Canada cancels fuel carbon tax, leaving crypto miners facing a new energy cost landscape

TechFlow Selected TechFlow Selected

Canada cancels fuel carbon tax, leaving crypto miners facing a new energy cost landscape

For crypto mining companies highly dependent on electricity, this marks the official start of a more complex cost博弈.

Author: TaxDAO

Introduction

On April 1, 2025, the Canadian federal government officially announced the cancellation of carbon taxes on fuel consumption—a move that sent shockwaves through energy-intensive sectors such as energy, manufacturing, and cryptocurrency mining. At first glance, this appears to be a tax relief measure for businesses, prompting widespread celebration over improved fiscal conditions. However, deeper analysis reveals that Canada has not relaxed its carbon constraints; instead, it has quietly tightened industrial-level controls, more precisely targeting large-scale emission facilities. For power-hungry crypto mining companies, this marks the official beginning of a far more complex cost博弈.

1 Policy Change: Cancellation of "Fuel Carbon Tax," But Carbon Pricing Remains Strong

To understand the real impact of this change, one must revisit the fundamental logic of Canada’s carbon pricing framework. Under the *Greenhouse Gas Pollution Pricing Act*, Canada's carbon tax system consists of two core components: the federal fuel charge (Fuel Charge) applied to end consumers and small businesses, and the Output-Based Pricing System (OBPS), which targets large industrial facilities. The latter was specifically designed to impose carbon costs while protecting energy-intensive industries from direct international competitive pressures.

The recent elimination of the fuel carbon tax only reduces tax pressure at the retail level. Meanwhile, industrial carbon prices—those with profound implications for major energy users like mining firms—continue to rise. According to federal plans, the price per tonne of carbon dioxide equivalent (CO₂e) will increase by CAD 15 annually from 2023 to 2030, reaching a final target of CAD 170 per tonne. Canada’s emissions reduction strategy remains unchanged; rising compliance costs under the carbon tax regime will inevitably be passed down through energy prices.

2 Rising Carbon Prices: Inflation for Energy-Intensive Industries

From an economic structure perspective, the true impact of industrial carbon pricing is not a blunt “emissions tax,” but rather an efficient transmission via electricity pricing chains. Notably, power generators do not pay for all their emissions. Under Canada’s dominant Output-Based Pricing System (OBPS), the government sets an emissions intensity benchmark, and power plants are only required to pay carbon costs on emissions exceeding this baseline.

In Ontario, for example, the industry benchmark for natural gas-fired generation is set at 310 t CO₂e/GWh, while average unit emissions stand around 390 t CO₂e/GWh. This means only the excess of 80 t/GWh is subject to carbon pricing. Yet even this surplus cost—when carbon prices reach CAD 95 per tonne—translates into approximately CAD 7.6 per MWh in additional expenses. If carbon prices climb to CAD 170 per tonne by 2030, this figure would rise to CAD 13.6/MWh. This mechanism then cascades downstream to mining, manufacturing, and especially high-power-consuming operations like Bitcoin mining.

It should be noted that the influence of carbon pricing is uneven across Canada, primarily depending on provincial power mix structures. In regions like Ontario or Alberta, where natural gas serves as the marginal (i.e., price-setting) power source, carbon costs are more easily incorporated into wholesale electricity prices. In contrast, in areas dominated by hydropower or nuclear energy, this transmission effect is significantly weaker. This directly leads to cost divergence for electricity-sensitive activities such as Bitcoin mining: in gas-powered markets, rising carbon prices almost equate to proportional increases in operating costs; in low-carbon electricity-rich regions, the impact is comparatively lower.

3 Dual Pressure on Miners: Rising Costs and Policy Uncertainty

For the electricity-dependent Bitcoin mining industry, Canada’s industrial carbon pricing system presents dual challenges that profoundly affect corporate operations and decision-making.

