New changes in crypto power structures: Anchorage's Iron Vault

TechFlow Selected TechFlow Selected

New changes in crypto power structures: Anchorage's Iron Vault

Custody Encryption: Anchorage's Iron Vault, the Iron Throne of Starship Troopers

More than a decade into the crypto craze, the wealth-creation era driven by Bitcoin's four-year halving cycle has ended, replaced by intermittent liquidity injections from U.S. stocks, the dollar, and Treasuries. Discrete hotspots now string together each cycle—much like Pendle’s journey from fixed income and LST to BTCFi, then Ethena and Boros.

Becoming new money is harder than managing old money.

As custodians say: whoever has the money, we earn from them.

In crypto, only three types of people truly have money: individual whales (early BTC miners, early ETH investors, DeFi Summer OGs), on-chain institutions (crypto-native VCs, CEXs and public chains, a few project teams), and Wall Street-backed new and old giants.

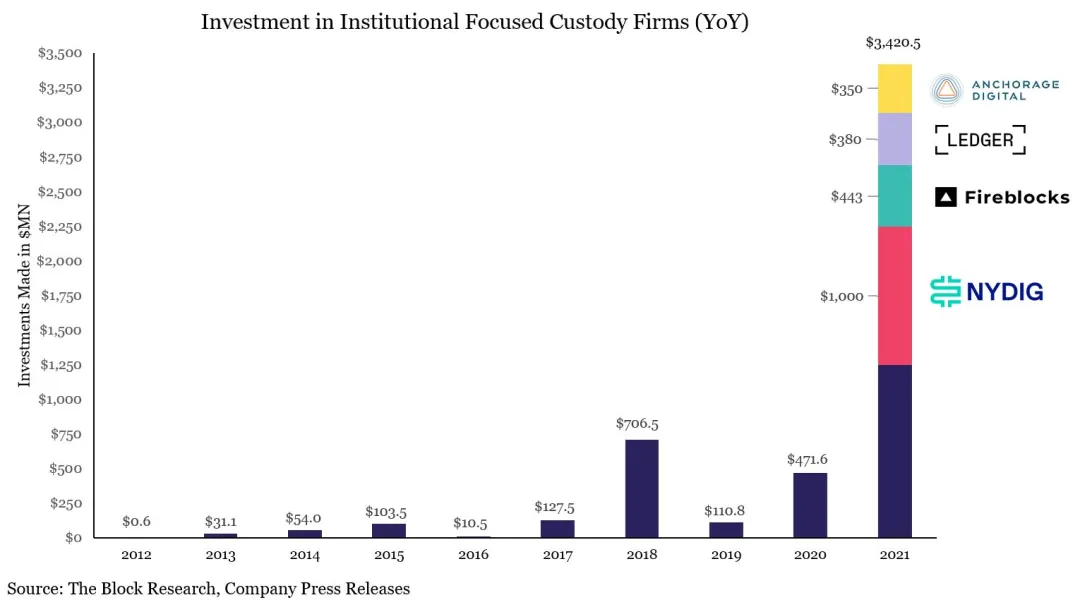

Custodians have since diverged. After a $3 billion financing in 2021, and the FTX-Celsius, 3AC-Luna-UST blowups in 2022, the basic格局 of the crypto custody赛道was established, for example:

-

• Serving on-chain projects: Copper/Ceffu/Cobo

-

• Serving ETFs: Coinbase

-

• Bank-grade: BNY (Bank of New York Mellon)

-

• Exchange-based: Fireblocks

Especially Coinbase, which has captured nearly all ETF custody份额, with over 80% of BTC and ETH ETF issuers choosing to partner with it. In treasury strategies, MSTR also prefers Coinbase for BTC custody.

The era of retail trading ends; the era of institutional wealth management begins

Ways to make money in crypto evolve with the times. Under economies of scale, whoever holds the most capital captures the most profit—from miners, exchanges, market makers, next will come custodians. Especially as traditional finance capital moves on-chain, it won’t go directly to public chains or exchanges, but through custodians as intermediaries.

Ethereum’s daily transaction volume has surpassed the peak of DeFi Summer, reaching 1.74 million transactions. But this cycle’s growth isn't driven by memes or trading activity—it's fueled by stablecoin circular lending ignited by Aave and Ethena.

