Pantera Capital Retrospective: The Largest Liquidation Wave in History, Tokens Plunge 60%—Where Is the Market Heading in 2026?

TechFlow Selected TechFlow Selected

Pantera Capital Retrospective: The Largest Liquidation Wave in History, Tokens Plunge 60%—Where Is the Market Heading in 2026?

Historically, periods of chaos have laid the foundation for growth in the next phase.

Author: Cosmo Jiang

Translation & Editing: TechFlow

TechFlow Intro: Pantera Capital’s annual report reveals the harsh truth of the 2025 crypto market—not a fundamentals-driven year, but one dominated by macro conditions, positioning, and market structure. Bitcoin fell only 6%, yet most tokens plunged 60%, reflecting extreme market divergence. For investors and practitioners aiming to survive in 2026, understanding these drivers matters more than blind optimism.

Outlook for 2026

2025’s crypto returns were not driven by fundamentals. It was a year dominated by macro environment, positioning, capital flows, and market-structure effects—especially for assets beyond Bitcoin.

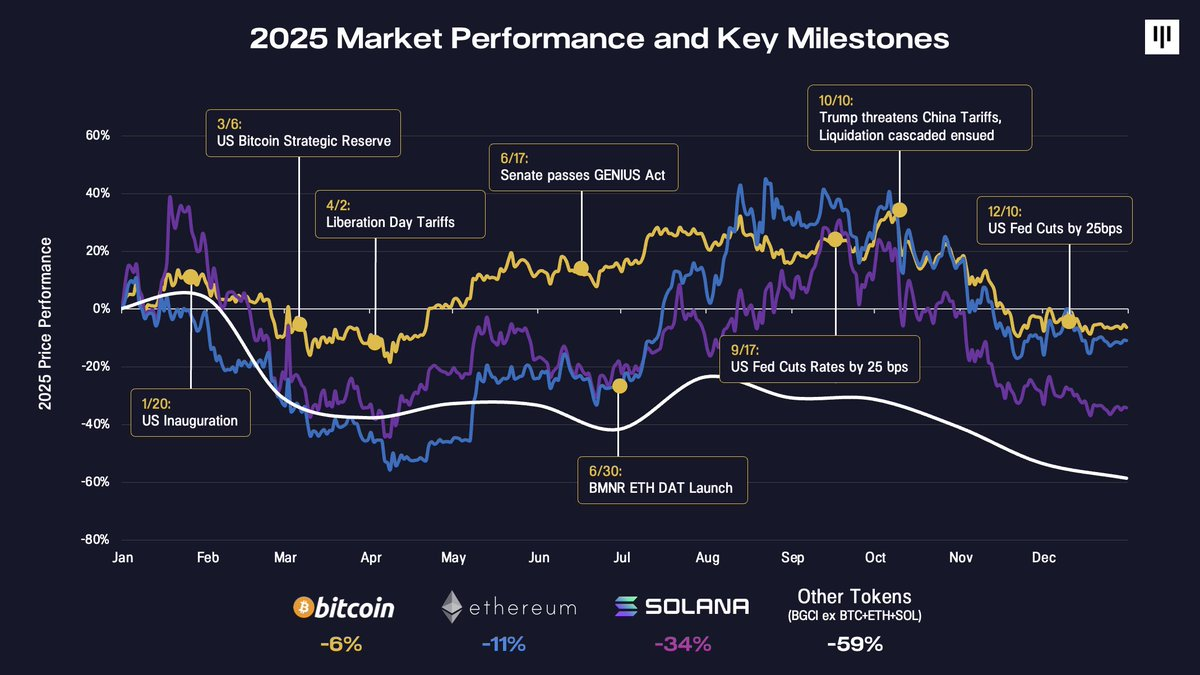

Reviewing the timeline of major macro and policy inflection points helps explain why price action was so disjointed.

The year opened with the U.S. presidential inauguration—an archetypal “buy the rumor, sell the news” moment and an early warning signal for volatility. Over the following months, risk sentiment swung repeatedly—from optimism around the announcement of a U.S. Strategic Bitcoin Reserve to renewed pressure from “Liberation Day” tariffs. Mid-year brought constructive developments, including passage of the GENIUS Act, the rise of Digital Asset Treasuries (DATs) such as Bitmine Immersion, and the Federal Reserve’s initiation of rate cuts—stabilizing market sentiment for several months.

