From 6,000 Points to Two “Circuit Breakers”: South Korea’s Semiconductor Stock Myth Paused by a Single Missile from the Middle East

TechFlow Selected TechFlow Selected

From 6,000 Points to Two “Circuit Breakers”: South Korea’s Semiconductor Stock Myth Paused by a Single Missile from the Middle East

Every investor buying Korean stocks believes they are benefiting from AI chips.

Author: David, TechFlow

The U.S.-Iran conflict continues, triggering panic across global capital markets—South Korea’s stock market has been hit especially hard.

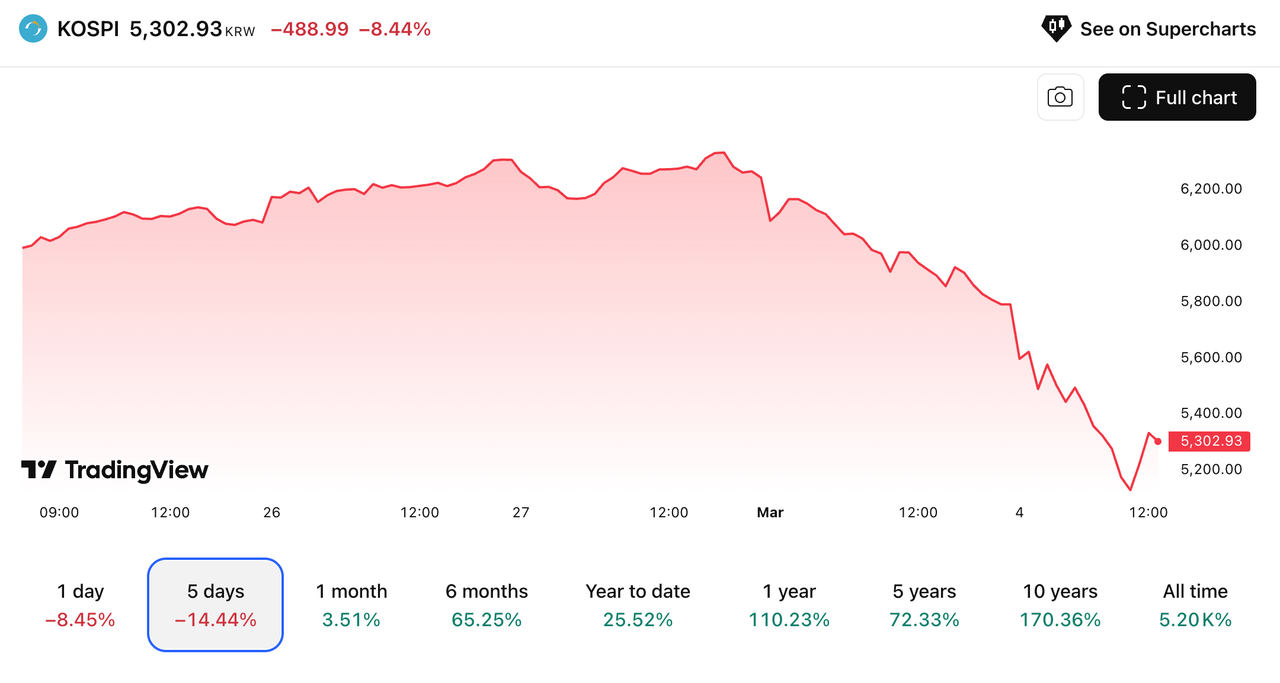

On March 3, the Korea Composite Stock Price Index (KOSPI) plunged 7.24%, triggering a trading halt. Samsung Electronics fell nearly 10%, and SK Hynix dropped 11.5%.

On March 4—the day of publication—KOSPI fell over 8% intraday, triggering another circuit breaker and halting trading for 20 minutes. It closed down roughly 6%, at 5,440 points. Samsung slid another 5.1%, and Hynix dropped another 3.9%.

In just two trading days, the market experienced two circuit breakers, with KOSPI collapsing from 6,244 to 5,440—a nearly 13% decline. This marks the steepest consecutive drop since 2008.

Just one week earlier, on February 25, KOSPI had broken above 6,000 points, pushing South Korea’s total stock market capitalization to $3.76 trillion—exceeding France’s and ranking ninth globally. Samsung and Hynix remained the most lauded stocks among investment bloggers.

