this creates a strange tension: Leopold is shorting, while NVIDIA appears cash-rich and profit-rich—yet still issues bonds. So what’s happening?

Decoding NVIDIA’s Bond Financing

Josh Kale: Ejaaz, could you break down this transaction itself? It’s not ordinary fundraising—it’s a bond issuance. Ultimately, NVIDIA’s balance sheet now carries another $25 billion—and the interest rate appears low.

Ejaaz Ahamadeen:

I’ll lay out two interpretations. NVIDIA already held ~$13.7 billion in cash—meaning it could fund operations outright. So why borrow externally? The simplest analogy is home-buying: many buyers with full cash still opt for mortgages, because their own capital can be deployed elsewhere—and if borrowing costs are low enough, it’s cheaper.

Interest-rate conditions haven’t been friendly lately—but as NVIDIA, one of the world’s most valuable and sought-after companies, it can borrow on exceptionally favorable terms. This $25 billion bond offering spans maturities from 2 to 30 years—essentially cheap money, with yields approaching U.S. Treasury levels.

Moreover, the offering was oversubscribed ~4x—meaning $85 billion in demand competed for $25 billion in supply. NVIDIA could essentially pick and choose investors. Officially, NVIDIA states this is primarily for refinancing existing debt. Google did something similar just weeks ago—and again in February. So you can accept this as financial optimization.

Yet another angle is hard to ignore: over the past six weeks, NVIDIA, Amazon, Google, and several other hyperscale cloud providers have all pursued external financing—some via bonds, others via equity sales. Perhaps Leopold’s view isn’t entirely unfounded: could this signal early bubble softening—or the house of cards beginning to wobble? Yet purely from a financial-structure standpoint, nothing yet points clearly to danger.

Josh Kale:

I agree. A $9 billion short on NVIDIA is enormous. But our research uncovered another detail: on May 18, NVIDIA’s board authorized an additional $80 billion in share buybacks—and raised its dividend from $0.01 to $0.25 per share—a 25x increase.

If a company simultaneously executes massive buybacks and multiplies dividends while borrowing money, it clearly isn’t borrowing due to cash shortage. A more reasonable interpretation is that cheap funding is available—and AI’s financing playbook is shifting subtly. Everyone wants in on these capital moves, and NVIDIA realized issuing debt is cheaper than alternatives—so it seized the opportunity. At least for now, NVIDIA remains in excellent shape.

Why He Rebalanced

Josh Kale: That brings us back to another question: What’s Leopold thinking? Why did his view change? Your chart also shows NVIDIA hasn’t performed especially strongly lately—but it’s hardly weak. It remains the world’s largest company, near $5 trillion in market cap; a 7% monthly drop pales against other AI stocks surging.

Ejaaz Ahamadeen:

I don’t think NVIDIA will disappear. Its GPUs—and its newly launched CPU product line—will perform extremely well. AI product demand is currently exponentially oversubscribed, and NVIDIA remains the primary supplier capable of meeting that demand.

Yet I do believe the classic AI ‘pick-and-shovel’ trade has grown too crowded—and Leopold’s recent positioning shifts convey precisely that signal. His latest 13F confirms a pronounced bearish tilt toward semiconductors—including NVIDIA, ASML, Oracle, and other infrastructure-tier firms.

Meanwhile, he’s heavily invested in memory, power, and new cloud providers. This suggests his view isn’t that AI infrastructure has peaked—but that certain layers within the infrastructure stack—especially semiconductors and traditional high-fliers—have become overly crowded.

If the question is where capital flows next, there are two answers. First and most direct: toward the next genuine infrastructure bottleneck—power, memory, data center networking. Second: toward that mysterious investment revealed just weeks ago.