A decisive turning point emerged in Q4, as multiple challenges converged. On October 10, a broad selloff triggered the largest cascade of liquidations in crypto history—exceeding both the Terra/Luna collapse and the FTX bankruptcy—with over $20 billion in notional positions wiped out. The market needed time to absorb this shock. Concurrently, the year’s key marginal buyers—DATs—began exhausting their incremental purchasing power. This downward momentum was further amplified by seasonal pressures, including tax-loss harvesting (particularly among ETFs and DATs), portfolio rebalancing, and year-end systematic CTA flows.

Bitcoin ended 2025 with a modest decline of ~6%. Ethereum fell ~11%. From there, performance deteriorated sharply: Solana dropped 34%, while the broader token universe (BGCI excluding BTC, ETH, and SOL) declined nearly 60%.

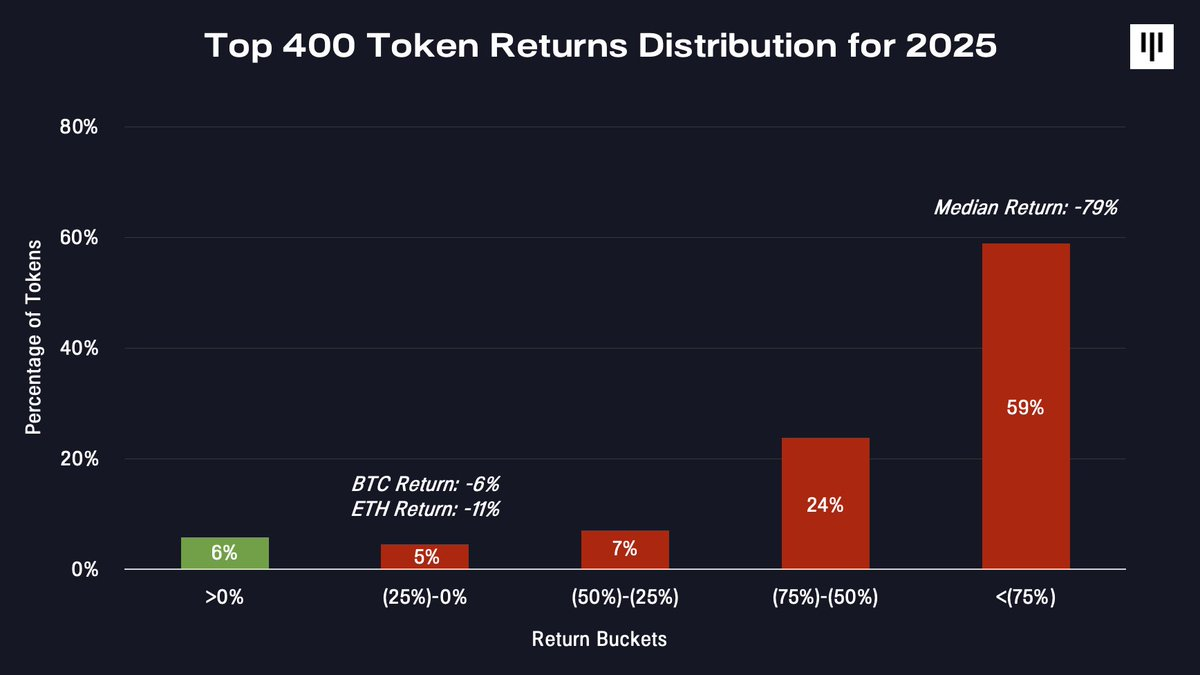

This was an extremely narrow market. When examining the return distribution across the token universe, this divergence becomes even starker.

Only a small fraction of tokens delivered positive returns. The vast majority suffered deep drawdowns—the median token fell 79%.

