Arkstream Capital Shares: How Ordinary Individuals Can Properly Participate in Tokenized Pre-IPOs

TechFlow Selected TechFlow Selected

Arkstream Capital Shares: How Ordinary Individuals Can Properly Participate in Tokenized Pre-IPOs

This article mainly clarifies two things: first, what traditional pre-IPO actually is; second, how retail investors can participate.

Author: @Chandler_btc | Arkstream Capital

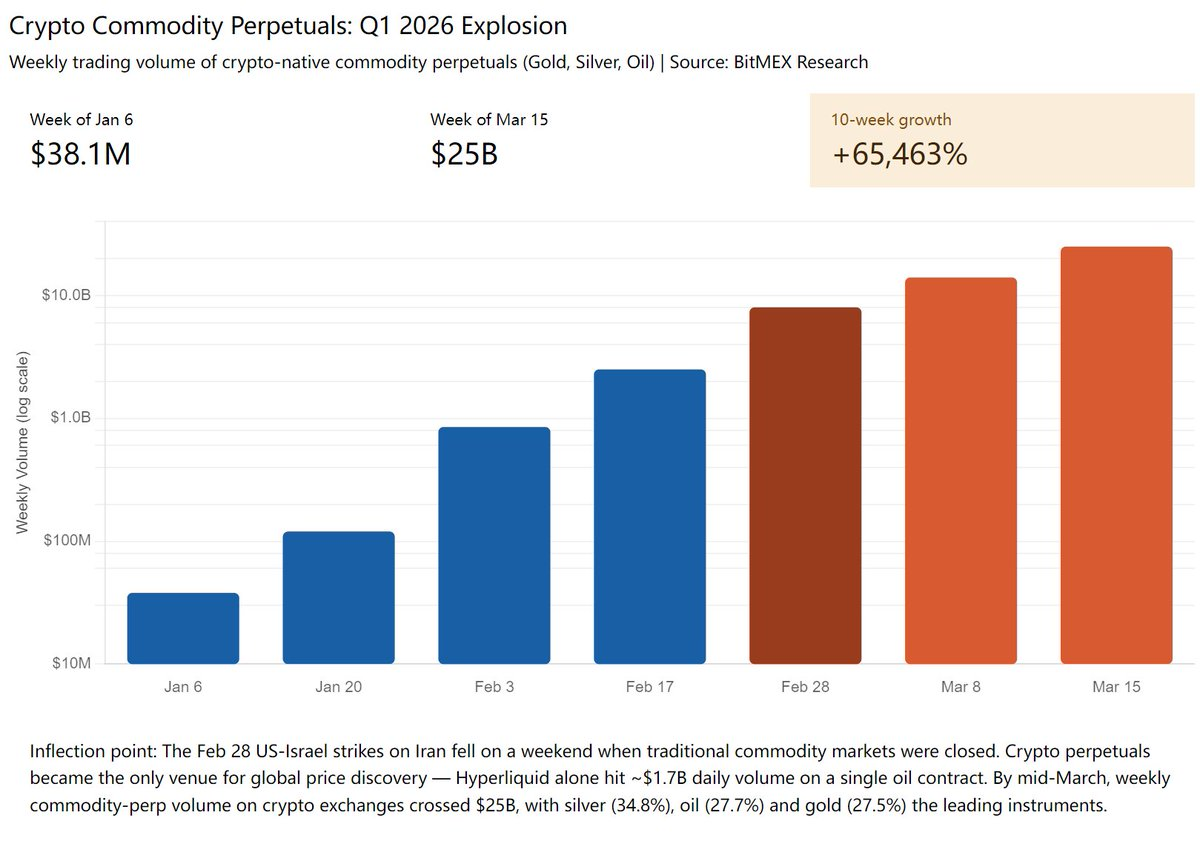

Introduction: In Q1 2026, weekly trading volume of commodity perpetual futures (gold, silver, crude oil) on crypto exchanges surged from $38.1M to $25B—a staggering 65,463% increase. Tokenization of traditional assets will be the dominant theme across crypto over the next 5–10 years; pre-IPO tokenization is merely the latest category entering this wave.

