Bitget UEX Daily Report | Powell’s First FOMC Press Conference Turns Hawkish; Half of Fed Officials Expect Rate Hikes; U.S. and Iran Sign MoU to Ease Geopolitical Risks; U.S. Major Indices Decline, Tech Stocks Under Pressure

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Powell’s First FOMC Press Conference Turns Hawkish; Half of Fed Officials Expect Rate Hikes; U.S. and Iran Sign MoU to Ease Geopolitical Risks; U.S. Major Indices Decline, Tech Stocks Under Pressure

Overall, it is recommended to focus on data verification and geopolitical implementation progress, maintaining a neutral-to-cautiously optimistic allocation.

I. Top News Highlights

Federal Reserve Updates The Federal Reserve held interest rates steady within the 3.5%–3.75% range, but the dot plot revealed deepening divisions among policymakers: nine officials now project at least one rate hike before the end of 2026, with the median projection rising to 3.75%. Chair Kevin Warsh emphasized that inflation remains far above the 2% target and appointed five special task forces focused on monetary policy. The newly revised statement features simplified language, placing renewed emphasis on price stability. Market expectations for a year-end rate hike have surged significantly—bolstering the U.S. dollar but potentially increasing volatility pressure on equities and other risk assets.

Global Commodities The U.S. and Iran formally signed a Memorandum of Understanding (MoU), pledging to halt military operations, lift sanctions, and reopen the Strait of Hormuz, covering 14 key provisions—including reconstruction funding and nuclear issue resolution. This agreement alleviates concerns over energy supply disruptions, exerting short-term downward pressure on oil prices while supporting safe-haven assets such as gold, underscoring the direct transmission of geopolitical easing to commodity markets.

Macroeconomic Policy Donald Trump stated that the Fed’s decision to hold rates “is also acceptable,” while hinting at potential future hikes. The Fed’s updated projections indicate higher core inflation and a slightly lower GDP growth forecast—reflecting ongoing supply-side shocks. Policy signals are turning more cautious; combined with Middle East de-escalation, this supports near-term improvement in risk sentiment—yet uncertainty around the inflation trajectory will continue to dominate market expectations going forward.

II. Market Recap

Commodities & FX Performance

- Spot Gold: ~$4,300/oz, +1.25%.

- Spot Silver: ~$69/oz, +1.9%.

- WTI Crude Oil: ~$75/bbl, −1.13%.

- Brent Crude Oil: ~$79/bbl, −1.0%.

- U.S. Dollar Index (DXY): ~100.332, −0.05%.

Key Drivers Analysis: The U.S.–Iran MoU substantially reduces the risk of disruption to Strait of Hormuz shipping lanes, driving oil prices lower. Meanwhile, the Fed’s hawkish pivot strengthened the U.S. dollar. Gold oscillated narrowly amid competing forces of safe-haven demand and strong dollar headwinds; silver posted a modest rebound aligned with improved industrial demand outlooks. Overall, geopolitical easing coupled with expectations of a higher-for-longer rate path is pressuring near-term upside potential for commodities—though persistent dollar strength may continue squeezing emerging markets and commodity-linked assets. Watch closely for actual supply-demand impacts following further sanction relief implementation.

Cryptocurrency Performance

- BTC: ~$64,600, −1.85%.

- ETH: ~$1,750, −2.34%.

- Total Crypto Market Cap: ~$2.31 trillion, −1.4%.

- Liquidations (24h): ~$440 million total; long liquidations ~$310 million.