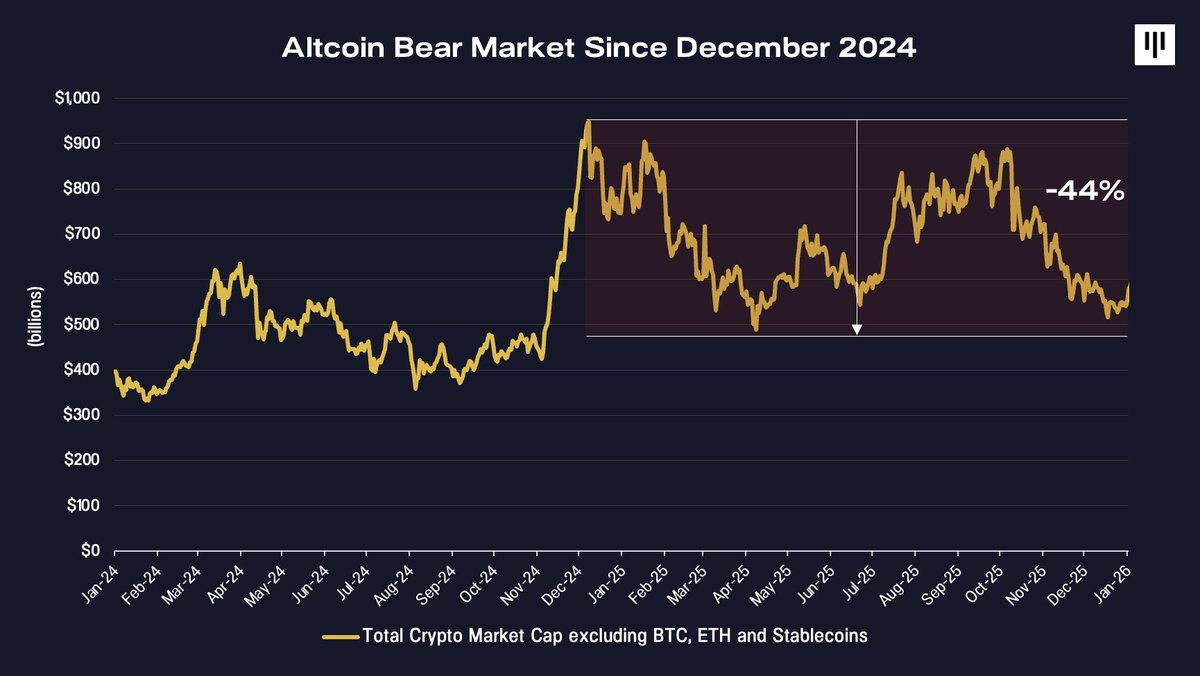

A Full-Year Altcoin Bear Market

One of the most underappreciated realities of 2025 may be that the non-Bitcoin token market effectively entered a bear market as early as December 2024.

Total market cap of cryptocurrencies excluding Bitcoin, Ethereum, and stablecoins peaked at year-end 2024 and has since been in gradual decline—down ~44% by end-2025. Viewed through this lens, a year that at times looked decent for Bitcoin represented, for the rest of the market, an ongoing, unresolved bear market.

Portfolios with significant exposure to mid- and small-cap tokens faced structural headwinds.

The divergence between Bitcoin and the broader token market reflects fundamental differences. Bitcoin benefits from a single, widely understood narrative—“digital gold”—and increasingly from mechanical demand driven by sovereign nations, governments, ETFs, and corporate treasuries. In contrast, other tokens represent a heterogeneous set of disruptive technologies, with less standardized access, weaker institutional support, and more complex value-capture dynamics.

This divergence is starkly evident in price action.

Structural Headwinds Facing Tokens

In 2025, multiple forces intensified pressure on the broader token complex.

