Hyperliquid's Journey (Part 1): Pricing Liquidity

TechFlow Selected TechFlow Selected

Hyperliquid's Journey (Part 1): Pricing Liquidity

Do not hate your enemy, or it will cloud your judgment.

Author: Zuoye

A specter is haunting the blockchain—the specter of hyper liquidity. To carry out a holy crusade against this specter, every force within CEXs—offshore and onshore, Perp DEXs and fragments of FTX, Solana radicals and L2 newcomers—has united.

The U.S. dollar anchors liquidity; Hyperliquid has become synonymous with crypto liquidity. Trading is increasingly concentrated in major assets like BTC/ETH. People have either forgotten or deliberately ignored how Hyperliquid seized its moment to grow, quietly becoming a towering giant.

Everyone is talking about Hyperliquid flipping Binance, as if Aster's offensive marks only the beginning of a long campaign. Yet the 20x leverage cap imposed by Binance in 2021 did not end its rivalry with FTX, and today’s Aster 1001x won’t stop Hyperliquid either.

Mystery fuels allure. The Hyperliquid ecosystem is overly complex. This article focuses solely on how Hyperliquid survived the CEX encirclement and struck back. As for the lineage of HyperEVM and its DeFi ecosystem, the flywheel of $HYPE, the closed loop of $USDH, and capital maneuvers involving ETFs and DATs, those stories will be told in later installments.

The Price of Time

Do not hate your enemy—it clouds your judgment.

The history of finance is as old as the history of arbitrage.

From CoinDesk exposing FTX's secrets on November 2, 2022, to FTX filing for bankruptcy on November 11, the attacks focused on undermining the security of $FTT as FTX's reserve asset and exposing market maker Alameda for misappropriating FTX user funds. CZ first expressed willingness to acquire FTX, then withdrew, disrupting SBF’s fundraising efforts to save himself.

While raising funds in the Middle East, SBF explicitly voiced his resentment toward CZ. Emotion is the enemy of business, and ultimately SBF failed to save FTX.

In hindsight, whether it was prediction markets, AI investments, the Solana chain itself, the ongoing liquidation of FTX assets, or even coordination between perpetual exchanges and market makers—we can see that SBF’s vision was sound. It was just that the man himself proved unstable.

