Bitget UEX Daily Report | Trump Pledges to Safeguard Crude Oil Transportation; Oil Prices Rally Then Retreat, While Gold and Silver Plummet and the US Dollar Strengthens

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Trump Pledges to Safeguard Crude Oil Transportation; Oil Prices Rally Then Retreat, While Gold and Silver Plummet and the US Dollar Strengthens

Overall market volatility has intensified; it is recommended to allocate defensive assets and monitor the evolving conflict dynamics.

Author: Bitget

I. Top News Highlights

Federal Reserve Updates

Kevin Warsh Faces Major Hurdles Before Taking the Helm; High Oil Prices May Undermine Trump’s Rate-Cut Vision

- Kevin Warsh faces multiple challenges ahead of assuming leadership of the Federal Reserve. U.S. economic trends and Fed officials’ views diverge from White House expectations, while soaring oil prices—reaching a four-year high amid Middle East tensions—further reinforce policymakers’ cautious stance.

- Most Fed officials believe inflation remains elevated and labor markets stable, rendering additional rate cuts unnecessary at this stage. Some colleagues question Warsh’s tech-revolution-centered rationale for easing and his commitment to balance sheet reduction. The Senate has yet to schedule his nomination hearing.

- This could lead to a more conservative Fed interest-rate path, heightening market uncertainty, potentially restraining equity rallies and pushing up bond yields.

International Commodities

Iran Claims Control Over Strait of Hormuz; Trump Offers Shipping Guarantees

- The Islamic Revolutionary Guard Corps (IRGC) Navy declared full control over the Strait of Hormuz. Several tankers ignored wartime warnings and were shelled and set ablaze. President Trump directed the U.S. International Development Finance Corporation (DFC) to provide low-cost political-risk insurance for energy shipments and authorized naval escorts as needed to ensure free global energy flows.

- Over a dozen tankers were struck. Qatar’s largest LNG plant remains offline, causing European natural gas futures to surge over 60% in two days—including a 32% single-day jump. Goldman Sachs urgently raised its April European gas price forecast to €55 per MWh. Asian buyers rushed to secure supplies, dismantling summer stockpiling logic.

- Concerns over energy supply disruptions are intensifying global inflationary pressures. Increased oil-price volatility may indirectly dampen gold’s upside momentum and threaten macroeconomic stability in emerging markets.

Macroeconomic Policy

Trump Says He Can Tolerate Short-Term Oil Price Increases to Prioritize Eliminating Iran Threat

- Trump stated he is willing to accept temporary oil price hikes to prioritize eliminating Iran’s “imminent” threat. U.S. gasoline prices surged sharply due to supply uncertainty. He also indicated that Iran’s arms stockpiles are nearly depleted and that surviving Iranian officials are open to cooperation.

- Military operations have destroyed most of Iran’s naval and aerial assets, significantly weakening its missile-launch capability. U.S. defense reserves remain ample, production is accelerating, and defense contractors are operating at full capacity under emergency orders.

- This posture may prolong the conflict, amplify energy-market uncertainty, boost demand for the U.S. dollar, and dampen global growth expectations.

II. Market Recap

Commodities & FX Performance

- Spot Gold: Up 0.97% to $5,140/oz, following yesterday’s gain of over 4.36%, slightly capped by a stronger dollar.

- Spot Silver: Up 1.52% to $83.20/oz, after yesterday’s surge of over 8.15%; notable pullback accompanied by tightening liquidity.

- WTI Crude Oil: Up 0.72% to $75.10/bbl, following yesterday’s rise of over 5.31%, driven by escalating geopolitical tensions and heightened supply concerns.

- U.S. Dollar Index: Up 1.07% to 99.17, propelled by safe-haven liquidity demand.

Cryptocurrency Performance

- BTC: Down 1.2% to $68,103, continuing volatile trading amid risk aversion.

- ETH: Down 2.67% to $1,975, testing the psychological $2,000 level.