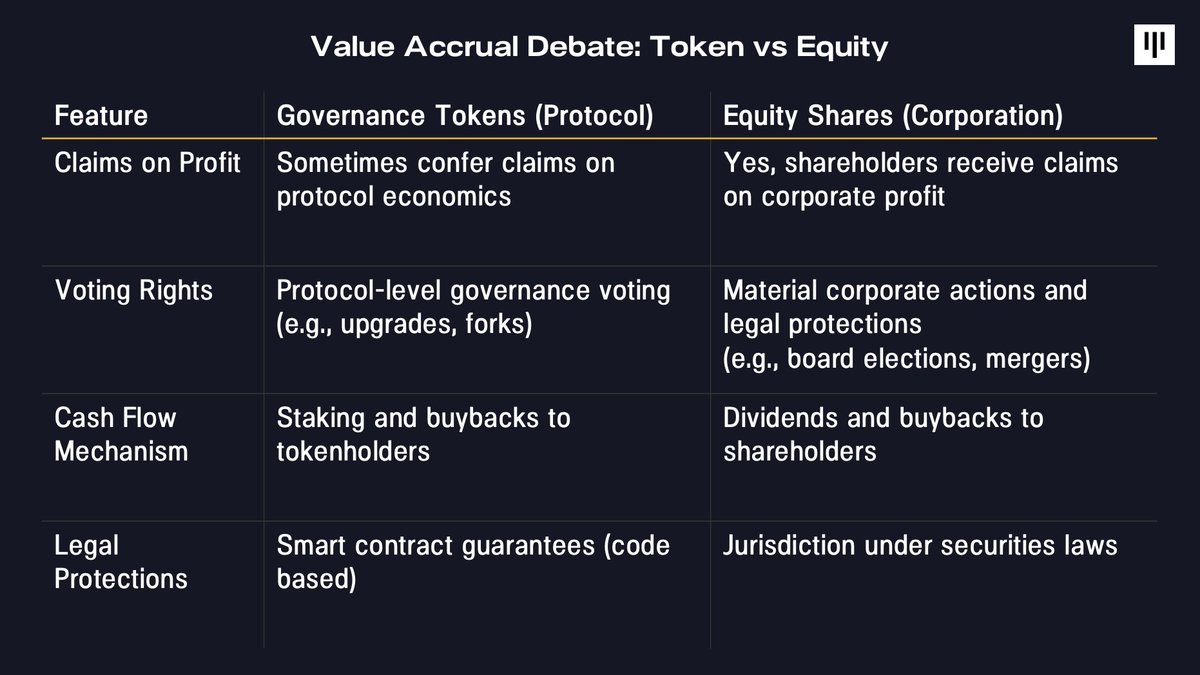

1. Value Accrual and Investor Rights

One of the most persistent challenges is the unresolved question of value accrual. In traditional equity markets, shareholders benefit from clear legal claims to cash flow, governance rights, and residual value. Tokens, by contrast, typically rely on protocol-level mechanisms enforced by code—not government-backed legal enforcement.

This tension came into sharp focus this year in several high-profile cases where token holders received no direct compensation during ecosystem acquisitions or restructurings—including Aave, Tensor, and Axelar. These events reverberated across the market, eroding confidence even in projects with relatively strong tokenomics.

Against this backdrop, digital asset equities outperformed tokens, benefiting from clearer value-capture pathways at a time when investors were already seeking defensive assets.

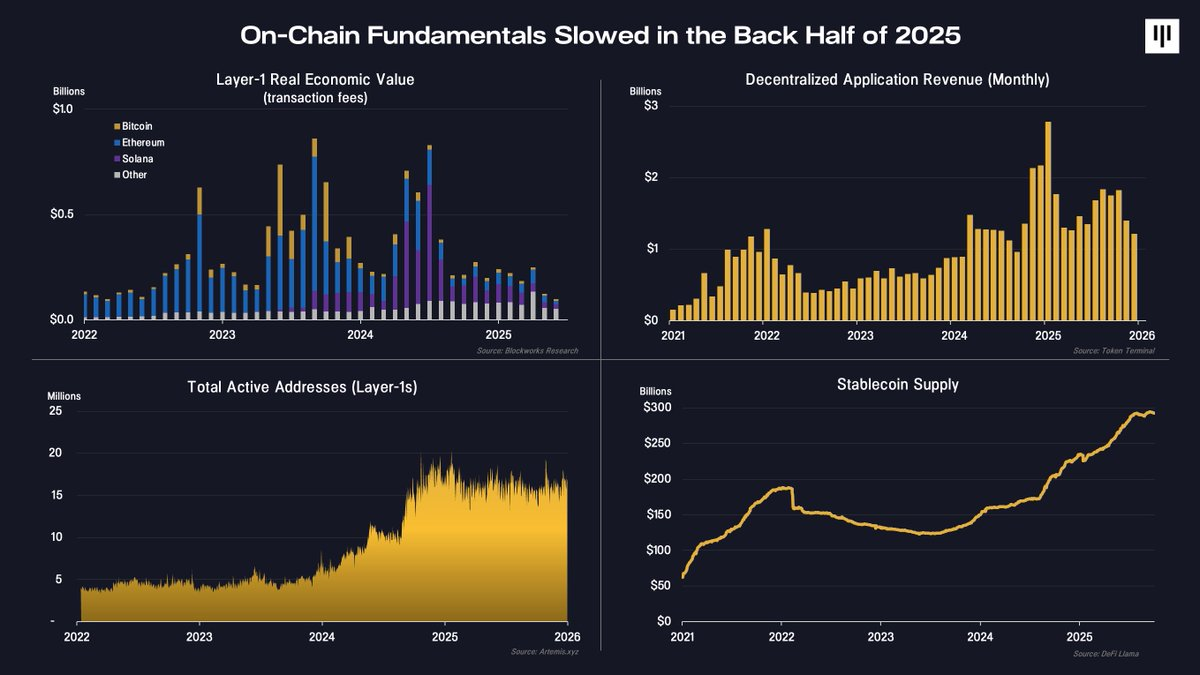

2. Slowing On-Chain Activity

On-chain fundamentals also softened in the second half of the year.