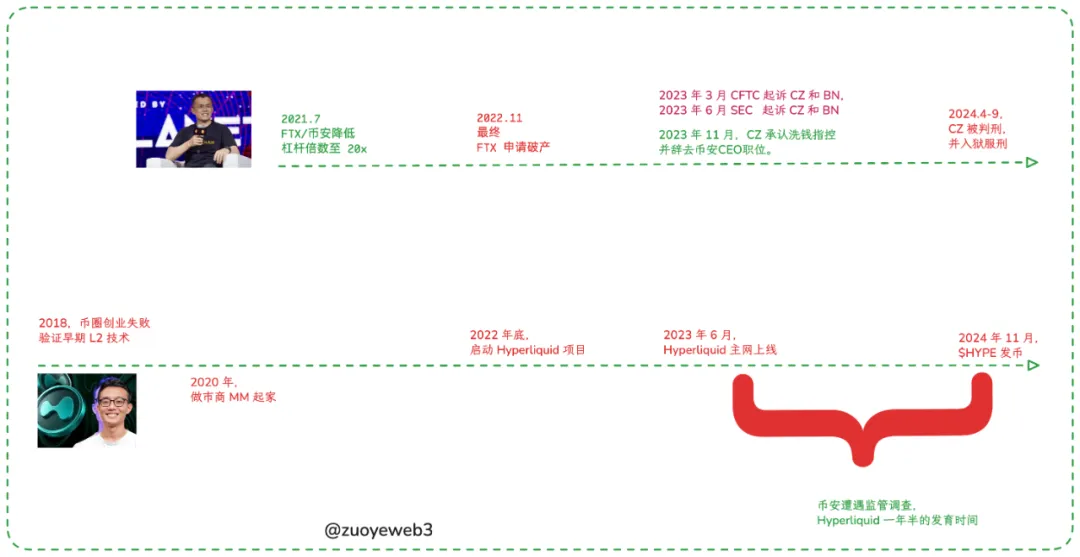

Caption: Early development timeline of Hyperliquid, Image source: @zuoyeweb3

After FTX collapsed, CZ began negotiating with the U.S. justice system over penalties. The price of getting on the train late was $4.2 billion. But unfortunately, even this high cost didn't secure Binance's dominance—Hyperliquid’s seed had already been planted.

The U.S. defines a challenger as any economy reaching around 60% of its own GDP—true of both the Soviet Union and Japan. Binance sets its threshold at 10%. Below this safety line, whether it's dYdX on-chain or centralized FTX, all are negotiable. Binance’s main site and ApolloX under the BNB ecosystem can jointly defend.

Hyperliquid grew almost in sync with Binance’s rhythm—from launch in June 2023 to token distribution in November 2024. Who remembers CZ publicly discussing Bio Protocol and teaching Giggle at exactly this time, dismissing Hyperliquid as just another token-driven Perp project?

Caption: Hyperliquid OI market share, Image source: @0xhypeflows

Unfortunately—or perhaps fortunately—for Hyperliquid, its growth flywheel didn’t stall after the epic 31% $HYPE airdrop. Instead, trading volume truly began to rise.

Counterintuitively, GMX also once saw explosive volume growth—volume in exchange for tokens, followed by token price and volume collapsing to zero after distribution. We can predict that Aster, Avantis, Lighter, Backpack, edgeX, StandX, Drift, and BULK will all follow this path. This does not mean they aren’t good projects, nor that their tokens shouldn’t be held.

We’re simply emphasizing that Hyperliquid surviving post-token launch is itself an anomaly—and it is precisely this abnormality that prompts us to examine whether it can endure across cycles and become a central axis in the crypto industry.

The rest of similar projects lose their appeal after launching tokens—Sushiswap can absorb Uniswap’s volume, GMX can absorb dYdX’s, Blur can absorb OpenSea’s.

Binance offshore exploits Coinbase onshore advantages; SBF used FTX to exploit Binance’s regulatory vulnerabilities; Hyperliquid exploits CEX inefficiencies.

Time windows are merely passively created—only active adaptation turns them into present success.

Centralization in BTC/ETH trading and the Meme craze mirror each other. Precisely because large capital and ETFs dominate mainstream coin prices, PumpFun could spark on-chain momentum. Desperate retail traders facing GameStop-style disconnections find no such restrictions in Memes.

