Sol Strategies rings the "STKE" bell

TechFlow Selected TechFlow Selected

Sol Strategies rings the "STKE" bell

The relationship between Wall Street and Solana will become closer in the future.

Author: Prathik Desai

Translation: Block unicorn

September 9, 2024

Sol Strategies, still operating under its original name Cypherpunk Holdings and yet to rebrand, was trading on the Canadian Securities Exchange—a market typically reserved for small and micro-cap enterprises. Just months earlier, the company had hired Leah Wald, former CEO of Valkyrie, as its new chief executive. At the time, Cypherpunk was little known and attracted minimal investor attention.

Meanwhile, Upexi focused on promoting consumer goods for direct-selling brands, concentrating on areas like pet care and energy solutions on Amazon. In this crowded space, competition for clicks was fierce. DeFi Development Corp (DFDV), then still operating under its old name Janover, was preparing to launch a marketplace connecting real estate syndication organizers with investors. On the other hand, Sharps Technology operated in the highly niche business of manufacturing specialized syringes for healthcare providers—an obscure medtech sector with little investor interest.

These companies were modest in both size and ambition at the time. Their combined holdings of Solana (SOL) amounted to less than $50 million.

A year later, everything has changed dramatically.

Today, they proudly stand on Nasdaq—the world’s second-largest stock exchange—holding over 6 million SOL, worth up to $1.5 billion. This represents a 30-fold increase compared to the value of their Solana holdings just one year ago.

Last week, the bell ringing at Nasdaq in New York wasn’t the only symbolic event marking Sol Strategies’ listing on the exchange. A virtual bell also rang, signifying the same milestone: STKE officially began trading.

The company invited community members to participate in the ceremony by visiting stke.community and “ringing the bell” via a Solana transaction. This action will permanently record their participation in this historic moment. In many ways, this marks Sol Strategies’ “graduation”—a company that previously traded on the Canadian Securities Exchange (under the ticker “HODL”) and the OTCQB Venture Market (ticker “CYFRF”), a stock market for mid-sized companies.

I call it a “graduation” because entry into the Nasdaq Global Select Market is no easy feat. Known for its strict standards, this tier is typically reserved for blue-chip companies. By passing this test, Sol Strategies has gained what most crypto companies dream of but few achieve—legitimacy.

This is also why the listing of Sol Strategies matters, even though institutional investors seeking exposure to Solana on Wall Street already have options like Upexi and DeFi Development Corp.

Unlike Upexi and DeFi Development Corp—both of which were public before pivoting to become Solana asset managers, each now holding over 2 million SOL—Sol Strategies took the slow lane. It built out validator operations, secured institutional stakes such as ARK Invest’s 3.6 million SOL, passed SOC 2 audits, and strategically positioned itself for the Nasdaq Global Select Market—the top tier of the exchange.

While others merely hold SOL, Sol Strategies actively operates the infrastructure supporting it, turning these holdings into a viable business.

I dove deep into Sol Strategies’ balance sheet to uncover the story behind the numbers.

For the quarter ending June 30, Sol Strategies reported revenue of 2.53 million Canadian dollars (approximately $1.83 million USD). While this figure may seem unremarkable at first glance, the real story lies in the details. This revenue came entirely from staking approximately 400,000 SOL and operating validators that secure the Solana network—not from selling traditional products. Upexi has been weighed down by its non-crypto secondhand commerce business, while DFDV relies heavily on continuous fundraising for growth, with 40% of its revenue still coming from its non-crypto real estate operations.

By offering validator-as-a-service, Sol Strategies has created a new revenue stream from its Solana asset management business. This model generates recurring income without the burden of mounting debt or traditional overhead costs.

Sol Strategies stakes SOL on behalf of institutional clients, including the 3.6 million SOL delegation received in July from Cathie Wood’s ARK Invest. Commissions from these delegations generate a steady revenue stream. Call it yield, call it fees—but from an accounting standpoint, it’s revenue, something many crypto asset managers cannot claim.