Key metrics—including Layer-1 revenue, DeFi application fees, and active addresses—showed decelerating activity. Notably, stablecoin supply continued growing, signaling sustained adoption of blockchains for payments and settlement. However, much of the economic value associated with stablecoins flowed to off-chain, equity-based businesses—not token-based protocols.

In practice, the underlying base layer remains intact, but marginal, pro-cyclical activity has declined. This shift is directly reflected in token price action.

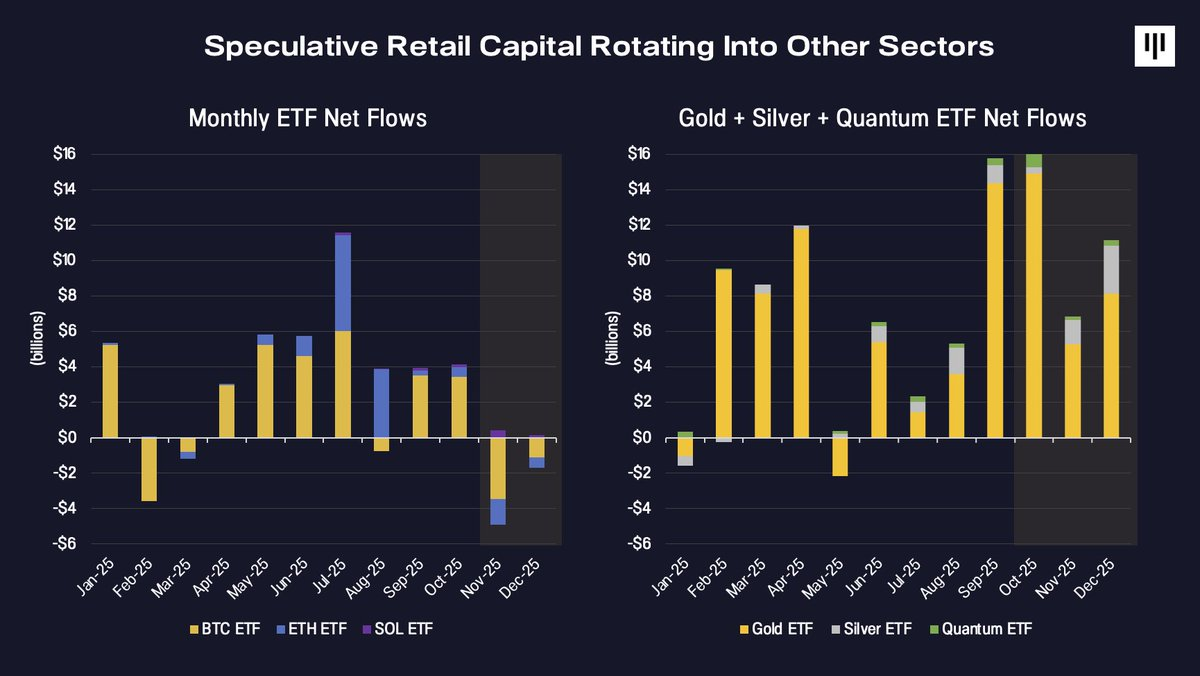

3. Rotation of Speculative Capital

Finally, capital flows reversed. Historically, marginal capital supporting the broader token space has been speculative retail. While institutional adoption continues to grow, it remains concentrated in ETF-accessible assets—including Bitcoin, Ethereum, and, by year-end, Solana.

In 2025, speculative attention shifted elsewhere.

ETF inflows surged into gold, silver, and emerging thematic trades (e.g., quantum computing), while digital asset ETF flows slowed and turned negative by year-end. This rotation coincided precisely with worsening token breadth, reinforcing downward momentum.

Sentiment, Positioning, and Historical Context

By year-end, sentiment had compressed to historically low levels associated with capitulation.

The Fear & Greed Index reached readings last seen during acute stress periods—including post-FTX collapse. Simultaneously, perpetual futures funding rates declined, signaling reduced leverage and diminished speculative excess.

Seasonality also played a role. December has historically been a weak month for Bitcoin and the broader crypto market, with tax-loss harvesting, portfolio rebalancing, and liquidity constraints generating mechanical pressure independent of fundamentals.