- Total Crypto Market Cap: Down 1.2% to $2.41 trillion, reflecting macro-driven capital outflows.

- Liquidations: Approx. $375 million liquidated across all markets in the past 24 hours, with ~$247 million on long positions.

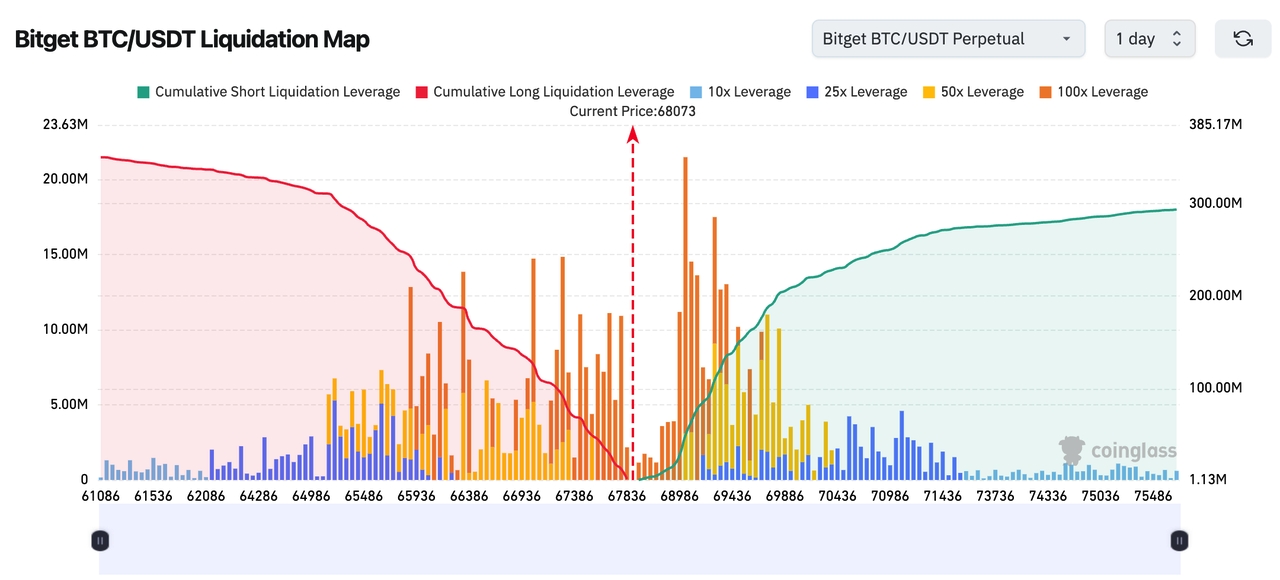

- Bitget BTC/USDT Liquidation Map shows current price near $68,073. A dense cluster of long-position liquidations exists between $67,800–$66,500; a break below may trigger cascading long liquidations. Meanwhile, short-position leverage is heavily concentrated between $69,000–$70,500; an upward breakout could spark a short squeeze, amplifying volatility.

U.S. Equity Index Performance

- Dow Jones Industrial Average: Down 0.83%, narrowing losses after Trump’s shipping assurance statement.

- S&P 500: Down 0.94%, with energy stocks providing partial cushion amid volatility.

- Nasdaq Composite: Down 1.02%, dragged down by technology and semiconductor stocks.

Tech Giants’ Updates

- Microsoft: Up over 1.35%, buoyed by steady cloud service demand.

- Amazon: Up 0.16%, supported by resilient e-commerce performance.

- Meta: Up 0.23%, with relatively robust advertising revenue.

- Nvidia: Down over 1.33%, amid chip supply-chain concerns.

- Alphabet (Google): Down nearly 1%, pressured by search and AI competition.

- Apple: Down 0.37%, as MacBook price hikes may prompt consumer hesitation.

- Tesla: Down 2.7%, potentially impacted by delays in Samsung’s U.S.-based Taylor plant ramp-up affecting EV chip supply. Overall, tech giants posted mixed results, primarily due to amplified chip and supply-chain risks stemming from geopolitical tensions—defensive names like Microsoft rose against the trend.

