DWF Ventures: The company concealed its most profitable phase—eight years—before going public. Can on-chain pre-IPO offerings allow retail investors to get a piece of the action?

TechFlow Selected TechFlow Selected

DWF Ventures: The company concealed its most profitable phase—eight years—before going public. Can on-chain pre-IPO offerings allow retail investors to get a piece of the action?

It is both a new channel for participating in early-stage projects and potentially a new trap for paying for the illusion of liquidity.

Author: DWF Ventures

Compiled and translated by TechFlow

TechFlow Intro: The average time for companies to go public has stretched from five years in the 1990s to twelve years today—meaning the most valuable growth phases of star companies like SpaceX and OpenAI are fully captured behind closed doors in private markets. Cryptocurrencies are disrupting this dynamic through tokenization—but reality shows pre-IPO tokens commonly trade at a 20–40% premium, suffer from poor liquidity, and operate under regulatory uncertainty. For investors, this represents both a new channel to access early-stage projects—and potentially a new trap where they pay for an illusion of liquidity.

Key Takeaways

Companies remain private significantly longer—the average IPO timeline has doubled since the 1990s. This concentrates the most valuable growth phase within private markets, driving retail demand toward on-chain alternatives.

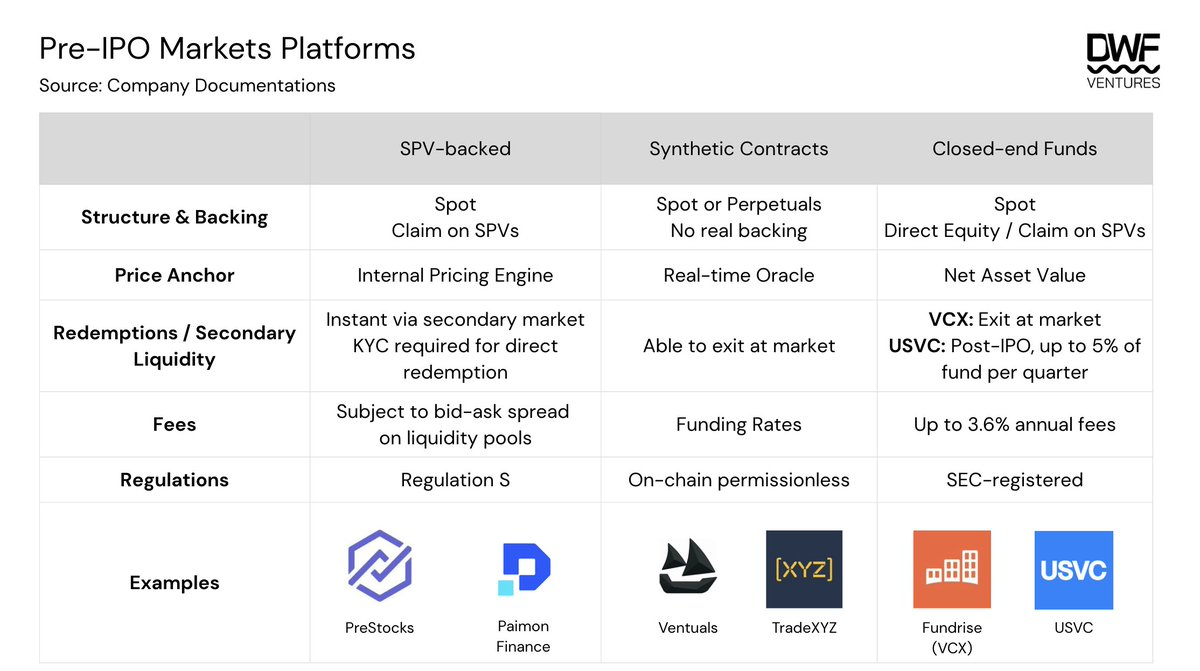

Three structurally distinct investment models have emerged: SPV-backed tokens, synthetic perpetual contracts, and closed-end funds. Each differs in underlying support mechanism, price anchoring, redemption terms, and regulatory treatment—catering to investors with varying risk appetites.

