Bank of Korea’s Interpretation of the AI Semiconductor Cycle: The Most Dangerous Signal Lies in the Financing Side

TechFlow Selected TechFlow Selected

Bank of Korea’s Interpretation of the AI Semiconductor Cycle: The Most Dangerous Signal Lies in the Financing Side

The Bank of Korea judges that both the magnitude and duration of supply-demand imbalance in this memory cycle significantly exceed those of the previous three cycles, with expansion confirmed to continue at least through the first half of 2026.

Compiled by Macro_Lin

Recently, I read a special report published by the Bank of Korea (BoK), titled “Assessing the Sustainability of the Global Semiconductor Boom.” This report is highly distinctive.

South Korea is a global leader in memory chip shipments; in effect, Samsung and SK Hynix’s earnings reports function as de facto national economic reports for the BoK. When this central bank itself steps into the arena to rigorously examine how long this AI-driven semiconductor supercycle can realistically last, its very posture warrants close attention. Sell-side research reports carry bias; bearish reports are emotionally charged. By contrast, the BoK’s report maintains the central bank’s characteristic tone of restraint—its argumentative density far exceeds its emotional density.

Core Takeaways

The BoK judges that both the magnitude and duration of supply-demand imbalance in this memory cycle significantly exceed those of the previous three cycles, with expansion confirmed to continue at least through the first half of 2026. Starting in 2027, however, five variables will jointly determine the timing of the cycle’s reversal—and two of the most worrisome signals have already emerged.

I. What Makes This Cycle Different from the Previous Three?

The BoK divides semiconductor cycles since 2010 into four phases: smartphone proliferation (2013–2015), cloud expansion (2017–2018), pandemic-driven contactless adoption (2020–2021), and the current AI diffusion phase (2024–present).

The script for the past three cycles was identical: new technologies drove demand growth; supply lagged behind, then surged as newly expanded capacity came online—eventually outpacing demand, triggering inventory accumulation, price declines, and cycle reversal. Since 2017, this reversal point has closely aligned with inflection points in U.S. mega-tech firms’ CAPEX.

This cycle differs in three key respects.

First, demand growth is historically unprecedented. High Bandwidth Memory (HBM) shipments have exploded alongside AI accelerator deployments, while general-purpose DRAM demand is also being lifted by inference workloads—resulting in synchronous expansion across all memory categories.

Second, supply elasticity is historically weakest. HBM manufacturing is extremely complex and requires long lead times for capacity ramp-up. Memory manufacturers, having endured the brutal downturn of 2022–2023, are exercising extreme caution in expanding capacity. Moreover, general-purpose DRAM production lines are being repurposed for HBM, further tightening supply of standard DRAM.