Sector Movement Observations

Gold Stocks Down Over 7%

- Key stocks: Newmont down over 7%; Barrick Gold down over 8%.

- Drivers: Sharp gold-price decline combined with a strong dollar suppressed valuations; tightening liquidity intensified selling pressure.

Silver Stocks Down Over 10%

- Key stocks: First Majestic Silver down over 10%; Coeur Mining down over 10%.

- Drivers: Plummeting silver prices amid industrial-demand concerns; risk-off sentiment shifted toward the dollar.

AI Application Software Stocks Up Over 2%

- Key stocks: ServiceNow up over 3%; Adobe up over 3%.

- Drivers: Sustained strong AI demand, resilience against macro uncertainty, and provision of growth buffer.

Popular Chinese Internet Stocks Down Over 2%

- Key stocks: Alibaba down over 4%; NIO down over 2%.

- Drivers: Global risk aversion spilling over into emerging markets; amplified concerns over supply-chain disruptions.

III. In-Depth Stock Analysis

1. MongoDB – Q1 Guidance Misses Expectations

Event Summary: MongoDB issued Q1 revenue guidance of $659–$664 million and adjusted EPS of $1.15–$1.19—both below analyst consensus estimates of $662.5 million and $1.20—triggering a >22% share price plunge to a six-month low. This followed broader software-stock selloffs, underscoring sector-wide valuation pressure. Market Interpretation: J.P. Morgan’s co-head of equity strategy warned that software-stock selling pressure may persist, noting U.S. equities have entered a “sell first, buy later” mode. While the current decline may not be fully rational, contagion to other sectors is possible; institutions are closely monitoring consumer demand and external uncertainties. Investment Implication: Avoid tech stocks amid near-term correction risks; wait for subsequent earnings reports to confirm demand recovery before re-entering.

2. Paramount Skydance – Rating Downgraded to Junk Status

Event Summary: Fitch downgraded Paramount Skydance and its subsidiaries’ long-term issuer default rating from BBB− (just above investment grade) to BB+ (speculative grade), placing them on Negative Watch. Post-merger net debt stands at $79 billion, significantly weakening risk resilience in a highly competitive and structurally shifting media landscape. Shares fell nearly 7% yesterday. Market Interpretation: Institutions express concern over ambiguous deal terms, financing arrangements, and deleveraging plans. The downgrade reflects fragile financial structure and heightened vulnerability to market swings—highlighting transformational challenges across the media industry. Investment Implication: Near-term share price pressure expected; await clarity on financing details before reassessing long-term potential.

3. Pinterest – Elliott Injects $1 Billion

Event Summary: Activist investor Elliott injected $1 billion into Pinterest to support its multi-year share repurchase program. The board approved an additional $3.5 billion buyback authorization and plans to deploy up to $500 million in cash for further repurchases. The announcement drove shares up >9% yesterday. Market Interpretation: Institutions view this as a strong positive signal for shareholder value enhancement. The scale of buybacks signals management confidence—particularly amid intensifying social-platform competition—and provides valuation support. Investment Implication: Buybacks bolster medium-term confidence; consider holding while monitoring user-growth metrics.

4. AutoZone – Q2 Sales Below Expectations

Event Summary: Auto parts retailer AutoZone reported Q2 sales growth of over 8% to ~$4.27 billion—below the analyst consensus of $4.31 billion. Net income declined nearly 4% to $469 million; EPS of $27.63 slightly exceeded the $27.13 consensus. Shares fell >6% yesterday, pressured by tariffs, winter storms, and automotive-market instability. Market Interpretation: Though consumer demand remains stable, external factors are exacerbating earnings volatility. Institutions stress the need to monitor supply-chain and cyclical risks. Investment Implication: Elevated near-term volatility; long-term prospects benefit from recovering auto-maintenance demand.

