Why don’t you buy a 2x long position on SK Hynix?

TechFlow Selected TechFlow Selected

Why don’t you buy a 2x long position on SK Hynix?

Does Silicon-Based Technology Have Cycles?

This month in South Korea, if you’re neither an SK Hynix employee nor a shareholder of SK Hynix stock, you’re most likely “a wretched soul.”

Once its first-quarter earnings—massive and staggering—were released, investment banks, ever eager to stir up excitement, not only aggressively raised their profit forecasts for Hynix this year but also inflated employees’ expectations for year-end bonuses. Leveraging the company’s annual bonus policy—which allocates 10% of operating profit into a bonus pool—they calculated that each employee could receive several million RMB in year-end dividends. In the process, they casually placed Samsung’s capital owners on the hot seat of moral condemnation.

Afterward, anything even remotely associated with the Hynix IP was met with frenzied enthusiasm.

Hynix-branded workwear became a priority “golden ticket” in South Korea’s matchmaking market; real estate agents in Icheon—the city where Hynix’s headquarters is located—experienced a surreal quarter, as property prices and transaction volumes surged across multiple neighborhoods along Hynix’s commuter bus routes; even China–South Korea semiconductor ETFs, long criticized for lacking technological sophistication, soared to a 30% premium, triggering frequent temporary trading halts.

Even Hong Kong’s stock market—often lambasted for its limited technological depth—briefly stood tall.

As of May 13, 2026, the Southern Eastern SK Hynix Daily 2x Leveraged ETF (07709.HK) (hereinafter, the “2x Long Hynix ETF”), listed on the Hong Kong Exchanges and Clearing (HKEX), had assets under management (AUM) nearing HK$60 billion—surpassing the long-dominant Tesla 2x Leveraged ETF (TSLL.NASDAQ) on U.S. markets and claiming the top spot globally among single-stock leveraged derivatives by AUM.

No matter how niche an investment product may be, once market sentiment reaches such fever pitch, anyone scrolling through tech or gadget blogs online will inevitably encounter well-meaning netizens in comment sections repeatedly urging: “Why aren’t you buying the 2x Long Hynix ETF?”