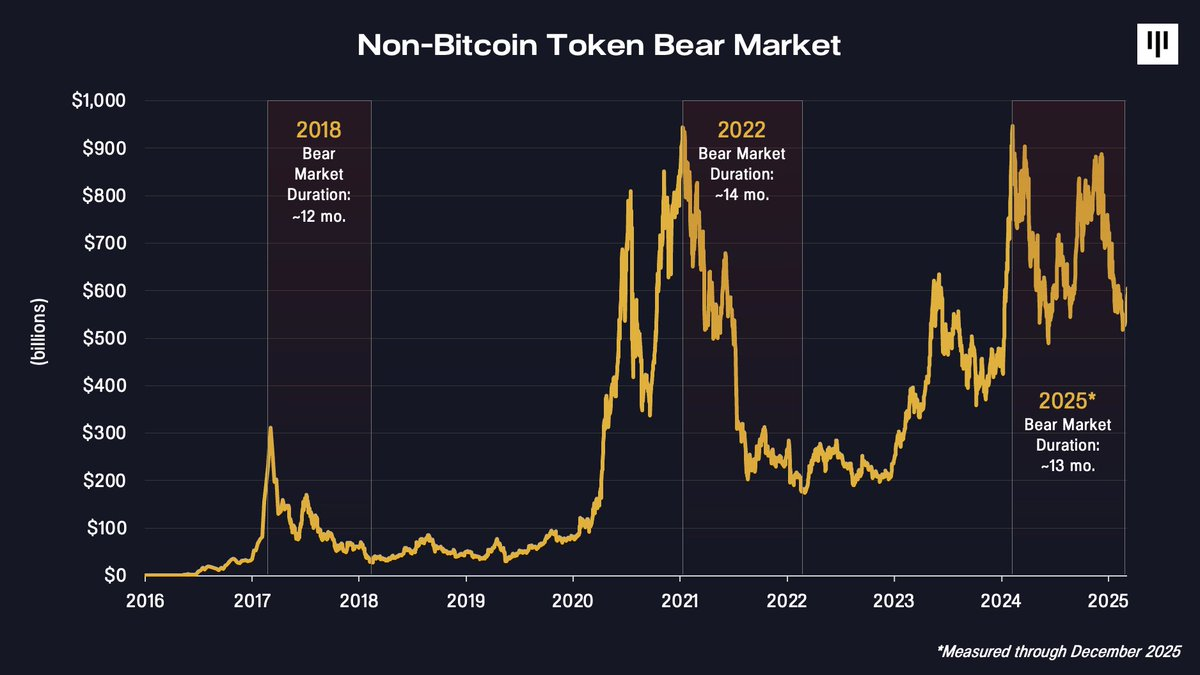

Importantly, viewed over a longer horizon, the duration of the current non-Bitcoin drawdown aligns closely with prior cycles.

The bear markets of 2018 and 2022 lasted approximately 12–14 months. Measured from the December 2024 peak, the current drawdown now falls squarely within that range. This does not guarantee a bottom—but it does indicate that substantial time- and price-based compression has already occurred.

Why the Outlook Improves from Here

Despite 2025’s challenges, several reasons justify constructive optimism going forward.

