Why We Invested in SBET: The Starting Point of a New Era of CeDeFi Convergence

TechFlow Selected TechFlow Selected

Why We Invested in SBET: The Starting Point of a New Era of CeDeFi Convergence

Our $425 million PIPE investment in SharpLink Gaming is based on a strong belief in Ethereum's strategic role in corporate treasury strategies.

Authors: Yetta ( @yettasing ), Investment Partner at Primitive Ventures

Sean Tan, Liquidity Partner at Primitive Ventures, Former Macro Portfolio Manager at Tower Research

Preface

This article was written in May 2025. In May, we completed our PIPE investment in SharpLink, marking a milestone in our focused research on the PIPE market since the beginning of the year. Since early this year, Primitive Ventures has actively positioned itself to capture the CeDeFi convergence trend with a forward-looking perspective, leading the charge in Digital Asset Treasury PIPE transactions. Under this framework, we have systematically analyzed all representative deals, and SharpLink is undoubtedly the most critical and emblematic transaction we have participated in to date.

Full Article

We are pleased to announce that Primitive Ventures has participated in the $425 million PIPE (Private Investment in Public Equity) transaction for SharpLink Gaming, Inc. (NASDAQ: SBET). This investment provides us with a unique exposure—investing in a native enterprise whose strategy centers on holding Ethereum as treasury reserves. The investment structure combines optionality with long-term capital appreciation potential, reflecting our strong conviction in Ethereum’s strategic position within the U.S. capital markets, and aligns with our broader assessment of the institutionalization trend in crypto assets.

Why We Invested

ETH vs BTC: The Divide in Productive Value

Compared to BTC, which lacks native yield capabilities, Ethereum as an income-generating asset inherently produces staking rewards. Strategies based on BTC, such as MicroStrategy, primarily rely on leveraged financing to acquire coins, lacking self-sustaining asset yields and carrying higher leverage risks. In contrast, SBET has the potential to directly utilize ETH staking rewards and the DeFi ecosystem to achieve compounding growth on-chain, creating tangible value for shareholders.

Currently, no ETH staking-based ETF has been approved under existing regulatory frameworks, leaving public markets largely unable to capture the economic potential of Ethereum's yield layer. We believe SBET offers a differentiated path: with support from Consensys, the company has the opportunity to implement protocol-native strategies and generate significant returns on-chain—potentially outperforming future ETH staking ETFs.

Additionally, Ethereum’s implied volatility (69) is significantly higher than Bitcoin’s (43), introducing asymmetric upside call options into equity-linked structures. This is particularly attractive to investors employing convertible bond arbitrage and structured derivatives strategies—in this context, volatility becomes a monetizable asset rather than a risk source.

Strategic Participation by Consensys

We are proud to partner with Consensys, the lead investor in this $425 million PIPE round. As one of the most effective executors of Ethereum commercialization, Consensys holds unique advantages in technical authority, depth of product ecosystem, and operational scale, making it the ideal investor to drive SBET as a native vehicle for Ethereum-based enterprises.

Founded in 2014 by Ethereum co-founder Joe Lubin, Consensys has played a pivotal role in transforming Ethereum’s open-source foundation into scalable real-world applications—from EVM and zkEVM (Linea) to the MetaMask wallet, which has brought tens of millions of users into Web3. Consensys has raised over $700 million cumulatively from top-tier investors including ParaFi and Pantera, and possesses a track record of successful strategic acquisitions, solidifying its position as the most deeply embedded commercial operator in the Ethereum ecosystem.

Joe Lubin’s role as chairman extends beyond symbolism. As one of the core architects of Ethereum and a leader in one of its most important infrastructure companies, Joe brings unparalleled and comprehensive understanding of Ethereum’s product roadmap and asset architecture. His early career on Wall Street also equips him with the sophistication to navigate capital markets, enabling him to guide SBET smoothly into institutional financial systems.

In SBET, we see a powerful combination of a unique asset and the most capable investor. This synergy creates a strong positive flywheel—driven jointly by protocol-native treasury strategies and a protocol-native leader. Under Consensys’ leadership, we believe SBET has the potential to become a flagship case demonstrating how productive Ethereum capital can be institutionalized and scaled within traditional capital markets.

