Bitget UEX Daily Report | Trump Says War Will End Soon; 30-Year U.S. Treasury Yield Hits Highest Level Since 2007; Google I/O Unveils New AI Products; NVIDIA Earnings Report Due Tonight

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Trump Says War Will End Soon; 30-Year U.S. Treasury Yield Hits Highest Level Since 2007; Google I/O Unveils New AI Products; NVIDIA Earnings Report Due Tonight

Overall, the current market is in a tug-of-war between geopolitical optimism and macroeconomic caution; we recommend maintaining flexible positioning and closely monitoring earnings season and upcoming inflation data.

I. Top News

Federal Reserve Updates

Trump’s “end of war” statement eases some pressure, but inflation signals persist Trump stated that the conflict involving Iran would soon end and that Iran would not acquire nuclear weapons—a comment that lifted U.S. equity index futures and drove oil prices lower.

- Key Point 1: Market concerns over geopolitical risk have eased temporarily, providing support to risk assets.

- Key Point 2: Traders’ forecasts now assign a higher probability to a Fed rate hike before July 2027.

- Key Point 3: The 30-year U.S. Treasury yield breached 5.19%, reaching its highest level since 2007—reflecting rising inflation expectations.

Market Impact: Short-term boost to risk sentiment, yet the high-yield environment may constrain the Fed’s future rate-cutting room; ongoing monitoring of geopolitical developments and data confirmation is warranted.

International Commodities

Trump’s remarks trigger oil price decline; easing geopolitical tensions dominate short-term trend Trump’s comments about an imminent end to the conflict sparked market expectations of easing energy supply constraints, pushing down both WTI and Brent crude prices.

- Key Point 1: Oil prices retreated from recent highs, alleviating some inflation concerns.

- Key Point 2: Shipping disruptions around the Strait of Hormuz persist, though short-term sentiment has improved.

- Key Point 3: Gold and silver experienced modest volatility amid rising yields and easing geopolitical tensions.

Market Impact: Lower oil prices help reduce imported inflationary pressure, offering positive support for global growth and consumption expectations—but actual supply recovery must be closely tracked.

Macroeconomic Policy

30-year U.S. Treasury yield surges to new high of 5.19%, reflecting inflation fears and rising borrowing costs The 30-year U.S. Treasury yield broke above 5.19%, the highest level since before the 2007 financial crisis; large sell orders intensified the selloff. Mortgage rates rose to their highest level since last July.

- Key Point 1: Inflation expectations are rising due to energy and geopolitical factors.

- Key Point 2: Forecast markets indicate growing uncertainty regarding the Fed’s policy path.

- Key Point 3: Elevated yields raise real-economy financing costs, pressuring real estate and equities.

Market Impact: Reinforces expectations of a “higher-for-longer” policy environment, increasing short-term market volatility and potentially constraining growth over the longer term; investors should monitor upcoming inflation data and Fed commentary.

II. Market Recap

Commodities & FX Performance

- Spot Gold: +0.41% at $4,500/oz.

- Spot Silver: +1.26% at $74/oz.

- WTI Crude: -0.26% at $103/bbl.

- Brent Crude: -0.38% at $110/bbl.

- U.S. Dollar Index (DXY): +0.04% at 99.34.

Cryptocurrency Performance

- BTC: -0.39% at $76,769.

- ETH: -1.19% at $2,110.

- Total Crypto Market Cap: -0.8% at $2.63 trillion.

- Liquidations: $158 million liquidated in past 24H, with $106 million long positions liquidated.