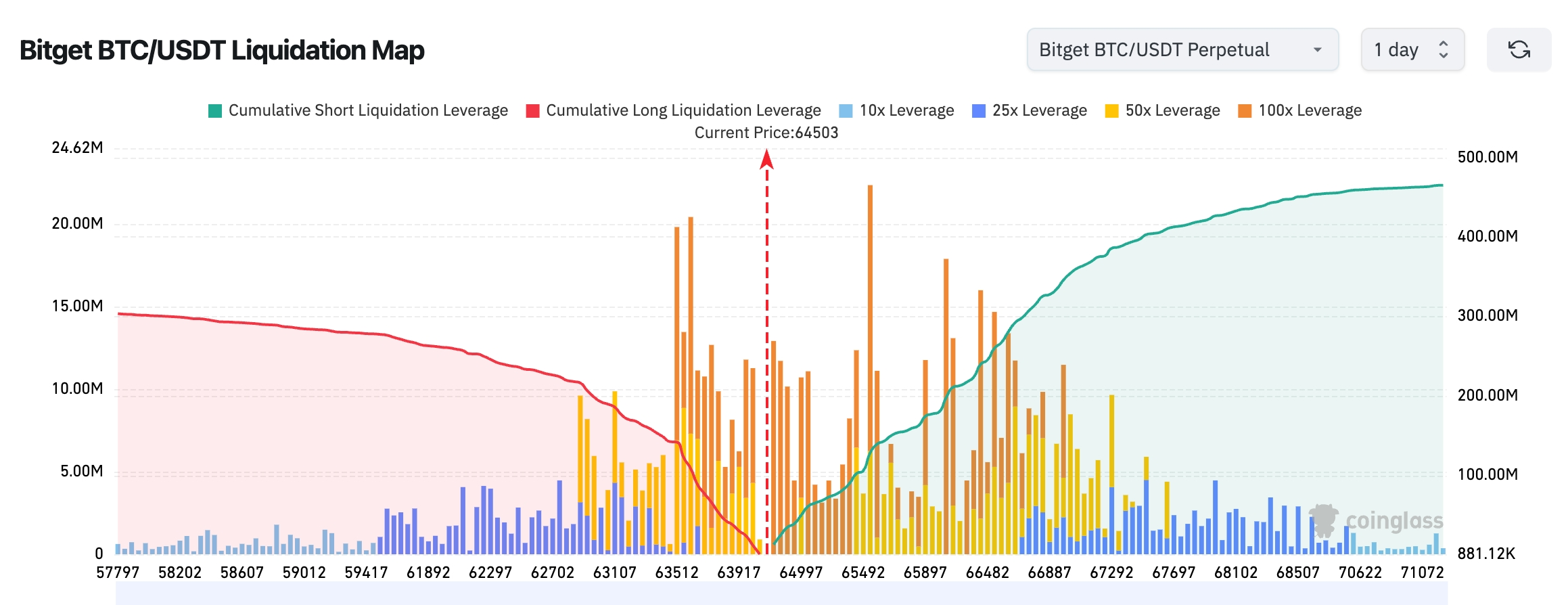

- Bitget BTC/USDT Liquidation Map: Current price ~$64,503 USDT—sitting just below the primary liquidation cluster zone. A large concentration of 50x and 100x short positions resides between $65,500–$66,900, with cumulative short liquidation volume far exceeding long liquidation volume below. While long liquidations are clustered between $63,500–$64,000, their scale is notably smaller. Thus, from a liquidation distribution perspective, the market appears more likely to first test short liquidity in the $65,500–$66,500 range before determining its next directional move.

- Spot ETF Net Inflows/Outflows: BTC spot ETFs recorded net inflows of $10.2 million as of yesterday’s close.

Key Drivers Analysis: Hawkish Fed signals and Chair Warsh’s communications triggered leveraged position unwinding, while the U.S.–Iran agreement eased risk sentiment—leading to synchronized pullbacks in BTC and ETH, though total market cap held key support levels. ETF flows remained relatively stable; liquidations were predominantly long-dominant, and BTC is currently testing critical technical support. Macroeconomic uncertainty and geopolitical easing are acting as countervailing forces—keeping near-term trends range-bound. Monitor institutional consensus on adapting to a higher-rate environment and capital rotation patterns.

U.S. Equity Index Performance

- Dow Jones Industrial Average: ~52,000 points (−0.6%).

- S&P 500: ~7,511 points (−0.57%).

- Nasdaq Composite: ~26,376 points (−1.15%).

Tech Giants’ Updates

- NVDA: ~$206.11, −0.02%.

- AAPL: ~$296.36, −0.96%.

- MSFT: ~$379, −1.5%.

- GOOGL: ~$365.94, −1.96%.

- AMZN: ~$239.85, −2.50%.

- META: ~$580, −1.2%.

- TSLA: ~$401.35, −0.82%.

Performance Summary & Driver Analysis: U.S. equity indices showed divergence—Dow Jones benefited from defensive positioning and hit a record high, while Nasdaq was weighed down by tech sector corrections. Among the Magnificent Seven, AI-related stocks faced valuation pressures and sensitivity to Fed signals; individual names like Tesla exhibited event-driven divergence. Sector-wide sentiment turned cautious amid hawkish policy and geopolitical easing. Though AI’s long-term narrative remains resilient, rising leverage sensitivity and interest-rate exposure have intensified stock-level dispersion.