Market Valuation Comparison

To understand SBET’s investment opportunity, we analyze crypto treasury strategies across various public companies:

MicroStrategy: Pioneer of Crypto Treasury Strategy

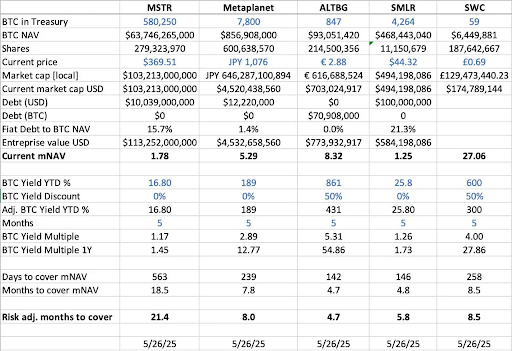

MicroStrategy set the industry benchmark for crypto treasury strategies. As of May 2025, it held 580,250 bitcoins, valued at approximately $63.7 billion. MSTR’s strategy involves issuing low-cost debt and equity to purchase Bitcoin—a model that sparked widespread corporate adoption and demonstrated the feasibility of crypto assets as reserve holdings.

As of May 2025, MSTR held 580,250 BTC (worth ~$63.7B) and traded at a 1.78x mNAV (market value / net asset value), highlighting strong investor demand for regulated, leveraged crypto exposure via public equities. This premium stems from multiple factors: upside potential from leverage, eligibility for index inclusion, and ease of access compared to direct ownership.

Historically, from August 2022 to August 2025, MSTR’s mNAV fluctuated between 1x and 4.5x, reflecting significant market sentiment influence. A 4.5x multiple typically coincided with Bitcoin bull markets and large-scale purchases by MSTR, signaling high investor optimism; while a drop to 1x often occurred during market consolidation periods, revealing cyclical shifts in investor confidence.

Peer Company Comparison

We conducted a cross-sectional analysis of several public companies employing BTC treasury strategies:

- In terms of BTC Net Asset Value (BTC NAV)—i.e., the total value of BTC held—MicroStrategy leads with 580,250 BTC (~$63.7B), followed by Metaplanet (7,800 BTC, ~$857M), SMLR (4,264 BTC, ~$468M), ALTBG (847 BTC, ~$93M), and SWC (59 BTC, ~$6.4M).

- Regarding the ratio of market cap to BTC NAV (mNAV), SWC has the highest premium at 27.06x, driven by small BTC base size and strong market enthusiasm. ALTBG stands at 8.32x, Metaplanet at 5.29x—both maintaining elevated levels. In contrast, MSTR at 1.78x and SMLR at 1.25x show more moderate premiums due to larger asset bases and existing debt burdens.

- Year-to-date BTC yield (BTC Yield YTD %) (dilution-adjusted, percentage increase in BTC per share): Smaller-cap firms show higher per-share BTC growth due to continuous accumulation—ALTBG reached 431%, SWC 300%. These figures reflect their capital efficiency and compounding ability.

- Based on current BTC reserve growth rate (Days/Months to Cover mNAV), ALTBG and SMLR could theoretically accumulate enough BTC within five months to cover their current mNAV premiums, offering potential alpha space for NAV convergence and relative mispricing trades.

- On the risk front, MSTR and SMLR carry debt equivalent to 15.7% and 21.3% of their BTC NAV respectively, exposing them to greater risk during BTC price declines; ALTBG and SWC are debt-free, presenting more manageable risk profiles.

The Japanese Metaplanet Case: Regional Market Arbitrage

Valuation differences often stem from variations in asset reserve scale and capital allocation frameworks. However, regional capital market dynamics are equally critical in explaining these divergences. A prime example is Metaplanet, frequently dubbed “Japan’s MicroStrategy.”