Solana validators typically charge around 5%-7% commission on staking rewards. With base staking yields hovering around 7%, this creates an annual nominal value of roughly 0.35%-0.5% for the delegated tokens. On 3.6 million SOL—worth over $850 million at current prices—this translates to over $3 million in annualized fee revenue, not including any price appreciation or yield on Sol Strategies’ own capital. This is effectively additional income, exceeding half of the staking rewards generated from its own 400,000 SOL holdings—all created from other people’s funds.

However, Sol Strategies reported a net loss of 8.2 million Canadian dollars (approximately $5.9 million USD) in Q3. But if you exclude one-time expenses such as amortization of acquired validator intellectual property, share-based compensation, and listing costs, the core operations generated positive cash flow.

What truly sets Sol Strategies apart from competitors is its view of Solana. For the company, the product isn’t just the Solana token—it’s the entire Solana ecosystem. This unique perspective is both innovative and strategic, distinguishing Sol Strategies within the field.

The more delegators Sol Strategies attracts, the more secure the network becomes. As its validators gain a reputation for reliability, this draws in even more delegations. Every user who directs their stake to a Sol Strategies node is both a customer and a co-creator of its revenue, transforming community engagement into a measurable driver of shareholder value. This approach makes every participant feel invested in the company’s success.

This is likely the most important factor giving Sol Strategies an edge over peers who hold even larger amounts of Solana.