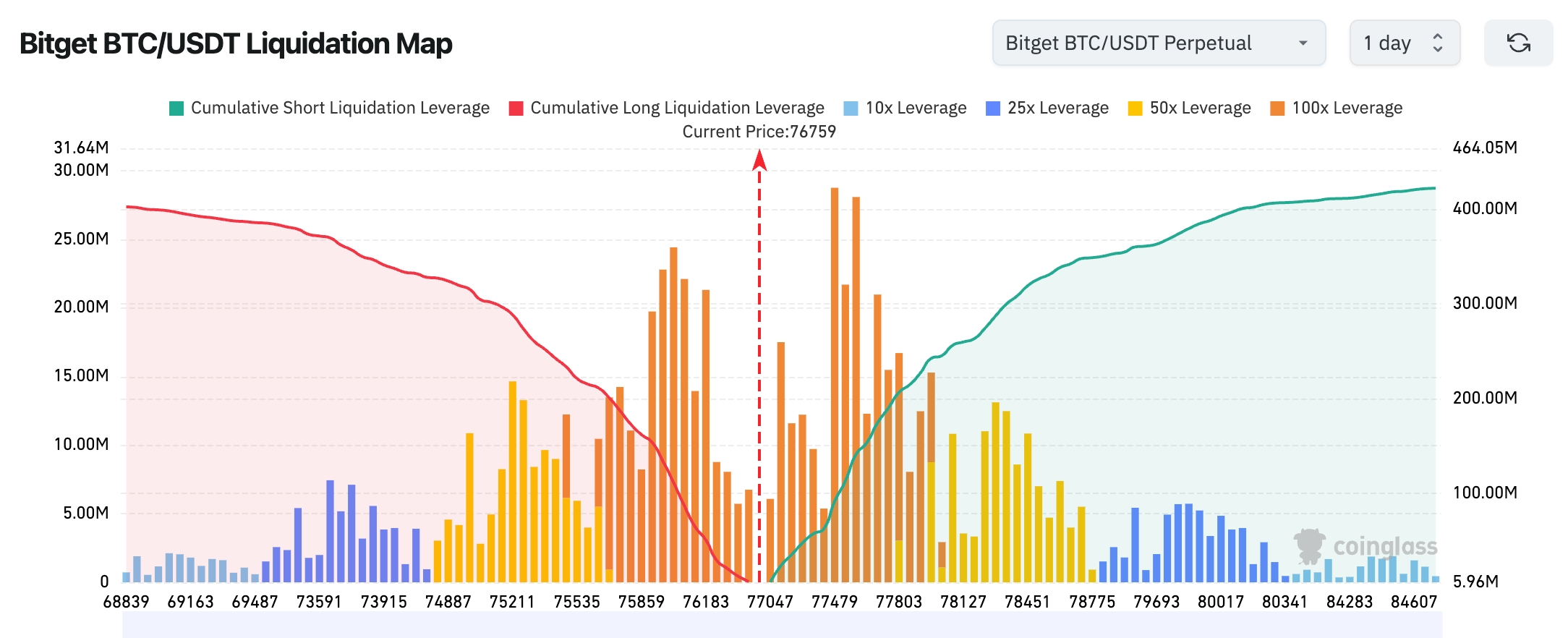

- Bitget BTC/USDT Liquidation Map: Near current price, liquidation pressure is relatively concentrated at key resistance levels above, while support zones below provide cushioning—short-term volatility may trigger cascading liquidations.

- Spot ETF Net Flows: BTC spot ETFs recorded $5.5 million net outflow yesterday—the third consecutive day of net outflows totaling $945 million.

- BTC Net Flows: Spot net outflow of $54 million yesterday; derivatives net outflow of $277 million.

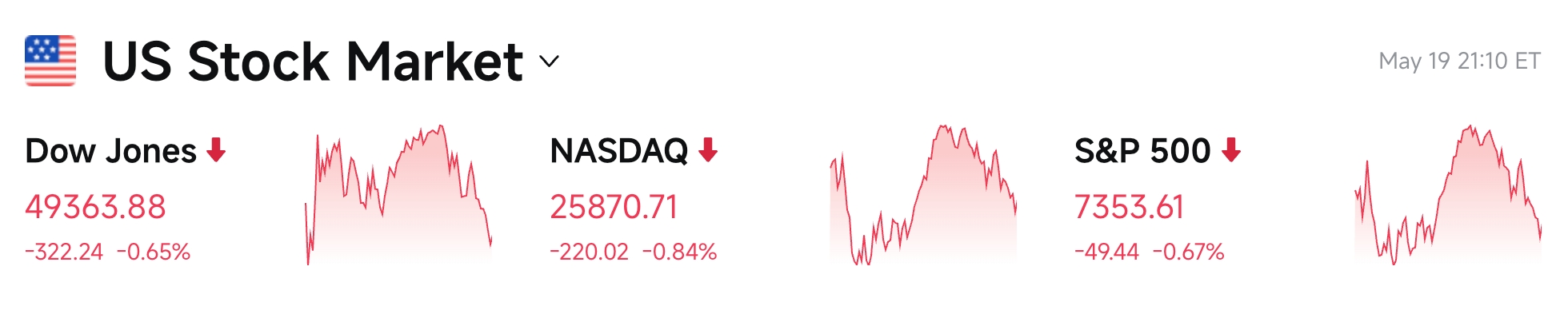

U.S. Equity Index Performance

- Dow Jones Industrial Average: -0.65% at 49,363.88—under pressure for three consecutive days.

- S&P 500: -0.67% at 7,353.61—dragged notably by technology and growth stocks.

- Nasdaq Composite: -0.84% at 25,870.71—driven by profit-taking in high-valuation tech stocks and upward pressure from rising yields.

Tech Giants Update

- Apple (AAPL) +0.38% at $298.97: Hardware division reorganization accelerates AI integration—relatively resilient.