The Unexpectedly Revealed Anthropic Position

Josh Kale:

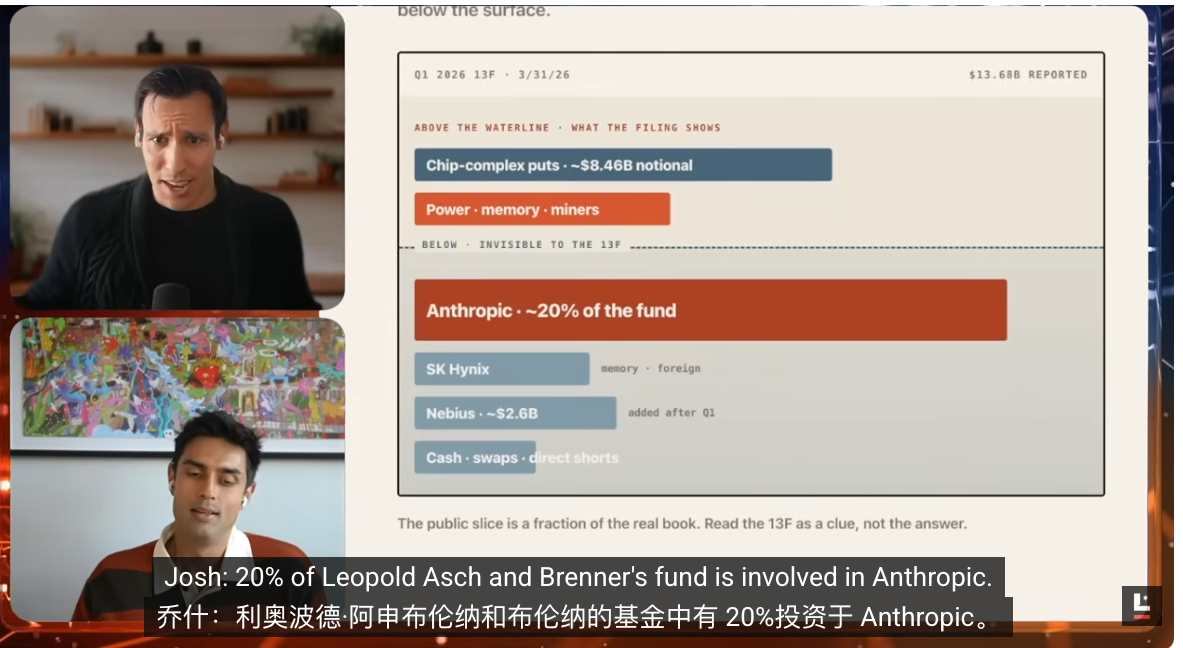

This is the biggest surprise—and I only learned it yesterday from you. My immediate reaction was disbelief. Could Leopold’s fund ‘Situational Awareness’ really hold 20% of its portfolio in Anthropic equity? External reports suggest Anthropic comprises roughly one-fifth of Leopold’s fund—confirmed by outlets including The Wall Street Journal and insiders close to the deal.

This became a completely market-unexpected card in his hand—because 13Fs disclose only public-market holdings, not private equity. Anthropic, being private, falls outside 13F reporting. Precisely because of this, analysts began revaluing his fund upward to $20 billion.

If 20% of his fund is Anthropic—and he invested around early 2025—that year’s return on Anthropic alone feels like seven years’ worth. This dramatically revises our understanding of his entire portfolio.

Ejaaz Ahamadeen:

Yes. His first private or fund-based investment in Anthropic occurred around March 2025, when Anthropic’s valuation stood at ~$60 billion. By its most recent round, it’s now valued at $96.5 billion.

That’s nearly a 15x gain. Using the algorithm shown on today’s show, his latest 13F-disclosed liquid portfolio value is $13.7 billion—if we add the Anthropic stake reported by The Wall Street Journal (~$7 billion), his total assets under management reach ~$20 billion.

How extraordinary is this? Bill Ackman—a top-tier investor with 30–40 years’ market experience—manages roughly $20 billion at Pershing Capital. Leopold entered this game just 1.5 years ago—and he’s only 24, with virtually no formal investment experience.

Yet he’s made astonishingly prescient calls—and remarkably, he wrote them all down in advance. Upon launching his fund 1.5 years ago, he published a 65-page AI manifesto titled ‘Situational Awareness,’ laying out his full thesis—including how capital would rotate from semiconductors and parts of infrastructure to other constraint-driven bottlenecks. Markets are now unfolding exactly along this path—an astonishing feat.

The Next Infrastructure Cycle

Ejaaz Ahamadeen:

So this tells me where capital flows next. If he’s cautious on NVIDIA, funds move to power and memory; simultaneously, he wants to invest directly into the ‘mine’ itself—not just keep buying ‘shovels.’ Anthropic is his favorite mine.

