Primary Market's Moonshot AI and DeepSeek, Where Does the Valuation Narrative "Premium" Come From?

TechFlow Selected TechFlow Selected

Primary Market's Moonshot AI and DeepSeek, Where Does the Valuation Narrative "Premium" Come From?

Moonshot AI is more about "financial premium" and "performance premium", while DeepSeek has many non-"financial premium" factors.

Author: MD

Produced by: Bright Company

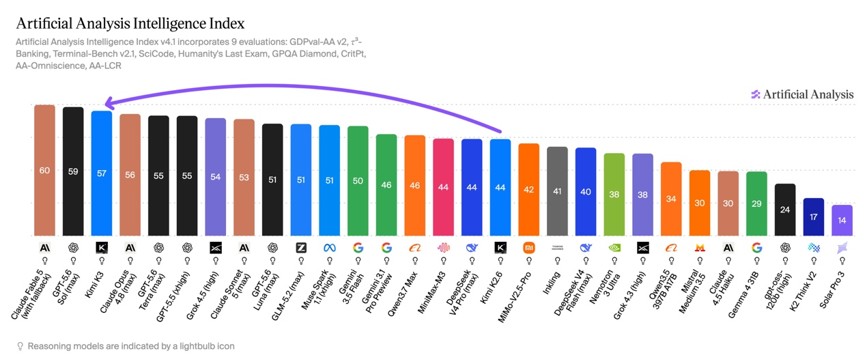

Recently, MoonShot AI released its latest model version Kimi K3, attracting high attention from the capital market due to its leading performance in various scores. According to MoonShot AI's introduction on X, K3 is a multimodal model with 2.8 trillion parameters, supporting 1 million token context, featuring native visual capabilities, and adopting multiple innovative technologies.

Artificial Analysis stated that Kimi K3 scored 57 on the Artificial Analysis Intelligence Index. Its intelligence level is comparable to Opus 4.8 and GPT-5.5, but still lags behind Fable 5 and GPT-5.6 Sol. MoonShot AI has stated plans to release the weights of this 2.8T parameter model, which will make it a leading open-source model.

In the AI Arena Code rankings, K3 even leads ahead of Anthropic's Fable 5, Gpt5.6-sol, and Zhipu's GLM-5.2 (max). Previously, MoonShot AI completed its last round of financing with a post-money valuation of approximately 31.5 billion USD. If looking solely at leaderboard performance rankings, MoonShot AI's valuation level is far lower than Anthropic and OpenAI.

Another Chinese AI company receiving significant attention in the primary market is DeepSeek. According to The Information and Bloomberg citing knowledgeable sources, DeepSeek is advancing its second financing at a 74 billion USD valuation, only one month after its first round pre-money valuation of 54.3 billion USD was finalized.

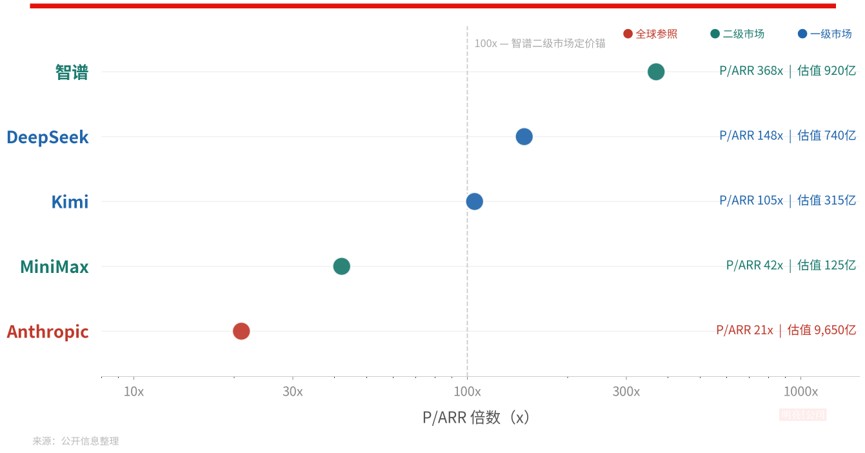

From a valuation perspective, DeepSeek and MoonShot AI, two primary market companies, are approaching or even surpassing comparable targets in the secondary market. Perhaps due to limitations in liquidity and information transparency in the primary market, Zhipu and MiniMax have undergone continuous pricing in the public market for over half a year, and the narrative consensus has become quite clear—whether rewarded or punished by the market; whereas although DeepSeek and MoonShot AI's valuations are more aggressive, the narratives surrounding them have not fully formed.

