a16z重磅预测:Vibe coding赢者通吃?

TechFlow Selected TechFlow Selected

a16z重磅预测:Vibe coding赢者通吃?

Wrong, vertical specialization is the future.

Have you noticed that AI app generation platforms are taking a path completely different from what everyone expected? Many assumed this would be a bloody zero-sum game, with companies fighting to the death in a price war until only one dominant player remained. But reality has been surprising: instead of battling each other, these platforms are increasingly carving out differentiated positions, coexisting and thriving in separate niche markets. This reminds me of the evolution of the large language model market—equally unexpected and deeply insightful.

Just yesterday, two a16z partners, Justine Moore and Anish Acharya, co-authored an analytical piece titled "Batteries Included, Opinions Required: The Specialization of App Gen Platforms," whose observations on the AI app generation platform market deeply resonated with me. They point out that these platforms are undergoing a differentiation process similar to foundational models—shifting from direct competition toward specialization. This insight made me rethink the developmental patterns of the entire AI tool ecosystem and reflect more critically on the myth of the "one-size-fits-all platform." I’ve long believed that "no universal coding platform can rule everything." Today, so many people are building applications with AI, across extremely diverse use cases: prototyping, personal websites, game development, mobile apps, SaaS platforms, internal tools, and more. How could any single product excel in all these areas?

My judgment is that this market will inevitably fragment. A consumer-grade application builder designed for beautiful landing pages simply cannot be the same product as an enterprise-grade internal tool builder. The former needs Spotify integration and viral potential on TikTok; the latter requires SOC 2 compliance and must be sold top-down to CTOs. The market is large enough to support multiple multi-billion dollar companies. Becoming the clear leader in a specific use case—focusing relentlessly on the features, integrations, and go-to-market strategies required by that scenario—may well be the winning strategy.

PS: I’ve recently started my own venture, building exactly such a vertically specialized vibe coding product, and we’ve already closed a Pre-seed round quickly. If you’re a VC partner who shares enthusiasm for this direction and has relevant insights, feel free to add me on WeChat (MohopeX) to chat. We’re also recruiting founding team members—interested candidates can find details at the end to submit resumes.

Lessons from Foundation Models: From Substitutes to Complements

Looking back at the foundation model market in 2022, nearly everyone held two incorrect assumptions. The first was that these models were essentially interchangeable substitutes—like fungible cloud storage solutions. Once you picked one, why bother with another? The second assumption was that since they were substitutes, competition would drive prices down to rock bottom, and the only way to win was to charge less.

But reality unfolded differently. We saw explosive growth in divergent directions. Claude dove deep into code and creative writing. Gemini carved out a unique edge in multimodal capabilities, offering high-performance models at low cost. Mistral focused on privacy and local deployment. Meanwhile, ChatGPT redoubled its efforts to become the "home base" for anyone seeking the broadest, most useful general-purpose assistant. Instead of consolidation, the market stayed open: more models, greater diversity, more innovation. Prices didn’t drop—they rose. Grok Heavy now charges up to $300 per month for its superior AI coding capabilities and viral text-to-image model, a price point unthinkable for consumer software just a few years ago.

This pattern repeats elsewhere. Recall the image generation space: in 2022, people said it was zero-sum or that “one model would eat it all.” Yet today, Midjourney, Ideogram, Krea AI, BFL, and others all thrive side by side, each focusing on distinct styles or workflows. These models aren’t “better” or “worse”—they make distinct artistic and functional choices, serving different creative tastes and needs.

Upon closer inspection, these models aren’t competitors at all—they’re complementary. This is the opposite of a race-to-the-bottom pricing war; it’s a positive-sum game: using one tool increases your likelihood of paying for another. My own usage illustrates this perfectly. When I need fast code generation, I turn to Claude; for multimodal analysis, I use Gemini; for creative writing, I might go back to ChatGPT. Each tool excels in specific scenarios, and I don’t feel they’re competing for my attention—they meet different needs at different times.

Specialization Has Begun in AI App Generation Platforms

I believe the same phenomenon is now unfolding in the AI app generation platform space. These tools help you build full applications using AI. It’s easy to get drawn into surface-level drama—Lovable vs Replit vs Bolt—but the truth is, this isn’t a winner-takes-all game. The market is massive and growing, with ample room for multiple breakthrough companies, each dominating its own niche.