- NVIDIA (NVDA) -0.77% at $220.61: Earnings report released tonight; market adopts cautious stance ahead of release, though long-term AI demand outlook remains unchanged.

- Microsoft (MSFT) -1.44% at $417.42: AI and cloud businesses remain solid, but overall market sentiment weighs on shares.

- Meta (META) -1.41% at $602.61: Advertising and AI investments proceed in parallel; short-term performance impacted by broader market weakness.

- Amazon (AMZN) -2.08% at $259.34: Cloud and e-commerce fundamentals remain steady, but valuation adjustments are emerging.

- Alphabet (GOOG/GOOGL) -2.09% at $387.66: I/O Conference unveiled multiple AI products; long-term tailwinds offset by near-term profit-taking.

- Tesla (TSLA) -1.43% at $404.11: Delivery progress and Robotaxi developments under scrutiny—volatility remains elevated.

Core Summary: High-valuation tech stocks face dual pressures from rising yields and profit-taking; the long-term AI narrative remains intact, but short-term volatility has intensified.

Sector Movement Highlights

Optical Communications Sector posted notable gains

- Representative Stocks: Astera Labs +13.3%, Credo Technology +8.14%, Marvell Technology +4.34%.

- Catalysts: Sustained robust demand from AI data centers and high-speed interconnect applications; some stocks rebounded sharply after oversold conditions and attracted bargain-hunting capital.

III. In-Depth U.S. Equity Analysis

1. NVIDIA – Earnings Report Tonight

Event Overview: NVIDIA will release its Q1 earnings after U.S. market close on May 20 (Eastern Time). Options market implied volatility suggests potential single-day price swings of ~7.56%. Wall Street broadly expects the company to exceed consensus estimates and raise full-year guidance, with AI data center demand remaining the core driver. Market Interpretation: Institutional analysts believe that although short-term geopolitical and macro volatility may cause disruptions, the AI capital expenditure cycle remains in its early stage—and NVIDIA, as a central beneficiary, retains a solid long-term growth thesis. Some analysts emphasize the need to monitor gross margin trends and next-generation product timelines. Investment Implication: Post-earnings volatility warrants attention; investors are advised to align positions with long-term AI trends and practice prudent leverage management.

2. Alphabet (Google) – AI Product Launches at I/O Conference

Event Overview: Google I/O launched Gemini 3.5 Flash (fastest and most cost-efficient model), Gemini Spark AI Agent (integrating Gmail, Docs, and other platforms to execute multi-step tasks), and upgraded search experiences—all offered free globally, strengthening multimodal and agent capabilities. Market Interpretation: Analysts view these moves as further cementing Google’s leadership in generative AI and search, with long-term upside for advertising and cloud monetization—though near-term market focus remains on commercialization pace and competitive dynamics. Investment Implication: Continuous iteration of the AI product suite is a key competitive advantage; investors should track developer adoption metrics and revenue contribution data.

3. Apple – Hardware Reorganization Accelerates AI Integration

Event Overview: Apple’s Chief Hardware Officer Johny Srouji initiated a major restructuring of the hardware development division, integrating in-house chip teams more tightly with product teams to accelerate AI feature deployment on hardware. Market Interpretation: Analysts note this organizational shift represents a critical step for Apple in catching up in the AI race; combined with prior chip and software initiatives, it could enable more competitive AI-powered end-user experiences starting in 2026 and beyond. Investment Implication: AI hardware rollout serves as a medium-to-long-term catalyst; investors should monitor product launch timelines and ecosystem feedback.

4. Optical Communications Stocks (e.g., Astera Labs) – Sector Surge Driven by AI Demand

Event Overview: Several optical and high-speed interconnect stocks posted sharp rebounds, with Astera Labs surging over 13% in one day—highlighting sustained market attention to AI data center infrastructure demand. Market Interpretation: Analysts affirm that AI training and inference continue to drive rapid growth in demand for high-speed, low-latency connectivity; some oversold names have drawn investor interest, though valuation and earnings realization timing warrant caution. Investment Implication: Sector divergence is pronounced; investors should prioritize fundamentally sound names with high order visibility and manage short-term volatility risk.

IV. Cryptocurrency Project Updates

1. Matt Hougan, Chief Investment Officer at Bitwise, stated that Hyperliquid’s HYPE token remains undervalued—even after gaining 77% year-to-date, making it the top-performing large-cap crypto asset in 2026. Hougan characterizes HYPE as a “second-generation” crypto token with equity-like appreciation potential over time, and believes its value remains underestimated.

