Identity, Traceability, Attribution: Decoding the Three Breakthrough Points of the Next-Generation AI Agent Economy

TechFlow Selected TechFlow Selected

Identity, Traceability, Attribution: Decoding the Three Breakthrough Points of the Next-Generation AI Agent Economy

Exploring the new infrastructure of trust for autonomous agent economies.

Author: Decentralised.co

Translation: AididaoJP, Foresight News

In the article "Internet Pricing," we argued that when metered payments are frictionless, machines will automatically pay. Humans have not fully embraced micropayments because monitoring usage requires mental effort and attention. Machines are different—they see only 1s and 0s. Their processing capacity or task-switching does not affect their ability to execute. If breaking costs down to sub-cent levels makes processes more efficient, they will do so—unlike humans.

We ended the previous article with a question: What happens when agents mess things up? Whether an agent's intent is correct doesn't matter. The key point is that we cannot supervise agents at every step.

This puts us in a dilemma: new technologies fail to inherit a major advantage of existing infrastructure—the ability to reverse payments when errors occur. This is the issue we explore in this article. We’ll discuss what autonomy requires for agents, who is building the foundational layers, and why startups are emerging at the intersection of blockchain payment channels and autonomous agents.

Emerging Standards

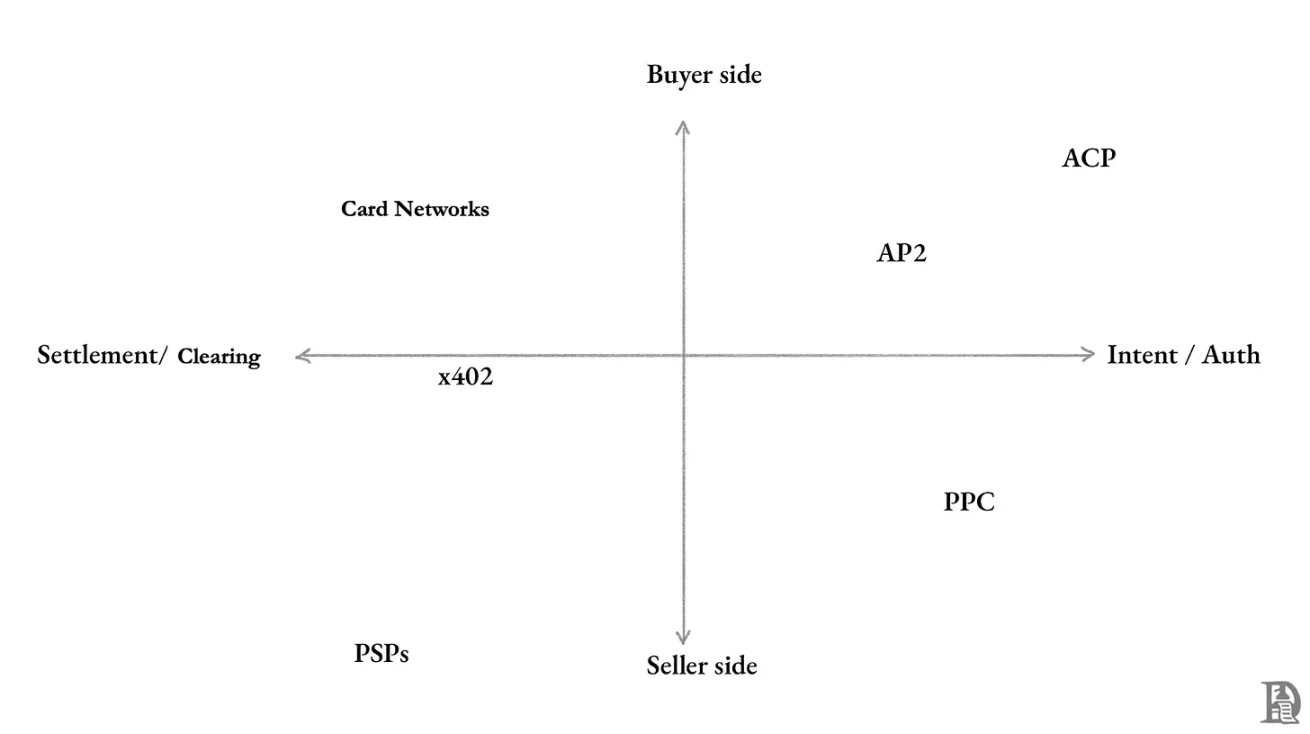

Any commercial activity involves three parties: buyer, seller, and intermediary enabling the transaction. Intermediaries can be platforms like Amazon or payment networks like Visa.

Buyer

Consumer apps typically handle funds or transactions and take a cut. But what happens when the consumer is an AI acting on our behalf? Several emerging standards are now seeking answers.