Crypto Stock Perpetual Contracts Overview

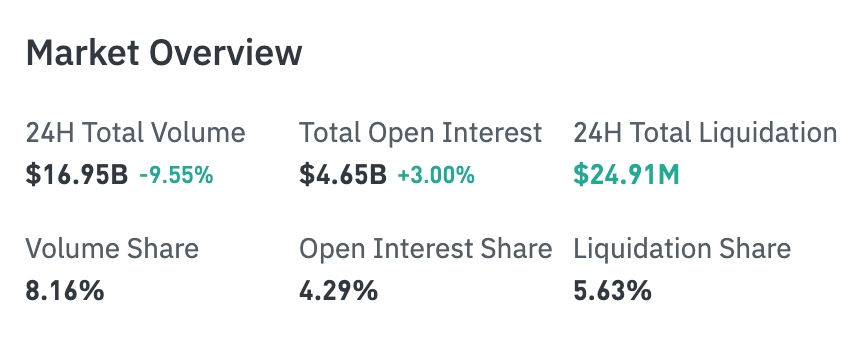

- 24H Trading Volume: $16.942 billion (−9.60%)

- Total Open Interest: $4.651 billion (+3.00%)

- 24H Liquidations: $24.912 million

- Trading Volume Share: 8.15%

- Open Interest Share: 4.29%

- Liquidation Share: 5.63%

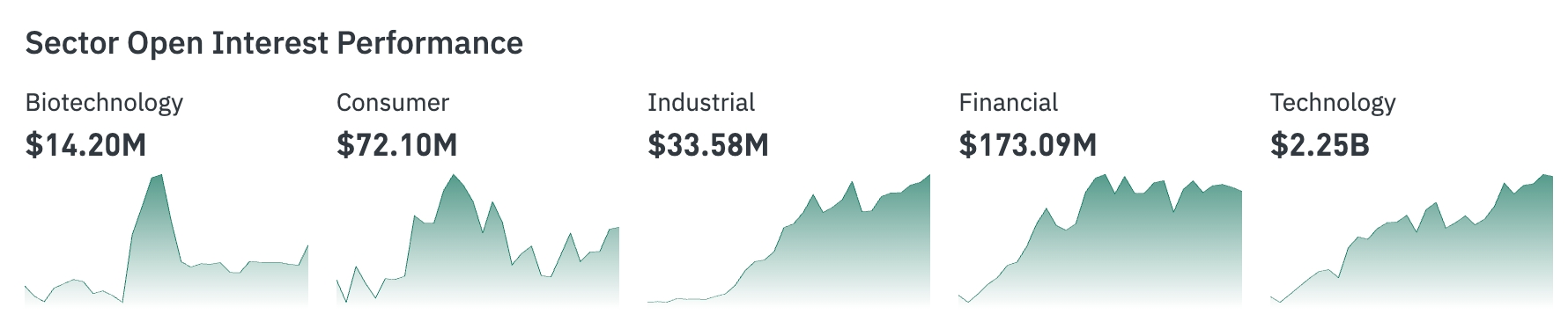

Sector Performance

- Tech Sector: Highest open interest—$2.246 billion

- Financial Sector: $173 million

- Biotech Sector: $14.205 million

- Consumer Sector: $72.103 million

- Industrial Sector: $33.605 million

Open Interest Heatmap

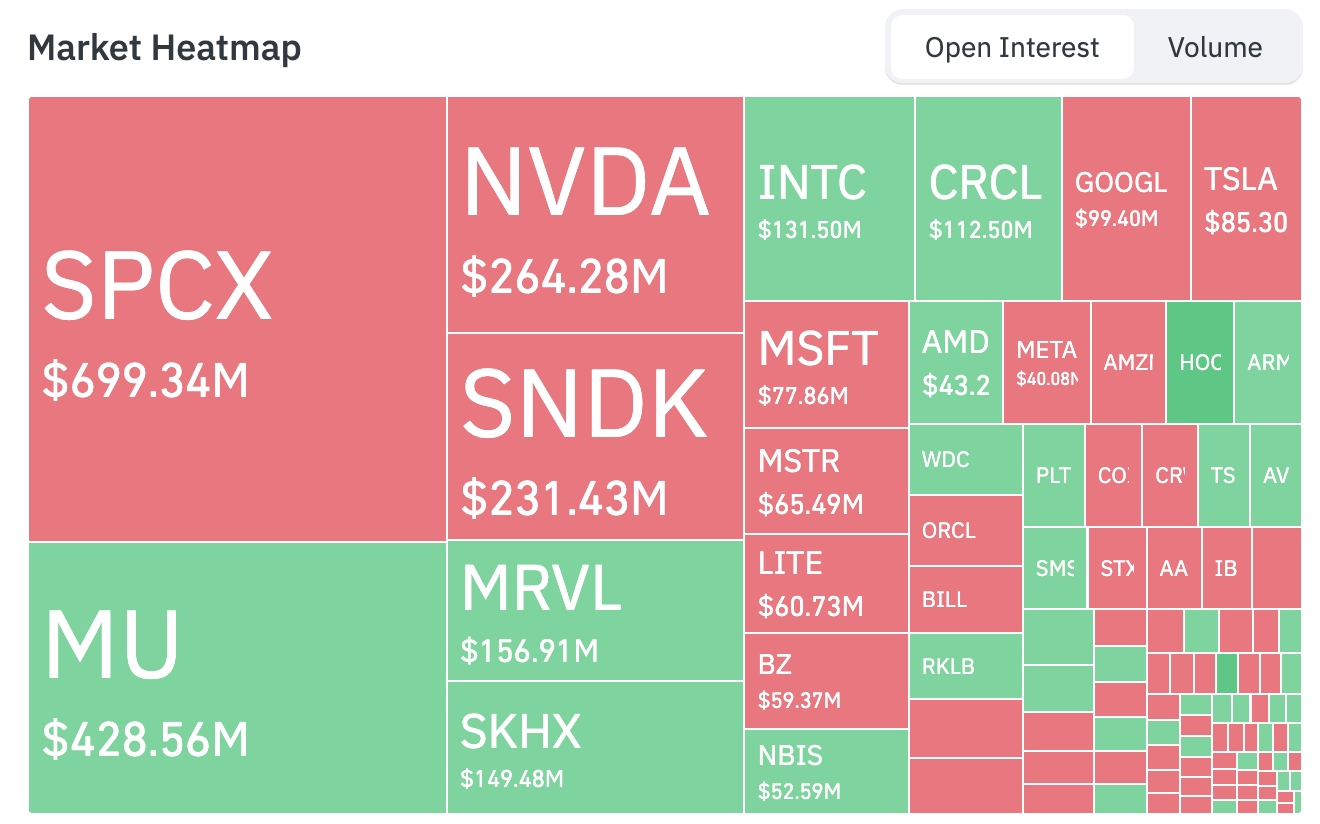

- SPCX: $699 million

- MU: $428 million

- NVDA: $264 million

- SNDK: $231 million

- MRVL: $157 million

Sector Volatility Observations

Semiconductor/Chip Sector: Mixed performance overall (with pronounced sub-sector divergence)

- Gainers: ARM up >5%; Western Digital (WDC), Applied Materials (AMAT), Broadcom (AVGO) up >4%.

- Losers: SanDisk-related names, NXP Semiconductors (NXPI), and NVIDIA (NVDA) down >1%. Key drivers: Chair Warsh’s inaugural hawkish communication—raising the median rate projection and streamlining the statement—has prompted market reassessment of long-term growth and capital cost assumptions, weighing on high-valuation AI/chip growth stocks. Yet ARM demonstrates resilience amid AI edge computing and agent-driven trends; Broadcom benefits from diversified applications and enterprise order flow. Memory/storage-related names face headwinds from cost pass-through challenges and cyclical concerns. While Intel’s 18A-P process risk production news provided some supply-chain uplift, the broader sector remains sensitive to macro rate-path developments—continuing its high-beta behavior in the near term.