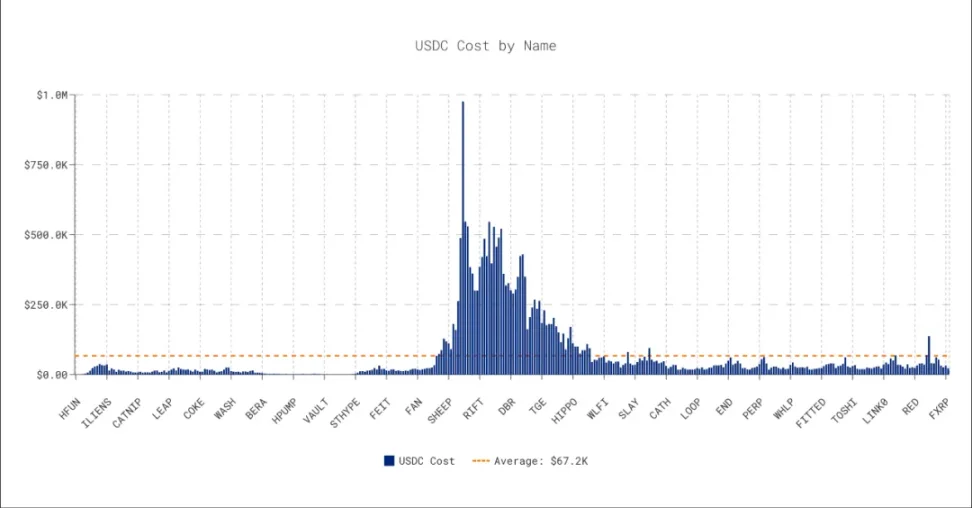

Mid-2024, Hyperliquid launched a Dutch auction model for listing tokens—an innovation beyond opaque CEX listing practices. More importantly, Hyperliquid gradually entered a dual-track mode, advancing both spot and derivatives trading.

However, apart from $GOD briefly touching $100,000 at the end of 2024, most auction bids remained low. Throughout 2024, nearly all listed tokens were “non-mainstream” Meme coins—far from rivaling Binance in BTC spot trading volume today.

Caption: Hyperliquid Dutch auction data, Image source: @asxn_r

More accurately, Hyperliquid began as a Perp DEX, emphasizing low latency, token incentives, and permissionless access through standard procedures. But by actively riding the Meme wave and introducing an auction mechanism, it genuinely penetrated spot trading and captured retail trader psychology, cultivating a complete trading ecosystem.

Tip: At the right moment, enter the current dominant ecosystem, position yourself as its synonym, use liquidity to drive traffic, empower $HYPE, and build a system.

$USDH follows the same path, as does the launch of HyperEVM. System thinking is Jeff, Hyperliquid’s founder, at his core. You’ll see this methodology reused across every stage of Hyperliquid’s development.

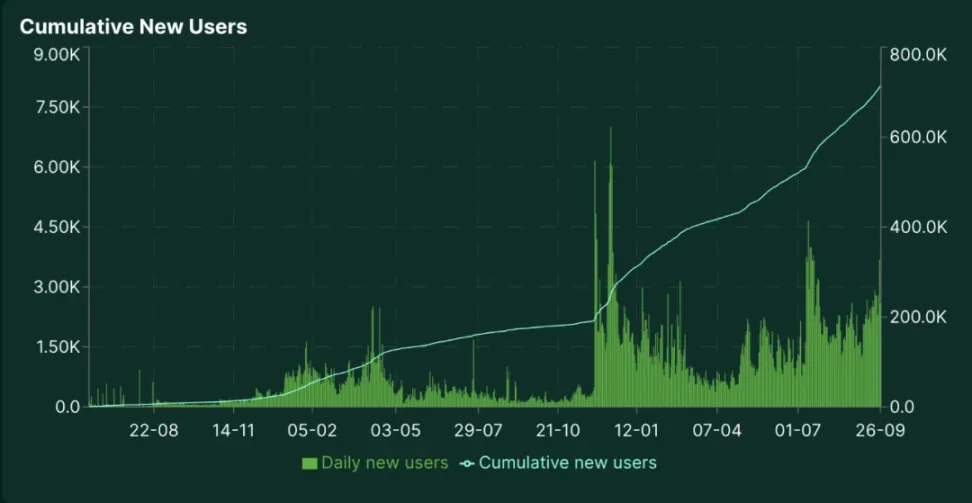

Caption: Hyperliquid user growth, Image source: @Hyperliquidx

From a visual perspective on user growth: During the October 2023 closed beta, Hyperliquid gathered its first 10,000 users. Then, during Season 1 (Nov 2023–May 2024), user count grew to 120,000.

Spot trading via Dutch auctions created a second small peak in April and May, and at the height of the Meme frenzy in late 2024, the rush to list $GOD brought $Solv into Hyperliquid’s spot market—the first mainstream BTCFi project token on the platform.

Of course, I cannot quantify the causal relationship between the spot market and Hyperliquid’s user and volume growth, but temporally, the two are highly correlated.

Hyperliquid did not gain market position simply through high leverage and No KYC. We must change our stereotypical view of Hyperliquid—right from the start, it was a full-service exchange, merely entering via Perp products.