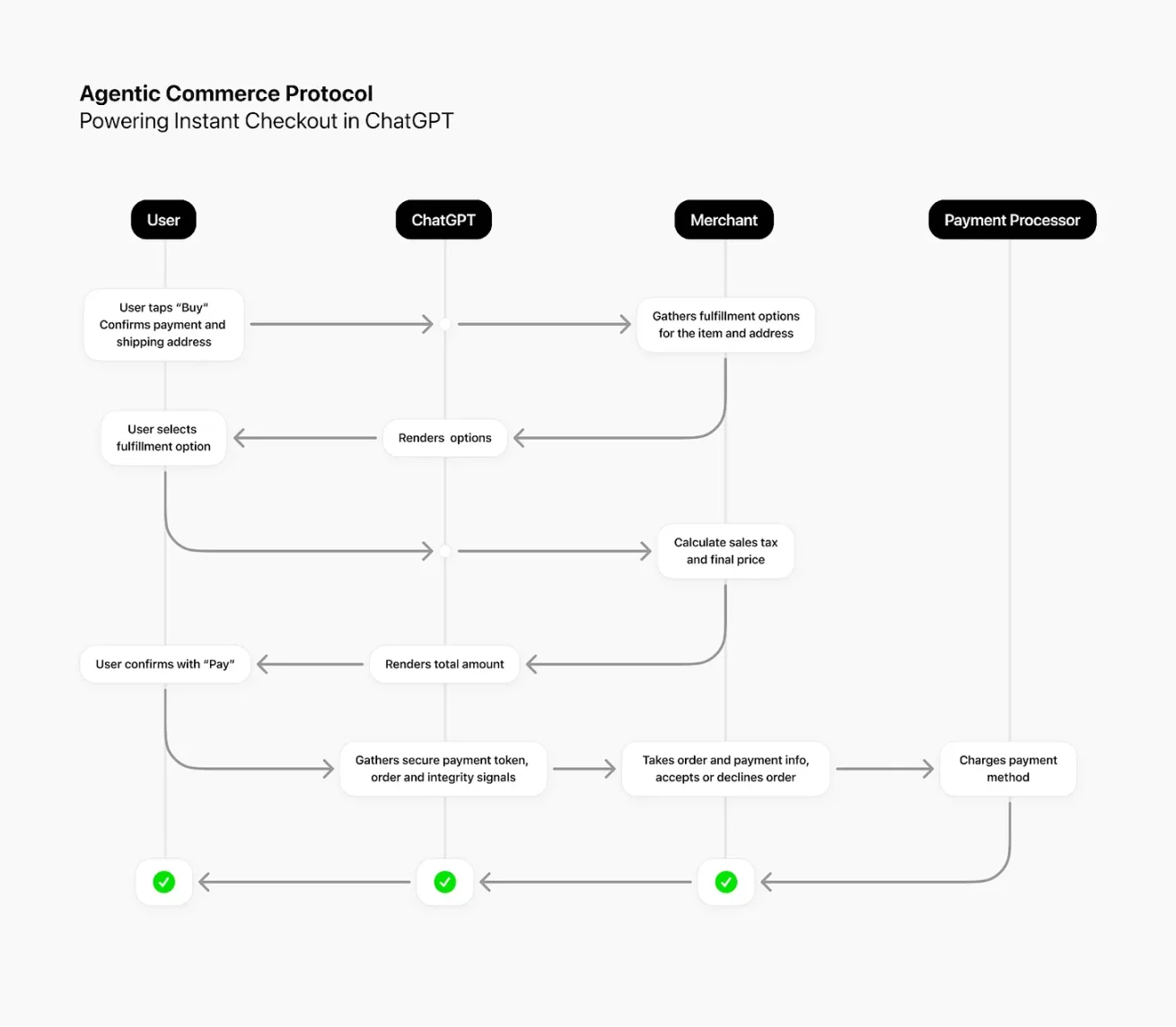

ChatGPT has 700 million active users, all trying to obtain information or services through AI. While we don’t yet directly buy goods via agent interfaces, we already widely use them to “discover” products. Whether buying running shoes or finding a hotel in El Calafate, I use AI for price comparisons. Being able to purchase directly within the same interface would clearly be far more convenient. This is precisely the goal of OpenAI and Stripe’s collaboration on the Autonomous Commerce Protocol (ACP).

Source: OpenAI

This is currently the most direct way for agents to handle funds: full user control throughout. After the user places an order, ChatGPT sends necessary information to the merchant backend via ACP. The merchant then decides whether to accept or reject the order, processes payment through existing payment providers, and handles shipping and customer service as usual.

You can think of ACP commerce as authorizing an intern to spend a fixed budget, with you making the final decision on which product/service to choose, from which vendor, and completing the payment.

OpenAI and Stripe have ACP, while Google has introduced the Agent Payment Protocol (AP2). Before diving into AP2, let’s take a step back. Google aims to solve the problem of “interoperability.” Currently, AI agents operate in silos: Gemini doesn’t talk to Claude, and ChatGPT knows nothing about what happens in Perplexity.

Ideally, when tasks become complex and require collaboration, we want these agents to communicate in a common language. To achieve this, Google developed A2A (Agent-to-Agent protocol), enabling different agents to coordinate and communicate.