War in the Middle East has sent global markets tumbling—but why has South Korea’s fallen hardest?

Buying Korean Stocks = Buying Memory Chips

South Korea’s bull market over the past year boils down, essentially, to the story of two companies.

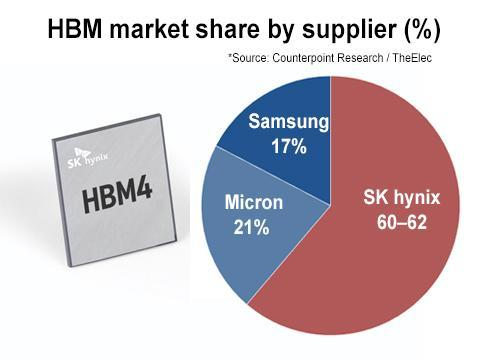

Global AI training requires GPUs, which in turn require high-bandwidth memory (HBM). Manufacturing HBM is extremely difficult, and only three firms worldwide can mass-produce it: SK Hynix, Samsung, and Micron.

SK Hynix alone commands over half the global market share, while Samsung holds around 30%. Together, these two Korean firms control over 80% of global HBM production capacity.

NVIDIA is their largest customer. Every H100 and every B200 GPU shipped relies on memory chips made in Korea. In Q1 2025 alone, NVIDIA posted $68.1 billion in revenue—much of which ultimately flows into SK Hynix’s and Samsung’s coffers.

This translated directly into stock performance: In 2025, SK Hynix surged 274%, while Samsung rose 125%. The entire KOSPI index climbed 75.6%, with nearly half that gain attributable to these two stocks alone.

Buying the Korean broad market is, in essence, buying memory chips.

This year’s momentum has been even stronger. In the first 20 days of February, South Korea’s chip exports surged 134% year-on-year to $15.1 billion—accounting for over one-third of total exports. Goldman Sachs forecasts 120% earnings growth for the Korean stock market in 2026, with 88 percentage points coming from technology hardware.

Put simply: Strip away chips, and Korean equities’ growth dwindles to negligible levels.

KOSPI took just 34 days to climb from 5,000 to 6,000 points. During this period, Nomura raised its target to 8,000, JPMorgan to 7,500, and Goldman Sachs to 6,400. Each number rests on the same assumption:

AI’s demand for computing power has no ceiling—so neither does Korea’s chip industry.

When the Strait Closes, Where Does the Power Come From?

But making chips requires electricity.

Where does South Korea get its electricity? Natural gas and coal each supply about 27%, while nuclear power accounts for 30%. Neither natural gas nor coal is domestically produced—South Korea imports all of it. It is the world’s third-largest importer of liquefied natural gas (LNG), behind only China and Japan.

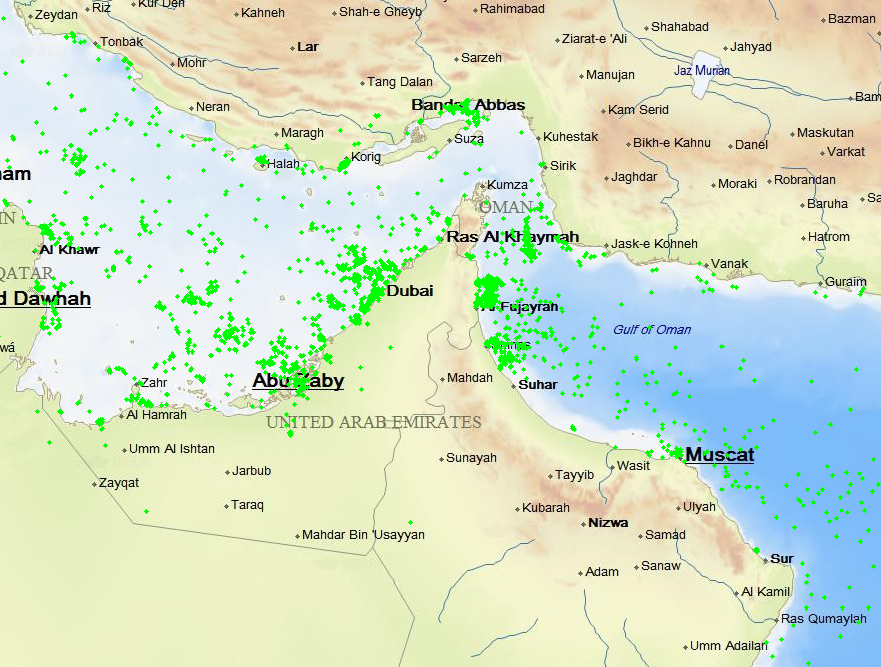

On February 28, the U.S. and Israel jointly launched airstrikes against Iran. After confirmation of Supreme Leader Ayatollah Khamenei’s death, Iran announced the closure of the Strait of Hormuz.