As Justine notes in her article, the market is already beginning to segment along these lines, with each platform uniquely "standing out" in one of the following areas:

-

Prototyping platforms—tools built specifically for rapidly experimenting with ideas. These products must excel in aesthetics, prompt adherence, and fine-grained visual control, while enabling quick and rough implementation of business logic.

-

Personal software platforms—designed to build apps tailored to you and your workflow. These may serve the least technical users, requiring true "out-of-the-box" usability, possibly even including an easily editable library of comprehensive templates.

-

Production-grade app platforms—built for teams or public release. These require built-in core functionalities like authentication, databases, model hosting, payments, and one-click scalability.

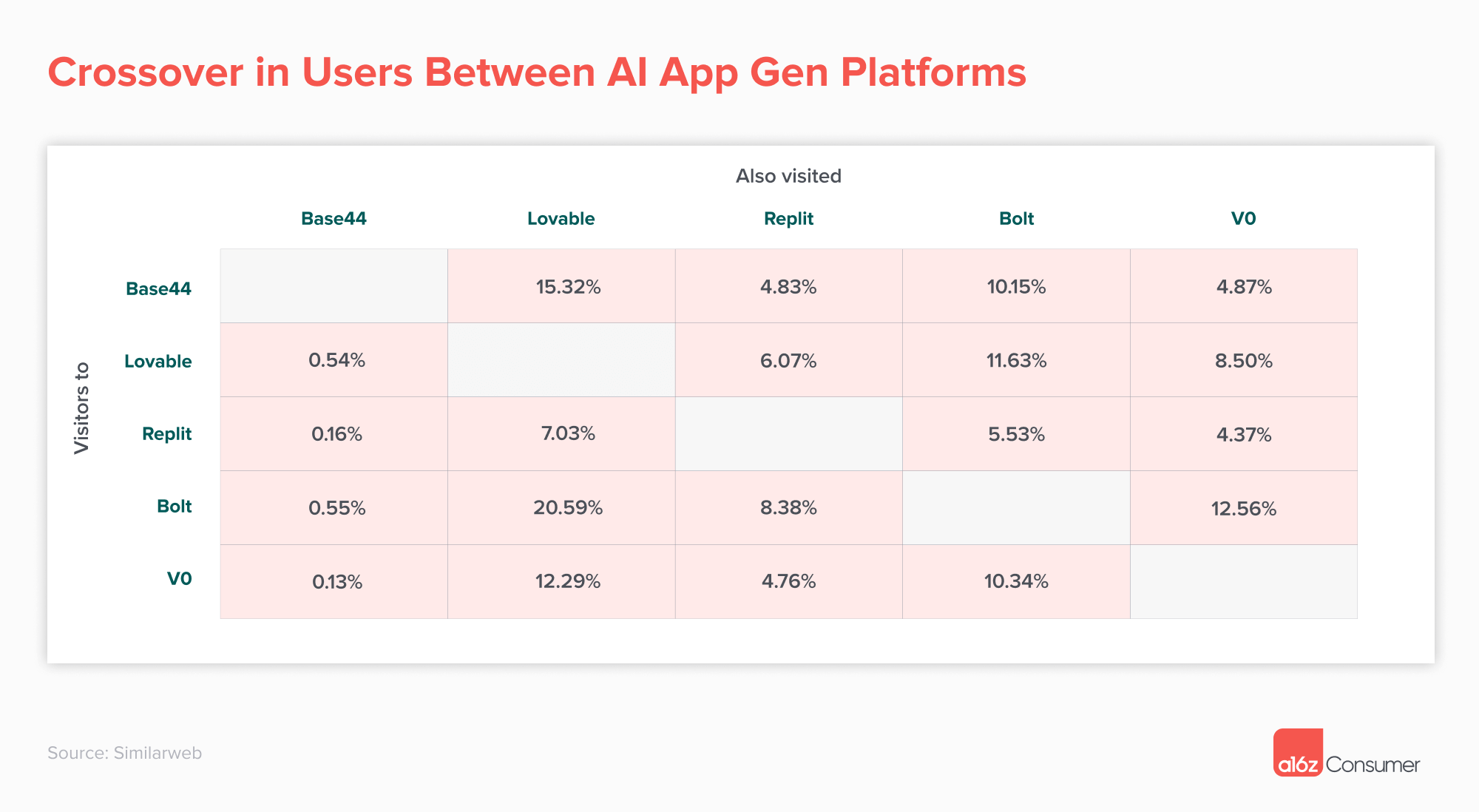

Within each category, there will likely be platforms targeting different user levels—from everyday consumers to semi-technical product managers, all the way to core developers. In other words, for every type of application, there will be a spectrum of solutions. Data from Similarweb, though still early, already shows this trend in cross-browsing behavior among key app generation platforms: Lovable, Bolt, Replit, Figma Make, v0, and Base44.

The data reveals two types of users. The first are loyalists—users committed to a single platform. For example, over the past three months, 82% of Replit users and 74% of Lovable users accessed only Replit or Lovable within this group. These users may perceive current app generation platforms as functionally similar but choose one primary tool, possibly due to marketing, UI, or a specific feature they care about. Anecdotally, Lovable appears favored for aesthetic web apps and prototyping, while Replit seems preferred for more complex, backend-heavy applications.

The second type are active multi-platform users. For instance, nearly 21% of Bolt users also visited Lovable over a three-month period. 15% of Base44 users also viewed Lovable. I suspect these are super-users who actively leverage multiple platforms in a complementary manner. This user behavior mirrors how I use different design tools: I might use one for rapid prototyping, switch to another for precise design control, and pick a third for collaboration with engineering teams. Each tool has unique strengths, and I select based on immediate needs.

Specialization Is the Inevitable Trend

I’m increasingly convinced that in the domain of tools helping users build scalable applications, constraints beat openness. Excelling at developing a specific kind of product is likely far better than being merely adequate at generating everything. An app generation platform that excels at building SAP-integrated internal tools is unlikely to also be the best choice for creating a highly accurate flight simulator app.