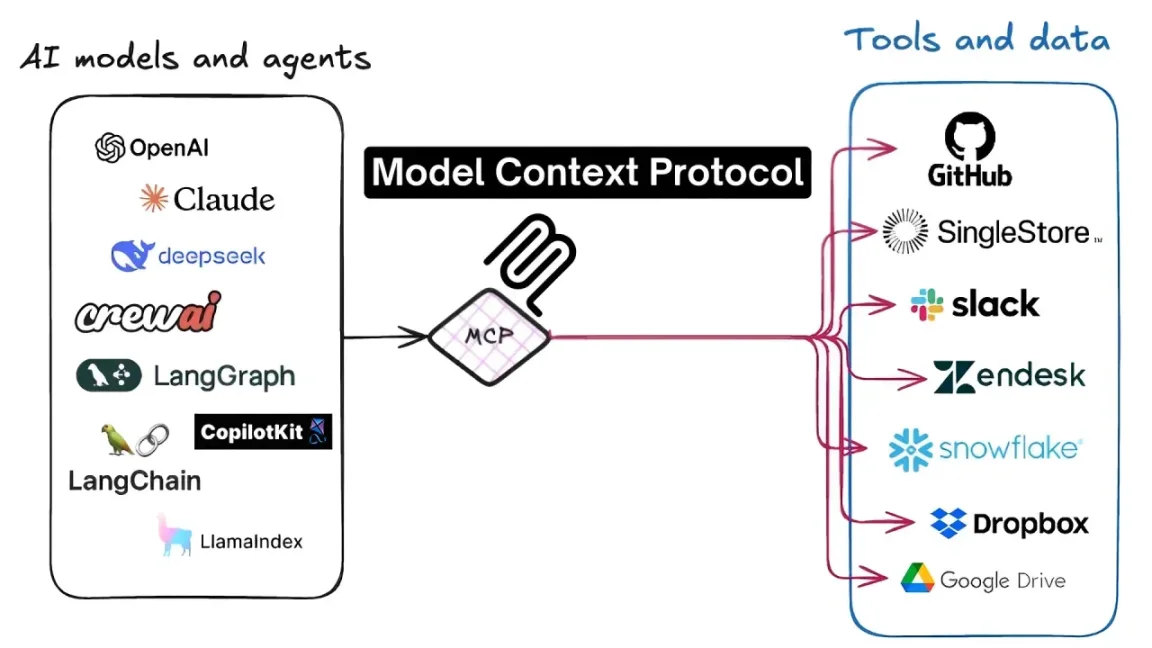

But being able to talk isn’t enough. Agents also need to use tools, access APIs, and services. The Model Context Protocol (MCP) enables agents to use tools like Google Calendar, Notion, and Figma.

Source: Level Up Coding

MCP defines a universal language. As long as agents “speak” MCP, they can use any tool without additional custom code. Developed by Anthropic, the specification is open and rapidly adopted across companies. An MCP server acts as a translation layer sitting in front of a company’s existing APIs, exposing services in standardized format to any MCP-compatible agent.

Back to AP2, it can be simply understood as follows: MCP gives agents access to data, files, and tools; A2A gives them a voice to talk to each other; and AP2 gives them a wallet to spend securely.

All these protocols keep users at the center of control, granting agents only limited spending permissions. They address distribution and workflow issues, but none answer the critical question: what happens when agents make mistakes?

Seller

The story isn’t just on the buyer side. New standards are also emerging on the seller side, focusing on how machines pay for API, data, and content access.