The Price of Liquidity

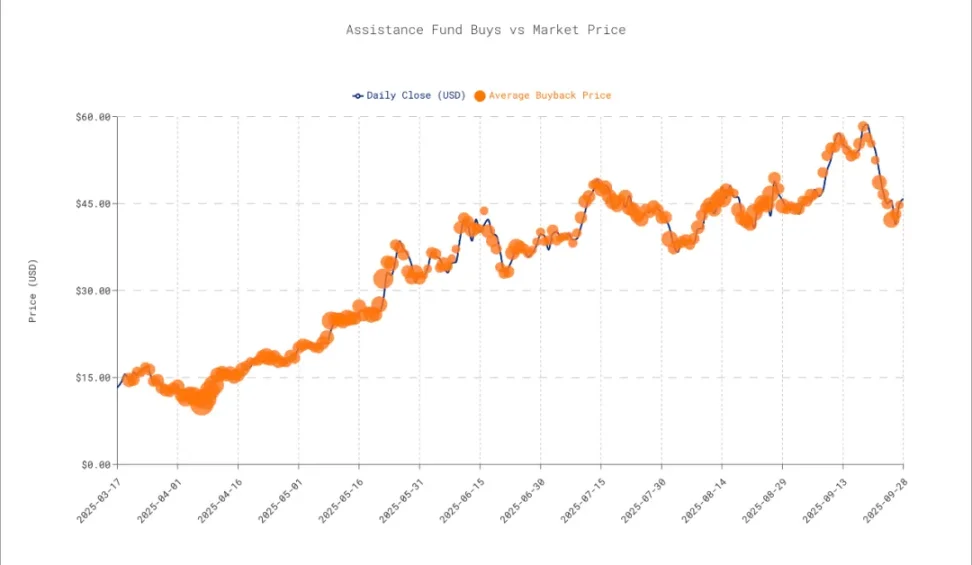

To date, Hyperliquid has spent $1.4 billion on buybacks.

After the $HYPE airdrop completed in November 2024, primary spot trading activity became internalized. However, a fork occurred here—Hyperliquid was no longer just a spot and derivatives exchange. HyperEVM had been under research and finally launched in early 2025.

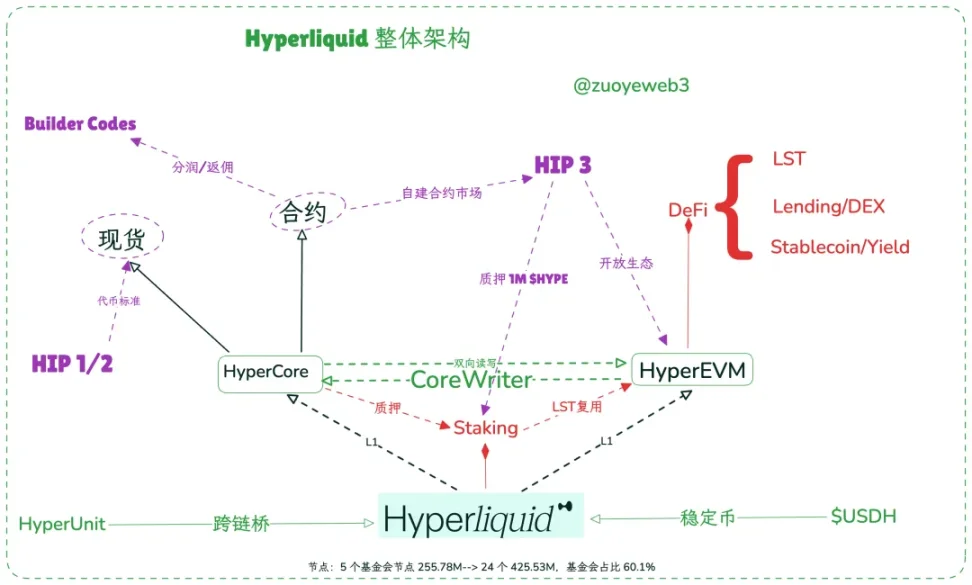

To categorize: Hyperliquid resembles an Ethereum with one consensus layer and two execution layers. HyperBFT serves as the consensus layer—nodes maintain HyperBFT consensus. HyperCore functions as the L1 for derivatives and spot trading, while HyperEVM is a permissionless open L1.

