Jefferies Research Report Analysis: Optical Module Market to Triple by 2027, 1.6T Still 30% Short, But InP is the Key

TechFlow Selected TechFlow Selected

Jefferies Research Report Analysis: Optical Module Market to Triple by 2027, 1.6T Still 30% Short, But InP is the Key

To see where the capital that tripled in optical modules is flowing, one must clearly identify who controls the irreplaceable links.

Written by: Rita

TechFlow Guide

Jefferies gave a core judgment at an optical expert conference call held on July 15: demand for optical modules is rising too fast, and supply cannot keep up. 800G is short by 10%, 1.6T is short by 30%, and the entire market size in 2027 will triple compared to 2025.

Behind the shortage is US companies blocking upstream chips, while China has advantages in passive components and Indium Phosphide (InP) substrates. The optical module market will triple, but where the money flows makes a difference.

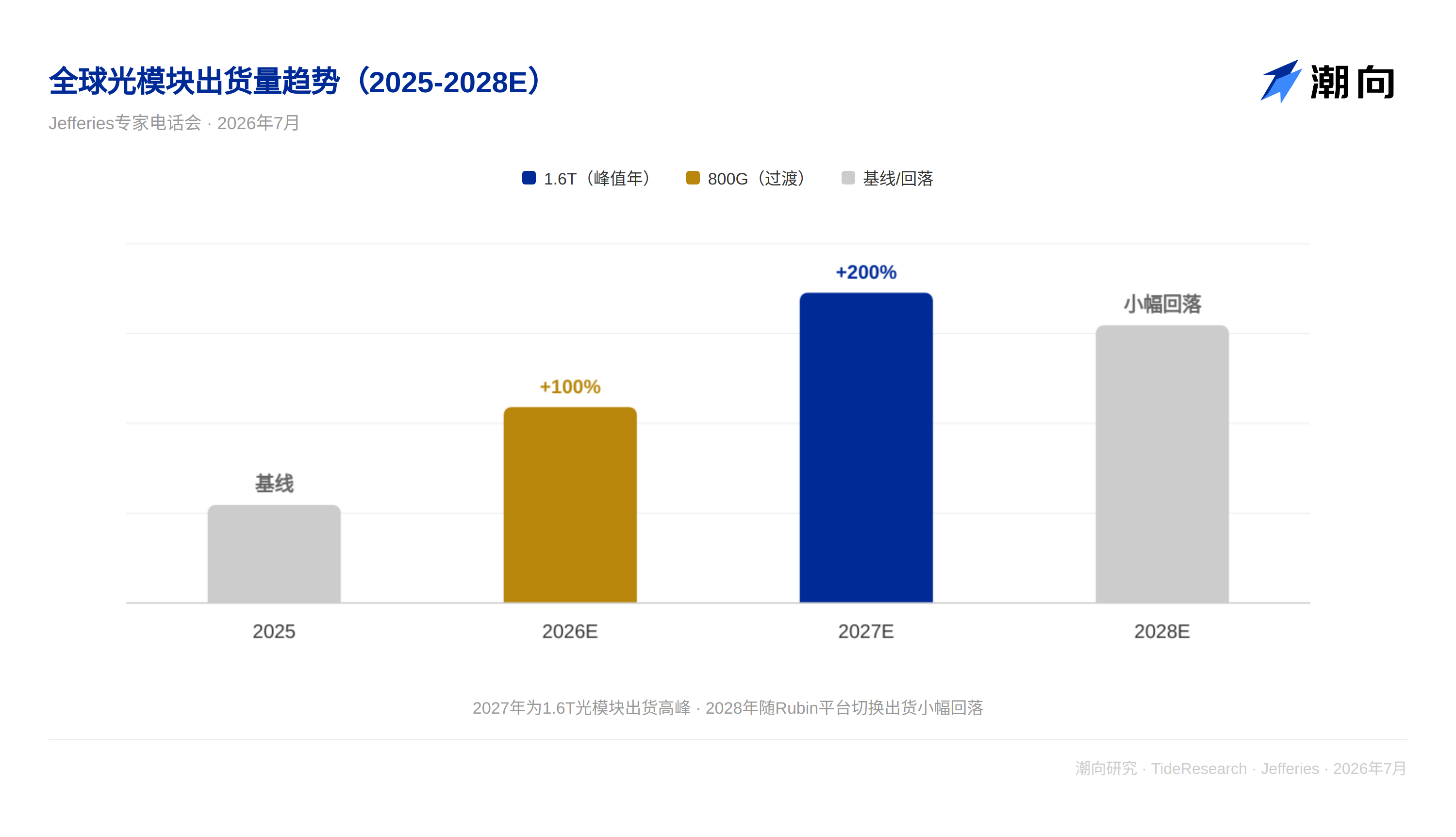

Optical Modules Triple, 1.6T Still Short 30%

The demand side is clear. 800G optical modules shipments in 2026 will be about 40-42 million units, demand exceeds 45 million units, a shortage of about 10%. 2027 shipments are expected to surge to 80 million units, with a slight decline in 2028.

The 1.6T gap is larger. 2026 shipments about 18 million units, demand about 26 million units, 30% shortage. 2027 shipments expected 55 million units, demand exceeds 75 million units, still 30% shortage.

3.2T samples are expected to ship in Q4 2026, small-scale commercial use waits until Q4 2027. In 2028, 1.6T shipments are expected to surge to 100 million units, 3.2T starting at about 2.5 million units.

At this pace, the 2027 optical module market will be three times that of 2025.