Aerospace/Emerging Tech Sector

- SpaceX declined ~4.95% on its first trading day post-IPO. Key driver: As a high-valuation new listing, profit-taking pressure emerged amid the Fed’s hawkish pivot and rising funding-cost expectations. Although SpaceX maintains a dominant long-term position in Starlink and launch services, heightened volatility is typical during early-stage public trading—exacerbated here by a temporary dip in market risk appetite.

III. Deep Dives: U.S. Equity Stocks

1. ASML – Terafab Project Supply Warning Summary: ASML’s CEO cautioned that delivering for new projects like Elon Musk’s Terafab requires avoiding supply bottlenecks—an opportunity of major wafer fab significance demanding careful execution. Market Interpretation: Institutions highlight ASML’s leadership in AI infrastructure equipment expansion, with supply-chain execution capability now a critical differentiator. Investment Implication: Long-term beneficiaries of semiconductor cycles—but monitor supply-chain execution closely; near-term volatility may offer entry opportunities.

2. Apple (AAPL) – iPhone Air Upgrade & Pricing Strategy Summary: Apple is advancing the second-generation iPhone Air (slated for Spring 2027), featuring upgraded cameras and enhanced battery life powered by the A20 Pro chip; Tim Cook confirmed pricing will rise to offset increased chip costs. Market Interpretation: Analysts view this as an effort to strengthen product appeal; passing through cost increases reflects mounting pressure across the supply chain. Investment Implication: Track innovation cadence and pricing elasticity; the services ecosystem provides a cushion against hardware cyclicality.