The first challenge is the direct increase in power generation costs due to rising carbon prices. Canadian mining firms commonly use Power Purchase Agreements (PPAs). As industrial carbon prices continue to rise, the “carbon price adjustment” clause in electricity contracts becomes increasingly significant, driving up per-unit computing power costs year after year. Neither market-linked floating-rate contracts nor seemingly stable long-term fixed-price agreements can permanently avoid this trend. The former quickly reflect rising costs, while the latter face higher carbon tax premiums upon renewal.

The second challenge stems from the complexity and uncertainty of the regulatory environment. Mining companies operating across Canadian provinces do not follow a uniform set of rules, but rather navigate a patchwork of divergent regulatory systems. For instance, certain jurisdictions (such as Alberta) temporarily maintain lower local industrial carbon prices to preserve industrial competitiveness, deviating from federal policy adjustments. While this approach reduces compliance burdens in the short term, it introduces significant policy risks. The federal government retains authority under the “equivalency principle” to assess provincial emission reduction efforts: if provincial measures are deemed insufficient, the stricter federal system may intervene. Such potential policy shifts mean that today’s “low-cost” investment decisions could require costly adjustments in the future. This uncertainty has become a critical factor that mining firms must incorporate into their Canadian expansion strategies.

4 Shifting Miner Strategies: From Cost Control to Compliance Planning

Faced with increasingly clear cost transmission pathways and a volatile policy landscape, the operational logic of Canada’s crypto mining sector is undergoing a profound transformation. Companies are shifting from passive electricity price takers to active compliance planners and energy structure designers.

First, structural changes are emerging in corporate energy procurement. One strategy involves signing long-term green power purchase agreements (Green PPAs) or directly investing in renewable energy projects. These moves are no longer solely about locking in predictable electricity rates—they aim to fundamentally decouple from existing price formation mechanisms driven by natural gas marginal pricing叠加 Canadian carbon costs. Under the OBPS framework, verifiable low-carbon power structures may also generate additional carbon credits for companies, transforming compliance expenditures into potential revenue streams.

Second, the regulatory disparities between provinces are giving rise to sophisticated arbitrage strategies exploiting policy differences. Take British Columbia (B.C.), for example: its OBPS accounting boundary focuses primarily on emissions within provincial borders. This design excludes imported electricity from out-of-province sources from carbon cost calculations. Mining firms can strategically structure their power procurement—for instance, using minimal local power while importing large volumes from other provinces—to circumvent high local carbon-powered electricity costs.

Additionally, the built-in incentive mechanisms of the OBPS system—where efficiency gains lead to reductions—are becoming new directions for corporate technological investments. This manifests on two levels: First, scale thresholds—facilities emitting below certain standards (e.g., 50,000 tonnes CO₂e annually) qualify for exemptions, prompting companies to consider total emissions during capacity planning. Second, performance benchmarks—under Alberta’s TIER system, industrial facilities generating power with emission intensities better than the government-defined “high-performance benchmark” can legally reduce or even eliminate their carbon costs—and in some cases, earn additional revenue by selling carbon credits.

These strategic shifts indicate that carbon compliance is no longer a simple financial deduction. As North America and Europe advance carbon border adjustment mechanisms (CBAM), Canada’s carbon pricing policies are evolving from domestic regulations into key cost determinants for international investment. Corporate compliance capability is rapidly becoming a core component of financial and strategic planning competitiveness.

5 From Strategy to Execution: Three Major Challenges in Enterprise Transformation

Based on the above analysis, the cancellation of fuel carbon tax in Canada reflects deeper policy recalibrations. Easing pressure at the fuel end while tightening control at the industrial end represents the federal government’s balancing act between emissions reduction goals and economic resilience. For high-energy-consuming industries like Bitcoin mining, this choice clearly points to three future trends:

-

First, energy costs will continue to rise—but there remains room for strategic planning;

-

Second, policy risks are increasing—but manageable through scientific site selection and compliance arrangements;

-

Third, green investments and carbon credit mechanisms will become new sources of profit.

