Gray Giant vs Whitelisted Players: The "Forking Moment" Brought by Transparent and Compliant Stablecoins

TechFlow Selected TechFlow Selected

Gray Giant vs Whitelisted Players: The "Forking Moment" Brought by Transparent and Compliant Stablecoins

USDT is a "gray monster" that has organically emerged from the market, while compliant stablecoins represent TradFi's biggest alpha source this year.

Author: imToken

From a macro perspective, stablecoins are entering an unprecedented reshuffling phase.

In July, U.S. President Trump officially signed the GENIUS Act, marking the落地 of stablecoin legislation; in August, Hong Kong's Stablecoin Ordinance also took effect, becoming the first regional regulatory framework globally; meanwhile, major economies such as Japan and South Korea are accelerating the follow-up of regulatory details, planning to allow compliant entities to issue stablecoins.

In other words, the stablecoin sector has entered a true "regulatory window period"—evolving from gray-market liquidity tools into financial infrastructure that balances compliance with experimentation.

Why focus on "regulated stablecoins"?

Within the classification system of stablecoins, regulated stablecoins occupy a unique and critical position.

First, from a market demand perspective, stablecoins have long ceased to be just the "common equivalent" for on-chain transactions. For crypto-native users, they are core assets for risk hedging and liquidity; for traditional institutions, they could become entirely new tools for cross-border settlement, treasury management, and payment clearing.

However, past stablecoins like USDT expanded naturally based on market demand. Despite their large scale, they have long operated in regulatory gray zones, frequently criticized for lack of transparency and compliance risks. In contrast, regulated stablecoins prioritize "compliance and usability" from inception—issued by regulated entities, meeting licensing requirements in their respective jurisdictions, and backed by clear asset reserves and legal accountability.

To put it simply, the defining feature of regulated stablecoins lies in regulated issuers + compliance with jurisdictional licensing requirements. Behind every token are clearly defined asset reserves and legal responsibilities, allowing users and institutions to trace both the regulatory authority and asset custody arrangements when using them.

This enables them not only to circulate on-chain but also to potentially appear in corporate financial statements and compliance reports, serving as an "official channel" between traditional finance and the crypto world.