At its narrowest point, the strait is just 33 kilometers wide—and approximately one-fifth of the world’s oil and large volumes of LNG pass through it. Qatar, one of the world’s largest LNG exporters and a primary supplier to South Korea, must route its LNG tankers through this strait.

Once the strait closes, oil prices surge first—then natural gas follows. Global energy markets are inherently interconnected.

Public data shows European natural gas prices rising nearly 50%, and Asian natural gas prices climbing nearly 40%. Following attacks on facilities operated by Qatar Energy—the region’s main LNG supplier—the company suspended LNG production.

Figure: Vessel-tracking data shows a sharp decline in ships transiting the Strait of Hormuz on March 1 local time. | Source: SoShip

Samsung and Hynix do not manufacture chips out of thin air. Producing an HBM chip—from wafer fabrication to final packaging—involves thousands of process steps, each consuming vast amounts of electricity. Semiconductor manufacturing ranks among the world’s most energy-intensive industries.

The theoretical chain looks like this:

NVIDIA places orders → SK Hynix begins production → factories need electricity → electricity generation requires natural gas → natural gas shipments must traverse the Strait of Hormuz → the strait is now closed.

South Korea’s stock market was closed on March 1, coinciding with its national Independence Movement Day holiday. While other markets panicked over the weekend, Korean investors could only watch helplessly.

When trading resumed on Tuesday, three days of accumulated panic compressed into a single red candle. Samsung plunged nearly 10%; Hynix tumbled 11.5%. Rising gas prices push up electricity costs, squeezing chipmakers’ gross margins—and casting doubt on factory utilization rates.

Wednesday brought even sharper declines. Iran escalated from threats to direct action—actively disrupting maritime traffic in the strait. Brent crude breached $82 per barrel, and natural gas prices surged further. Over two days, Samsung fell nearly 15% cumulatively; Hynix dropped 15%.

Yet on the same Korean exchange, Hanwha Aerospace rose nearly 20% on March 3, while LIG Nex1 surged 30% to its daily limit.

Hanwha Aerospace manufactures fighter jets and missile engines; LIG Nex1 produces air defense systems and precision-guided munitions. With war erupting in the Middle East, global militaries rush to replenish inventories.

One sector—chipmakers—is plunging; another—missile-makers—is soaring.

Has the “Korea Discount” Disappeared?

South Korea’s stock market carries a nickname: the “Korea Discount.”

It refers to the phenomenon where identical companies trade at lower valuations when listed in Korea versus the U.S. or Japan. Samsung Electronics and TSMC are both chipmaking giants with comparable profitability—yet TSMC’s price-to-book ratio has long been two to three times higher than Samsung’s.

You might think of it as the same dish costing less in Seoul than in New York.

Why? Because major Korean corporations are almost exclusively controlled by family-run conglomerates—chaebols. Samsung, Hyundai, SK, and LG are all structured via pyramidal cross-shareholding, enabling founding families to exert control over entire empires with minimal equity stakes.

Profits go undistributed as dividends; treasury shares remain unretired; boards consist overwhelmingly of insiders; independent directors have not cast a single dissenting vote in five years. Foreign investors review this governance structure and conclude investing means working for someone else—so they walk away.

How long has this discount persisted? Over the past decade, the S&P 500 rose 179%, the Nikkei 155%, India 255%, and even Brazil surged 167%.

KOSPI rose only 35%.

In 2025, newly elected President Lee Jae-myung introduced sweeping corporate law reforms—mandating dividend payouts, requiring retirement of treasury shares—and personally traveled to the New York Stock Exchange to tell Wall Street: “The Korea Discount is becoming the Korea Premium.”