DSP and 200G EML Blocked by the US

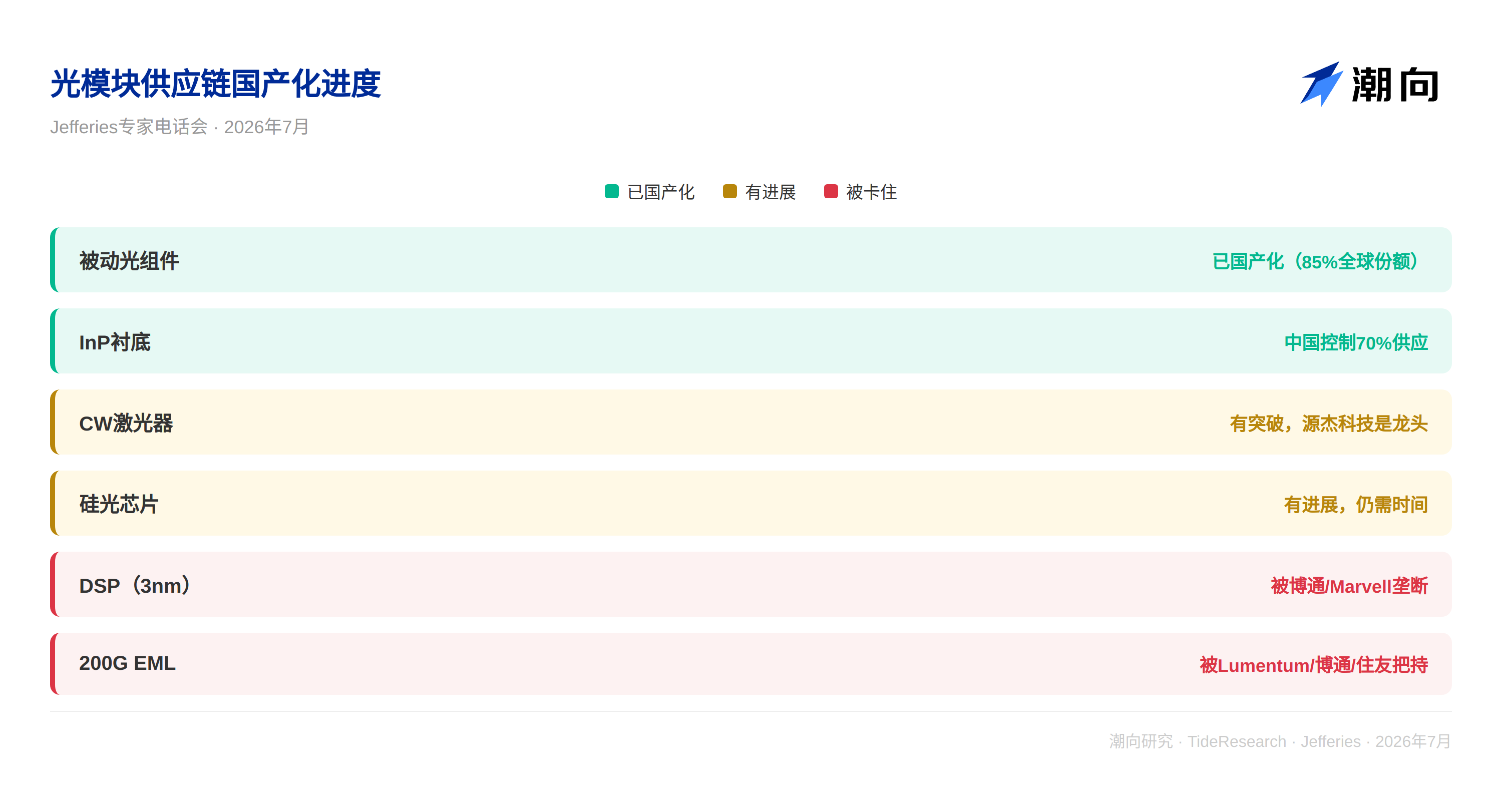

The upstream bottleneck for optical modules lies in DSP and 200G EML.

3nm DSP chips used for 1.6T are monopolized by Broadcom and Marvell. 200G EML is controlled by Lumentum, Broadcom, and Sumitomo Electric. China currently has no mature 200G EML suppliers; Desay Battery is expected to start mass production in the second half of 2026.

China's localization progress varies in speed. For passive optical components (isolators, filters, lenses, AWG), China already accounts for 85% of the global share. In terms of CW lasers, Yuanjie Technology is the leader, with four others working on it. Electrical chips and silicon photonics chips have progress, but still need time.

In the optical module complete machine segment, Zhongji Innolight, Eoptolink, Accelink Technologies, and Tfc Optical Communication are the main players.

Material Route's Key Factor: InP Irreplaceable

The 800G era belongs to EML. By 1.6T, silicon photonics solutions are expected to take over 60% of market share—15% lower power consumption, lower cost (only need 2-4 CW lasers, EML solution needs 8), higher integration. But by 3.2T, EML will dominate again, because silicon photonics frequency is not high enough.

More critically, no matter which technical route is taken, Indium Phosphide (InP) cannot be avoided. EML needs InP substrates, and CW lasers needed for silicon photonics and CPO solutions also use InP. China controls 70% of global InP supply; Yunnan Germanium Industry is the core target.

Thin-film lithium niobate may become a new modulation material in the 3.2T era, but it is only responsible for modulation function; the light source still relies on InP-based CW lasers. Therefore, InP is irreplaceable in data center optical interconnect solutions.

TechFlow Perspective

Optical module demand is certain, but the upstream supply pattern determines profit distribution. US companies are blocking DSP and high-end EML, Chinese companies are blocking InP substrates and passive components. Where the money from the tripled optical module market flows depends on seeing clearly who controls the irreplaceable links.

For investors, the two directions most worth watching: first, the InP supply chain (70% of global supply is in China), second, China's breakthrough progress in 200G EML (Desay Battery mass production in the second half of the year is a key node).

Disclaimer

This article is a compilation and interpretation by TechFlow Research of a third-party securities firm research report (Jefferies, July 16, 2026). The ratings, target prices, earnings forecasts, and related judgments cited in the text are the views of the securities firm analysts, represent only their affiliated institution's stance, do not represent the views of TechFlow Research, and do not constitute any investment advice.

The market has risks, decisions must be independent. This article should not be used as a basis for buying or selling any securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News