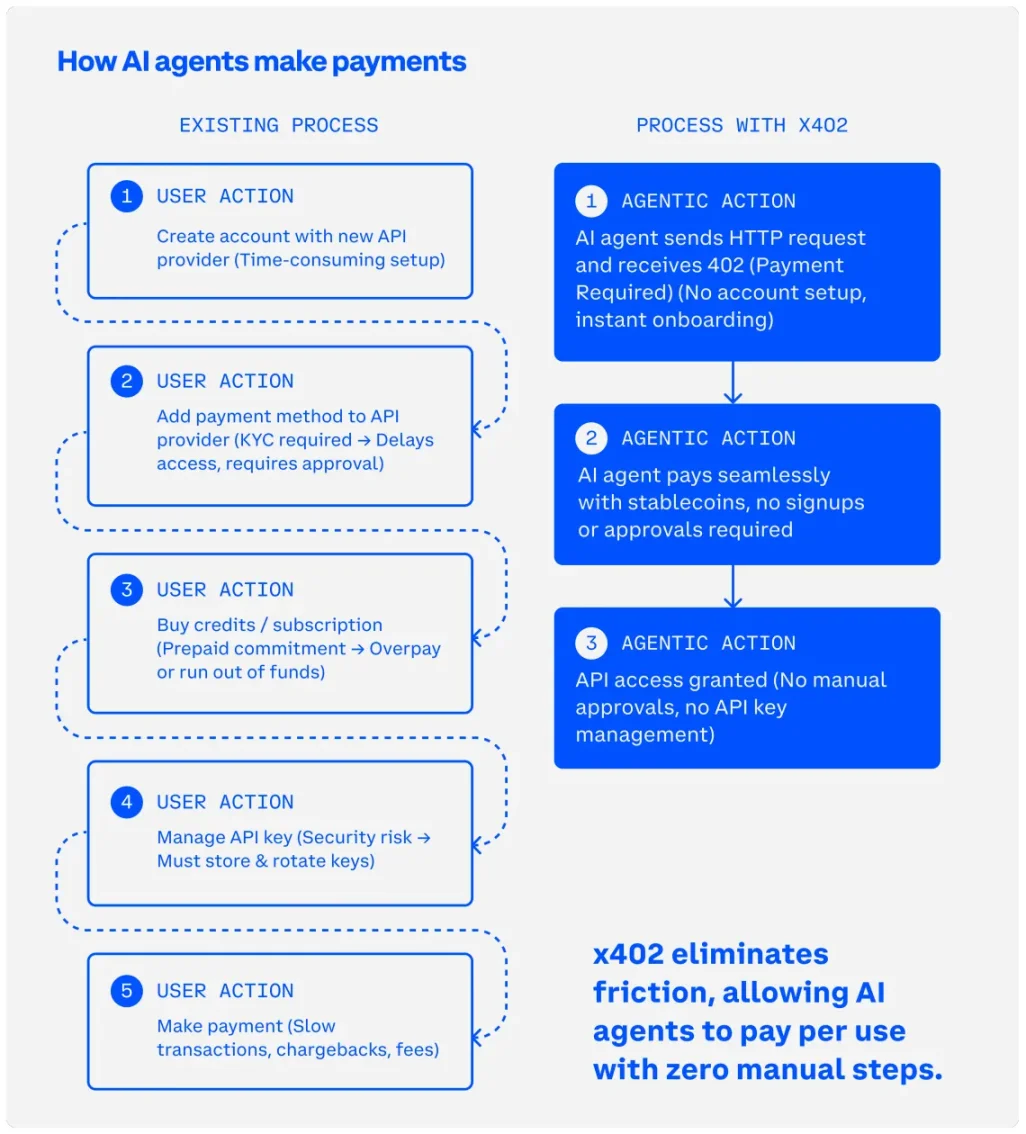

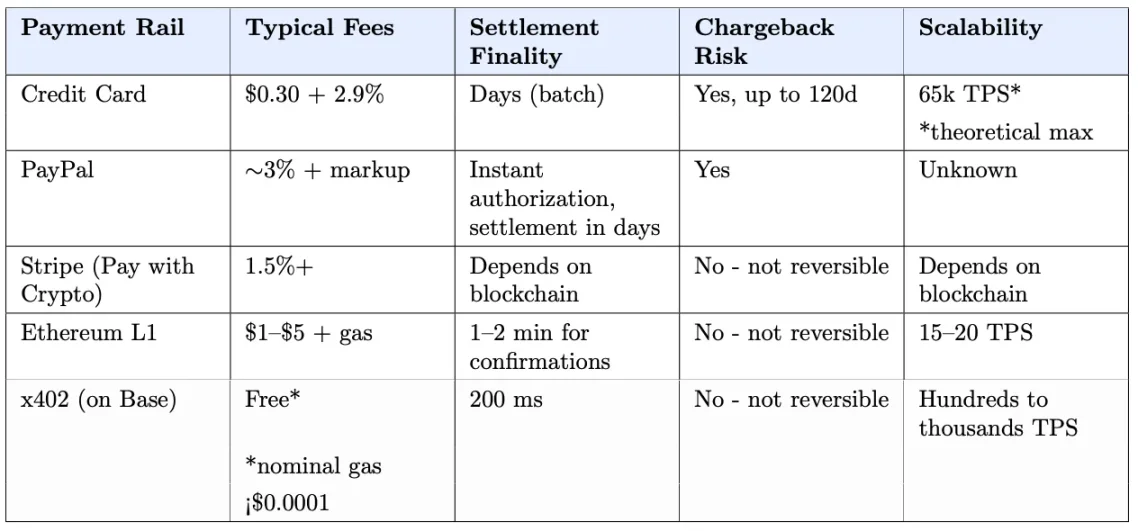

The most discussed standard today is x402, an open protocol developed by Coinbase. It revives the HTTP status code 402—"Payment Required"—defined back in 1997 but never used. By combining it with stablecoin payments, x402 breathes new life into this status code, enabling economically efficient micropayment settlement.

x402 turns HTTP requests into paid requests. Whenever payment is required, the server issues a demand. Since agents have preset budgets, they can pay the server and retrieve data within the same flow. This makes "pay-per-request" or "pay-per-call" feasible in machine-to-machine transactions.

With x402, agents can pay exactly what they need right when they need it. For example, spending 2 cents to read a paywalled article, or fractions of a cent for a single API call. Transactions settle on-chain within seconds, without requiring long-term relationships.

Source: Coinbase's x402 paper

Cloudflare has borrowed this concept to build a more specific "pay-per-crawl" system. It also uses HTTP 402 at its core, but the key difference lies in Cloudflare’s dominant market position—20% of global web traffic flows through its network, giving it immense influence.

"Pay-per-crawl" leverages Cloudflare’s edge network to require payment before delivering content to AI crawlers. This turns content access into mandatory metering. Publishers are facing plummeting traffic as people no longer click through from search engines but instead read AI-generated summaries directly. With this system, publishers can charge AI labs directly each time their content is accessed by crawlers.

Card networks are also attempting to extend existing payment rails to handle agent transactions. Visa has launched an MCP server and agent acceptance toolkit. Mastercard has a project called "Agent Payments." Both are still in early pilot stages, but they’re important because Visa and Mastercard already possess global distribution networks, issuing bank relationships, and extensive merchant acceptance ecosystems. The basic idea is to register agents, set spending controls, and allow agents to initiate transactions over existing human credit card payment networks.