The Lethal Leverage

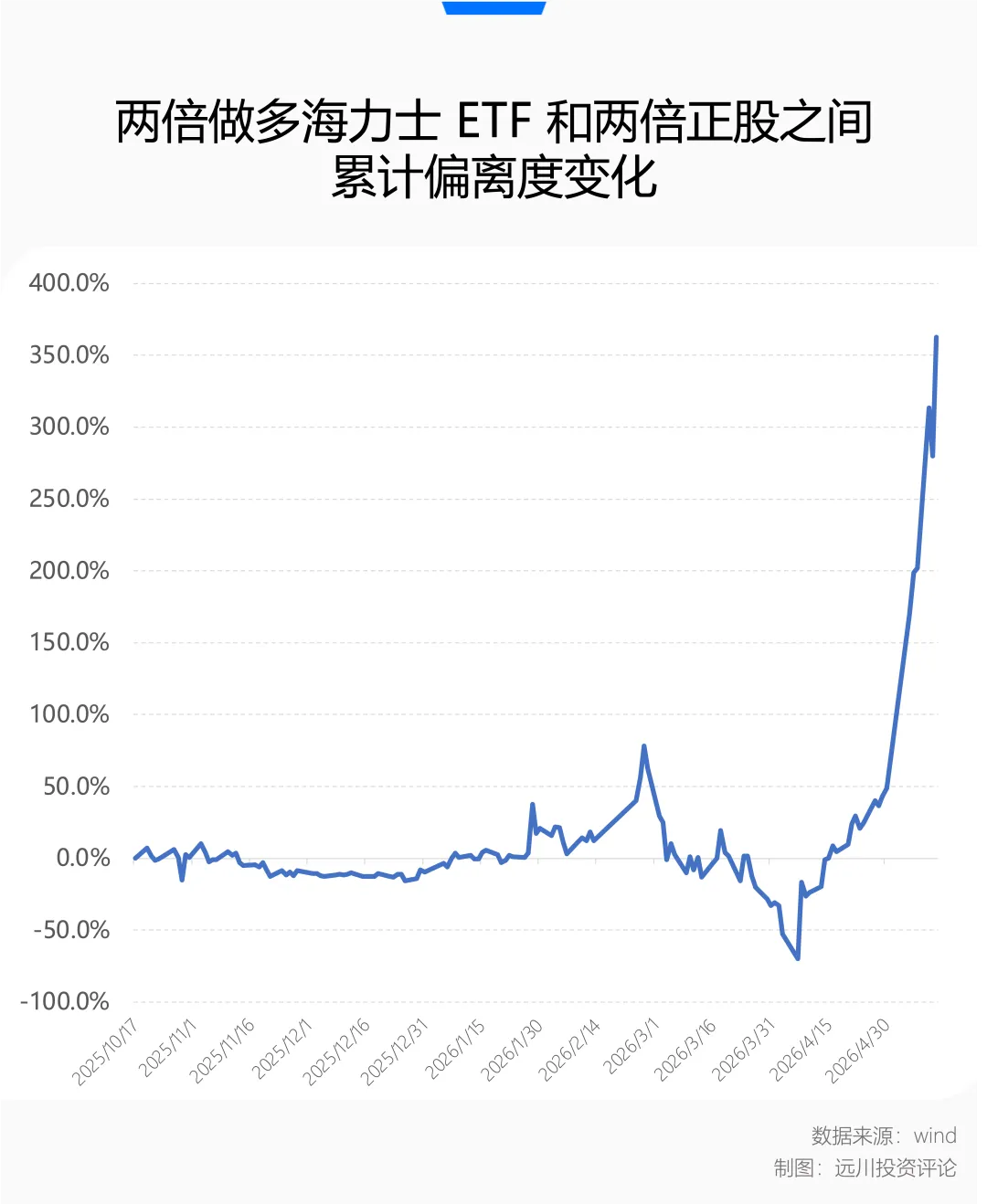

When the 2x Long Hynix ETF debuted on the HKEX on October 16, 2025, its initial issuance size was less than HK$5 billion. As of its closing price on May 13, 2026, the ETF’s net asset value (NAV) had surged 1,011.58%—and its AUM ballooned over 13-fold—in just seven months.

By contrast, CloudMinds Technology—the so-called “first hotel-robot IPO”—which launched on the same day on the HKEX, has seen its share price climb steeply, yet its market capitalization remains less than four times its listing value.

If you attribute this explosive growth solely to 2x leverage, consider this: SK Hynix’s underlying stock, traded on the Korean exchange, rose only 324.49% between October 17, 2025, and May 13, 2026. Under the tailwind of a strong, one-way uptrend, the ETF’s performance deviated from theoretical 2x returns by an additional 362%—making “3x leverage” seem like a more accurate descriptor.

Yet if we zoom out to examine the past seven months, this apparent excess return proves fleeting.

Just two months ago, the Strait of Hormuz plunged into Schrödinger-like uncertainty—neither fully sealed nor fully open—triggering global panic amid sudden disruptions to oil and gas supplies. Amid rapidly shifting geopolitical developments, markets avoided traditional one-way declines, instead descending into cognitive dissonance.

By day, traders priced in “World War III breaking out and supply chains collapsing”; by night, a vague statement from a White House spokesperson could instantly pivot sentiment toward “de-escalation and a return to the tech rally.” This ambiguity and unpredictability—amplified by rapid social media dissemination—translated directly into capital markets: violent selloffs hitting tech stocks, or frantic bargain-hunting at every dip.

While common sense tells us wars eventually end—and AI’s daily token consumption continues accelerating—when market volatility spikes, the tortuous path cannot be ignored.

It was precisely during this period that many investors first felt the ETF’s volatility drag.

Real trading data from March to April 2026 shows Hynix’s share price trending downward amid violent oscillations. The decline itself was problematic—but the repeated, >10% intraday rebounds only worsened matters.