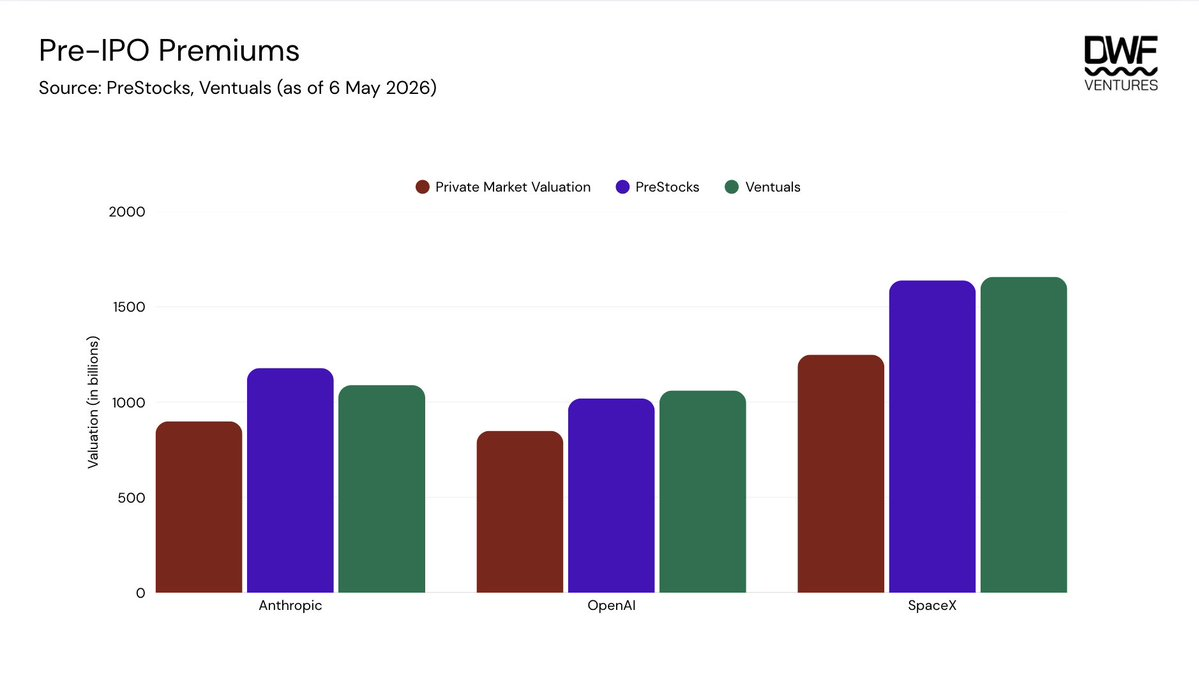

Pre-IPO stocks typically trade at a persistent 20–40% premium over the last known private-market valuation, and most platforms lack short-selling mechanisms to correct mispricing.

As demand expands beyond the retail level, platforms capable of solving liquidity challenges—and addressing all the risks outlined in this report—stand to capture enormous opportunity.

Market Context

Public markets were founded on a simple premise: democratizing wealth accumulation for ordinary investors. Traditionally, IPOs served as the primary route for startups to access larger capital pools—to fund further growth and raise brand visibility. This enabled investors to gain exposure to early-stage companies and earn returns as those companies matured. Yet with increasing participation from private capital and institutional players, enhanced price discovery has become confined to private markets.

This distorts the so-called “free market” nature of equity markets: IPOs have shifted from fundraising tools into liquidity events for institutions. Cryptocurrency emerged as a field designed to level the playing field—where ICOs and tokens became the default first step for any project, offering permissionless global access. That ethos has extended beyond crypto-native assets: tokenization has become a core on-chain use case. Public equities, commodities—and now pre-IPO markets—are being brought on-chain, establishing new venues for price discovery that transcend the infrastructure historically dominating these markets.