Caption: Hyperliquid overall architecture, Image source: @zuoyeweb3

Through the CoreWriter system, HyperEVM can invoke and allocate liquidity from HyperCore—LST protocols, for example, need no intermediary wrapping but can directly reuse native staking standards.

Beyond that, Unit Protocol bridges external ecosystem assets into Hyperliquid, while Builder Codes allow any frontend to utilize HyperCore liquidity and share in fee revenue—Rabby Wallet and Based App are examples of such frontends.

The earlier section described how Hyperliquid leveraged a passive time window and active moves to build two super-markets—spot and derivatives. But we haven’t yet addressed how it avoided liquidity fragmentation before and after $HYPE’s launch. Here is the full account:

First, reconstruct the appearance of Hyperliquid’s growth flywheel—the most rational path being:

-

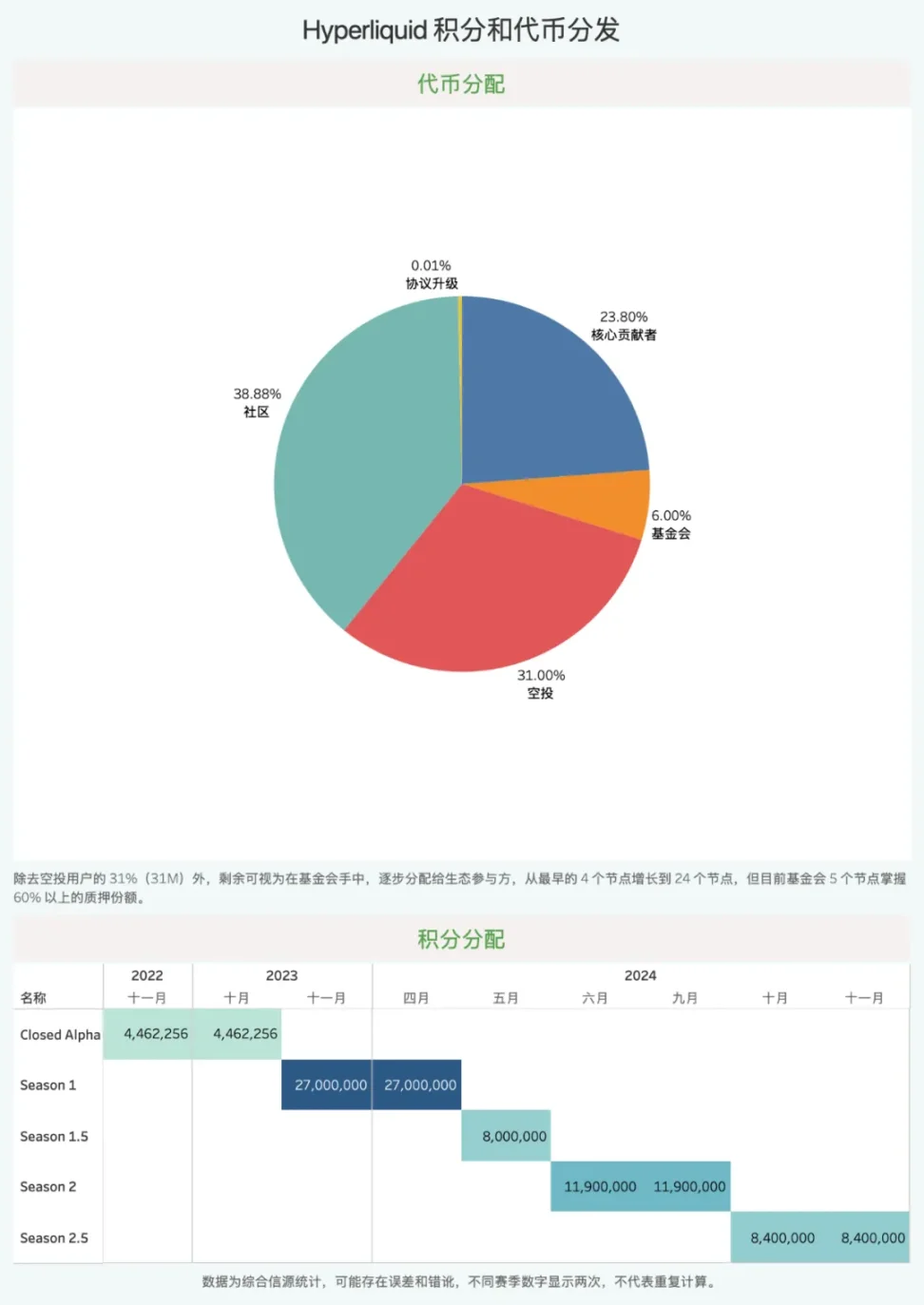

S1 and points system: In November 2024, after the token airdrop, 31% (31M) of tokens were distributed to S1 and Closed Alpha users, primarily based on users’ derivatives trading volume;

-

But note: ongoing activities hidden as S1.5 and S2.5 continued after the airdrop, giving the Hyperliquid team great flexibility through semi-hidden public campaigns;

-

Hyperliquid claims a team of 10 people, no VC backing, prioritizing community interests. Fees are roughly split equally between HLP (the liquidity treasury, responsible for liquidations) and $HYPE buybacks—this is also a key support for the token’s price.

Pre-airdrop: driven by points. Post-airdrop: driven by buybacks.

Caption: Hyperliquid points system, Image source: @zuoyeweb3

Hyperliquid resembles Solana’s founder Anatoly in valuing the token’s market price as a crucial indicator to sustain ecosystem vitality—a rare trait. Vitalik cares more about technology and ethical values, while VC-backed chains and major projects constantly face game-theoretic pressures from various parties dumping tokens.