For a daily-rebalanced 2x Long Hynix ETF, a sustained downtrend might be bearable. But high-volatility, choppy declines are true meat grinders: at its worst, the ETF fell over 50% more than twice the underlying stock’s decline.

Ignoring other fees and management expenses, the ETF’s daily rebalancing mechanism means that in a steady uptrend, yesterday’s gains automatically become today’s “principal,” upon which 2x leverage is reapplied—generating extra upside. Conversely, in a sharp, one-way crash, the shrinking daily base reduces actual losses below theoretical 2x drawdowns.

However, in a “zigzag” market—where up and down days alternate—the leveraged ETF reveals its vicious side.

The 2x Long Hynix ETF repeatedly suffers “double whammies”: after a big gain, it rebalances upward—only to lose more on the next day’s drop, then rebalance again—only to suffer another loss on the rebound, now on a diminished base.

This back-and-forth friction causes the ETF’s actual NAV decline to far exceed twice the underlying stock’s drawdown—producing pronounced negative volatility drag that erodes investor capital.

Yet today, markets have refocused on the AI narrative, and speculative capital has flooded back in—delivering a joyful, one-way surge.

As Hynix’s market cap hits new highs and a hundred-billion-dollar leveraged ETF ignites frenzied trading, the market inevitably circles back to the same question—day after day: Does this industrial revolution truly lack cyclical patterns?

Silicon-Cycle Stocks

One must acknowledge that, timing-wise, the 2x Long Hynix ETF was launched under near-perfect auspices—“fate, fortune, and feng shui” all aligned.

For much of its history, memory chips were never the absolute focal point for going long on AI in secondary markets. After all, since humanity boarded the information-age express train in the 1990s, memory has often been the sector where “prosperity turns to carnage”—its terrifying cyclicality dwarfing any dreams of growth.

Memory chips—especially traditional DRAM and NAND—are highly standardized commodities. Memory modules produced by different vendors differ little physically beyond branding—making them, in silicon terms, “pork stocks.” The entire industry has long been trapped in a brutal cycle:

Shortage → Price hikes → Rampant capacity expansion by giants → Oversupply → Price collapse → Losses and production cuts → Shortage again.

Each upcycle is hailed as a “super-cycle” amid euphoric optimism; each downturn leaves behind carcasses strewn across battlefields of cutthroat price wars and multibillion-dollar losses.

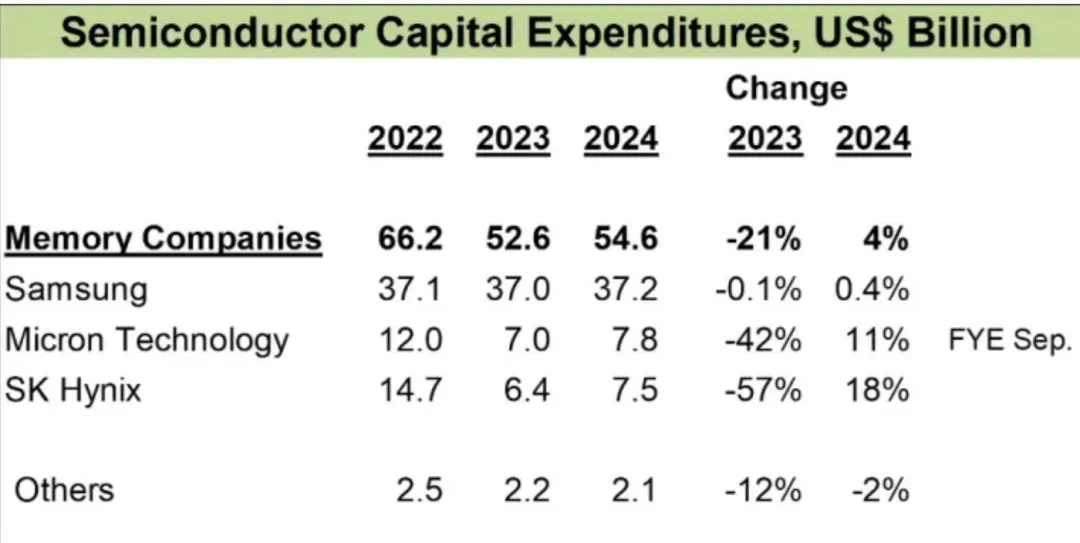

After the semiconductor industry’s harshest winter on record—from 2022 to 2023—the three surviving memory oligopolists—Micron, Samsung, and Hynix—tacitly curbed capital expenditures, abandoning self-destructive, scorched-earth capacity expansions.