2. K33 Research noted in a report that this Bitcoin bear market differs significantly—extreme pessimism among traders has capped downside risk. Bitcoin traders remain in defensive mode, reducing the likelihood of leveraged collapse. Research Head Vetle Lunde pointed out that the current slow bottoming process does not mirror previous cycles where bear-market rallies were quickly reversed; instead, derivatives data points to extreme pessimism. Bitcoin’s 30-day average funding rate has been negative for 81 consecutive days—approaching the longest historical streak—and the CME Bitcoin futures annualized basis has fallen below 2.5%, signaling exceptional caution. Still, open interest in Bitcoin derivatives remains elevated; further price weakness could trigger volatility. K33 maintains its base case that Bitcoin’s drop to $60,000 in February likely marked the peak drawdown of this cycle.

3. As traditional asset managers accelerate tokenization of real-world assets (RWAs), the total RWA market cap has surpassed $65 billion—up ~44% from the start of the year. Ethereum commands ~33% market share, retaining its position as the default institutional tokenization platform.

4. According to The Block, daily trading volume for tokenized equities hit a record $3.57 billion on Monday. Platforms such as Ondo and Bitget have collectively driven cumulative on-chain stock trading volume into the billions of dollars. Notably, Bloomberg reported on Monday that the U.S. SEC is developing guidelines and innovation exemptions for the emerging on-chain equity ecosystem.

5. Per CoinDesk, Christoph Hock, Head of Digital Assets & Tokenization at Union Investment—one of Germany’s largest institutional asset managers—stated that stablecoin reserve structures at Tether and Circle resemble speculative funds rather than true fiat-backed instruments. Even holding substantial U.S. Treasuries does not insulate them from sudden liquidity crises. Hock highlighted that Tether holds significant gold and Bitcoin reserves, rendering USDT and USDC more akin to hedge funds—exposing structural fragility in their tokenomics that could impact holders’ financial interests.

6. Total stablecoin supply has surpassed $300 billion—but growth has stalled. Tether’s USDT expanded by over $5 billion in the past month, while USDC, USDe, and PYUSD collectively contracted by ~$4.2 billion, resulting in a net increase of only ~$900 million—or just 0.3% of total supply.

V. Today’s Market Calendar

Data Release Schedule

Key Event Preview

May 20 (Wednesday)

- NVIDIA (NVDA) releases Q1 earnings after market close (the absolute highlight of the week) ★★★★★

- SpaceX may file its IPO prospectus as early as Wednesday, targeting June 12 for listing ★★★★★

- U.S. EIA Crude Oil Inventories data for the week ending May 15;

- Other major U.S. earnings: Lowe’s (LOW), Analog Devices (ADI), Target (TGT), Intuit (INTU), GDS (GDS).

May 21 (Thursday)

- Fed releases minutes from the April 28–29 FOMC meeting (the final minutes of Powell’s tenure—signaling the onset of the “Waller era”) ★★★★★

- U.S. initial jobless claims for the week ending May 16;

- U.S. May S&P Global Manufacturing PMI preliminary and Services PMI preliminary;

- Major U.S. earnings: Walmart (WMT); Chinese ADRs: NIO, NetEase (NTES), Vipshop (VIPS)—all pre-market.

May 22 (Friday)

- U.S. May University of Michigan Consumer Sentiment Index final reading.

*This week’s U.S. equity highlights: NVIDIA’s pivotal earnings (key test of AI rally sustainability), Fed meeting minutes (signal of Powell’s departure), Google I/O Developer Conference, SpaceX’s potential IPO filing, and a wave of major earnings from consumer, tech, and Chinese ADR names—including Walmart—alongside dense macro data releases. Expect heightened market volatility.

Institutional Views:

Summarizing the past 24 hours, Trump’s statement on the imminent end of hostilities injected temporary optimism into markets—lifting U.S. equity futures and lowering oil prices, effectively easing some inflation concerns. However, the 30-year Treasury yield breaching 5.19% clearly reflects market anxiety over persistent inflation and a “higher-for-longer” policy regime. Leading investment bank analysts broadly agree that if geopolitical easing continues, it will support risk assets—especially AI and technology growth sectors—but high yields may suppress valuations. Short-term pullbacks remain possible if data disappoints. NVIDIA’s earnings are viewed as a critical barometer: consensus anticipates continued outperformance and raised guidance, supporting the broader AI supply chain. Crypto markets move in tandem with macro and risk sentiment—BTC and ETH trade sideways near key support levels, while ETF flows and leveraged liquidation data merit close tracking. Overall, markets are navigating a tug-of-war between geopolitical optimism and macro caution. Investors are advised to maintain flexible positioning and prioritize earnings season and upcoming inflation data.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute investment advice. Data presented herein may contain unavoidable inaccuracies; please refer to real-time market data for accuracy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News