Let’s analyze this specialization trend further. Different types of applications impose vastly different requirements on the underlying platform:

Data/service wrapper apps aggregate, enrich, or present large existing datasets or third-party services—like LexisNexis or Ancestry. Infrastructure must support operations on big datasets. The core challenge here lies in data processing power and integration complexity, not interface aesthetics.

Utility apps are lightweight, single-purpose tools solving highly specific needs—such as PDF converters, password managers, or backup utilities. Most horizontal platforms already perform well in generating these. Their hallmark is clear functionality, relatively simple logic, and high demands on reliability and performance.

Content platform apps are built for content discovery, streaming, or reading—like Twitch or YouTube—and require specialized infrastructure for content distribution. Technical challenges center on large-scale content delivery, real-time streaming, and personalized recommendation algorithms.

Business hub apps facilitate and monetize transactions, focusing on logistics, trust, reviews, and price discovery. These require integrations for payments, refunds, discounts, etc. Here, compliance, security, and financial integration complexity are paramount.

Productivity tools help individuals or organizations complete tasks, collaborate, and optimize workflows, often involving extensive integrations with other services. These demand deep understanding of enterprise workflows and existing tool ecosystems.

Social/messaging apps enable users to connect, communicate, and share content, often forming networks and communities. Infrastructure must support large-scale real-time interactions. Key challenges include managing social graphs, real-time communication, and content moderation.

What I observe is that each category has its own distinct tech stack, integration needs, and UX considerations. A platform specializing in e-commerce app generation would embed payment processing, inventory management, order tracking, and deeply optimize these flows. A platform focused on data dashboards would invest heavily in data visualization, real-time updates, and complex query optimization. This specialization goes beyond features—it reflects fundamentally different product philosophies and technical architectures.

The Deeper Logic Behind Market Segmentation

At a deeper level, this market segmentation reflects the inherent complexity of software development itself. In the past, we treated software development as a unified domain, but in reality, different application types face entirely different challenges and constraints. Mobile apps must consider touch interaction, battery life, offline functionality; web apps must address browser compatibility, SEO, responsive design; enterprise internal tools must handle security compliance, legacy system integration, and permission management.