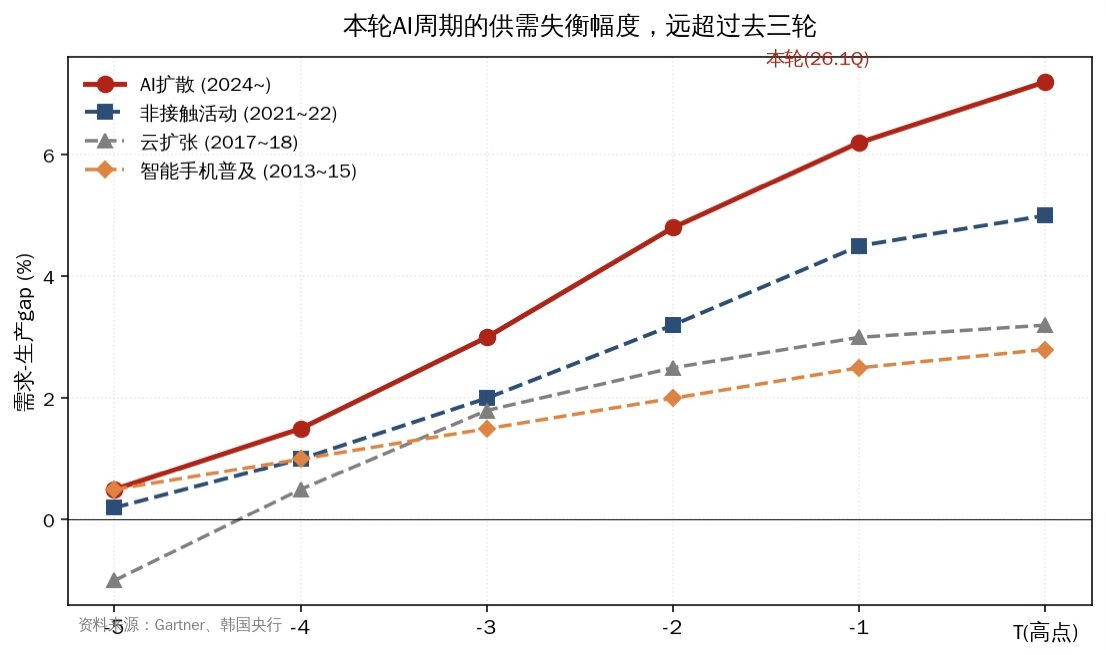

Third, the outcome. The BoK produced a pivotal chart plotting the “demand-production gap” across all four cycles on a single coordinate axis—revealing that this cycle’s degree and duration of imbalance clearly surpass those of the prior three. Inventory levels at both the DRAM manufacturing and end-demand ends are declining, with no signs of accumulation.

Figure 1: Comparison of demand-production gaps across historical semiconductor cycles—the current AI cycle shows markedly greater magnitude and duration

II. Five Variables That Will Determine How Far This Cycle Extends

The BoK lays out a clear five-factor framework—three demand-side, two supply-side. I present them here in order of importance.

① Timing of profitability validation for AI investments. Today, OpenAI and Anthropic remain unprofitable; their valuations and continued investment rely entirely on market expectations of future dominance. The BoK’s assessment is nuanced: starting next year, market focus will shift from “land-grabbing” to “can it generate profits?” Compounding this are data center power constraints, accelerated GPU depreciation, and underutilization risks—making it difficult for CAPEX growth to sustain its current pace.

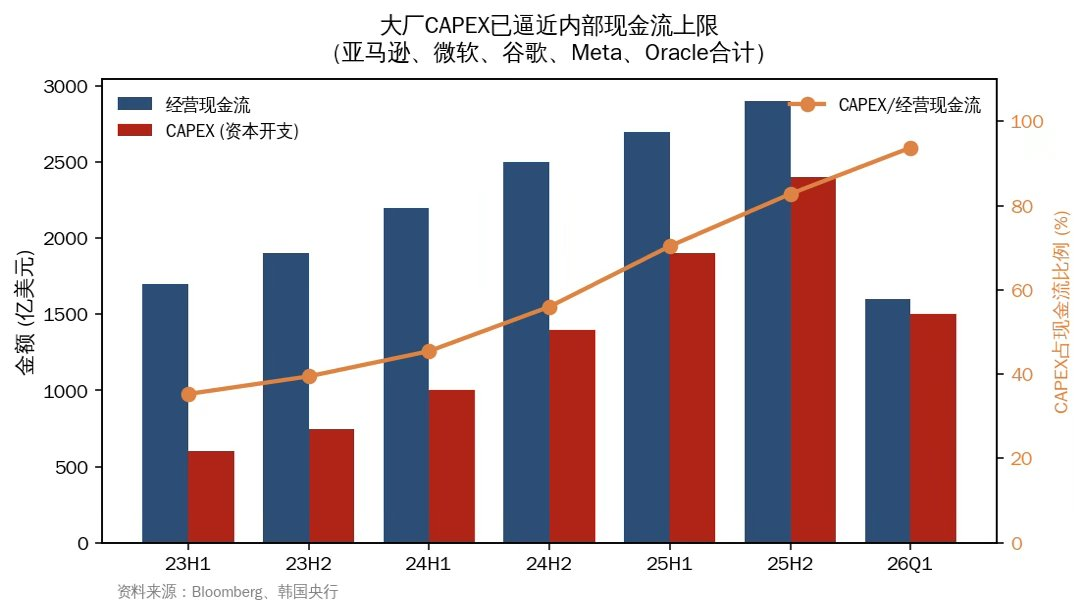

② Whether mega-firms can continue raising capital. This section contains the report’s richest insights. The BoK explicitly draws parallels between today’s situation and the late-1990s telecom bubble—and highlights an emerging deterioration: mega-firms’ internal cash flow can no longer support CAPEX at this scale. Since the second half of last year, these firms have cut back on share buybacks and significantly increased corporate bond issuance; some companies’ credit default swap (CDS) spreads have already widened.