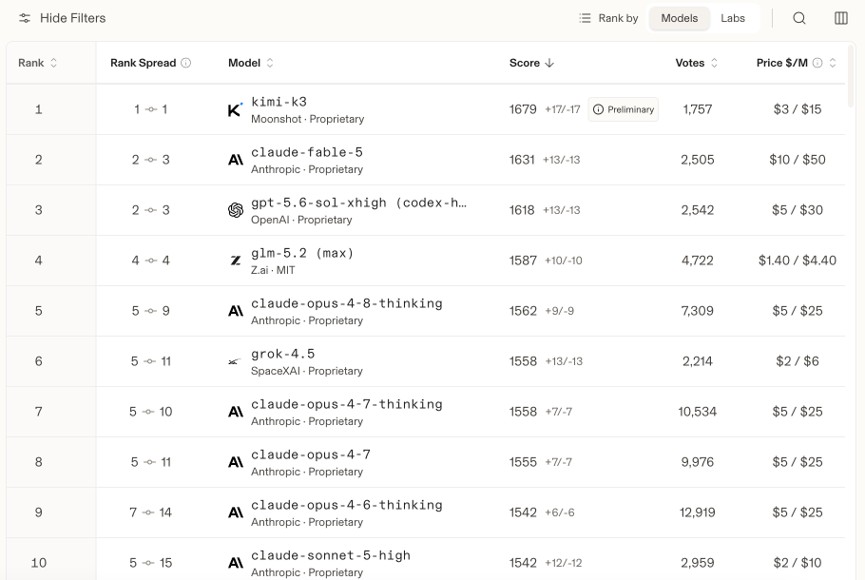

Kimi-K3 temporarily ranks first on the Arena AI Code leaderboard (Source: Arena AI)

Narratives of Two Companies in the Secondary Market: Coding Performance and ARR Growth Slope

The listings of Zhipu (02513.HK) and MiniMax (00100.HK) have provided a valuation line for independent Chinese model vendors. If looking at P/ARR, their narrative clarity and ARR growth rate determine the premium magnitude.

Since listing on the HK Stock Exchange in January this year, Zhipu's stock price has surged over 1000%, with a market cap of approximately 92 billion USD. Supporting this price is a rarely steep revenue curve: ARR increased from 67 million USD in January to 1 billion USD in July, a 15-fold growth in 7 months, completing the full-year target half a year early—multiple brokerages pointed out that this slope exceeded Anthropic's record of completing 100 million to 1 billion USD ARR in 15 months back then. Latest information from 36Kr shows that Zhipu's ARR has already reached 1 billion USD, far faster than the expectation of reaching 1 billion USD by the end of the year.

MiniMax's market cap has retraced approximately 75% from the listing high of about 410 billion HKD to about 81 billion HKD, implying a P/ARR of about 13 times. "Bright Company" has recently discussed the challenges of MiniMax's valuation narrative: when the industry main thread shifts to Coding and Agent, MiniMax's "full-modality, C+B dual-wheel" multi-line layout has instead become the object of market questioning.

Active Financing in the Primary Market

DeepSeek's first round of financing was signed at the end of May: scale exceeded 50 billion RMB, approximately 7.4 billion USD, creating the largest single round in the history of Chinese AI large models.

According to The Information, the company clearly informed investors during the first round roadshow: no intention to commercialize the model, focusing on frontier R&D, no clear IPO timeline. Liang Wenfeng began planning the second round before the first round of financing was officially completed. The terms of this round underwent a fundamental shift: valuation rose to 74 billion USD, a jump of approximately 36% compared to the first round.

The Information also stated that DeepSeek has planned to submit an application this year and list on the Shanghai STAR Market in 2027. The core factor driving all this is the huge computing power expenses required for model R&D.

MoonShot AI's financing rhythm is equally rare: post-money valuation at the end of 2025 was only 4.3 billion USD; completed 2 billion USD financing in May 2026, post-money 20 billion USD, new round launched on June 30, pre-money valuation 31.5 billion USD, valuation increased over 7 times in half a year.

Both DeepSeek and MoonShot AI have obtained very high primary market valuations, but the logic supporting the valuations seems different. The former relies more on call volume, technical influence, and efficiency engineering; the latter seems more like replicating Anthropic's early revenue curve.

According to knowledgeable sources revealing to The Information, DeepSeek's recent annualized revenue has reached 400-500 million USD, mainly from API services; calculated at the upper limit of 500 million USD, a 74 billion USD valuation corresponds to approximately 148 times P/ARR—not only the most expensive among the four Chinese companies, but also far exceeding many American AI startups.