Its valuation premium reflects not only its Bitcoin holdings but also structural advantages tied to Japan’s domestic market:

- NISA Tax Advantage: Japanese retail investors are actively allocating to Metaplanet stock through NISA (Nippon Individual Savings Account). This scheme allows up to approximately $25,000 in capital gains to be tax-free—significantly more attractive than the up to 55% tax on direct BTC holdings. According to data from SBI Securities, as of the week ending May 26, 2025, Metaplanet was the most purchased stock across all NISA accounts, driving its share price up 224% over the prior month.

- Japanese Bond Market Dislocation: With Japan’s debt-to-GDP ratio reaching 235%, the 30-year JGB yield has risen to 3.20%, indicating structural stress in Japan’s bond market. Against this backdrop, investors increasingly view Metaplanet’s 7,800 BTC holdings as a macro hedge against yen depreciation and domestic inflation risks.

SBET: Positioning for Global ETH Blue-Chip Status

When operating in public markets, regional capital flows, tax regimes, investor psychology, and macroeconomic conditions are as important as the underlying asset itself. Understanding jurisdictional differences is key to unlocking asymmetric opportunities at the intersection of crypto assets and public equities.

As the first public company centered on ETH capital, SBET similarly holds potential to benefit from strategic jurisdictional arbitrage. We believe SBET could unlock additional regional liquidity—and mitigate narrative dilution—by pursuing dual listings in Asian markets such as HKEX or the Nikkei. Such a cross-market strategy would help establish SBET as the most representative globally recognized native Ethereum public asset, earning institutional recognition and participation.

Institutionalization of Crypto Capital Structures

The convergence of CeFi and DeFi marks a pivotal turning point in the evolution of crypto markets, signaling increasing maturity and integration into the broader financial system. On one hand, protocols like Ethena and Bouncebit exemplify this trend by combining centralized components with on-chain mechanisms to enhance the utility and accessibility of crypto assets.

On the other hand, the integration of crypto assets with traditional capital markets reflects a deeper macro-financial transformation—the gradual establishment of crypto as a compliant, institution-grade asset class. This evolution can be broken down into three key stages, each representing a leap in market maturity:

- GBTC: One of the earliest institutional BTC investment vehicles, GBTC provided regulated market access but lacked a redemption mechanism, causing persistent price deviations from NAV. While groundbreaking, it exposed structural limitations of traditional wrapped products.

- Spot BTC ETF: Approved by the SEC in January 2024, spot ETFs introduced daily creation/redemption mechanisms, tightly anchoring prices to NAV and significantly boosting liquidity and institutional participation. However, as passive instruments, they fail to capture key aspects of crypto’s native potential—such as staking, yield generation, or active value creation.

- Corporate Treasury Strategies: Companies like MicroStrategy, Metaplanet, and now SharpLink advance the evolution by integrating crypto assets into their financial operations. This stage goes beyond passive holding, incorporating strategies such as compounding yields, asset tokenization, and on-chain cash flow generation to improve capital efficiency and drive shareholder returns.

From the rigid structure of GBTC, to the mechanistic breakthrough of spot ETFs, to the emergence of yield-optimized treasury models today, this trajectory clearly shows crypto assets becoming increasingly embedded in modern capital market architecture—delivering stronger liquidity, higher maturity, and greater value creation potential.

Risk Warnings

Despite our strong conviction in SBET, we remain cautious about two potential risks:

- Premium Compression Risk: If SBET’s stock price trades persistently below its net asset value, it may lead to dilution in future equity financings.

- ETF Substitution Risk: If an ETH ETF is approved with staking functionality, it could offer a simpler compliant alternative, potentially diverting capital away from SBET.

Nevertheless, we believe SBET’s native ETH yield generation capability will allow it to outperform ETH ETFs over the long term, achieving a healthy balance of growth and yield.

In summary, our $425 million PIPE investment in SharpLink Gaming is rooted in a firm belief in Ethereum’s strategic role in corporate treasury strategies. With the backing of Consensys and leadership from Joe Lubin, SBET has the potential to represent a new phase of crypto value creation. As CeFi and DeFi convergence reshapes global markets, we will continue supporting SBET to deliver long-term superior returns, fulfilling our mission of “discovering high-potential opportunities.”

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News