When AI begins automating development, these differences become even more critical. An AI system skilled at generating beautiful landing pages is trained, prompted, and optimized around visual appeal, conversion rate, and marketing impact. In contrast, an AI system for enterprise internal tools focuses on entirely different priorities: data security, system integration, user permissions, audit logs, and more.

I often see teams attempting to build "universal" AI app generation platforms that aim to satisfy all user needs. But this approach overlooks a crucial point: conflicting optimization goals. When you try to simultaneously optimize for visual appeal and enterprise compliance, you end up compromising on both. Specialized platforms avoid this trade-off, achieving excellence in their chosen domain.

This reminds me of the evolution of traditional software development tools. We once had "super IDEs" aiming to cover all development scenarios, but the market ultimately fragmented. Now we have dedicated tools for web development, mobile development, and data science. Each delivers unparalleled experience in its niche—proving more valuable than a jack-of-all-trades, master-of-none alternative.

In AI app generation, I expect a similar divergence. There will be platforms exclusively for e-commerce sites, with built-in Shopify integration, payment handling, and inventory management. Platforms for data dashboards will specialize in connecting data sources, creating interactive charts, and enabling real-time updates. Mobile app generators will understand iOS and Android design guidelines, push notifications, and app store optimization.

Insights from User Behavior

The user behavior data mentioned in Justine’s article is particularly illuminating. The "super users" who switch between multiple platforms validate my view: different platforms suit different use cases. A developer might use Lovable for rapid prototyping, Replit for backend-heavy applications, and other platforms for specific integrations.

This usage pattern mirrors modern developers’ toolchains. No one expects a single tool to do everything. We use Figma for design, VS Code for coding, GitHub for version control, Vercel for deployment, Stripe for payments. Each excels in its domain, and together they create a development experience far more powerful than any single "do-it-all" tool.

AI app generation platforms will likely follow a similar trajectory. Users will select the best-suited platform for each task rather than being forced into a generalized, mediocre solution. This freedom of choice actually enhances the ecosystem’s overall value, as each platform can focus on doing what it does best.

Another interesting trend I’ve observed is that users’ tolerance for switching costs is decreasing. In traditional software development, learning a new tool is costly, so developers tend to stick with familiar ones. But in the AI-driven era, learning curves have flattened dramatically. If a platform enables most tasks via natural language, the barrier to trying a new one becomes very low. This further encourages specialization, as users are more willing to seek the optimal tool for specific needs.

Rethinking Business Models

This trend toward specialization will also reshape the business models of AI app generation platforms. Traditional SaaS models emphasize economies of scale and network effects, aiming to acquire and lock in as many users as possible. But in a specialized world, depth matters more than breadth.

A platform focused on e-commerce apps can forge deep integrations with Shopify, WooCommerce, BigCommerce, and deliver an app generation experience unmatched by generalist platforms. Its customer count may be smaller, but each customer brings higher value and stronger retention. Such a specialized platform could even develop industry-specific pricing models, such as revenue sharing based on transaction volume, rather than flat subscriptions.

Likewise, a platform for enterprise internal tools can deeply integrate with existing IT infrastructure, offering seamless single sign-on, data synchronization, and compliance auditing. Such platforms may adopt enterprise sales models—using direct sales teams to serve large clients—rather than relying on self-service signups.

I believe this diversification of business models fosters a healthier competitive landscape. Each platform can focus on serving its core user base instead of trying to please everyone. This reduces head-to-head competition and allows each player to build strong moats in its specialty.

From an investment perspective, this also means different investors will be drawn to different platforms. Consumer-focused platforms may attract those prioritizing user growth and virality, while enterprise-focused ones may appeal to investors valuing stable cash flow and long-term client relationships. This diversity brings more capital and attention to the entire sector.

Differentiation in Tech Stacks

At the technical level, I find that different applications demand vastly different underlying tech stacks—further reinforcing the necessity of specialization. A platform focused on real-time apps (like chat or collaboration tools) must heavily optimize WebSocket connections, message queues, and state synchronization. A platform for data-intensive apps must prioritize database query optimization, caching strategies, and data visualization.