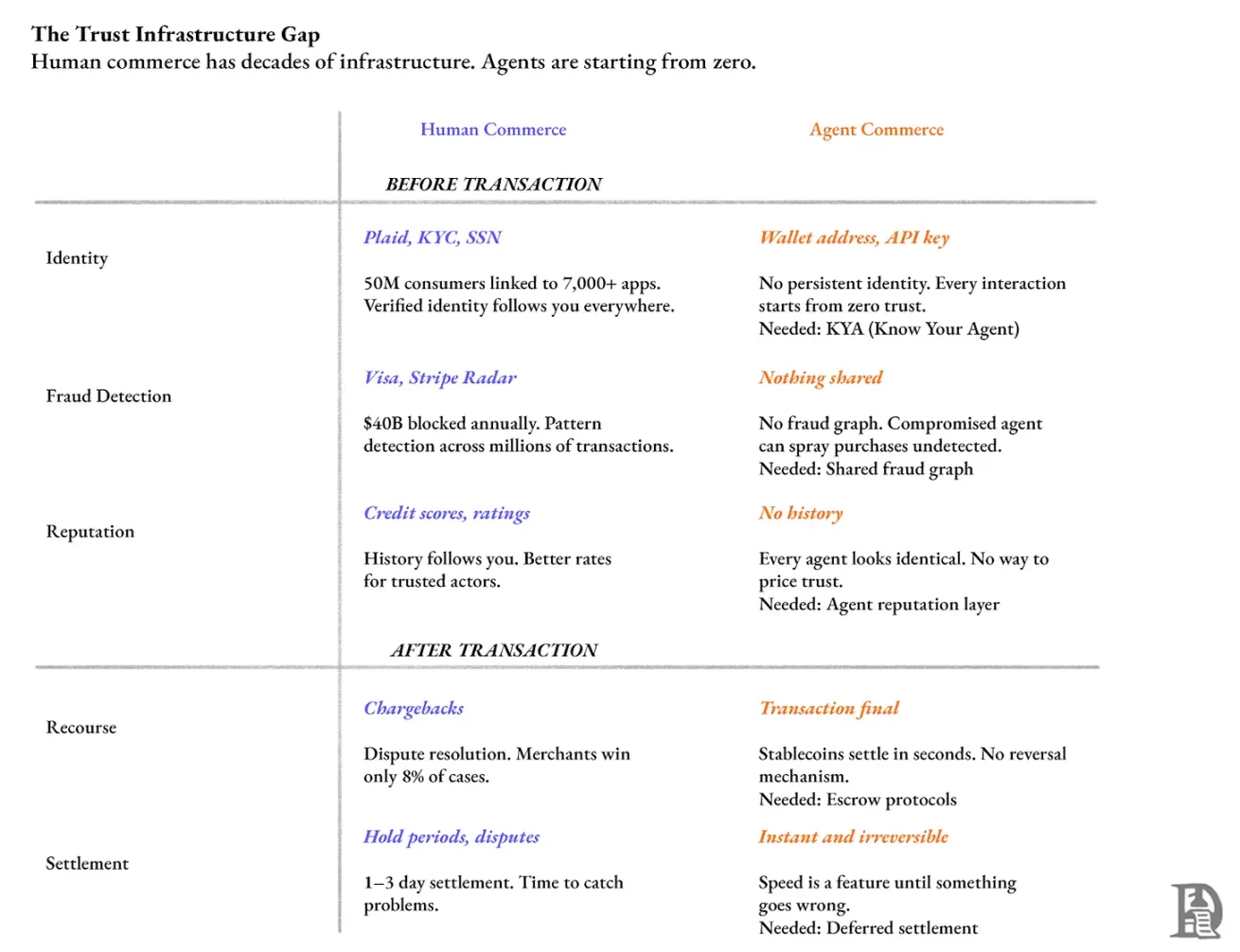

Closing the Trust Gap

All the above standards assume payments proceed smoothly and outcomes meet expectations. ACP and AP2 involve humans at checkout, providing some level of safety. x402 variants handle machine-to-machine data access, which typically carries low risk. Card networks extend familiar protection mechanisms, but at the cost of slow settlement and high fees.

Speed is paramount for scaling micropayments. Card network settlements take days, and merchants pay fees amounting to several percent of transaction value. Cryptocurrency channels settle in seconds, costing less than a cent. But this efficiency comes with irreversibility—crypto payments, once made, cannot be undone.

Traditional commerce has built entire infrastructures around the assumption that things can go wrong. When a credit card purchase goes bad, there’s a process: contact your bank, file a dispute, the card network investigates and holds funds temporarily, and finally rules on refund or merchant support. In 2025, 261 million transactions were disputed, totaling $34 billion.

Yet agents operating over stablecoin channels have none of these safeguards.

The problem becomes even more complex when agents start collaborating. When hundreds or thousands of multi-agent workflows intertwine, determining responsibility could become a nightmare.

Card networks won’t bear this risk—at least not under their current business models. Visa and Mastercard’s agent projects still charge standard interchange fees, and settlements still take days. They could switch to instant stablecoin settlement, but that would mean abandoning the dispute resolution system upon which their fees are based.

Traditional finance’s dispute resolution wasn’t built overnight. The first credit card (Diners Club) emerged around 1950, but consumers waited another 24 years to gain the right to dispute transactions. The modern infrastructure we take for granted today evolved gradually as problems arose.

Autonomous agent commerce doesn’t have that luxury of time. API requests already account for 60% of dynamic HTTP traffic processed by Cloudflare. Bot and automated traffic now approach half of all web traffic. ChatGPT’s 700 million users can already check out directly on Etsy via ACP, with Shopify integration coming soon. Transaction volume already exists, and users have latent demand for using agents to complete tasks—agent-driven commerce is imminent.

Therefore, we face a choice: continue with traditional financial infrastructure and its slow settlement, or consciously build trust infrastructure to match fast blockchain settlement? The former will limit agent potential; the latter is both an opportunity and a necessary evolution for autonomous agent commerce.