Current Market Landscape

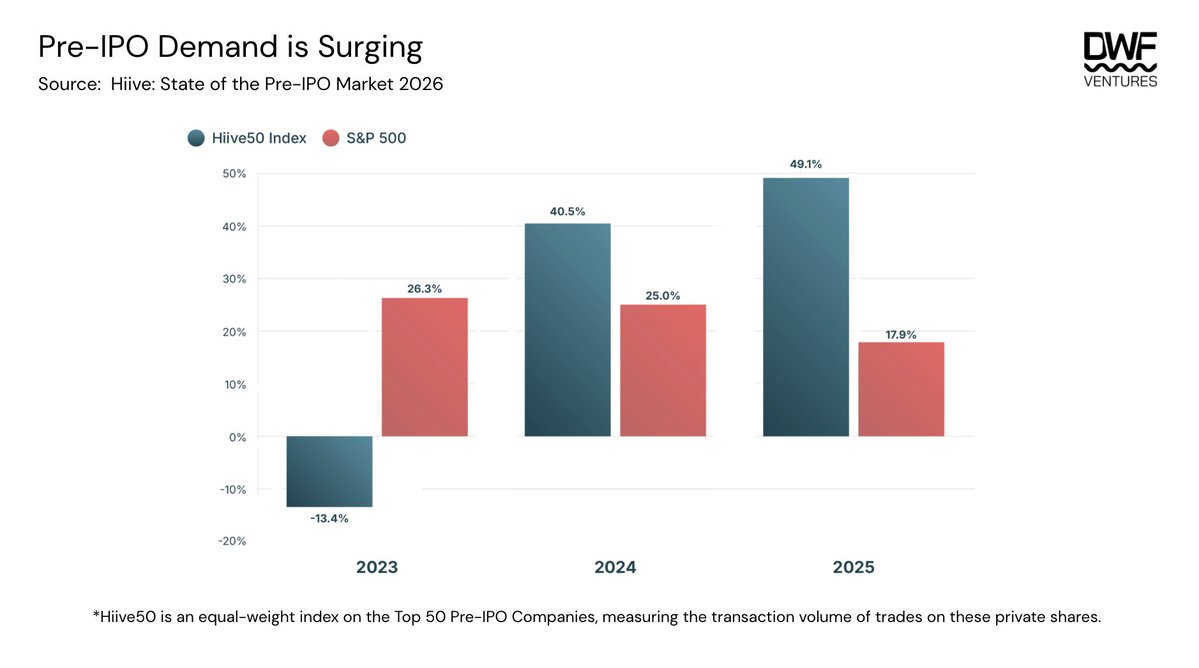

The exponential growth of the pre-IPO market stems largely from the dramatically extended timeframe required for companies to go public. Today, the average time to IPO is 12 years—up from 4–5 years in the 1990s. With companies like SpaceX, OpenAI, and Anthropic preparing for record-breaking IPO valuations, demand for private-market access has reached unprecedented levels. The private secondary market is booming: Hiive’s Pre-IPO Market Pulse Report shows its Hiive50 Secondary Market Index outperforming the S&P 500.

Demand is concentrated across several sectors—crypto, AI, and fintech. While the AI sector accounts for the largest number of companies in the index, crypto firms command significantly higher per-company stock demand. Hiive’s trading volume hit an all-time high, with top-tier companies seeing premiums surge between 100% and 200%.

Average trade size on Hiive exceeded $1 million in 2025—indicating its market serves primarily institutional buyers. This likely reflects regulatory constraints: the platform is restricted to accredited investors, who tend to write larger checks and hold investments for longer durations. As a result, retail demand for pre-IPO investment remains underserved—and on-chain competition has already begun.

Democratizing Price Discovery

Investment products available to users fall into three broad categories: SPV-backed, synthetic contracts, and closed-end funds. The table below compares each category across structure, backing, pricing and redemption mechanisms, fees, and regulation.

Structure and Backing

Investors can access exposure via spot or perpetual markets—the latter currently available only on-chain. Platforms offering spot exposure typically back their tokens with real underlying assets—either via Special Purpose Vehicles (SPVs) or direct company equity. In theory, this establishes a price floor and increases investor confidence, since these tokenized shares can ultimately be redeemed for USDC or actual shares post-IPO.

In contrast, synthetic contracts offered via perpetual markets are anchored solely to real-time oracles—with no underlying backing or claim on the reference asset. Closed-end funds like VCX and USVC involve more indirect and opaque underlying structures. Although VCX holds direct equity stakes in portfolio companies, those rights do not flow through to VCX investors. USVC’s mandate permits either direct allocations or investments in VC funds holding pre-IPO company stakes—adding an extra counterparty layer and introducing illiquidity at final redemption.

Price Anchoring

These platforms’ price oracles typically blend off-chain pricing signals—e.g., recent trades on private secondary market platforms—with on-chain mark-price moving averages driven by demand. Methodology and update frequency vary across platforms: PreStocks’ oracle lacks a fixed schedule, while Ventuals updates every three seconds. For SPV-backed platforms and registered funds, net asset value (NAV) serves as the pricing benchmark—though tokens and shares may still trade at premiums above NAV depending on investor interest, given limited issuance supply.