5. Ross Stores – Annual Guidance Beats Expectations

Event Summary: Off-price retailer Ross Stores released annual guidance exceeding market expectations, driving after-hours shares up >6%. This reflects retail-consumer resilience and optimized inventory management, building on strong prior-quarter performance. Market Interpretation: Analysts see this as evidence of retail-sector recovery, with the off-price model gaining advantage amid persistent inflation. Target prices have been raised. Investment Implication: Opportunities emerging in the consumer sector; suitable for allocating defensive retail exposure.

IV. Cryptocurrency Project Updates

- On-chain data shows the U.S. government transferred approximately 0.3346 BTC—valued at ~$23,000—from a seized-funds wallet labeled as linked to “Miguel Villanueva.”

- Per Onchain Lens, Circle minted 1 billion new USDC tokens on Solana over the past 10 hours. Additionally, amid geopolitical tensions lifting oil prices and weakening rate-cut expectations, Mizuho analysts raised their target price for Circle from $90 to $100, maintaining a “Neutral” rating. They note that shifts in interest-rate expectations may impact Circle’s valuation multiples more than near-term revenue uplift.

- U.S. President Trump posted on Truth Social stating that the GENIUS stablecoin legislation is being threatened and undermined by banks.

- CFTC Chairman Mike Selig stated the agency will release policy guidance within the coming weeks to enable compliant listing of crypto perpetual contracts in the U.S., and to advance the launch of “professional-grade” perpetual futures.

- MARA Holdings disclosed in its latest SEC 10-K filing that it has expanded its 2026 digital asset management strategy—from previously selling only BTC mined in the same year—to now permitting sales of accumulated BTC held on its balance sheet.

- Per Onchain Lens, BlackRock withdrew 4,376 BTC (~$298 million) from Coinbase over the past 10 hours, while depositing 567 BTC (~$38.05 million) and 7,553 ETH (~$14.7 million) back into Coinbase.

V. Today’s Market Calendar

Data Release Schedule

| 08:15 | U.S. | ADP Nonfarm Employment Change | ⭐⭐⭐⭐ |

| 09:45 | U.S. | S&P Services PMI Final | ⭐⭐⭐ |

| 10:00 | U.S. | ISM Services PMI | ⭐⭐⭐⭐ |

| 00:45 | Eurozone | France Government Budget Balance | ⭐⭐⭐ |

| 01:00 | Eurozone | Spain Unemployment Change | ⭐⭐⭐ |

Key Event Preview

March 4 (Wednesday)

- U.S. releases February ADP employment numbers, S&P Global Services PMI final, and February ISM Non-Manufacturing PMI;

- Nvidia CEO Jensen Huang to participate in a fireside chat at Morgan Stanley’s TMT (Technology, Media & Telecom) Conference in San Francisco;

- After-market: Chip giant Broadcom (AVGO) reports earnings—extending the U.S. market’s discussion around AI investment fervor. (5-star event)

- After-market: Cybersecurity firm CrowdStrike reports earnings.

March 5 (Thursday)

- 21:30 ET: Weekly Initial Jobless Claims; 03:00 ET: Fed releases Beige Book.

March 6 (Friday)

- 21:30 ET: February Unemployment Rate and Seasonally Adjusted Nonfarm Payrolls (forecast: +60,000 jobs). (5-star event)

Institutional Views:

Risk aversion dominated U.S. equities on March 3. Indices such as the Dow plunged early but pared losses. Energy stocks benefited from a 4.7% oil-price surge. Gold, despite falling 4.41%, retained safe-haven support; institutions view $5,200 as a key level, with a short-term rebound likely. Crude oil rose to $74.56 amid Strait-of-Hormuz disruption risks; Brent crude tests above $80, potentially exacerbating inflation. The U.S. Dollar Index climbed 1.07% to 99.42, reinforced by liquidity demand, pressuring emerging-market currencies. Overall market volatility widened; investors are advised to allocate to defensive assets and closely monitor conflict developments.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News