Figure 2: Mega-firms’ operating cash flow can no longer cover CAPEX—the coverage ratio has surged from 25% to nearly 100%

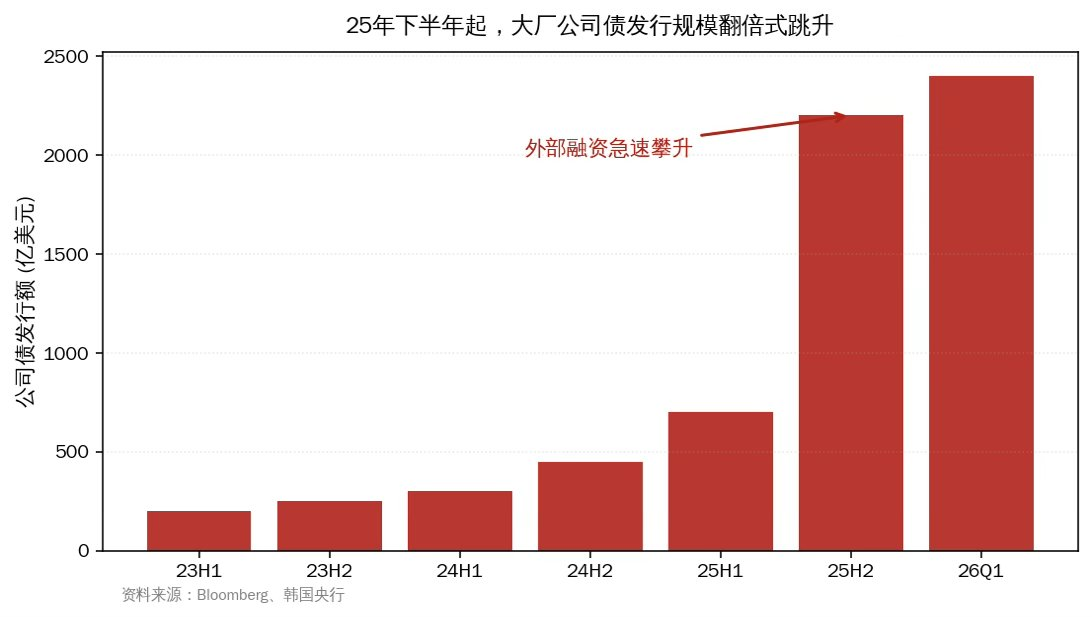

Figure 3: Corporate bond issuance surged starting in H2 2025—external financing has become the primary supplement

Even more concerning is the nature of the financing itself. “Neo-cloud” firms (e.g., CoreWeave), though far smaller than mega-firms, continuously procure GPUs and build AI data centers. NVIDIA extends vendor financing to them to boost its own GPU sales. This structure closely mirrors Cisco’s and Lucent’s vendor financing for nascent telecom companies during the dot-com era.

A further layer involves off-balance-sheet financing. Meta’s Hyperion data center, structured via a Special Purpose Vehicle (SPV) and private credit, carries $29.5 billion in debt that does not appear on Meta’s balance sheet. Oracle’s Stargate ($66 billion) and xAI’s Colossus ($20 billion) use similar structures. The BoK notes a telling detail: in February–March 2026, institutions including Blue Owl, BlackRock, Morgan Stanley, and Cliffwater paused redemptions for certain private credit funds due to AI-related disruption concerns—a crack appearing in the foundation.

③ Progress in AI model efficiency. Following DeepSeek, memory-saving techniques—including quantization compression, Mixture of Experts (MoE), Mamba, NVIDIA’s CMX, and Google’s TurboQuant—have rapidly proliferated. The BoK candidly acknowledges the net impact remains uncertain: efficiency gains could either reduce per-unit demand or, via the Jevons paradox, expand total demand. In the BoK’s overall assessment table, this factor is marked with a bidirectional arrow—the only one among the five without a determinable directional bias.

④ Expansion pace of major memory manufacturers. This year, Samsung’s P4 and SK Hynix’s M15X fabs have already reached full cleanroom utilization—yet still fall short. The real supply release window opens in H2 2027. SK Hynix’s Yongin fab and Micron’s new facility come online in H2 2027; Samsung’s P5 begins production in 2028. These represent hard, calendar-dated supply-side constraints.