Simultaneously, AI fundamentally reshaped valuation frameworks for Samsung and Hynix. These two developments collided, drawing massive foreign inflows—and KOSPI surged 75.6% in one year, the highest globally.

A discount built over two decades appeared erased in a single year.

Yet two consecutive days of collapse reveal another issue: The old discount stemmed from poor corporate governance—and governance reform is underway.

But a deeper layer of discount remains buried beneath the surface.

In Korea, two stocks drive half the market’s gains; electricity generation depends on imported natural gas and coal; the entire market rides on a single industry.

When anything outside that industry goes awry, the result is back-to-back circuit breakers. This structural vulnerability—embedded in Korea’s geography and industrial composition—cannot be fixed by corporate law reform alone.

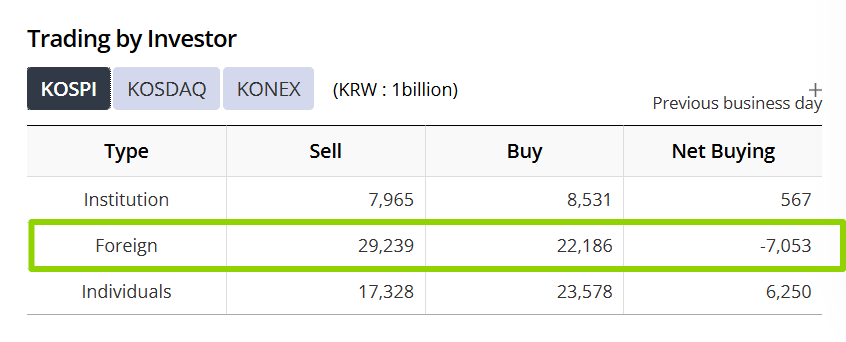

Foreign Capital Exits, Retail Investors Step In

On February 27, foreign investors net-sold ₩6.8 trillion worth of Korean equities—a new single-day record. On March 3, they sold another ₩5.1 trillion. Combined, nearly ₩12 trillion—equivalent to $8.5 billion—vanished in just two days, wiping out half of the inflows accumulated over six weeks.

Foreign investors’ affection for emerging markets has always been conditional. When conditions are favorable, they hail you as the “core of the global AI supply chain”; when conditions shift, you become the most liquid, easiest-to-exit position in their portfolio.

Korea’s stock market is highly active and deeply liquid—precisely because it’s easy to sell, it’s the first to be dumped.

So who’s stepping in to buy?

On March 3, retail investors net-bought ₩5.8 trillion—foreign capital fled, and Korean households rushed in. A post on Seoul Forum declared Samsung’s current price a “once-in-a-decade opportunity.”

The next day, however, the market plunged another 6%, briefly falling 8% intraday and triggering yet another circuit breaker. Those who bought on March 3 lost more money within 24 hours. On March 4, retail investors continued bargain-hunting—but were overwhelmed by foreign selling pressure.

The last time Korean retail investors staged a large-scale buying spree was in August 2024, during the yen-carry-trade collapse. That time, they got it right—and recouped losses within a month. Whether they’ll succeed this time may hinge on a variable entirely beyond their control:

When will the Strait of Hormuz reopen?

Emotion Matters More Than Facts

KOSPI took 34 days to rise from 5,000 to 6,000—and just two days to fall from 6,000 to 5,440.

Two days. Two circuit breakers.

The energy chain is real: LNG must transit the Strait of Hormuz; chips rely on electricity generated from that LNG.

But a 13% two-day plunge isn’t pricing LNG—it’s pricing collective panic. When 75% of a market’s gains depend on just two stocks, everyone crowds into the same exit lane.

After such steep gains, panic favors speed: whoever exits fastest survives longest.

SK Hynix will likely rebound. AI’s compute demand is real. The HBM supply gap is real. NVIDIA’s next-quarter orders won’t vanish just because of war in the Middle East.

But these two days deliver one clear message:A rebound is driven by fundamentals; a crash is driven by sentiment. Fundamentals move slowly; sentiment moves fast.A 34-day rally can lose most of its value in two days.

Every investor buying Korean equities believes they’re capturing AI chip upside.

But for Korea, chips grow on an economy powered by imported natural gas, sell to a customer that may impose tariffs at any moment, and sit beside a nuclear-armed neighbor.

Every research report tells you what a stock is worth.

No report tells you what will happen in the world while you hold it.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News