If analyzed, the reasons supporting this multiple may come from three aspects.

First is call volume.

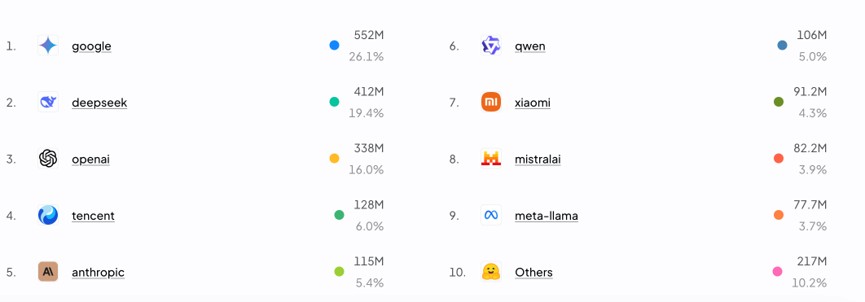

CMB International's July 3 report shows that as of the week of June 22, DeepSeek ranked first globally on the OpenRouter platform with 6.7 trillion tokens, exceeding Anthropic's 4.25 trillion; in Q2 2026, OpenRouter's total call volume increased from about 21 trillion to 46.66 trillion tokens, doubling in a single quarter, growth mainly contributed by Chinese open-source models, Chinese vendors' combined call volume has exceeded American vendors.

Source: OpenRouter

From OpenRouter's latest weekly market share ranking, DeepSeek is also second only to Google, ranking second in market share.

Second is efficiency engineering. V4's single token computation volume in million token context scenarios is only 1/20 of the previous generation, V4-Pro performance rivals top closed-source models, Changjiang Securities evaluates it close to Claude non-thinking mode level.

Third is validated UE. According to Bloomberg, although its API charges are only a fraction of OpenAI and Anthropic's, V4's gross sales margin remains above 50%—low price does not equal low gross margin, this is the key data point for the "computing power efficiency" narrative completing financial validation.

In addition, in terms of strategic direction, the company launched the V4 official version in mid-July and introduced a peak-valley pricing mechanism—this is its first pricing action with clear commercialization intentions; V4 deeply adapts to domestic computing power such as Huawei Ascend and Cambricon, plus direct shareholding by the National AI Fund, its strategic positioning as a "domestic computing power closed-loop model layer anchor" is clearly visible.

Looking at MoonShot AI again.

Its 31.5 billion USD pre-money valuation corresponds to approximately 105 times P/ARR; if adopting the 400-500 million USD ARR caliber given by experts on Nomura's expert conference call, it is approximately 70 times. And with the release of Kimi K3, the market generally expects the K3 model released in Q3-Q4 to open new pricing space.

Multiple brokerages compare MoonShot AI's revenue curve to Anthropic's early stage: developer call volume surge, API proportion increase, overseas payment growth, model iteration driving price system upward.

Nomura's July 6 expert conference call minutes show that experts expect its ARR to exceed 1 billion USD by the end of the year. But from public information channels, Yang Zhilin has never talked about the goal of "1 billion USD ARR by the end of the year".

Premium of Narratives: Where Does It Come From, and What Will It Face in the Secondary Market?

Comparing Zhipu's approximately 100 times and MiniMax's approximately 13 times public market pricing, the source of premium for the two primary companies is completely different.

At least from previous valuations, MoonShot AI's premium leans more towards "financial premium" and "performance premium".

If year-end ARR indeed reaches 1 billion USD, the forward multiple corresponding to 31.5 billion valuation is only about 30 times—cheaper than Zhipu's current value caliber; investors are also betting on the listing revaluation of "replicating Zhipu's path". Zhipu's last primary round valuation was 13.7 billion USD, and market cap once exceeded 100 billion USD after listing.

This type of premium is falsifiable and trackable; every month's ARR data is testing it.

And compared to MoonShot AI, DeepSeek's premium has a "non-financial premium" part: technical influence premium composed of call volume and architecture definition rights, geopolitical options brought by national strategy scarcity, "founder faith" endorsement formed by Liang Wenfeng's personal investment of 20 billion RMB... etc., especially the impact of the "DeepSeek Moment" on the revaluation of Chinese assets, which currently cannot be replicated by other vendors.

148 times static multiple cannot be self-consistent with any cash flow model; what investors are buying is the belief that "when the commercialization switch is fully opened, it has the ability to achieve Anthropic-level revenue".