Josh Kale:

This indeed looks like a new trend—and again, he’s ahead of most. Over the past 12 months, investors hunted for AI bottlenecks: rare metals, memory, RAM—each cycle saw frenzied chasing. Those calls weren’t wrong—the rallies happened.

But now, those formerly bottlenecked areas see valuations gradually normalizing. Investors increasingly understand these companies’ business models, addressable markets, and future revenues—so much of that value is already priced in. Our focus now shifts to where capital flows next.

You mentioned land, power, enclosures, physical infrastructure—this direction looks right. Because if we ask what AI truly needs most, the answer increasingly points to physical construction capability. Consider xAI—or more accurately, SpaceX (now publicly traded). Its core revenue isn’t rockets themselves—but AI infrastructure development.

Its recent deals with Anthropic and Google have generated more value than Starlink, Starship, and its entire satellite business combined. Clearly, massive demand and value exist here. So the question becomes: who can actually build these things?

SpaceX is clearly one answer. Its after-hours share price hit $230—implying a ~$3.1 trillion valuation. We’ll dedicate a full episode to SpaceX this week, given its extraordinary momentum: fresh off acquiring Cursor, its valuation now stands at $3 trillion—and Elon Musk earned more in one day than Warren Buffett amassed over his entire career.

Who Captures the Next Wave of Value

Josh Kale: We’re focused on which companies excel at building this hardware infrastructure—and developing ‘machines that build machines.’ Aligning with Leopold’s direction and broader trends, we believe capital flows here next. So Ejaaz—where does this rotation land in reality?

Ejaaz Ahamadeen:

Many will be unglamorous infrastructure companies. Marvell has been frequently cited lately. Weeks ago at Computex in Taiwan, Jensen Huang declared it “the next trillion-dollar company.”

Three months before that statement, NVIDIA invested $1.5 billion in Marvell. I’m almost unsure whether this qualifies as insider trading or market manipulation—because after his comment, Marvell’s stock rose another 70%.

I think declaring AI infrastructure peaked is easy—but comparing this cycle to historical financial crises (e.g., 2008) reveals key differences. The highly leveraged, financial-engineering–driven, systemic manipulation flavor hasn’t fully emerged yet.

Two critical distinctions exist. First: today’s companies sell real products to real customers paying real money. Neither the dot-com bubble nor the 2008 crisis featured such robust underlying demand. Second: physical laws constrain infinite leverage—we simply can’t scale infinitely because human labor and construction capacity bottleneck the system.

You can raise limitless capital—but you can’t build data centers fast enough, ramp memory chip capacity quickly enough, or expand grids, power lines, and related infrastructure instantly. There aren’t enough skilled workers on-site—and permitting, regulation, and bureaucracy impede progress.

So paradoxically, this gives investors an edge. Knowing the hottest chips and ‘pick-and-shovel’ trades are overcrowded, capital flows next to power, data networks (e.g., Astera Labs), and adjacent sectors. You must ask: when do these contracts begin delivering? When do fabs truly come online? When will SpaceX launch AI satellites? Even—when might solar power train AI models?

Timelines dictate timing. I personally invest this way—though this isn’t investment advice. I adopt this framework because over the past 18 months, we’ve witnessed capital rotating from broad AI stocks to semiconductors and infrastructure plays.

Josh Kale:

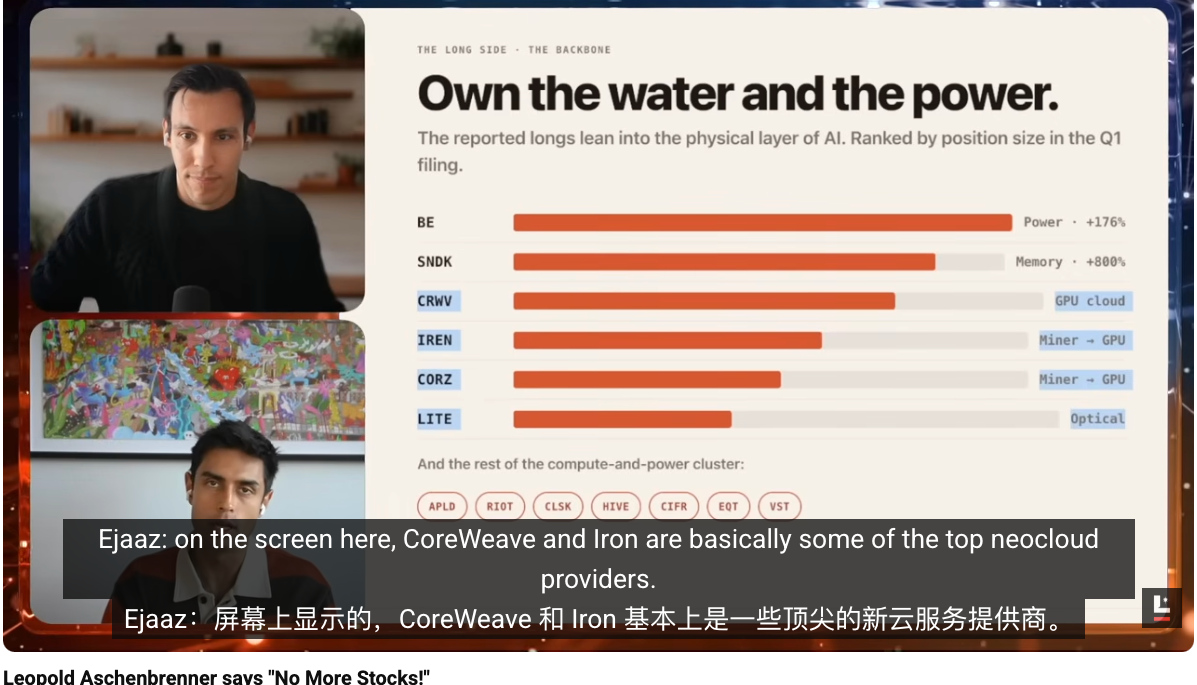

Looking deeper at this portfolio chart, you’ll see this narrative embedded in his holdings. By category, his largest allocation? Power and energy. Second: memory. Third: cloud and GPU miners—the most tangible infrastructure.

He seeks exposure to new cloud providers like CoreWeave—and miners pivoting to cloud compute. He wants physical infrastructure—because he sees it as the true bottleneck. As you noted, many finer-grained layers exist—actual construction, hardware manufacturing, data center deployment—all extraordinarily difficult.

If anything’s the biggest bottleneck, permitting may top the list. Who solves this? SpaceX aims to relocate data centers to space; Tesla aims to deploy humanoid robots to solve labor shortages. But both remain distant. In the near-to-mid term, vast white-space opportunities exist—precisely where Leopold is betting.

Optical Modules and Fiber Advantages

Josh Kale: Let me add one detail we didn’t explore earlier. For those digging deeper—seeking further alpha—many of his clues lie in optics and lower-level tech stacks. Ejaaz, you’ve studied this closely—could you walk us through his thinking?

Ejaaz Ahamadeen:

Looking at his screen positions, CoreWeave and Iron are top-tier new cloud providers. Simply put, they resemble Amazon Web Services—but while AWS serves internet companies, these serve AI firms with ready-made GPU infrastructure.

They bundle GPUs, networking, and deployment—so AI firms skip infrastructure headaches and jump straight to model training and compute access. CoreWeave and Iron were among his largest concentrated positions from inception—and delivered outsized returns.

Notably, he still holds them as top positions today—indicating, in his view, the trade isn’t over. Further, he privately invested in Core Scientific, which helps unlock CoreWeave’s infrastructure supply capacity. In effect, he layered additional leverage onto CoreWeave.

Beyond these, Coherent and Lumentum—optical and fiber interconnect suppliers—are also key. Put simply: semiconductors and GPUs communicate traditionally via copper wiring. The problem? As GPU scale grows, copper heats up, energy loss escalates, and efficiency plummets—making fiber the logical next upgrade path. It enables faster data transfer, higher cost efficiency, and greater profitability for inference/training providers. So he consistently bets on highly infrastructure-oriented assets—both optical firms and power-related companies. They may lack glamour—but in my view, this is precisely where capital is flowing.