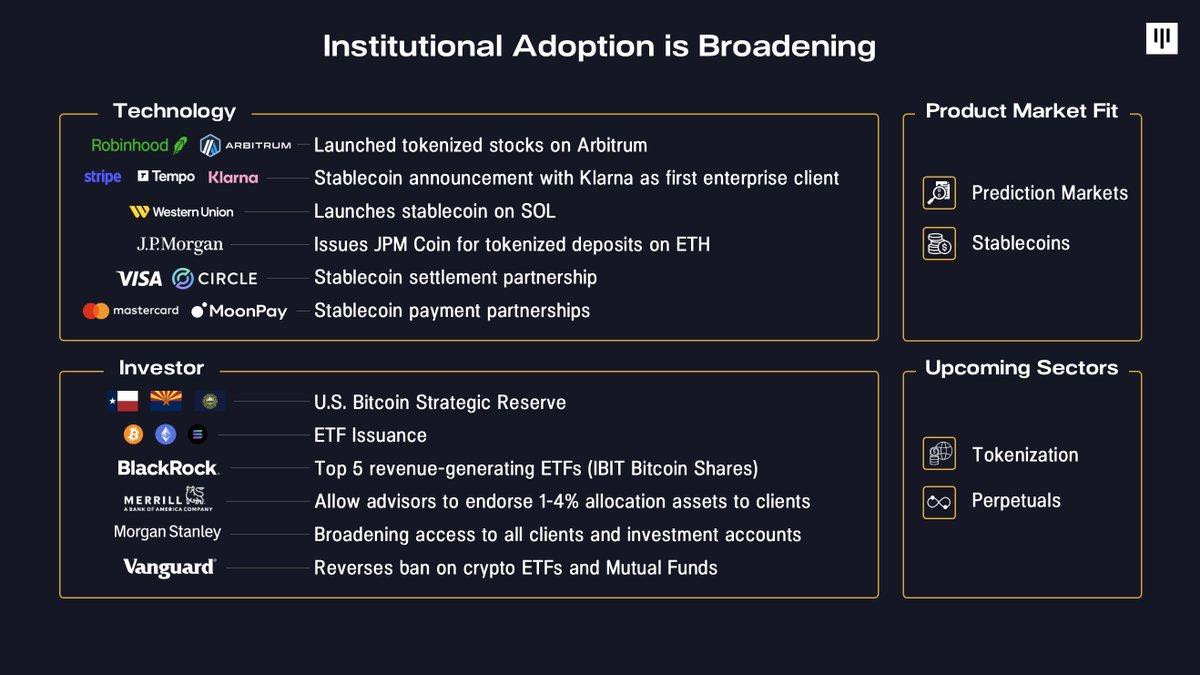

First, institutional adoption continues expanding. Corporations are increasingly integrating blockchain into core products—from Robinhood launching tokenized stocks to Stripe developing stablecoin infrastructure to JPMorgan tokenizing deposits. On the capital side, sovereign reserves have been established, and broker-dealers, retirement platforms, and large asset managers have dramatically lowered participation barriers.

Second, product-market fit is becoming clearer. Stablecoins and prediction markets gained breakout attention and adoption in 2025 as standout use cases, while broader tokenization and perpetual futures show early signs of product-market fit.

Third, the macro backdrop is supportive. The U.S. economy remains resilient, wage growth exceeds inflation, and corporate earnings are expanding. With the Fed having halted quantitative tightening, liquidity conditions are improving. Falling long-term yields combined with accommodative monetary policy have historically been constructive for risk assets—including digital assets.

Finally, penetration remains strikingly low. As Bitmine’s Tom Lee noted: Only 4.4 million Bitcoin addresses hold over $10,000 in value—versus 900 million traditional investment accounts globally. According to Bank of America’s institutional investor survey, 67% of professional portfolio managers still maintain zero digital asset exposure. Even modest allocation shifts over time would represent a significant source of latent demand.

Conclusion

2025 was a difficult year for most of the token market—characterized by extreme divergence, stronger performance among major coins, and prolonged weakness outside Bitcoin. Yet it was also a year that advanced institutional adoption, clarified product-market fit, and compressed valuations across much of the ecosystem.

A robust fundamental backdrop following a full-year altcoin bear market may present opportunity. With sentiment cleansed, leverage reduced, and a major repricing already behind us, forward-looking allocations appear increasingly asymmetric—provided fundamentals remain stable and breadth returns. Historically, periods of disorder lay the groundwork for the next phase of growth.

[1] Bloomberg Galaxy Crypto Index (BGCI) performance is shown net of fees that would reduce returns. Any index is for reference only and serves solely as a general illustration of market performance. No index can be directly compared to Pantera Fund performance, partly because indices are not actively managed. Pantera Fund investment results are not intended to predict or imply future returns of the Pantera Fund.

PANTERA RETROSPECTIVE — Looking Back at 2025

Author: @JonathanGieg

As we enter 2026, we expect the coming year to be more exciting for crypto than the last. But before turning the page, we’d like to take a moment to reflect on what 2025 brought.

2025 was a landmark year for Pantera. We deployed more capital than ever before, led most of our new investments, and expanded our global footprint across industries and regions we believe will define crypto’s next decade. At the same time, our portfolio achieved strong public-market validation—four portfolio companies went public or announced major strategic acquisitions.

Read about our progress in 2025:

Nine Predictions for 2026

Author: @veradittakit

#1 Real-World Assets (RWA) Take Off

As of mid-December 2025, RWA total value locked (TVL) reached $16.6 billion—approximately 14% of total DeFi TVL.

Predictions:

· U.S. Treasury and private credit tokenization could double at minimum.

· Tokenized equities and stocks may grow faster once the SEC’s anticipated “Innovation Exemption” under its “Crypto Project” is launched.

· An unexpected sector—carbon credits, mining rights, or energy projects—will explode. These areas are characterized by fragmented liquidity, global dispersion, and lack of standards—precisely where blockchain-based markets can help solve critical pain points.

#2 AI Revolutionizes On-Chain Security

AI-powered security and blockchain development tools have become extraordinarily powerful. Real-time fraud detection, 95%-accurate Bitcoin transaction labeling, and instant smart contract debugging are now live—and have already detected multi-million-dollar blockchain vulnerabilities.