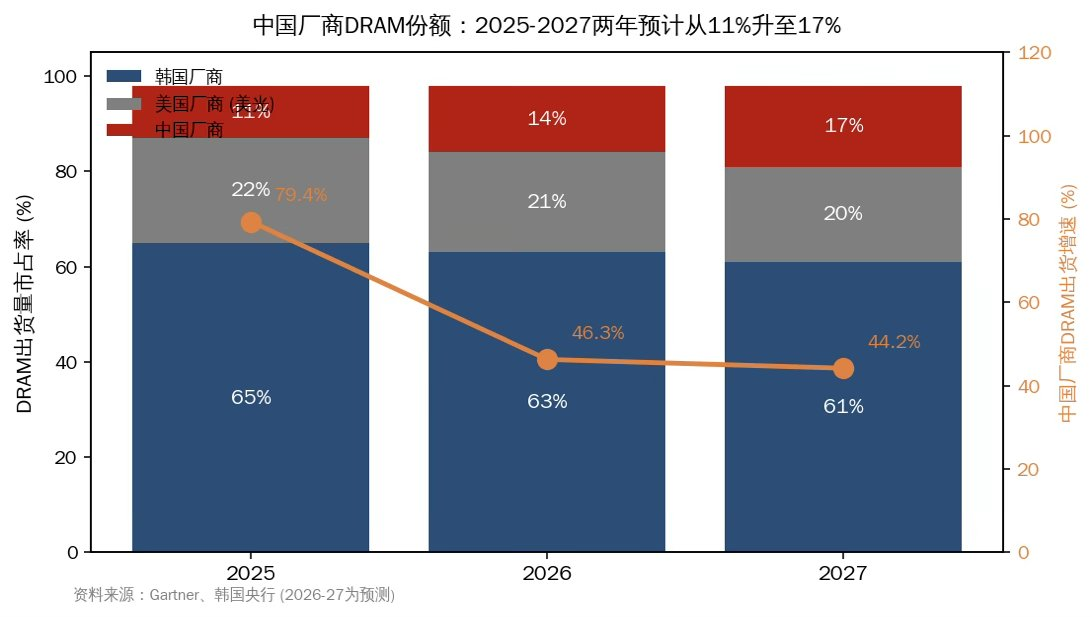

⑤ Pace of Chinese manufacturers’ catch-up. The BoK estimates China lags South Korea technologically by roughly four years—both in HBM and general-purpose DRAM. Thus, the high-end landscape remains stable in the near term. However, one figure stands out: Chinese DRAM vendors’ market share may rise from 10.5% in 2025 to 17% in 2027—a two-year growth rate over three times faster than that of major memory manufacturers. This share gain will exert downward pressure on general-purpose DRAM prices, accelerating the resolution of the current imbalance.

Figure 4: Chinese DRAM vendors’ market share rises from 11% to 17%; shipment growth far outpaces that of major memory manufacturers

III. On the Middle East Conflict, the BoK’s Assessment Is More Sober Than Expected

No evidence currently suggests delayed data center construction or slowed memory supply. The AI investment cycle is dominated by U.S. mega-firms—74% of data centers under construction are located in the Americas. Over the past two years, the linkage between the global economy and semiconductors has notably weakened.

Nonetheless, the BoK outlines several potential transmission channels: rising oil prices increasing data center operating costs; tighter financial conditions raising mega-firms’ funding difficulty; supply disruptions of Middle Eastern raw materials and equipment (bromine, helium); and potential knock-on effects on memory if Taiwan’s system-on-chip production is hampered by energy shortages. The most direct consumer-side backlash is already forecast: Gartner predicts storage price hikes will cause PC shipments to decline 10.4% YoY and smartphone shipments to drop 8.4% YoY in 2026.

IV. Assembling the Timeline

In its final section, the BoK visualizes the relative impact intensity of each of the five factors across 2026, 2027, and 2028 using a color-coded matrix. Below, I translate the matrix’s implications into a chronological narrative.

2026: Demand remains dominant, supply remains constrained—this is the most certain year.

2027: Contradictions begin accumulating. Mega-firms face mounting financing pressure; Chinese capacity expansion accelerates; new fabs have yet to come online, but fragility in the financing channel is already exposed.

2028: Samsung’s P5, SK Hynix’s Yongin, and Micron’s new facility enter mass production simultaneously—supply-side risk intensifies significantly.

A Brief Extension

What makes this report truly compelling is its narrative approach. A central bank whose national economic foundation rests on memory chips does not reflexively cheerlead for its domestic industry. Instead, it devotes substantial space to analyzing the fragility of financing structures, the ambiguous dual-directional impact of technological efficiency, and the subtle inflection point of 2027. Such restraint itself conveys a distinct stance.

The comparison with the telecom bubble is the section I reread multiple times. The original script was: strong initial demand + competitive capacity expansion + a technology breakthrough (WDM wavelength division multiplexing) that arrived faster than anticipated = rapid, severe supply overhang. All three conditions are present in today’s AI industry—the sole difference is the absence, so far, of a WDM-equivalent “tipping-point” technology.

Domestic investors tracking the memory supply chain habitually fixate on supply-side metrics—HBM yield rates, CXMT progress, etc. This BoK report shifts the lens to the other side: the true variable driving this cycle lies on the demand side—and more precisely, within the financing sustainability of the AI industry. Vendor financing extended to neo-cloud firms, off-balance-sheet leverage via SPVs, and suspended redemptions in private credit funds—all these signals warrant closer scrutiny than any capacity expansion timeline.

At minimum, the story continues through the first half of 2026. Beyond that, the plot hinges entirely on how those five variables unfold.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News