Similarly, Aave and Plasma are collaborating to bring stablecoins on-chain for traditional finance. Under Genius Act restrictions, payment-oriented stablecoins cannot pay interest to users. Once funds settle on-chain, they become dead weight for issuers.

On the other hand, as overall CEX trading volumes continue to shrink, developing non-trading services such as custody, staking, and yield generation will become a new business model targeted by traditional financial institutions (TradFi). Especially under rate-cut expectations, channeling liquid assets represented by 401(k) and treasury strategies safely onto the blockchain will become a new entrepreneurial frontier.

The exchange cycle is nearing its end, squeezed by on-chain migration and IPOs. Hyperliquid shows signs of flipping Binance, while Kraken, Bullish, and others challenge Coinbase’s status as the sole listed exchange.

Strategically, everyone is eyeing post-CEX yield dividends. For large pools of legacy capital, APR can be lower, but principal safety is paramount. Tether built a physical gold vault for its own gold reserves—digital vaults on-chain are also a promising business.

Under ETF dominance, it's hard to shake Coinbase’s supremacy. Yet every generation has its champion, and the new market landscape offers fresh opportunities for second- and third-tier players.

Compared to the massive wealth flows of the dollar, U.S. Treasuries, and equities, current on-chain adoption is still like catching water with a basin. Only sufficiently secure large-scale "bathtubs" will allow seamless liquidity flow.

Thus, established players are fragmenting. Anchorage Digital and Galaxy Digital are undoubtedly two most representative examples.

-

• Treasury services (DATCO): Galaxy

-

• Stablecoins: Anchorage

-

• Emerging ETF staking: Anchorage Digital & Galaxy Digital

Beyond BTC and ETF spot ETFs, both Digitals share the same goal: capturing more market share from Coinbase. We begin with this commonality.

In today’s spot ETF market, two fundamental trends exist. First, generalization—altcoins and meme coins beyond BTC and ETH may transition directly into ETFs after meeting Coinbase derivatives listing requirements for six months. Second, approval of staking-enabled ETFs, allowing ETF issuers to redeem in-kind and opening interfaces to on-chain staking services.

For instance, Anchorage Digital became the exclusive custodian and staking partner for REX-Osprey’s Solana staking ETF—perfectly aligning with both trends. If the bull market continues, more ETF products will become focal points for Digital’s custody expansion.

In traditional ETFs, Anchorage also secured partnerships with 21Shares and BlackRock. More remarkably, it became the custodian for Trump Media Group’s Bitcoin treasury—proving that cats have their paths, and Anchorage’s northern winds have reached Mar-a-Lago.

Anchorage’s Licensed Bank Strategy in Stablecoins and the Dream of a Crypto Iron Vault

2019: Attempted collaboration with Visa, eventually becoming Visa’s USDC settlement agent bank in 2021.

2021: Launched crypto custody business, valued at $3 billion, became an OCC-licensed crypto bank, and digital asset custodian for the U.S. Marshals Service (USMS).

2022: Amid the crypto crash, became preferred custodian for Aptos; Anchorage co-founder Diogo Mónica is also an Aptos investor.

2023: Q1 platform assets grew 80%, yet laid off 75 employees (20% of staff), and called for stablecoin regulation.

2024: Co-founder Diogo Mónica stepped back from core operations; Nathan McCauley took full control.

2025: Anchorage Digital to custody Trump Media’s Bitcoin treasury; acquired Mountain Protocol, issuer of USDM.

Let’s formally introduce Anchorage Digital, founded in 2017 by Nathan McCauley and Diogo Mónica. Initially just a small local trust company in South Dakota, a stroke of luck in 2021 transformed Anchorage Digital into the only institution ever granted a crypto bank charter by the OCC (U.S. Office of the Comptroller of the Currency).

In Silicon Valley, on Wall Street, or in Washington—exclusive financial services ultimately come down to relationships.