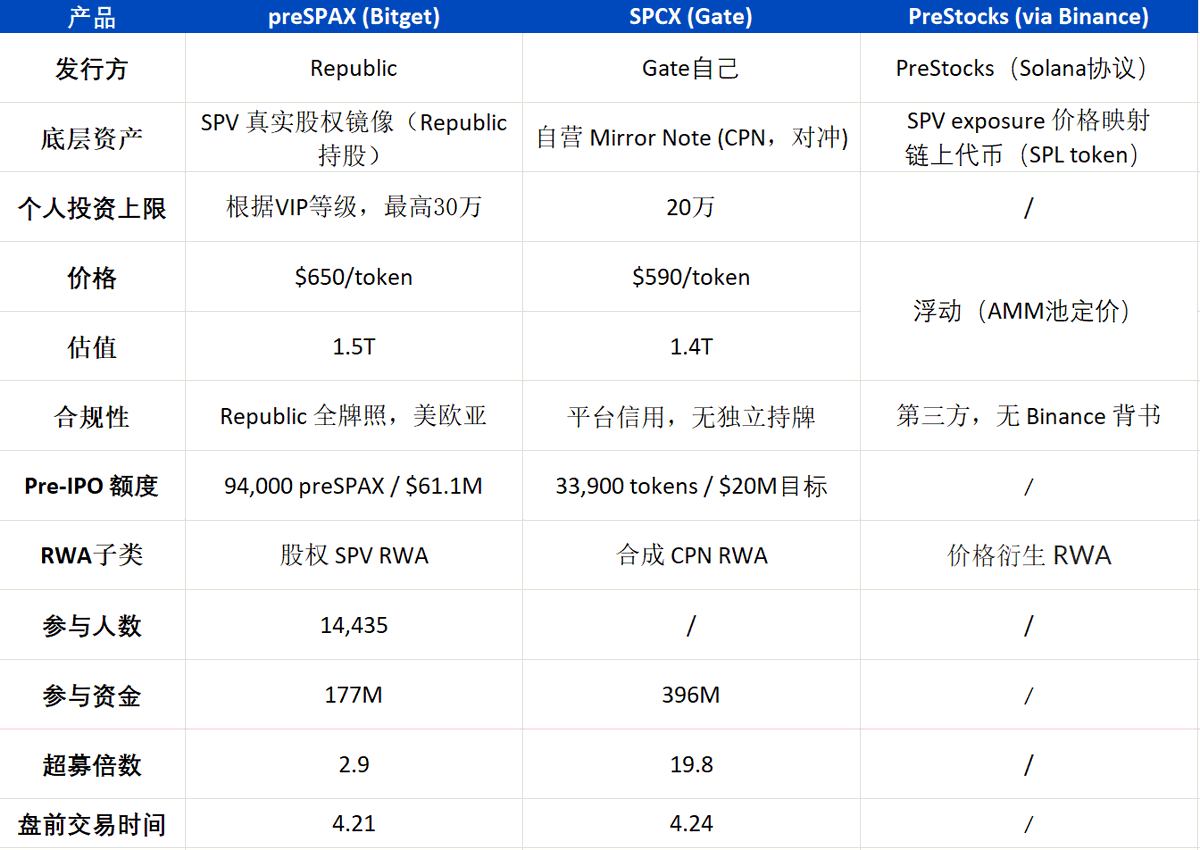

In April, three leading exchanges—Bitget, Gate, and Binance (via PreStocks)—launched SpaceX-related tokenized products almost simultaneously. Though their compliance approaches differ, all share the same core idea: fractionalizing pre-IPO equity stakes—historically accessible only to ultra-high-net-worth individuals—and selling them to retail investors.

Tokenization of Traditional Assets Will Be Crypto’s Dominant Theme for the Next 5–10 Years

According to data, in Q1 2026, weekly trading volume of commodity perpetual futures (gold, silver, crude oil) on crypto exchanges surged from $38.1M to $25B—an increase of 65,463%. After launching its TradFi Perpetuals section in January, Binance recorded over $153B in cumulative trading volume and more than 114 million trades within three months. Its XAG (silver) perpetual contract achieved an average daily trading volume of $1.31B, lifting its global market share from 0.2% to 4.9%—a 23.5x increase.