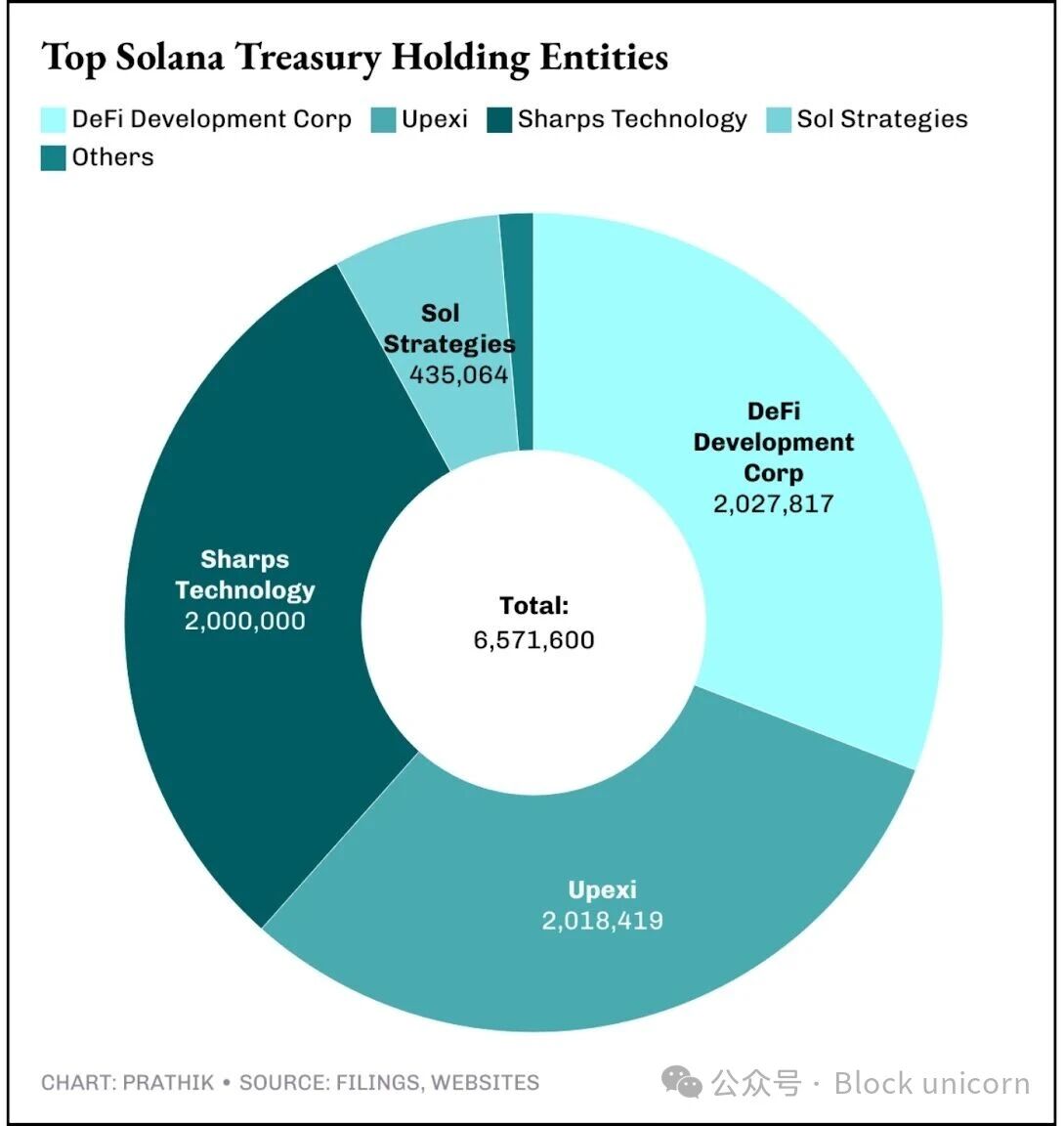

Currently, at least seven publicly traded companies control 6.5 million SOL, worth approximately $1.56 billion—about 1.2% of the total supply.

In the race for Solana asset management, each company is vying to become the preferred proxy through which investors gain exposure to Solana. Each has a slightly different strategy: Upexi acquires SOL at a discount, DFDV bets on global expansion, while Sol Strategies focuses on diversified asset reserves. The goal is the same: accumulate SOL, stake it, and sell packaged products to Wall Street.

The path from Bitcoin to Wall Street was paved by companies like MicroStrategy, which transformed from a software business into a leveraged BTC asset manager, culminating in the highly successful spot ETF. Ethereum followed a similar trajectory through companies like BitMine Immersion, Joe Lubin’s SharpLink Technologies, and more recently, spot ETFs. For Solana, I expect adoption will primarily be driven by operational companies within the network. These firms don’t just hold assets—they operate validators, earn fees and staking rewards, and report quarterly earnings. This model is closer to active management than to an ETF.

It is precisely this combination of growing net asset value and real cash flows that will likely convince investors to back this approach. If Sol Strategies succeeds, it could become the BlackRock of Solana.

The relationship between Wall Street and Solana will grow even tighter in the future.

Sol Strategies is already exploring the possibility of tokenizing its own shares on-chain. Imagine STKE stock existing not just on Nasdaq, but also as a Solana-based token tradable in DeFi pools and instantly settled with USDC. A stock listed on Nasdaq also trading on-chain would be a bridge that ETFs cannot cross. This remains speculative for now, but it signals a move toward erasing the boundary between public equity and crypto assets.

Still, it won’t be easy. “Graduating” to Nasdaq brings new challenges and greater responsibilities for Sol Strategies.

Poor validator performance or missed governance steps could trigger immediate investor backlash. Sol Strategies’ decision to bet on the Solana ecosystem—not just the Solana token—may bring higher risks and commensurate rewards. Solana itself faces network outages and competition from emerging blockchains. If stock investors perceive the share price as trading significantly below net asset value, arbitrageurs might sell off regardless of fundamentals.

Nonetheless, I believe Sol Strategies’ Nasdaq listing represents Solana’s best chance to take a front-row seat on Wall Street. Can you package on-chain assets into structured investment products and integrate them into Nasdaq? Sol Strategies now carries this formidable responsibility.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News