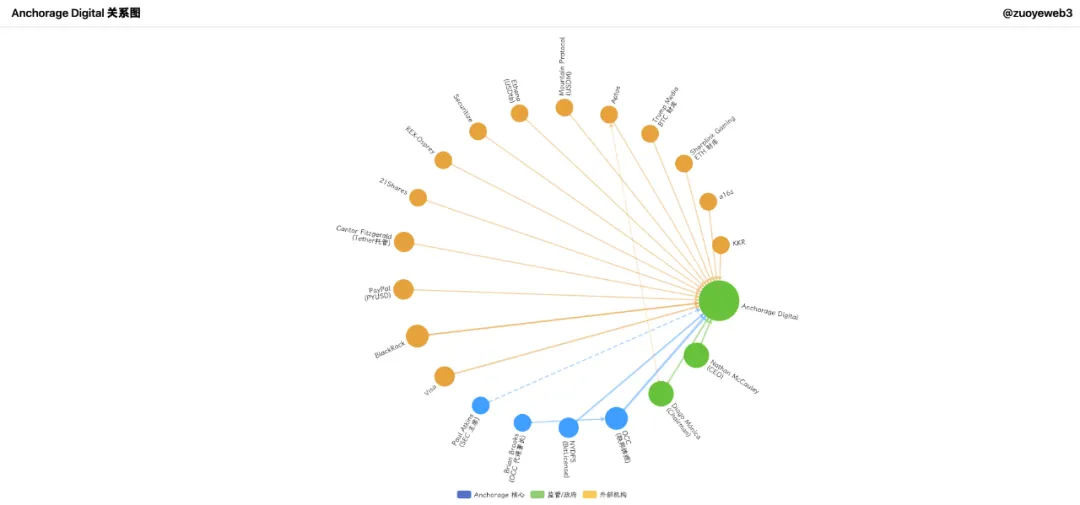

Image caption: Anchorage Digital network map

Image source: @zuoyeweb3

Anchorage Digital has developed diverse services around institutions—trading, derivatives, clearing, staking, and custody—essentially offering one-stop crypto solutions. Beyond traditional crypto custody, Anchorage is betting its future on stablecoins, which is its key difference from Galaxy.

Thus, we arrive at the first chapter of the story: startup rule #1—timing is everything.

In 2021, Democrat Joe Biden, who held strict regulatory views on crypto, entered the White House. SBF, who had spent millions supporting Biden, was eagerly awaiting a crypto spring. Meanwhile, Brian Brooks, former chief legal officer at Coinbase, became acting comptroller of the OCC.

During his tenure, Brooks maintained a pro-crypto stance, pushing banks to open service windows for crypto businesses and launching the Responsible Innovation in Financial Technology (REACh) initiative, encouraging banks not to discriminate against crypto firms.

Anchorage seized the moment, transforming overnight from a regional trust firm into Anchorage Digital Bank—a true national bank.

Again: on January 13, 2021, Anchorage Digital Bank gained eligibility to accept USD deposits and perform crypto custody.

One day later, on the 14th, Brian officially left office. By sheer coincidence, Anchorage Digital became the only licensed crypto bank to date.

Today, you’ll see references to this license’s value across nearly every page and product description at Anchorage Digital. This helped raise $430 million in Series C and D rounds, carrying it through to ride the 2025 stablecoin wave.

Notably, investors include both crypto VCs like a16z and Wall Street giants like KKR and BlackRock.

A side note: Bitpay and Paxos were also applying at the time, but weren’t lucky. Recently, Paxos was fined $26.5 million by New York DFS for BUSD non-compliance.

Incidentally, Anchorage holds both an OCC federal crypto banking license and a New York BitLicense—second in compliance credibility only to BNY.

Still, after Brian’s departure, Anchorage clashed with the OCC—but incredibly, retained its license.

One license, lifetime benefits.

With the license, Anchorage can custody almost anything—from stablecoin reserve assets and cryptocurrencies to NFTs. However, the 2022 crypto crash gradually destabilized Anchorage, starting with founder “infighting.”

Ultimately, Diogo Mónica left to join Hanu Ventures as a partner, retaining the role of Executive Chairman at Anchorage Digital, focusing on hiring and strategy. Nathan McCauley took over primary operations, beginning outreach to BlackRock and stablecoin initiatives.

To summarize: in ETFs, Anchorage became custodian for 21Shares’ Bitcoin and Ethereum spot ETFs, and exclusive custodian and staking partner for REX-Osprey’s Solana staking ETF.

But beyond ETFs, Anchorage Digital has achieved significant success, especially in stablecoins—partnering with Visa on stablecoin payments and introducing “compliant” stablecoins like PayPal’s PYUSD for institutional investors.

Even more striking: Cantor Fitzgerald, both a Tether investor and custodian, partnered with Anchorage to provide custody services for Cantor’s Bitcoin business.

Anchorage Digital thus became the custodian for Tether’s custodian.