The most striking moment came at the end of February during the Iran conflict: U.S. and Israeli strikes against Iran occurred over the weekend, when traditional futures, equities, and forex markets were closed. Only crypto markets remained open globally. Hyperliquid’s crude oil perpetual spiked +5% instantly; Tether’s gold token (XAUT) saw over $300M in single-day trading volume; Bitwise’s CIO dubbed it “the weekend that changed finance.”

U.S. equities, precious metals, crude oil, and foreign exchange—assets previously traded only weekdays, 9 a.m.–4 p.m.—are now being tokenized, put on-chain, and offered with 7×24 global liquidity. Pre-IPO tokenization is simply the newest entrant into this wave.

Source: BitMEX Research

What Exactly Is Pre-IPO?

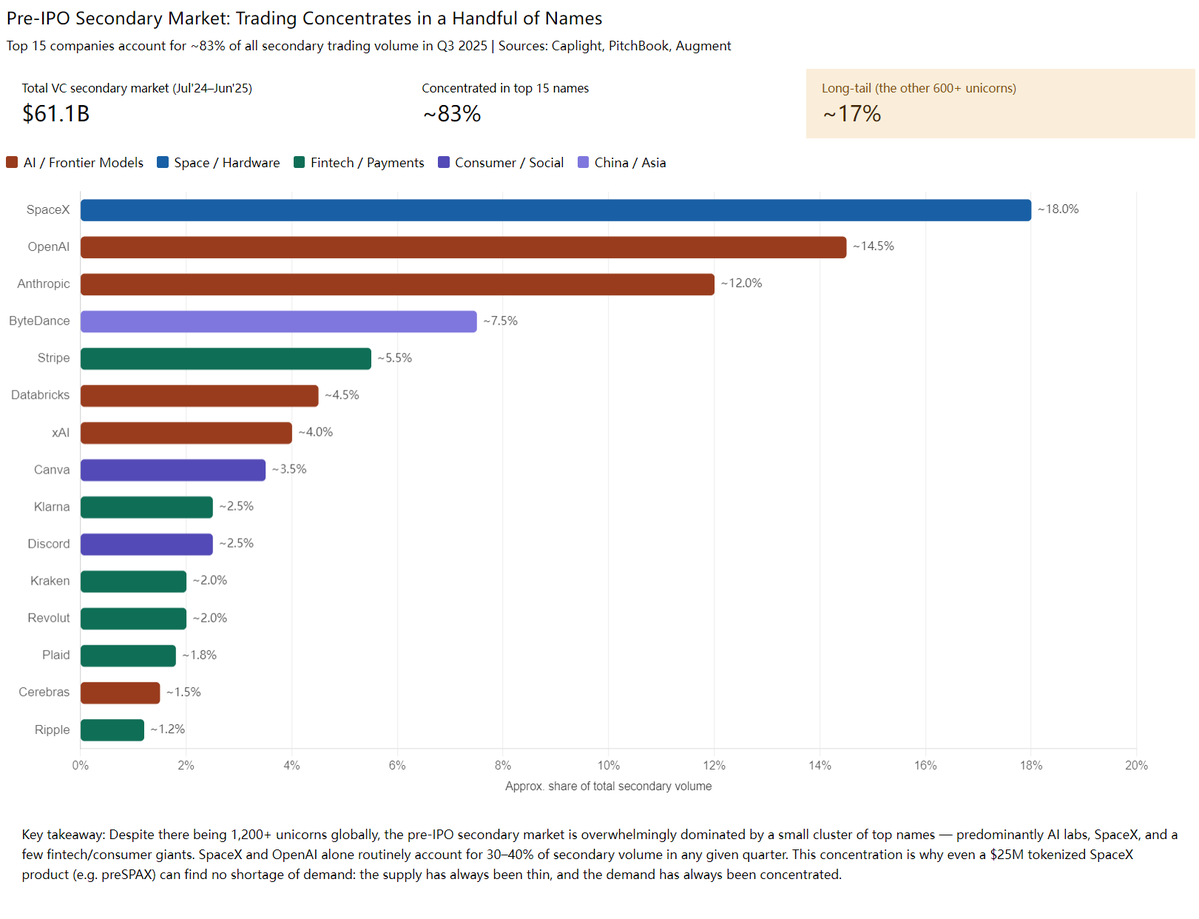

The pre-IPO secondary market (also known as “secondary sales of existing shares”) has existed for over a decade. Global transaction volume reached $160B in 2024 alone, with $61.1B transacted in the U.S. direct secondary market. Buyers are predominantly family offices, sovereign wealth funds, institutional investors, and high-net-worth individuals. Minimum ticket sizes typically exceed $10M, effectively excluding retail investors.

Most transactions occur via SPVs (Special Purpose Vehicles): original shareholders transfer their shares into a newly formed shell company, which then sells interests in that entity to new buyers. Buyers receive SPV interests—not direct shares—thereby holding indirect exposure to the underlying company. This structure avoids placing unknown third parties directly onto the company’s cap table (shareholder register), which would trigger other shareholders’ ROFR (Right of First Refusal) and introduce procedural complications—or even outright blocking by existing shareholders. As such, buyers ultimately acquire LP interests or units in the SPV, representing indirect rights to the underlying pre-IPO shares.

Secondary market activity is highly concentrated among a small group of top-tier names. U.S.-based AI and aerospace giants—including SpaceX, OpenAI, and Anthropic—have consistently accounted for 30–40% of total trading volume. Combined with other leading unicorns such as ByteDance, Stripe, Databricks, and xAI, the top 15 companies collectively account for ~83% of the entire market’s volume. (This concentration explains why Bitget and Gate’s launch of a single SpaceX token easily raised over $100M—supply of top-tier pre-IPO assets remains scarce, while demand is intensely focused.)