Source: IC Insights

Then came the AI narrative—reigniting shortage-driven price surges and effectively installing printing presses for everyone.

Especially since last year’s second half, AI’s competitive focus has shifted from “training” to “inference,” redirecting infrastructure demand from “compute power” to “memory power,” and bottlenecks from bandwidth to capacity—turning memory shortages into the hottest trade narrative.

At this point, anyone still muttering, “But wasn’t AI supposed to end with electricity?” has almost certainly missed the boat.

Since Q3 2025, nearly every AI-related headline has revolved around memory chip shortages: one day, tech giants announce HBM orders booked through 2027; the next, they notify clients DDR5 is also running short—so apologies, but all tiers—premium and budget alike—will see across-the-board price hikes.

As NVIDIA’s primary HBM supplier, Hynix captured massive first-mover advantages and market share. Born at the perfect moment, the 2x Long Hynix ETF debuted just as memory module prices spiked past gold—and a single box could trade for a Shanghai apartment.

So—can hopping aboard the AI express train truly escape the gravitational pull of cycles? What matters isn’t rushing to conclusions now, but identifying where change may emerge.

Under HBM yield barriers, Hynix has achieved de facto monopoly status: in Q1 2026, SK Hynix posted a record quarterly gross margin of ~79%, even surpassing NVIDIA’s profitability that quarter.

Human nature dictates that extreme excess profits inevitably ignite fierce capacity expansion urges. The tacit “production cuts” agreement among memory giants crumbles under the weight of such astronomical margins.

Thus, whether Samsung or Micron will break through HBM yield bottlenecks in the future—diluting the scarcity narrative—and whether resulting bull-bear divergence triggers sector-wide volatility, remains a key variable to monitor.

Beyond supply-side shifts, demand-side debates haven’t vanished—even amid accelerating Agent adoption and rising token consumption.

Ultimately, Hynix’s frenzy rests atop NVIDIA’s frenzy—and NVIDIA’s frenzy rests atop downstream tech giants’ annual AI capital expenditures, totaling hundreds of billions of dollars.

Changes at the margin of Capex remain the strongest gravitational force behind all AI-related anxiety and exuberance in secondary markets.

Epilogue

Whether you buy—or don’t buy—the 2x Long Hynix ETF, it will remain a subtle footnote when we look back on this era.

In our time, “long” and “short” often refer to two distinct things: “long” reflects faith in the AI industry; “short” expresses macro-geopolitical anxieties.

People habitually turn to history books, seeking parallels in the dot-com boom of the millennium or earlier macro upheavals. Yet every technological revolution unfolds differently—and this one’s uniqueness lies in its unprecedented speed of disruption.

AI is reshaping global productivity and production relations at an acceleration never before witnessed. This extreme “speed” breaks the traditional tech cycle’s slow, prolonged phases of penetration and fermentation. It grants markets no time to digest valuations gradually—and offers scant rotational opportunities for “old-timers” to catch a break amid liquidity floods.

Both industry titans and secondary-market capital are forced to pick sides and price assets within razor-thin time windows—so equity gains are now measured in multiples; seasoned AI practitioners have already accepted that six months qualifies as “long-term” in this era.

Yet the storm over the Strait of Hormuz reasserts this tech revolution’s shared trait with all prior tech cycles: industries determine final outcomes and returns; macro factors shape paths and volatility. The 2x Long Hynix ETF’s massive negative deviation wasn’t caused by AI’s progress stalling—but by the extreme swings in global macro expectations over those few weeks.

And the world’s real vulnerabilities extend far beyond that narrowest 33-kilometer stretch of the Strait of Hormuz.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News