LDO, Down 96%, Launches $22 Million Buyback—Markets Take No Notice

TechFlow Selected TechFlow Selected

LDO, Down 96%, Launches $22 Million Buyback—Markets Take No Notice

Lido generates revenue, holds an unassailable market-leading position, and possesses an extremely deep moat—its revenue will not disappear (effectively, never).

Author: basedpotato

Translation & Editing: TechFlow

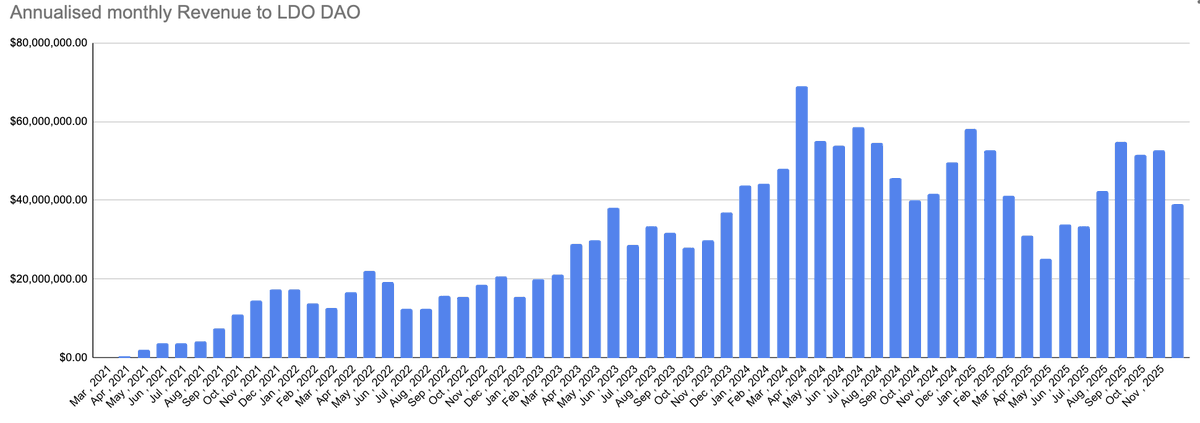

TechFlow Intro: Crypto KOL basedpotato argues that while LDO has plunged 96% from its all-time high, Lido’s staking revenue has remained stable. The protocol generates roughly $40 million in annual revenue, yet its market cap stands at just $275 million—bringing its valuation multiple back into a reasonable range. More importantly, the DAO recently approved a proposal to repurchase $22 million worth of LDO (10,000 stETH), representing ~8% of the circulating supply—yet the market barely reacted.

Lido is literally buying itself back from “death”—and no one is watching.

I understand ETH’s price action has been weak, security incidents have piled up over the past two quarters, and EVM-based DeFi has shown little innovation. Aside from a handful of projects delivering consistently >8% APY (e.g., @Neutrl, integrated with the STRC yield engine), DeFi has offered few fresh hooks to attract new capital.

That doesn’t mean value isn’t there to be uncovered. In fact, many of the most successful compounding players from the last cycle generated their largest PnL precisely where others refused to look.

This cycle offers far fewer bloated treasuries to arbitrage, and DAOs seem passé. Yet a small number of projects go beyond lip service on governance tokens—and genuinely recognize a fiduciary duty toward token holders. LDO is one such project.

The logic behind this trade is simple, supported by two key arguments:

Valuation Misalignment

For most of LDO’s history, I’d have unhesitatingly labeled it overvalued. Persistent insider unlock pressure, combined with aggressively high valuation multiples (peaking at 30–35x), implied perpetual growth. In reality, LDO’s liquid staking derivative (LSD) market share and LSD’s share of total staked ETH both hit ceilings—capping revenue growth.

The good news? LDO has dropped 96% from its peak—finally bringing its valuation back into reason.

Revenue quality is exceptionally high: stakers rarely churn. So while valuation collapsed, revenue held steady. And that $40M annual revenue is denominated in ETH—meaning it appreciates as ETH rises.

At a $275M market cap, LDO trades at ~7x revenue—or, assuming zero operating costs, implies a 14% yield. Compared to 2024 valuations, a protocol that will *permanently* generate fees is now deeply undervalued.

By the way, downside protection exists too. The treasury currently holds $157M in ETH and stablecoins. Yes, LDO’s spending has been elevated and the treasury is shrinking—but we’ve spoken with contributors who expect tighter cost controls going forward.

Buybacks

This is what makes the trade actionable. We know LDO generates solid revenue; we know more revenue will flow into the treasury as costs are cut—but how does the token benefit *now*?

Just today, the LDO team approved a Snapshot proposal allocating 10,000 stETH for LDO buybacks—and almost no one reported it.

📎 Further reading: Snapshot Proposal Link

At current prices, that’s $22 million—~8% of the circulating supply. This is an explicit “quantitative easing” program—yet the token price barely moved.

For comparison: @monad publicly announced a $30M buyback of its native token at end-January—and has since ranked among the top-performing alts over the past three months.

LDO’s daily trading volume on Binance sits around $3M. Assuming a 6-month buyback window, that’s ~$122K per day—roughly 4% of daily volume. Add in upside potential from rising ETH prices (since revenue is ETH-denominated), and the math looks compelling.

My Conclusion

Lido has durable revenue, an unassailable market position, deep moats, and income that won’t disappear—essentially, forever. Contributors are actively exploring new growth vectors—but none of this is priced in today.

The DAO has finally begun deploying real capital into its own token—and almost no one in crypto Twitter is talking about it.

If risk appetite rebounds, LDO should outperform ETH—with higher elasticity. If we enter a risk-off environment and you’re looking for a place to park capital, LDO’s downside protection is also solid.

At current valuations, LDO is extremely cheap—and insiders appear to agree.

Disclosure: I hold a long LDO position.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News