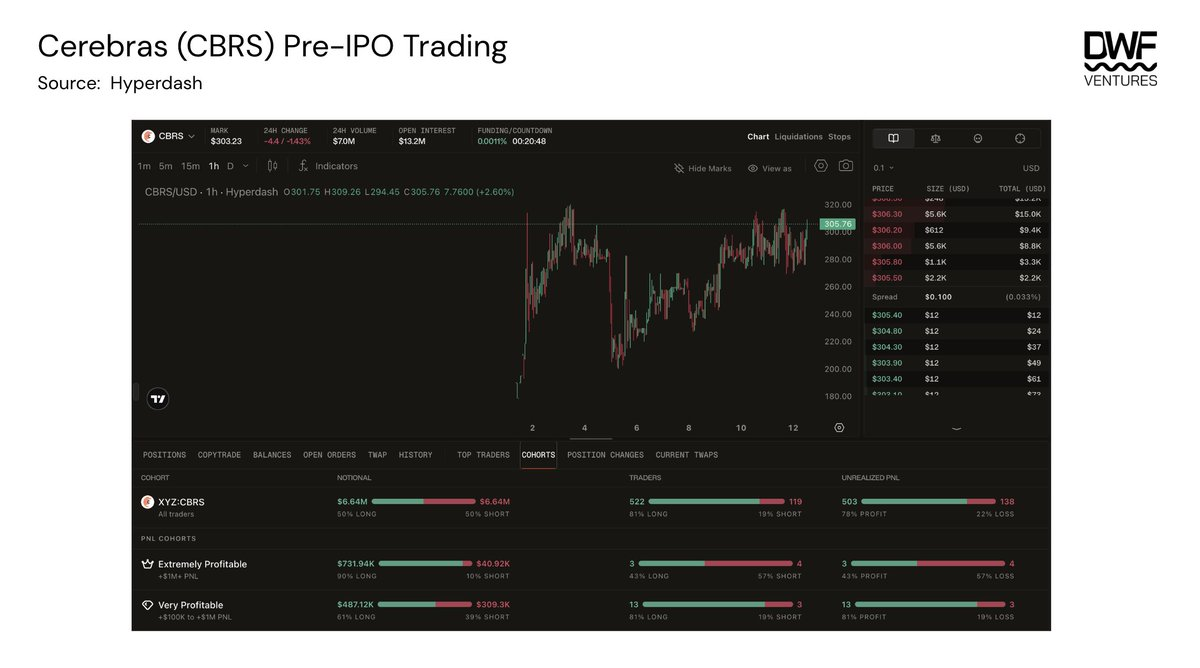

Ventuals applies additional constraints to limit volatility: mark-price changes are capped at 1% per three-second update, and the mark price itself is bounded within ±20% of the oracle price. Since the oracle price combines off-chain data with a 2-hour EMA of the mark price, this creates a bullish bias—the mark price tends to drift upward toward the upper band via reflective feedback between mark and oracle prices, especially given thin short-side liquidity. Open interest (OI) in available assets is also capped between $5M and $7.5M, constraining meaningful scale and price discovery. When the cap is reached, rising funding rates pressure existing holders to reduce positions—making it difficult to maintain large long-term exposures.

Ventuals has modified its funding rate mechanism: as the mark price approaches the ±20% band limits, funding rates increase exponentially to incentivize shorting. This helps dampen the intensity of the reflective loop and ensures optimal trading experience.

Redemption and Secondary Liquidity

On-chain platforms offer immediate exit via secondary market liquidity—though pool depth limits the size of any single exit, and most trades incur 0.5–1% slippage. As a fund, VCX offers comparable flexibility through its NYSE listing, allowing investors to exit at market price on any trading day.

Direct redemption models are more restrictive—and riskier. Redemption into USDC via SPV liquidation occurs only after the underlying position is sold on the private secondary market—a lengthy process with no defined timeline. Underlying fund structures introduce further constraints. USVC has no obligation to repurchase shares from investors; even if buybacks are offered, they’re discretionary and capped at 5% of quarterly net assets. In a post-IPO NAV decline scenario, investors may wait years for full exit—without guaranteed capital return.