So, How Exactly Do We Build It?

Unsurprisingly, this involves two parts: pre-transaction and post-transaction.

Pre-Transaction: Should the Agent Be Allowed to Transact?

This depends on three factors: identifying the counterparty, fraud detection, and using reputation scores to determine pricing and access rights.

In the U.S., Plaid connects nearly half of all bank accounts, processing millions of account verifications daily. When you verify your identity on Venmo, you’re using Plaid.

Currently, any agent interacting with APIs, scraping web pages, or initiating payments lacks equivalent identity verification. Servers see only a vague ID (such as a wallet address or API key), with no knowledge of who is calling. Without cross-service universal identity, reputation cannot accumulate, and every interaction starts from “zero trust.”

In 2024, U.S. adults lost approximately $47 billion to identity fraud.

We need a “Know Your Agent” (KYA) layer, similar to how Plaid provides identity infrastructure for fintech. It should issue persistent, revocable credentials binding agents to their underlying human or organizational principals.

Card networks spent decades building systems capable of detecting suspicious patterns from millions of transactions. They understand normal human spending behavior and can flag anomalies in real time. If an agent is compromised and makes unauthorized purchases across multiple merchants, there is currently no shared fraud graph to detect it.

Visa reported that after investing $11 billion in security between 2019–2024, its systems blocked $40 billion in fraudulent attempts. Stripe processes over $1.4 trillion in payments annually, training its Radar anti-fraud system. During Black Friday and Cyber Monday 2024, Radar blocked 20.9 million fraudulent transactions worth $917 million.

Agent transactions currently lack such fraud detection layers. When an agent makes an x402 payment, there’s no shared system to flag abnormal behavior like sudden spending spikes or unusual frequency.

Without persistent identity and reputation, every agent interaction starts from zero. Reputation is deeply embedded in human commerce: the ads you see are based on browsing history, Uber ratings affect driver pickups, credit scores follow you to every financial institution. Agents deserve the same.

Post-Transaction: What Happens When Things Go Wrong?

Chargebacks are how card networks handle disputes: when a customer disputes a transaction via their bank, funds are pulled back from the merchant. But this is often abused. In 2023, chargebacks cost merchants about $117.47 billion. For every $1 lost in refunds, merchants typically incur $3.75–$4.61 in additional costs (including fees, lost goods, and administrative overhead).

Source: Coinbase's x402 paper

Merchants win only 8.1% of actively contested disputes. 84% of customers believe initiating a chargeback through their bank is simpler than requesting a refund from the merchant.

Stablecoin transactions initiated by agents settle in seconds and are currently irreversible. Cloudflare has proposed a delayed settlement extension for x402, allowing a “waiting period” before funds are finally transferred.

Developers are already building early versions of this infrastructure. At ETHGlobal Buenos Aires hackathon, one team created Private-Escrow x402. Its escrow mechanism works as follows: the buyer deposits funds into a smart contract, signs a “payment intent” off-chain during payment. A coordinator batches hundreds of such signatures into a single settlement transaction, reducing gas fees by 28x.

But this is just a basic component—it needs to be productized.

Who Will Build All This?

This reminds me of the era when telecom operators dominated the industry. They held billing relationships with every mobile user, yet missed capturing the value created by smartphones. App distribution and mobile advertising generated hundreds of billions in revenue—value that could have belonged to carriers.

Card networks now face a similar situation. Visa and Mastercard have spent decades building the very trust infrastructure that autonomous agent economies lack. But their business model relies entirely on interchange fees, which depend on controlling the payment rail. They invest heavily in maintaining this infrastructure, funded by taking a few percentage points from each transaction. Offering consumer protections for stablecoin transactions would mean subsidizing competitors’ payment rails with their own revenue.

If card networks won’t act, the next candidates are AI labs like OpenAI, Google, and Anthropic. They all want their agents to be widely adopted. But operating a centralized identity registry means taking responsibility when agents misbehave. They don’t want to become the court deciding your “wrong hotel booking” disputes.

They’d prefer third parties to build identity and recourse infrastructure that they can plug into directly, just as they integrate with payment systems or search engines today.

Cloudflare is in a unique position. It already processes massive web traffic, runs bot detection, and its “AI Audit” tool allows publishers to track crawler visits. Moving from “identifying bots” to “verifying agent identity and reputation” is not a huge technical leap.

But Cloudflare has always positioned itself as neutral infrastructure. Once it begins issuing trust scores or adjudicating disputes, it becomes more like a regulator—a different business, and one with different liabilities.