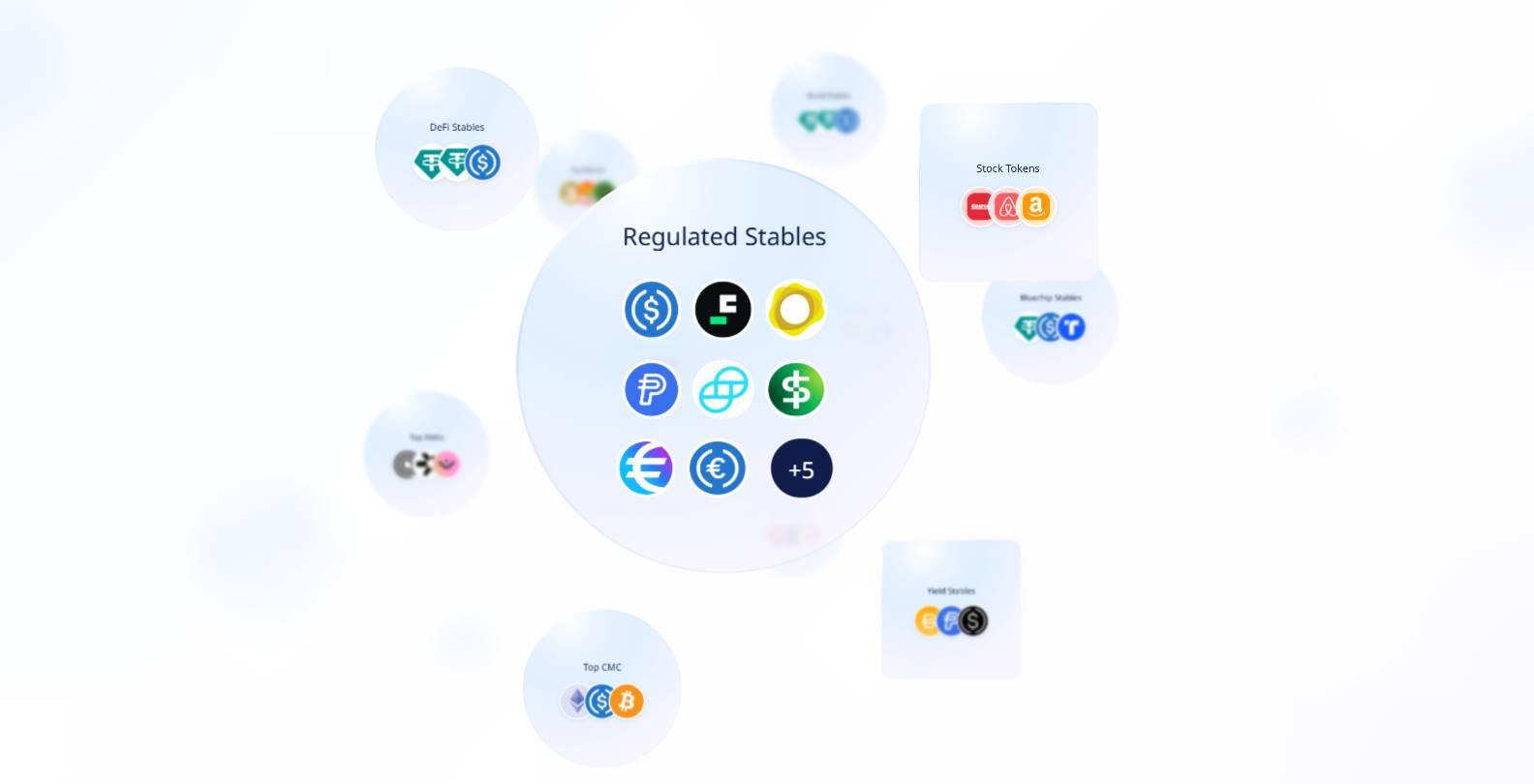

Source: Regulated stablecoins from imToken Web (web.token.im)

From imToken’s perspective, stablecoins can no longer be summarized by a single narrative but instead represent a multidimensional "asset aggregate"—different users and needs correspond to different stablecoin choices (Further reading: Stablecoin Worldview: How to Build a Stablecoin Classification Framework from a User Perspective?).

Within this classification, regulated stablecoins (such as USDC, FDUSD, PYUSD, GUSD, USD1, etc.) do not aim to replace USDT, but rather function as a parallel track, offering legal and secure options for cross-border payments, institutional applications, and financial compliance.

If USDT's significance lies in "driving global liquidity in the crypto market," then the significance of regulated stablecoins lies in 'bringing stablecoins into the everyday realities of finance and life.'

Global Landscape of Major Regulated Stablecoins

From this vantage point, the global paths of regulated stablecoins vary, yet converge toward the same destination—they are transitioning from gray-market liquidity to compliant financial interfaces. Their future applications may extend beyond exchange matching and arbitrage, reaching into cross-border payments, corporate treasury management, and even personal daily transactions.

Globally, several distinct development paths for regulated stablecoins have already emerged.

In the United States, USDC is the most representative regulated stablecoin. Issued by Circle, it is backed by cash and high-liquidity short-term U.S. Treasuries and undergoes regular audits to ensure 1:1 dollar redemption, making it the most widely adopted dollar stablecoin among institutions and one of the few stablecoins eligible for inclusion in financial statements.

Running parallel is USDP, issued by Paxos Trust Company and holding a trust charter from the New York Department of Financial Services. Though less prevalent in circulation than USDC, its compliance attributes are clear, primarily targeting institutional payment and clearing use cases.

Meanwhile, PayPal's PYUSD carries greater symbolic weight—it was not created for trading markets but aims directly at retail payments, attempting to bring stablecoins into everyday consumer spending and cross-border transfers.

In Hong Kong, the Stablecoin Ordinance, effective August 2025, makes it the first region globally to establish a comprehensive regulatory framework for stablecoin issuance, reserves, and custody. This means stablecoins issued in Hong Kong are no longer tokens operating in gray areas but are now recognized financial tools under financial regulation. First Digital's FDUSD is emblematic of this shift.