An interesting trend I’ve noticed is that platforms are beginning to diverge in their choice and optimization of AI models. Platforms generating beautiful interfaces may rely more on image generation models and design-centric training data. Those generating backend logic lean more on code generation models and software architecture-related data. This targeted optimization significantly boosts each platform’s performance in its specialty.

More importantly, evaluation criteria for output quality differ drastically across app types. A consumer app may prioritize UI beauty and smooth user experience—even tolerating suboptimal code. An enterprise app values code maintainability, security, and scalability—even if the interface is plain. These differing standards dictate distinct optimization goals and quality control mechanisms across platforms.

I’ve especially noted that platforms are beginning to differentiate in deployment and operations. Platforms for personal projects may offer simple one-click deployment to static hosting. Enterprise-focused platforms need complex CI/CD pipelines, multi-environment management, monitoring, and alerting. These subtle differences have decisive impacts on end-user experience.

The Evolution of the Ecosystem

From a broader perspective, the specialization of AI app generation platforms reflects the overall trajectory of the software development ecosystem. We’re witnessing a shift from "tool-centric" to "outcome-centric" development. Users no longer care which tool they use—they care about the results they achieve. This shift creates massive opportunities for specialized platforms.

I expect that in the coming years, we’ll see a surge of vertical AI app generation platforms. There will be platforms dedicated to game development—understanding game engines, physics systems, level design. Platforms for educational apps—embedding LMS integration, progress tracking, personalized learning paths. Platforms for healthcare apps—compliant with HIPAA and other medical data regulations.

This verticalization won’t just change product forms—it will reshape talent demands. Specialized platforms require hybrid talent: people who deeply understand both AI and specific industries. A platform for financial apps needs experts in financial compliance, risk management, trading systems. This shift in talent needs will further solidify the competitive advantages of specialized platforms.

I’ve also observed that specialized platforms are starting to cooperate rather than compete. A front-end generation platform might partner with a back-end specialist to offer end-to-end solutions. This collaborative model fosters a more open, interconnected ecosystem where each platform focuses on its core strength.

In the long run, I believe this trend will push the entire field of AI app development toward greater maturity. When every niche has dedicated platforms innovating deeply, the overall industry level rises, and users benefit from better experiences. It’s a win-win: platforms build deep moats in their specialties, users gain more tailored solutions, and the ecosystem becomes richer and more diverse.

My Predictions and Thoughts

Based on these observations, I have several predictions for the future of AI app generation platforms. Within the next three to five years, I expect the market to clearly split into several major categories: consumer-facing rapid prototyping platforms, template-based platforms for small businesses, custom internal tool builders for large enterprises, and various vertical-specific specialized platforms.

In each category, 2–3 dominant players will emerge, gaining advantage through deep specialization and ecosystem building. These platforms won’t aim to replace each other—they’ll deepen their expertise in their domains, delivering specialized value that generalist platforms can’t match.

I’m especially bullish on platforms that can build deep moats in specific verticals. For example, a platform focused on restaurant apps that deeply integrates ordering systems, inventory, staff scheduling, and financial reporting will be hard to displace by generalist platforms. Accumulated industry knowledge and specialized integrations are difficult for generic platforms to replicate.

I also believe user behavior will fundamentally shift. As switching costs between platforms decrease, users will become more "tool-rational"—choosing the best platform for each specific need rather than remaining loyal to one. This shift will further accelerate platform specialization, as only those excelling in a particular domain will earn a spot in users’ toolkits.

Technologically, I expect even greater divergence in AI model training and optimization across specialized platforms. Different application domains demand different AI output qualities, driving platforms to develop more targeted models. We may see models specifically optimized for code generation, UI design, or business logic, respectively.

Finally, I believe this trend will redefine what "platform success" means. In the past, success meant having the most users and widest reach. But in a specialized world, success may mean deepest impact in a niche, highest customer value, and strongest domain expertise. This shift in success metrics will unlock more diverse business opportunities and foster a healthier, more sustainable industry.

In summary, the specialization of AI app generation platforms isn't just an inevitable technological outcome—it's a sign of market maturity. As user needs grow more diverse and sophisticated, the limitations of one-size-fits-all solutions become apparent. Platforms that deeply understand specific user needs and deliver tailored solutions will dominate the future. The market is large enough to support multiple successful specialized companies—the key is finding your position and going deep.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News