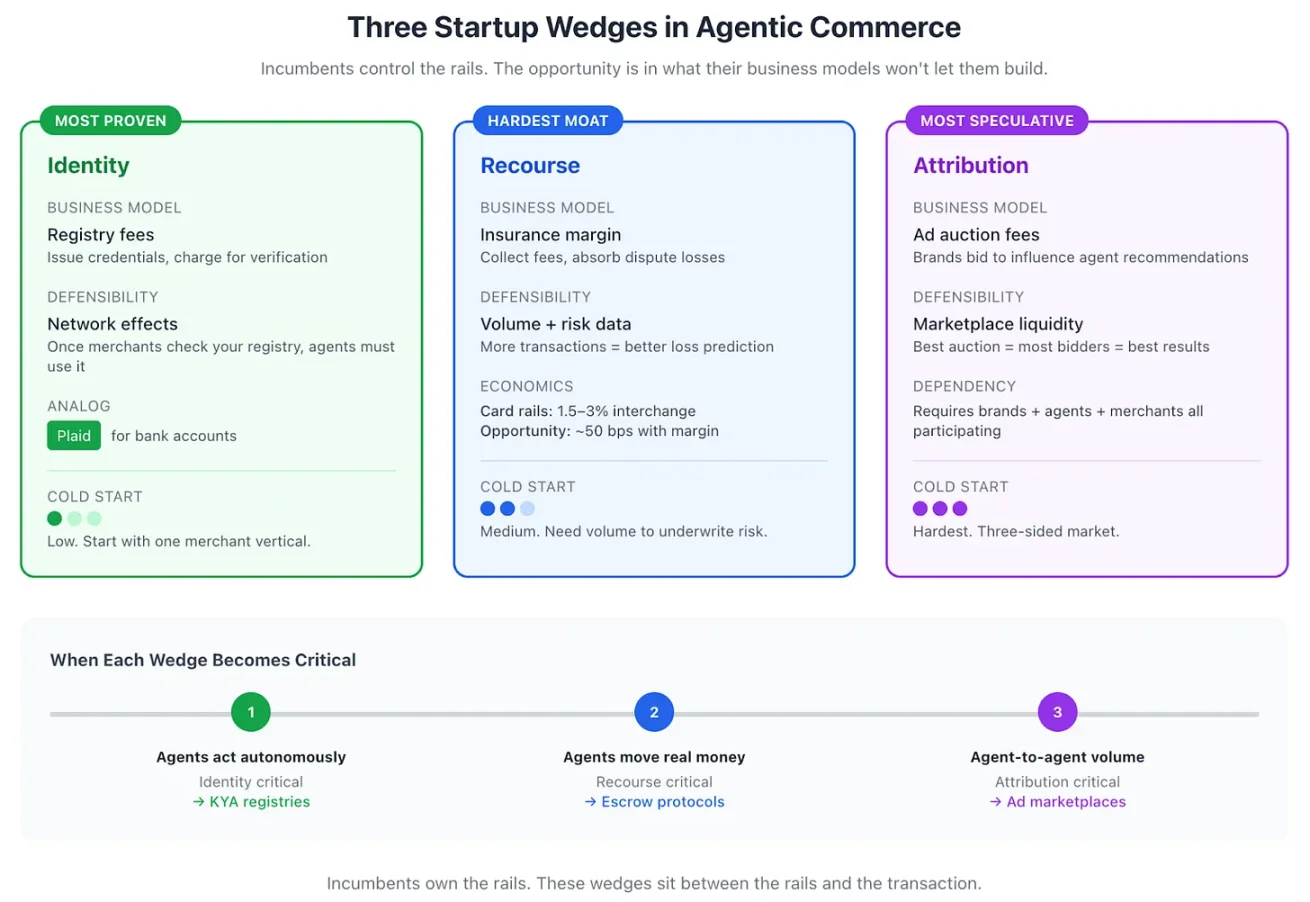

Three Entry Points for Startups

You can’t beat OpenAI on model quality or surpass Cloudflare on traffic. You must find parts of the tech stack that their business models (at least currently) prevent them from touching, yet still hold value. I see three entry points: identity, recourse, and attribution.

Agent identity is the most straightforward. The registration model is proven. While Plaid is a classic example—and fitting: they did identity verification for bank accounts. Startups can do the same for agents: issue credentials, accumulate reputation, and let merchants check reputation scores before accepting payments. Its moat comes from network effects: once enough merchants use your registry to verify, agents are forced to maintain good standing.

Recourse mechanisms are harder because they require assuming risk. Think of it as insurance: charge a small fee per transaction and cover losses when things go wrong. Scale is crucial. Card interchange fees range from 1.5%–3%, which includes dispute handling costs. Stablecoin channel costs are far below this, so a recourse layer could offer comparable protection at 0.5% and still profit.

Attribution mechanisms are the most forward-looking, but ultimately inevitable. When agents begin influencing purchasing decisions, brands will pay to shape recommendations. Auction mechanisms can be designed. But it suffers from a “cold start” problem—it requires participation from brands, agents, and merchants to form a functioning market, unlike the first two entry points.

The importance of these three entry points evolves with the stage of agent economy development:

-

Identity becomes critical when agents no longer require human approval for each transaction.

-

Recourse becomes essential when agents start handling real money.

-

Attribution will only activate when inter-agent transaction volume is large enough to sustain an advertising market.