In reality, it's hard to believe Hyperliquid had zero external funding. Initial market making requires proprietary or third-party capital to attract real retail and institutional users. Just look at how quickly Aster’s volume surpassed Hyperliquid’s to understand why.

Current Hyperliquid nodes include several known market makers—Infinite Field, Alphaticks, CMI, Flowdex, FalconX—and Galaxy has also joined as a node. Paradigm confirmed purchasing $HYPE in November 2024.

The most plausible guess: market makers participated early in Hyperliquid trading. But unlike traditional VC equity/token allocation models, they gradually acquired tokens from the foundation—fully consistent with the "no VC" narrative, since market makers aren’t VCs.

Warning: However, Hyperliquid’s data isn’t fully transparent—especially before November 2024.

For market makers, Hyperliquid’s strong buyback mechanism ensures longer-term gains, while Hyperliquid secures sustained liquidity support—breaking the trilemma of post-launch volume decline, falling token price, and eventual lack of node adoption.

According to @Mint_Ventures’ estimate, approximately $50 million flowed into the Assistance Fund (buyback fund) around the airdrop, plus $40 million allocated to HLP—treatable as market-making costs and overall marketing expenses respectively. VC and market maker roles remain blurred within these figures.

Beyond market makers, both HLP and the buyback mechanism contribute to price support. However, ultimate control over HLP rests with the Hyperliquid team. In the $JELLYJELLY incident, the team chose to use the HLP treasury to cover a $20 million bad debt. But in the $XPL hedging incident, users were left to bear the losses.

Good news: Arthur Hayes sold $5M, immediately followed by DragonFly buying $3M.

Institutions haven’t abandoned Hyperliquid. The only debate is: what is $HYPE actually worth?