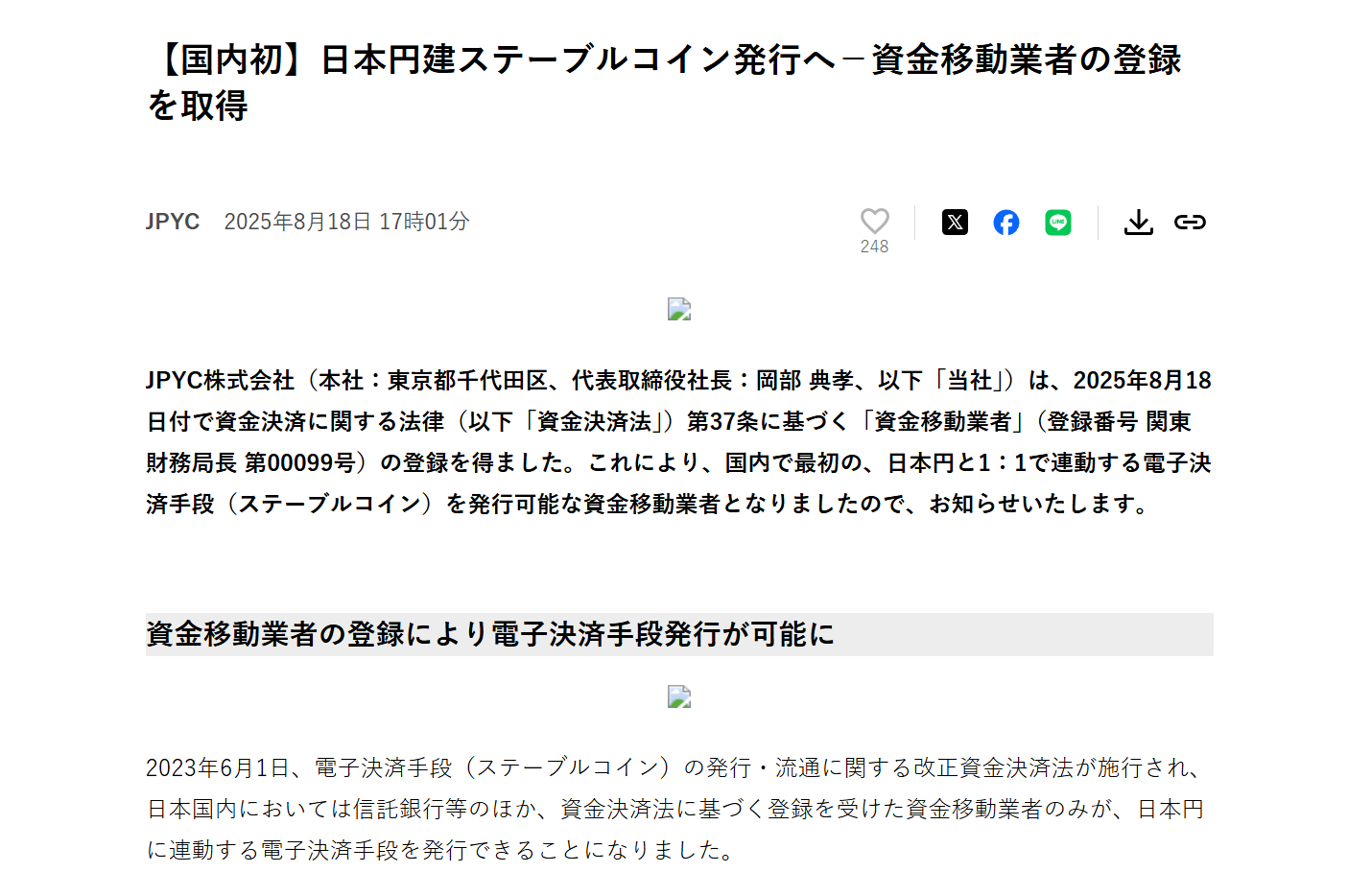

In Japan, JPYC has become the first approved yen-denominated stablecoin, issued by JPYC Inc. and regulated under the Funds Transfer Service Provider license. It will be backed by liquid assets such as government bonds. The Japanese Financial Services Agency (FSA) plans to approve it as early as this fall. The issuer has already completed registration as a money transfer operator and intends to deploy its yen stablecoin across Ethereum, Avalanche, and Polygon networks.

South Korea follows a similar path, currently exploring won-denominated stablecoin applications through a "regulatory sandbox," focusing on cross-border payments and B2B settlements.

These initiatives collectively point to one trend: regulated stablecoins are not aiming to challenge the market positions of USDT or USDC, but are carving out a separate lane to serve real-world scenarios that require compliance and transparency. Their emergence signifies that the stablecoin narrative is shifting from "gray-market liquidity for trading platforms" to "legitimate interface for global finance."

While their paths differ, their directions are highly aligned: regulated stablecoins are becoming a parallel track to USDT. Their significance does not lie in competing for liquidity dominance, but in providing legal, transparent, and supervisable alternatives for financial institutions, cross-border payments, and everyday applications.

What's Next?

Overall, the most significant structural change in TradFi in 2025 is the full-scale arrival of regulated stablecoins, with the competitive focus shifting from scale and traffic toward compliance capability and real-world penetration.

Whether it's Hong Kong's pioneering Stablecoin Ordinance or the strengthened regulation of USDC, PYUSD, and others in the U.S. market, the message is consistent: stablecoins capable of truly serving global users and traditional capital must achieve deep integration between off-chain compliance and on-chain architecture.