The majority of these targets are U.S.-based, making CFIUS (Committee on Foreign Investment in the United States) the primary regulatory hurdle. CFIUS restricts foreign investment in sensitive U.S. sectors—including AI, semiconductors, and defense—subjecting capital from certain countries to strict scrutiny when purchasing shares in companies like SpaceX or Anthropic. Sellers therefore commonly prohibit purchases by ultimate beneficial owners (UBOs) from restricted jurisdictions (e.g., China, Russia, Iran). General Partners (GPs) conduct UBO due diligence through SPV layers; deeper structures complicate verification—but not infallibly. We’ve encountered cases where Chinese UBOs hidden behind two SPV layers were uncovered, causing entire deals to collapse.

Sources: Caplight, PitchBook, Augment

Following IPO, U.S. companies also observe a standard lock-up period: SEC Rule 144, combined with underwriter agreements, prohibits early shareholders and employees from selling shares on public markets for six months post-IPO. This applies to virtually all U.S. firms (e.g., Facebook, Coinbase, Reddit, Cerebras). Hence Bitget and Gate’s pre-IPO tokens require a six-month settlement delay—but do permit pre-settlement trading.

Real-World Pre-IPO Transaction Details

Extremely High Ticket-Size Thresholds

Traditional pre-IPO ticket sizes start at $10M; deals below $1M are rarely entertained—not due to lack of interest, but because fixed costs (legal fees, KYC, SPV formation, channel commissions) cannot be amortized. Thus, exchanges’ recent initiatives represent a truly disruptive breakthrough—dismantling structural barriers. Historically, only sophisticated retail investors (with U.S. brokerage accounts, etc.) could participate post-IPO; now, despite higher fees, exchanges have opened access to ordinary users.

Broker/FA Misconduct

A cross-border pre-IPO deal typically passes through multiple intermediaries:

Underlying GP → Representative (seller-side agent) → Tier-1 broker → Tier-2 broker → … → Financial Advisor (FA) → End client

Each layer adds 1–5% in fees. A deal valued at $500B at source may cost the end buyer over $600B.

Take SpaceX: its true market valuation sits around $1.25T, plus an access fee of 3–11% depending on channel and tier—pushing final pricing to ~$1.375T before adding tokenization compliance costs. All things considered, exchange-offered prices appear relatively fair—likely driven by user acquisition strategy.