The Price of Leverage

Extend the selling curve, slow down the pace of dumping.

Interest rate is the speed of money flow; price reflects differences in mutual valuation.

If we simply compare Hyperliquid’s income and expenses, revenue comes from spot listing fees (Dutch auction), spot trading fees, derivatives fees, liquidation fees, and Builder Codes revenue sharing. Expenses include buybacks and burns.

But it’s not that simple. Otherwise, $HYPE’s price would merely reflect trading volume—like $BNB at roughly 10%, i.e., $100. Yet currently it stands at only $40–50.

Caption: $HYPE buyback price, Image source: @asxn_r

Continuing from above, $HYPE buybacks contrast with the Ethereum Foundation selling at short-term highs—they don’t disrupt normal ecosystem development, nor do they rely solely on buybacks to inflate prices and create false prosperity. In contrast, when EF sells, you’d better run.

Three factors distort the $HYPE valuation framework:

-

High concentration: Most $HYPE spot and derivatives volume occurs on HyperCore, and the foundation controls most of the $HYPE staking and circulating supply;

-

Price-to-sales ratio (P/S): P/S is only valid in fully traded markets. Coinbase and Circle represent CEX and stablecoin valuations on U.S. markets, but $HYPE’s price can be manipulated under high concentration;

-

Institutional pricing: The participation of ETH, DAT, and the interweaving of staking systems and HyperEVM ecosystem are still maturing—$HYPE hasn’t yet achieved the cross-cycle market consensus enjoyed by $BNB.

Still, P/S gives us an illusion—false objectivity masked by numbers. Let’s do a rough P/S calculation to see how far $HYPE is from $1,000:

-

To date, Hyperliquid earned $730 million in 2025. Assuming $1 billion annual revenue is reasonable, with a $15 billion market cap, P/S is around 15.

-

Coinbase P/S is 11.8. Binance earns about $10 billion annually, with BNB valued at $136 billion—P/S around 13.6. Robinhood’s current P/S is 30—clearly too high—but just before its Cannes launch in June, it was exactly 11.4.

Rough estimates suggest that normal CEX/crypto brokerage P/S ratios on U.S. markets hover around 11—that is, token prices embed about 10x leverage, reflecting the market’s discounted expectation of 10x potential.

Yet Hyperliquid’s price is “operated” through multiple mechanisms. The only concern is Arthur Hayes’ belief that $HYPE buybacks can’t outpace selling pressure. He predicts 237.8 million $HYPE tokens will unlock on November 29, creating massive sell-side pressure that could crush $HYPE’s future—though he maintains his long-term forecast of 126x.

Facing the end of S2, the Hyperliquid team chose to empower NFTs rather than continue direct token airdrops—a move that channels traffic to HyperEVM without directly increasing $HYPE sell pressure.

$BNB reflects Binance’s unrivaled dominance in trading. Hyperliquid ruling only the Perp DEX space isn’t enough—it must defeat Binance to keep $HYPE elevated. Once market volatility intensifies or bears take over, today’s massive buying demand could reverse into overwhelming sell pressure. UST wasn’t Bitcoin, and $HYPE might not be $BNB either.

Either it becomes the next living Binance, or the next dead FTX.

Conclusion

Plant seeds of gentle wind, leave storms for future generations.

Hyperliquid hasn’t transcended its era—it seized a rare window of opportunity to deliver the strongest synergistic effect from market combinations. Much like early Midjourney, Hyperliquid brought Perps to retail markets, made DeFi OGs use chains daily, created a testing ground for institutions, and became a hunting ground for whales.

Unleash Memes, seize the moment to grow stronger.

After growing, Hyperliquid chose not to enter sell-off mode, instead striving to maintain $HYPE at a moderate price level. One must remember: it took Binance eight years to push $BNB to $1,000. With only three years for Hyperliquid and two for $HYPE, there’s still a long journey ahead.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News