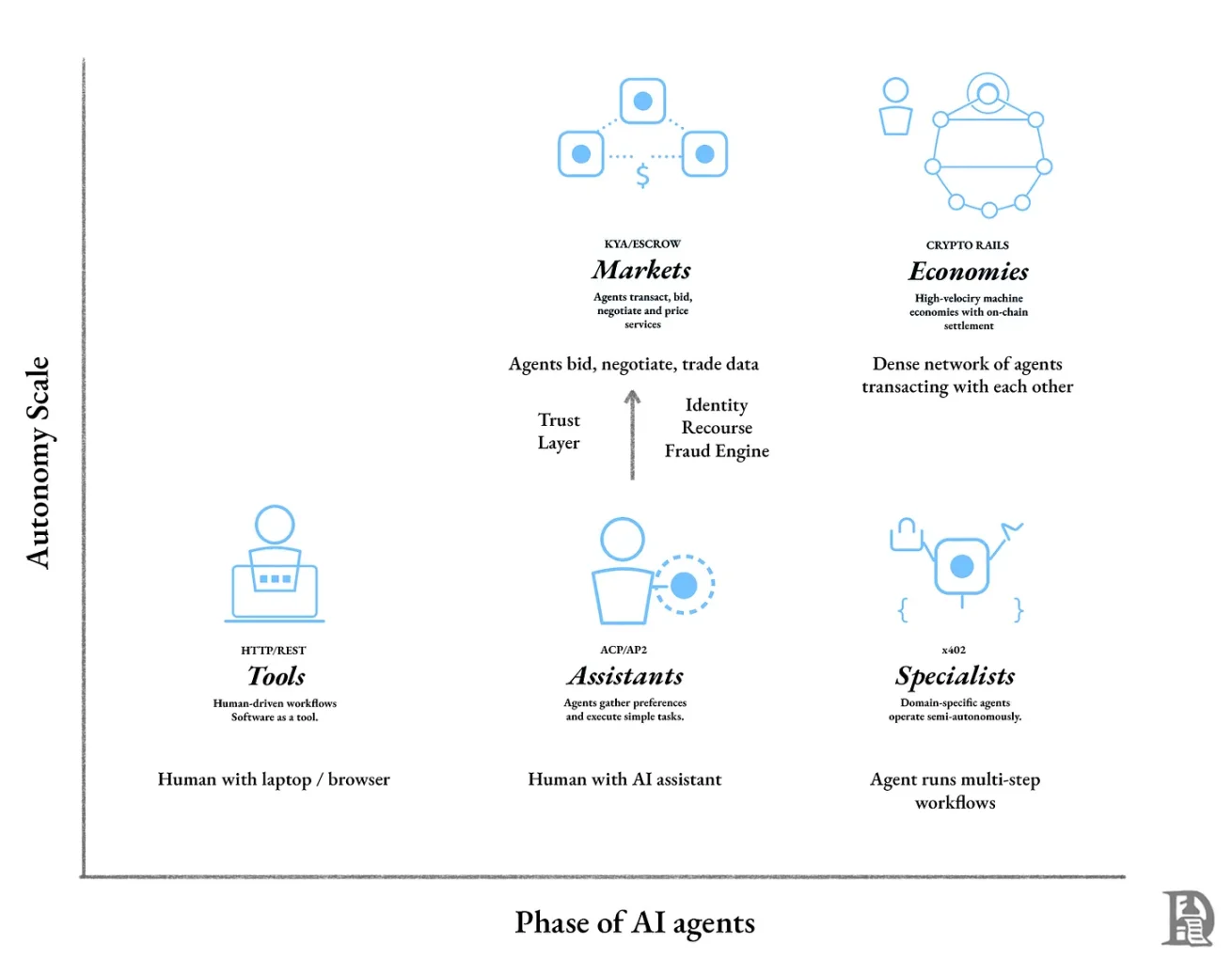

This leads to a practical development trajectory:

Source——Chart generated using Claude

Startups Will Build Parts of the Agent Economy Infrastructure

Agent development can be divided into three stages:

-

As an interface

-

Executing under human supervision

-

Autonomous transactions among agents

We are currently in the first stage. ChatGPT’s Etsy checkout integration is a good example: we browse products within a chat interface (though not exclusively), agents recommend options, but humans make the final decision. Trust is entirely borrowed from existing systems.

This stage belongs to existing giants, as it’s a battle for user access and distribution. Value accrues to players who control the interface where purchasing decisions are made.

The second stage is marked by agents gaining greater autonomy. Agents don’t just suggest itineraries—they book flights, rent cars, and reserve hotels directly. We set goals or constraints, agents execute, and we review the results.

At this point, trust layers become indispensable. Without recourse mechanisms, users won’t authorize agents; without identity verification, merchants won’t accept agent payments.

This is where startups have their opportunity. Existing giants may lack sufficient incentive to build trust infrastructure for stablecoin rails, as they still have massive growth potential in the current phase—which they dominate. OpenAI generated $13 billion in revenue this year. In comparison, Tether earned $10 billion in profit in just the first ten months of 2025, with full-year profits expected to be higher.

Identity, recourse, and attribution layers will be built by new companies focused on solving specific problems at the boundary between agent capability and user authorization.

The third stage is autonomous agent commerce. Your agent no longer seeks permission for daily decisions—it negotiates with other agents, bids for compute resources, participates in ad auctions, and continuously settles thousands of microtransactions. Stablecoins, due to their scalability, speed, and granularity required for machine-to-machine transactions, will become the default settlement layer.

Competition in this stage will no longer center on who has the best model or fastest blockchain, but on who builds the most trusted infrastructure: the agent’s “passport,” the “court” for resolving disputes, the “credit system” enabling overdrafts. These institutions serving software will determine which agents can participate in the economy and under what conditions.

Conclusion

We’ve laid the pipes for agents to “spend money,” but haven’t yet built the mechanisms to verify whether they “should spend.” HTTP 402 slept for thirty years, finally awakening as micropayments became viable. Technical problems have been solved. But the trust infrastructure underpinning human commerce—identity verification, fraud detection, dispute resolution—still lacks counterparts for agents. We’ve solved the easy part. Enabling agents to transact confidently with each other will take time.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News