Moreover, most “block” supply in the market is illusory: identical shares are repeatedly listed by multiple brokers; fewer than 10% of listings represent genuinely available, executable inventory. For example, platforms list SpaceX shares at a $1.2T valuation—but deep-dive discussions reveal nearly all such listings are fictitious—even major platforms and top-tier intermediaries are rife with this practice.

Sources: A secondary share trading platform

If the transaction involves an LP interest swap, GP consent is required—the GP of the underlying SPV must approve any transfer of LP interests. GPs retain full discretion to reject such transfers. In practice, GPs often disfavor these transfers: vetting new LPs, ensuring compliance, and introducing outsiders create administrative burdens. Consequently, bribes (“facilitation payments”) to GPs are common—adding yet another cost layer.

Poor Liquidity Is Pre-IPO’s Biggest Pain Point

Exiting mid-hold is extremely difficult. Options are limited to: (1) waiting for IPO (typically 3–7 years), followed by an additional six-month lock-up; or (2) finding a new buyer and repeating the entire structured process—taking at least two to three weeks (minimum) plus FA fees.

Every resale constitutes a standalone OTC transaction requiring full re-execution of legal documentation, KYC/AML/UBO due diligence, and GP approval. This is precisely why pre-IPO assets are persistently priced as “illiquid.”

How Retail Investors Can Participate in This Pre-IPO Wave

We anticipate a wave of secondary-share tokenization products hitting the market shortly—all sharing the same fundamental model: platforms purchase authentic pre-IPO shares in the traditional secondary market, then tokenize and fractionalize them for retail sale.

For retail investors, this unlocks participation ahead of IPO—allowing them to ride successive valuation increases alongside the company.

Top-tier targets typically exhibit monotonic valuation growth: SpaceX rose from $74B in 2021 to over $1.4T today; OpenAI climbed from $29B to $852B+; Anthropic expanded from $4B to $800B+; ByteDance grew from $75B to $600B+. Each funding round lifts valuations—and incumbent shareholders benefit accordingly.

But one truth must be heeded: this is not risk-free. Historically, Stripe endured a down round slashing its valuation from $95B to $50B; TrueLayer dropped 30%; Cybereason plunged 90%; WeWork collapsed from a $49B valuation to bankruptcy. In 2023 alone, 128 unicorns saw valuations decline—and 42 fell out of unicorn status entirely.

Hence, success in pre-IPO investing hinges on selection—not timing. Focus on long-term appreciation aligned with the company’s organic valuation growth—not short-term emotional trading triggered by token launches. Many crypto-native users mistakenly treat pre-IPO tokens like IDOs; the two operate under entirely distinct logics.

To summarize the participation framework:

1. Do you hold a long-term conviction in this asset? Does SpaceX/OpenAI/Anthropic justify its post-IPO valuation? Are you prepared to hold through the next funding round—or IPO?

2. Is this product secure? Who is the issuer? Where is the recourse? Who bears liability if something goes wrong?

RWA Landscape Over the Next Three Years

Pre-IPO RWA (Real World Asset) tokenization remains in its infancy. Supply of top-tier assets is scarce, demand is hyper-concentrated, and valuations trend upward over time. Over the coming months, tokenized offerings for OpenAI, Anthropic, xAI, Stripe, ByteDance, Kimi, and others will roll out sequentially.

Yet this represents just one subsegment of the broader tokenization ecosystem. Four clear architectural layers are already emerging:

- Stablecoin issuers: Providing on-chain USD and settlement infrastructure

- Public blockchains: Serving as the foundational layer for asset issuance and transfer

- Trading and distribution platforms: Centralized (CEX) and decentralized (DEX) exchanges. We also see strong potential for LaunchPad/IDO platforms (e.g., Buidlpad), which already possess end-to-end capabilities for KYC, issuance, allocation, and distribution of new assets—having previously launched crypto tokens, they’re now fully equipped to launch pre-IPO tokens

- Asset tokenization service providers: Firms specializing in bringing diverse real-world assets on-chain

Tokenization won’t merely spawn a cohort of unicorns—it holds potential to nurture new trillion-dollar infrastructure players and a cluster of hundred-billion-dollar platform companies.

Everything has just begun.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News