Despite holding a license, Anchorage’s business wasn’t outstanding before 2025. Though valued at $3 billion with $50 billion in AUM, it felt hopeless competing with Coinbase in ETFs. Anchorage Digital’s real focus has always been stablecoins.

As mentioned earlier, Anchorage Digital holds a federal crypto license. Its subsidiary, Anchorage Digital Bank NA, can accept both USD and stablecoin deposits and offer custody services.

-

• Off-chain: Partnered with Ethena to expand USDtb issuance scale, complying with Genius Act stablecoin regulations

-

• On-chain: Joined forces with Paxos and Kraken to form the USDG stablecoin alliance, jointly maintaining the Global Dollar Network’s on-chain operations

That said, Anchorage hasn’t been idle in treasury strategies. Former BlackRock executive Joseph Chalom joined ETH treasury firm Sharplink Gaming as Co-CEO and was instrumental in forging the BlackRock-Anchorage ETF custody partnership.

Moreover, the BlackRock BUIDL fund is deeply tied to Chalom, with Anchorage serving as custodian. Decoded:

$BUIDL = Issued by BlackRock = Securitize (tokenization tech) + Anchorage Digital (custody) + BNY (cash services)

We can further stretch connections: SEC Chair Paul Atkins holds at least $250,000 in Anchorage Digital shares and is also a shareholder in Securitize, which partners with Ethena in co-issuing Converage.

Spurred by Galaxy’s public listing, Anchorage Digital has long faced IPO speculation. Expanding stablecoin operations requires more capital—perhaps this year we’ll see the first crypto bank IPO.

Galaxy Digital Claims the Iron Throne of the Treasury Era

Compared to Anchorage Digital, Galaxy stands out more—not only as Goldman Sachs’ 2022 crypto OTC trial partner but also as a major exit venue for large BTC whales. Beyond that, Galaxy has diversified into Bitcoin mining, investments, and AI computing power. Founder Mike Novogratz also boasts broader connections than Anchorage Digital.

On July 25, Galaxy helped an early miner sell approximately 80,000 BTC ($9 billion). Though sold in tranches, news of the sale caused Bitcoin to drop nearly 4%, falling below $115,000.

Amid such massive trades, some accused Galaxy of manipulating or damaging the market. But Galaxy is a relatively pure institutional investor—unlikely to have motives to actively harm the market. Institutions seek low volatility and stability; return orientation drives larger market scales.

Yet that’s not the point. Galaxy’s defining trait is “timeliness”—its ability to keep pace with every cycle and era. Founder Mike Novogratz, an early non-technical finance professional, never approached crypto with faith but with profit in mind.

Now, as retail exits and institutions enter, Galaxy’s direction matters even more—especially the expansion of crypto treasury strategies.

Remember Sharplink, the ETH treasury company led by former BlackRock executives?

In June 2025, SharpLink made multiple ETH purchases via Galaxy OTC, totaling at least $800 million. Coincidentally, Galaxy is also one of SharpLink’s investors—buying from myself, left hand to right hand.

Beyond BTC and ETFs, Galaxy has participated in funding and building Ethena’s treasury Stablecoinx, and Mill City Ventures III, Ltd., a $450 million treasury for $SUI.

Galaxy is also expanding into more OTC offerings—providing OTC support for Liquid Collective’s LST token LsETH. Liquid Collective’s SOL version lsSOL also targets institutional investors, supported by Anchorage Digital.

Once again, what a small world.

Furthermore, GDN captures both Anchorage Digital and Galaxy Digital—validating that today’s custodians collaborate more than compete viciously.

However, unlike Anchorage Digital’s bank-license-driven passion for stablecoins, Galaxy’s main expansion remains focused on treasury strategies, with many non-BTC/ETH treasuries still in development.