Fees

Funds charge management fees, which compound rapidly when allocation flows through underlying fund managers—layering a second fee tier atop the base rate. USVC’s estimated total fee—including underlying fund fees—is 3.61% annually, a figure not prominently disclosed and one that could materially erode net returns for investors unfamiliar with the structure.

On-chain platforms charge no fixed fees, but costs are embedded in bid-ask spreads for each trade—meaning effective entry/exit costs depend on trade size and pool liquidity. Synthetic contracts on Ventuals incur additional cost via funding rates, settled every eight hours rather than the hourly settlement common on most crypto perpetual exchanges. This longer interval aims to make holding costs more manageable for long-duration positions awaiting IPO events.

Regulation

SPV-backed platforms operate primarily under Regulation S—a U.S. securities exemption restricting offerings to non-U.S. investors. Beyond this constraint, most are globally accessible—though individual platforms may impose additional country-specific exclusions.

SEC-registered funds like VCX operate under an entirely different framework. As a NYSE-listed closed-end fund, VCX is open to any investor with a brokerage account—giving it the broadest regulatory coverage possible.

Synthetic contracts are unregulated, as they are offered permissionlessly on-chain.

Other Potential Risks

Transfer rights for tokenized equity: This poses greater risk for fund structures like USVC than for on-chain platforms. OpenAI and Anthropic have publicly condemned unauthorized tokenized investment products and signaled intent to strictly control share transfer rights. Given funds rely on the integrity of underlying SPV positions to calculate NAV, such funds may face bank-run-like scenarios—where reported valuations cannot be realized upon redemption.

Poor closed-end fund performance: Fund structures bundle investments into indices, depriving investors of control over individual company allocations. If allocation decisions diverge from where actual returns materialize, funds may underperform concentrated single-name positions.

Lack of short-selling mechanisms: A structural gap in the market—investors cannot express bearish views on spot markets or hedge via perpetuals. This contributes to persistent premiums relative to the last known private-market valuation. Ventuals is among the few venues offering short exposure via synthetic contracts—though short-side liquidity remains thin due to the absence of natural hedging counterparties elsewhere in the market.

What happens when companies actually IPO? Many of these pre-IPO assets currently trade at a 20–40% premium over the last known private-market valuation on PreStocks/Ventuals. Immediate liquidity at IPO is not guaranteed—especially for shares held within SPV structures, which require separate liquidation processes. Historical IPO performance adds further pressure: average public market valuations exceed IPO financing valuations by ~25%, leaving investors who entered at a premium with only a narrow margin before turning negative. For funds, NAV compression may outpace capital returns—exposing investors to risk during the gap period.

Market for New Entrants

Competition in this rapidly expanding market is intensifying. Exchanges like Binance and Bitget have launched their own pre-IPO stock tokenization offerings—either by integrating with PreStocks or developing proprietary synthetic contracts. On-chain participants are accelerating too: TradeXYZ recently launched pre-IPO perpetual contracts, achieving ~$7M daily volume—currently trading at a ~90% premium to expected IPO valuation (~$160/share).

New categories are also emerging. Backpack is launching on-chain IPOs backed by Superstate and Solana—offering investors actual legal securities. IPOs are traditionally reserved for institutions and accredited investors; conducting legally compliant, regulated IPOs on-chain would represent a major breakthrough for retail investors.

Where Value Flows

Asset tokenization will only grow more pervasive—the longer companies stay private, the greater the market demand for such investments. Interest has already moved beyond retail: governments, institutions, and funds are all vying for a slice. For example, the South Korean government recently launched a “National Growth Fund” aimed at enabling citizen participation—targeting investments in emerging domestic AI and semiconductor industries. With $160 billion in capital expected to be raised via IPOs this year, the race to capture demand for these liquidity events will be fierce.

Each new entrant validates market demand—but with no true stress test yet conducted, questions remain around structure, regulation, and viability of these assets. We believe platforms that solve liquidity challenges in the near term will win—but regulation remains decisive over the long run. The SEC and CFTC jointly issued a comprehensive report on how federal securities laws apply to digital assets: once underlying securities list publicly, many of these tokenized SPV wrappers will face heightened scrutiny and enforcement risk. Platforms capable of optimizing across all conditions will inherit a massive market.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News