This also means the logic of competition among stablecoins has shifted—from the past question of "who holds more dollar reserves" to "who can enter real user scenarios faster," including cross-border settlement, corporate treasuries, retail payments, and daily consumption. Under this trend, new compliant initiatives continue to emerge.

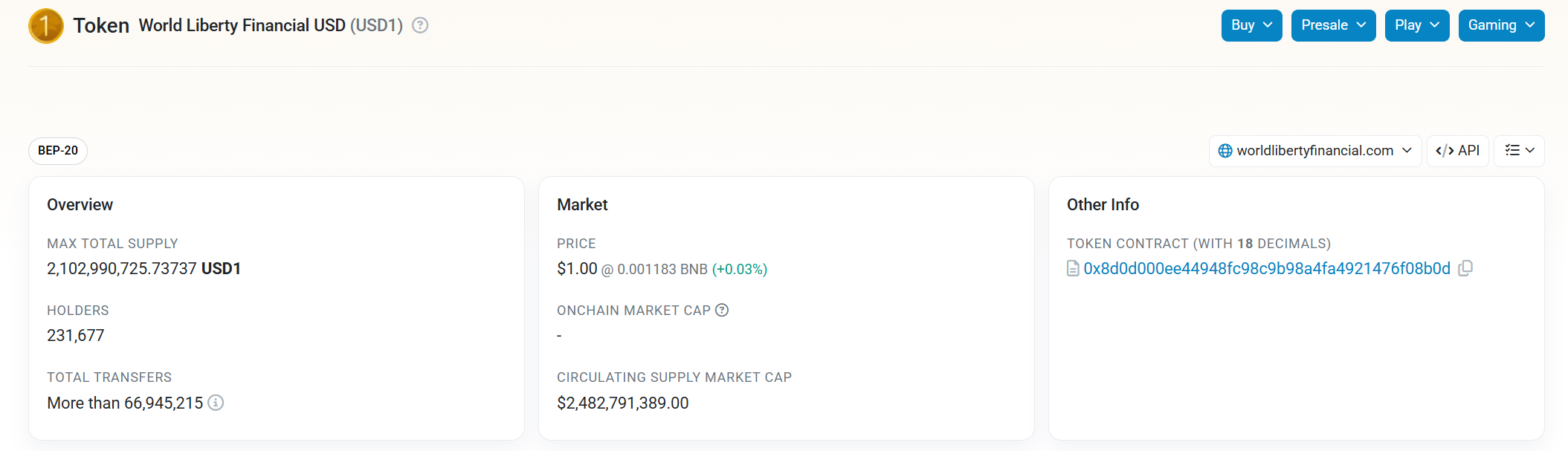

For example, emerging stablecoin projects like USD1 emphasize compliance pathways and integration with global use cases from day one, leveraging strong traditional capital and policy resources. Backed politically by the Trump family, USD1 achieved a near-phenomenal "zero-to-one" growth and top exchange coverage within just six months of launch:

Since March, its issuance has surged to $2.1 billion, surpassing FDUSD and PYUSD to rank as the fifth-largest stablecoin globally (per CoinMarketCap data), and it has rapidly gained listings on leading CEXs such as HTX, Bitget, and Binance. In comparison, PYUSD, backed by PayPal for two years, continues to struggle with adoption.

At the same time, infrastructure around Liquidity-as-a-Service (LaaS) is emerging, aiming to transform stablecoins from mere on-chain token symbols into globally accessible settlement APIs.

This gives rise to a foreseeable future scenario: cross-border payments, corporate treasuries, and even personal daily transactions may gradually find a new equilibrium between USDT's gray liquidity and the whitelisted systems of regulated stablecoins.

From a broader perspective, stablecoins are undergoing a "fork." The future landscape will inevitably be multipolar and parallel:

-

USDT continues as the liquidity engine of the global crypto market;

-

Yield-bearing stablecoins meet demands for capital appreciation;

-

Non-dollar stablecoins open up multipolar narratives;

-

Regulated stablecoins progressively embed into the real-world financial system;

Over the past decade, USDT represented the gray force of "organic growth," driving global liquidity in the crypto market; semi-compliant products like USDC built transitional bridges between gray and white. Now, with the implementation of the U.S. GENIUS Act, Hong Kong's Stablecoin Ordinance taking effect, and Japan and South Korea successively approving pilot programs, regulated stablecoins are entering their true window of opportunity.

This time, stablecoins will no longer be merely tools for on-chain users, but will become ubiquitous financial instruments in cross-border settlements, corporate treasuries, and even daily consumption.

This is the meaning of regulated stablecoins: enabling stablecoins to truly step out of the crypto world and into the daily fabric of finance and life.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News