Prediction: In 2026, envision a larger shift toward on-chain intelligence—where deterministic, verifiable rules govern smart-contract-based governance. This application will scan code near-instantly, immediately flag logic errors and vulnerabilities, and provide real-time debugging feedback. The next major unicorn will be an innovative on-chain security firm that boosts security by 100x.

#3 Prediction Markets Become Acquisition Targets

$28 billion traded across the top 10 prediction markets in the first 10 months of 2025—spurring consolidation around institutional infrastructure. On the week of October 20, we hit a record $2.3 billion.

Prediction: The industry will see a >$1B acquisition—not involving Polymarket or Kalshi. The winning platform will build in native liquidity rails and embedded market-discovery intelligence—identifying where capital hides and why. Forget flashy new buttons. This is entirely about effortlessly empowering users with superpowers: instant access to hidden liquidity pools, smarter routing, and predictive order flow.

Sports-focused platforms like DraftKings and FanDuel are now mainstream, partnering with media for real-time odds distribution. New entrants focused on sports—like NoVig—will vertically scale their presence, and new startups will emerge across Asia-Pacific, a region worth watching.

#4 AI Becomes Your Personal Crypto Copilot

As systems mature and deliver hyper-personalized experiences aligned with user expectations, consumer AI platform usage will surge. Seamless integration makes advanced AI feel effortless—shifting usage from clunky to instantaneous.

Prediction: Platforms like Surf.ai will attract users ranging from crypto-curious newcomers to active traders in 2026—powered by intuitive, state-of-the-art AI models, proprietary crypto datasets, and multi-step workflow agents. I believe complex technology paired with accessible design makes Surf the go-to crypto research tool—delivering market insights with on-chain support four times faster than generic alternatives on other platforms.

#5 Banking Giants Prepare: G7-Linked Stablecoins Are Imminent

Ten major banks are in early-stage exploration of issuing consortium stablecoins pegged to G7 currencies. Financial institutions are assessing whether industry-wide stablecoins can deliver the benefits of digital currency to individuals and institutions—compliantly and with sound risk management. Meanwhile, a group of ten European banks is investigating issuance of euro-pegged stablecoins.

Prediction: A major banking consortium will launch its own stablecoin—whether via these pilot programs in 2026 or through a different alliance.

#6 Privacy, Payments, Perps: The Institutional Triumvirate

Privacy technologies thrive in institutional use—Zama, Canton, and others offer transparent-confidential combinations—even as retail adoption lacks traction or scalability. Stablecoins now stand at $310 billion—more than doubling in market cap since 2023 and expanding for 25 consecutive months. Perpetual swap contracts now account for ~78% of crypto derivatives volume, with the gap between perps and spot options continuing to widen.

Prediction: For privacy, the institutional-retail gap will widen in 2026. Stablecoins have a long-term path to >$2 trillion—reaching at least $500 billion next year—and perpetuals’ momentum will continue through 2026.

#7 Institutional Macro Lens

As of December 15, 17.9% of BTC supply is now held by public and private companies, ETFs, and nation-states.

Prediction: 2026 won’t be about hype or memes. It will be about consolidation, genuine compliance, and institutional capital driven by public-market liquidity. Crypto will integrate into mainstream platforms, upgrade financial rails, and challenge incumbents.

#8 The Largest Crypto IPO Year Ever

2025 saw 335 U.S. IPOs—up 55% overall versus 2024; many were crypto-friendly, including nine blockchain IPOs. These included crypto-native firms like Circle Internet Group (listed May 27, 2025) and crypto-inclusive SPACs—for example, Bitcoin Infrastructure Acquisition Corp, listed December 2, 2025.

Prediction: 2026 will be an even bigger year for digital asset public listings. Coinbase reports that 76% of firms plan to add tokenized assets in 2026, with some targeting >5% of their entire portfolios. Morpho, as one example protocol, held $8.6B TVL as of November 2025.

#9 Accelerating Digital Asset Treasury Integration

In 2021, fewer than 10 publicly traded companies held Bitcoin. By mid-December 2025, 151 public companies held $95 billion—including governments, the count rose to 164 entities holding $148 billion.

Prediction: 2026 will see brutal pruning. Across each major asset class, only one or two players will dominate. Everyone else will either be acquired or left behind—except for one long-tail token winner that follows along. It’s also globalizing. Japan’s Metaplanet is already aggressive—so the U.S. no longer owns this trend, as the global treasury landscape diversifies.

Wishing you a successful 2026.

For more, read our Pantera Blockchain Letter.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News