Josh Kale:

Copper fascinates me too—I only recently grasped its centrality in short-distance data transmission. In many high-bandwidth, short-distance scenarios, copper is virtually the only material people truly want. Only when it fails—due to excessive distance or heat—do they switch to fiber. Hence, current demand for copper-and-fiber combinations is exceptionally strong. That’s why tracking copper trades is insightful. Copper futures have surged—because everyone needs it. It’s the foundational material for short-distance, high-bandwidth transmission; fiber is the next step.

Thinking deeper, materials remain fascinating. At the absolute base layer—the foundation of intelligence—what raw inputs matter most? Copper is one; lithium is another; many others exist. We should dedicate a full episode to materials. Perhaps Leopold hasn’t reached this layer yet—and we might spot the next rotation first.

Josh Kale:

Going all the way to the stack bottom—even visiting copper mines to see how these materials are produced—brings us back to the core thesis: the next rotation shifts from smaller bottlenecks to genuinely hard problems—hardware and large-scale data center construction.

Who can build data centers captures the profits. We’ve already seen how much SpaceX earns from data center demand. Whoever launches more data centers faster—and supplies adequate power and GPUs—earns the most. That’s precisely where Leopold is betting.

Is a Bubble Forming?

Josh Kale: In summary, we don’t believe a bubble burst has begun. Leopold’s positioning looks more like rotation than wholesale retreat. So—should we still follow him?

Ejaaz Ahamadeen:

I admit: my first reaction upon seeing his 13F was disbelief—how could someone short the world’s most valuable company, with demand booked through 2029? Yet seeing this financing, I now wonder: if NVIDIA continues adding external debt—or even sells equity—could Leopold be right again?

If so, his fund could surpass the world’s top traders and best hedge funds. He’s consistently winning—and that’s hard to deny.

Josh Kale:

One more point matters greatly: his entire track record is long-only—he’s never truly faced a large-scale selling test. Recall Bill Ackman: generating 30x returns and surviving 30 years in markets are two different things.

If he sustains this growth—and learns when to exit, how to manage risk, and how to hedge effectively—that’s even scarier. We’re already seeing early signs: that $9 billion short isn’t naked cash—it’s achieved via options and leverage. Regardless, this warrants continued observation.

Energy Is the Core Bet

Josh Kale: If you had to pick one stock from his entire portfolio to buy yourself—which would it be?

My answer is energy stocks. I’ve long favored energy because even if AI demand slows, energy remains a global necessity—and demand only rises. Even ignoring AI, we need more energy and electricity. Companies like Bloom Energy—which enhance power generation and delivery—are my most exciting area, as they function like hedged bets. The single trend rising across all scenarios is our growing need for energy, electricity, and power. These are the companies I’m most willing to hold long-term.

Ejaaz Ahamadeen:

My answer’s slightly cheating. I most want to follow companies Jensen Huang invests in—and whose logic overlaps with Leopold’s. My closest proxy right now is Marvell. Though not in Leopold’s public holdings, it aligns tightly with his fiber and power bets—and Jensen has already committed $1.5 billion.

I’ve observed a pattern: whenever Jensen invests in a company via NVIDIA—be it Intel, CoreWeave, or others—it tends to rally. So my current position sits here. I also hold CoreWeave—because both Jensen and Leopold are extremely bullish on it.

Josh Kale:

Marvell has surged 270% over the past six months. This may indeed be a useful heuristic: when influential figures like Jensen—or even Trump—publicly endorse a stock, it’s often worth serious attention.

History repeatedly proves such signals deliver outsized returns. Cases like Intel and Marvell confirm: they understand what they’re saying—and possess the ability to influence outcomes. This cycle is truly wild.

I hope it continues—and current evidence suggests it likely will. At least for now, we remain net long and optimistic—and will keep adapting daily to evolving conditions.

Josh Kale: Any final thoughts on Leopold’s portfolio update?

Ejaaz Ahamadeen:

I’d genuinely welcome dissenting views. If you listened to our analysis and think we’re entirely wrong—or misinterpreted something—please call it out directly.

Yesterday, I scrutinized NVIDIA’s $25 billion financing news for hours, seeking flaws. Yet purely on financial logic, it makes sense: why not borrow near-risk-free cheap money? Borrowing others’ capital to expand is clearly more rational than selling equity—preserving more upside.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News