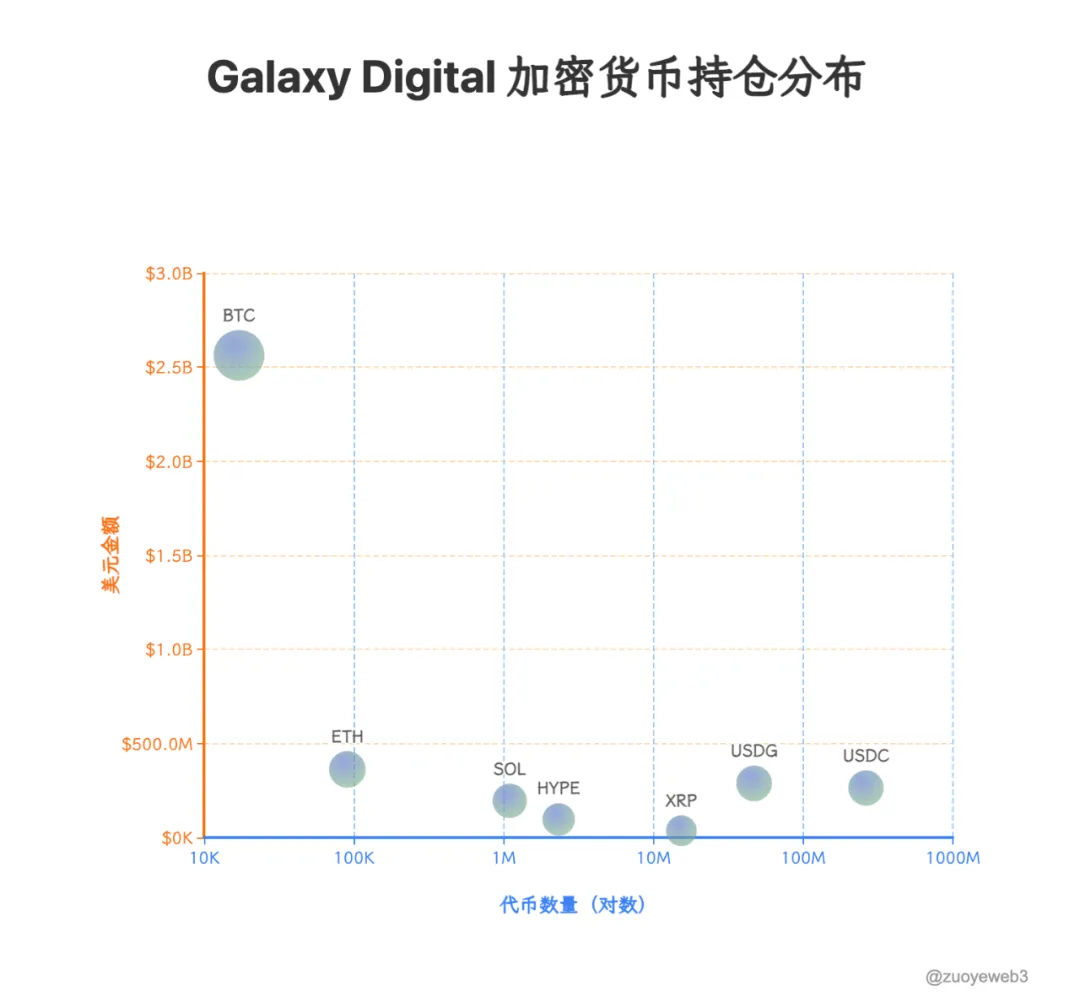

Leveraging its capital size, Galaxy itself holds $1.8 billion in BTC and strategically increased its stake in Ripple’s XRP by $34.4 million. Ironically, Ripple announced a $200 million acquisition of Rail, a stablecoin company backed by Galaxy.

Again: I buy myself, left hand to right hand.

Based on Galaxy’s reports, upcoming treasury or market-making focuses likely include $HYPE, $SOL, and $XRP. With Ripple fully resolving its SEC litigation, its price surged 10% that day—Galaxy was ahead of retail.

Galaxy has already exited positions in UNI and TIA—old aristocrats no longer have seats on the new train. USDG, HYPE, and XRP are newly ascendant. When the river warms, OTC knows first.

Previously, OTC could only passively accept whale orders, rarely influencing secondary markets directly—this is its key difference from on-exchange market makers. But treasury strategies change everything. Stocks, bonds, and tokens will issue in tandem. Who controls token prices remains uncertain.

Conclusion

Custodians are the new convergence points of capital. Off-chain funds need secure on-chain movement; on-chain assets require compliant off-ramping. Treasury strategies empower custodians to actively influence token prices. Crypto liquidity forms the fundamental power structure—once dominated by CEXs and market makers (MM), but both now fading.

BNY manages over $52 trillion in assets—compared to less than $4 trillion total crypto market cap, and only $520 billion combined in dollar-pegged stablecoins, crypto ETFs, and treasury companies. The market influence of crypto custodians still needs considerable time to mature.

But where the money is, that’s where the profits are. Every founder must think carefully.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News