3. Intel (INTC) – Process Progress & AI CPU Outlook Summary: 18A-P has entered risk production, improving performance and power efficiency; Bernstein raised its price target, emphasizing that AI agents will drive stronger CPU demand. Market Interpretation: Institutions anticipate a rebalancing of CPU/GPU configurations in the AI 2.0 era. Investment Implication: Process breakthroughs could reshape competitive positioning—monitor foundry customer migration trends.

4. Amazon (AMZN) – Quantum Computing Outlook Summary: Executives forecast the first commercially viable quantum computer will emerge within 5–7 years, following a development trajectory similar to semiconductors. Market Interpretation: Long-term technology investments are gaining recognition, reinforcing cloud and AI competitiveness. Investment Implication: Quantum investment horizons are long—focus on milestone progress updates.

IV. Market Updates

1. Strategy’s preferred stock STRC closed Wednesday at $89—down 11% from its $100 par value—and touched an intraday low of $88.50, marking its lowest closing price since listing. STRC currently pays an effective dividend yield of 12.9%, adjusted monthly to maintain a stable ~$100 price. When the share price trades above par, Strategy issues new shares to purchase Bitcoin—but this program has been suspended amid STRC’s current discount trading.

2. Kay Haigh, Analyst at Goldman Sachs Asset Management, stated today’s rate decision confirms the Fed’s recent hawkish shift extends beyond energy-price-driven inflation. Despite recent oil price declines, half of FOMC members now anticipate at least one rate hike as early as this year—driven by robust labor-market data and sticky inflation metrics. Her base case remains that the Fed can narrowly avoid hiking—but the margin for error is slim, and upcoming inflation reports will carry outsized weight.

3. Nick Timiraos—the so-called “Fed whisperer”—commented on the Fed’s rate decision: “This meeting’s dot plot displays a clearly hawkish tilt. Of the 18 voting members, nine now project at least one hike this year, with six expecting multiple hikes.”

4. The Royal Government of Bhutan transferred 533.2 BTC (~$34.52 million) into a centralized exchange (CEX). Since June last year, the Royal Government of Bhutan’s address has gradually sold approximately 10,451 BTC for ~$979 million—averaging $93,738 per BTC.

5. Research firm K33 noted in its market report that Bitcoin rebounded after two consecutive weeks of double-digit declines. Long-term holder (LTH) holdings have reached an all-time high—potentially signaling the end of the bear market. Research Head Vetle Lunde stated: “The decline in old-coin transaction activity suggests reduced selling willingness among long-term holders, while patient participants steadily absorb supply—further indicating the bear market may be nearing its conclusion. Supporting this view, 79% of Bitcoin’s circulating supply is now held by long-term holders—a record high—reflecting sustained accumulation and a gradual shift toward a more constructive market environment.”

V. Today’s Market Calendar

June 18 (Thursday)

- U.S. Economic Data: Weekly Initial Jobless Claims (for week ended June 13), Philadelphia Fed Manufacturing Index, etc.

- U.S. Earnings: Accenture (ACN), Kroger (KR), among others—key focus areas include consumer and tech services sectors. ★★★★

June 19 (Friday)

- U.S. Markets Closed for Juneteenth Federal Holiday.

Key U.S. Equity Themes This Week:

“Fed Focus Week”: Kevin Warsh’s debut FOMC meeting + Retail Sales and other economic data + Earnings from Accenture/Kroger—will shape macro-policy expectations and market sentiment. SpaceX (SPCX) IPO’s first full trading week—watch implications for space/tech-related equities.

Institutional Views: Leading investment bank analysts observe that Chair Warsh’s hawkish inaugural tone—combined with the upward revision in the dot plot—has heightened near-term rate uncertainty. However, the U.S.–Iran MoU significantly eases energy-related risks, providing a buffer. The联动 (interplay) between dollar strength and falling oil prices benefits defensive U.S. equity sectors, while tech/growth stocks face valuation headwinds. Crypto markets face near-term pressure, yet ETF fundamentals remain solid; long-term outlook remains positive under a soft-landing macro scenario—supporting broad risk-asset recovery. Overall, investors should prioritize data validation and geopolitical implementation progress, maintaining a neutral-to-cautiously optimistic allocation stance.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute any investment advice. Data presented herein may contain unavoidable discrepancies—please refer to real-time market data for accuracy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News