However, a gap exists between recognizing these strategic opportunities and implementing them effectively. In practice, companies face three core challenges in moving from decision-making to execution:

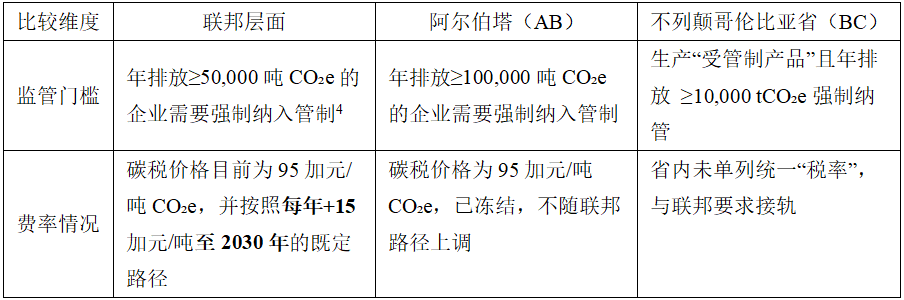

First, the “federal–provincial” two-tiered structure creates regulatory complexity, making it difficult for decision-makers to obtain accurate information. Although Canada has a federal carbon pricing benchmark, provinces are permitted to design and implement their own equivalent industrial pricing systems (such as OBPS or TIER). This results in not a single standard, but a situation of “one benchmark, multiple implementations.” Provinces differ significantly in defining exemption thresholds, setting emissions benchmarks for specific industries, establishing rules for carbon credit generation and usage, and calculating imported electricity. These localized implementation details prevent companies from applying a uniform national standard—one emissions-saving strategy proven effective in Province A may fail to yield reductions in Province B due to differing calculation methods, creating immense difficulty in formulating optimal strategies.

Table: Comparison of carbon tax rates at federal, Alberta (AB), and British Columbia (BC) levels

Second, traditional cost decision-making models are no longer fully applicable. Historically, miner site selection hinged primarily on immediate electricity prices (/kWh). Under the new rules, however, companies must shift toward risk-weighted assessments. Decision-makers now need to quantify elusive variables: what premium should be assigned to the hidden risk of policy reversal behind a region’s temporarily low carbon price? More complex still, investing in green energy (Trend 3) represents a substantial capital expenditure (CAPEX) decision, whereas paying carbon taxes is an ongoing operational expense (OPEX)—assessing the future financial impacts of these two choices exceeds the capabilities of traditional operations teams.

Third, the lack of a compliance system among execution teams hinders strategy implementation. Even if leadership devises a perfect strategy, execution faces major hurdles. The sole deliverable outcome of any strategy is the submission of compliance reports to regulators. This requires companies to build an integrated verification system spanning legal, financial, and engineering domains. For example, does the data scope of the MRV (Monitoring, Reporting, Verification) system meet tax audit requirements? Are the sources and attributes of cross-provincial electricity consistent across legal contracts and financial records? Without such systematic compliance capabilities, even the most sophisticated strategies cannot translate into real financial gains.

6 From "Tax-Paying" to "Adapting": Where Should Crypto Miners Go?

Currently, Canada’s carbon pricing policy is entering a more refined phase. It is no longer merely a tax collection tool, but a dual consideration of economic governance and industrial restructuring. Under this system, competition among energy-intensive enterprises depends not only on electricity costs, but also on depth of policy understanding, sophistication of financial modeling, and precision of compliance execution. For crypto mining firms, this represents both a challenge and an opportunity—those still relying on outdated single-cost models for site selection may suffer passively in future policy shifts; only those capable of integrating energy markets, tax policies, and compliance frameworks into systemic planning will truly possess cycle-resilient capabilities.

Yet, as previously analyzed, companies face three core obstacles in moving from strategic formulation to compliance execution: inadequate information inputs, lagging decision models, and deficient compliance systems. In this context, carbon tax planning, energy structure design, and policy risk assessment have become the new core logic of competition for mining firms. Therefore, transitioning from the past passive "tax-paying" business model to an active "adapting" strategic posture has become an unavoidable reality for miners.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News