However, when these two companies move towards IPO, they will face the continuous pricing mechanism of the public market, which will also make their valuation logic face some changes, or even pressure.

First is the quarterly test of growth rate.

The primary market can pay for "narratives", the secondary market pays more and more for "fulfillment". MiniMax's market also gave about 65 times P/ARR in the early listing stage; as the industry narrative shifted to Agent and its monetization path was questioned, the valuation was ground down by three-quarters.

The mid-range price band where DeepSeek is located experienced 95% inference price deflation in Q2. CMB International data shows that the optimal call price in the 40-50 intelligence index range decreased from 1.2 USD/million tokens in March to 0.058 USD in June. Whether "first in call volume" can continue to translate into revenue growth will be a mandatory question for every quarterly report.

The second aspect is the unlocking pressure on the supply side.

Zhipu and MiniMax fell 8.5% and 22.5% respectively during the July unlocking week, followed by placements totaling over 40 billion HKD—this "unlocking-placement" supply shock will similarly await DeepSeek and MoonShot AI listing in the future.

Finally is the unification of the valuation coordinate system, for example, "single token monetization rate" will become a directly comparable indicator.

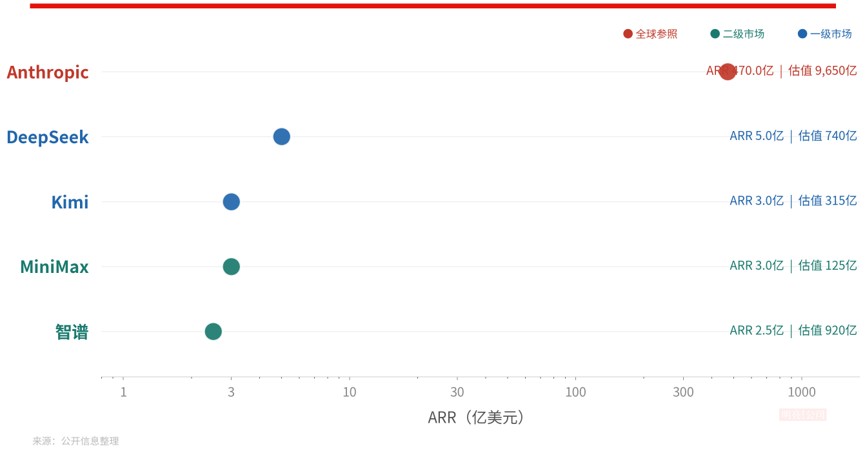

Source: Public information compilation, Bright Company (Valuation, market cap as of close of July 16, excluding Zhipu's latest rumored ARR)

In addition, at the narrative level, a benchmark object that Chinese model companies cannot bypass at this stage is Anthropic.

Anthropic completed a 65 billion USD Series H financing at a 965 billion USD post-money valuation on May 28, and has confidentially submitted an IPO application. Its ARR increased from 9 billion USD at the end of 2025 to 47 billion USD in May 2026.

According to Jefferies citing SemiAnalysis, its July ARR will exceed 60 billion USD, net revenue retention rate about 500%, API gross margin over 80%, expected to achieve GAAP operating profit over 1 billion USD in Q3.

Calculated at 47 billion USD ARR, 965 billion valuation corresponds to approximately 20 times P/ARR. OpenAI has also confidentially submitted an IPO application, ARR about 25 billion USD—the former absolute leader, revenue scale has been surpassed by Anthropic.

Anthropic's valuation multiple compressed from 184 times when ARR was 100 million USD to about 20 times now.

This means DeepSeek's 148 times and MoonShot AI's 105 times are essentially advancing valuation for "revenue growth that has not yet occurred"—multiple downward trend is certain, the only variable is whether ARR upward trend can outrun multiple contraction. After Zhipu's July ARR reached 1 billion USD, its current value multiple has automatically been significantly digested from the beginning of the year level.

In addition, at the "geopolitical competition level", Jefferies hinted in its July 13 report that as American vendors obtain more new generation computing power in the second half of the year, plus anti-distillation mechanisms, there is a possibility that the capability gap between Chinese and American models may widen again.

All current valuation logic of Chinese models—from Zhipu's 100 times to DeepSeek's 148 times—implies the premise of "capability gap continuously narrowing"; at least the release of K3, from the current view, offsets the judgment of "capability gap widening" to some extent.

Currently, whether from financing valuation or model performance, MoonShot AI and DeepSeek perform optimistically.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News