Pump/Bonk/$M: Three Meme Coins, Two Paths to Asset Issuance

TechFlow Selected TechFlow Selected

Pump/Bonk/$M: Three Meme Coins, Two Paths to Asset Issuance

The first layer is an elephant in a tin room; the second layer hides beneath the elephant, and when the window is punched through, the elephant flies into the sky.

Author: Zuoye Waboshan

Secret to getting rich quick = creating new asset classes + improving capital efficiency

In the full lifecycle of $PUMP—from token launch and hype to noise and finally silence—the biggest winner has already emerged: MemeCore. Its token $M not only dominated CT's trending charts but also secured a spot on Binance Alpha, followed closely by Bonk, which is now targeting Chinese-speaking users.

When foreign projects speak Chinese again, it reminds me of the SBF era, when the world still felt unified.

Caption: Bonkfun speaks Chinese

Image source: @SolportTom

But don't panic—this article isn't about analyzing price movements of PUMP-like tokens. Instead, I want to explore why meme platforms are launching tokens, and how, even after the broader meme cycle has ended, such launches can still generate significant waves.

Earning the Last Penny

PumpFun’s token issuance maximizes the platform's own value as a meme ecosystem.

A typical meme platform should have died the moment CZ announced FourMeme. Note that I'm referring to the end of the industry-wide consensus around meme platforms as mainstream asset issuance venues. If we're talking about memes themselves, their peak arguably ended in January with the launch of $TRUMP.

For context: Memecoins Come from the Sea, and Return to the Sea

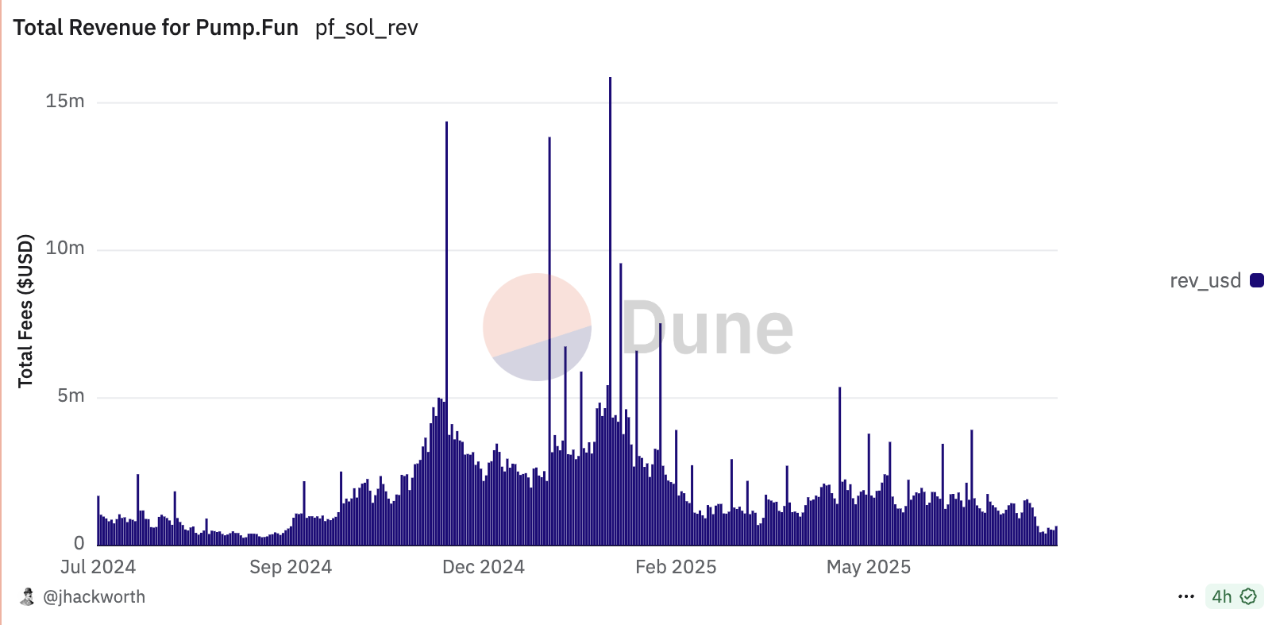

The subsequent split between PumpFun and Raydium—where one builds AMM pools while the other focuses on meme token launches—is clear evidence of fragmented consensus.

Caption: PumpFun profit trend

Image source: @jphackworth42

It’s increasingly strange: how did PumpFun not only become the center of attention for its platform token nearly half a year later, but also attract competitors like Bonk and $M to share liquidity? Compare this to sectors like DePIN, NFTs, BTCFi, and L2s—none of these typically sustain massive token launch traffic after their main narratives have concluded.

The more common pattern is to issue a token at the peak of sector-wide attention, extracting maximum market liquidity all at once:

-

• For NFTs: Blur (success), OpenSea (failure)

-

• For DePIN: Filecoin, Helium (Mobile) (success), Starpower (failure)

-

• For BTCFi: Babylon (success), most BTC L2s (failures)

In theory, once $TRUMP absorbed most of the normal meme liquidity, and especially after FourMeme launched, PumpFun should have been finished. Yet the $PUMP token still managed to stir things up.

PumpFun has delivered the perfect exit strategy for a dying sector—earning every last penny the market had saved.

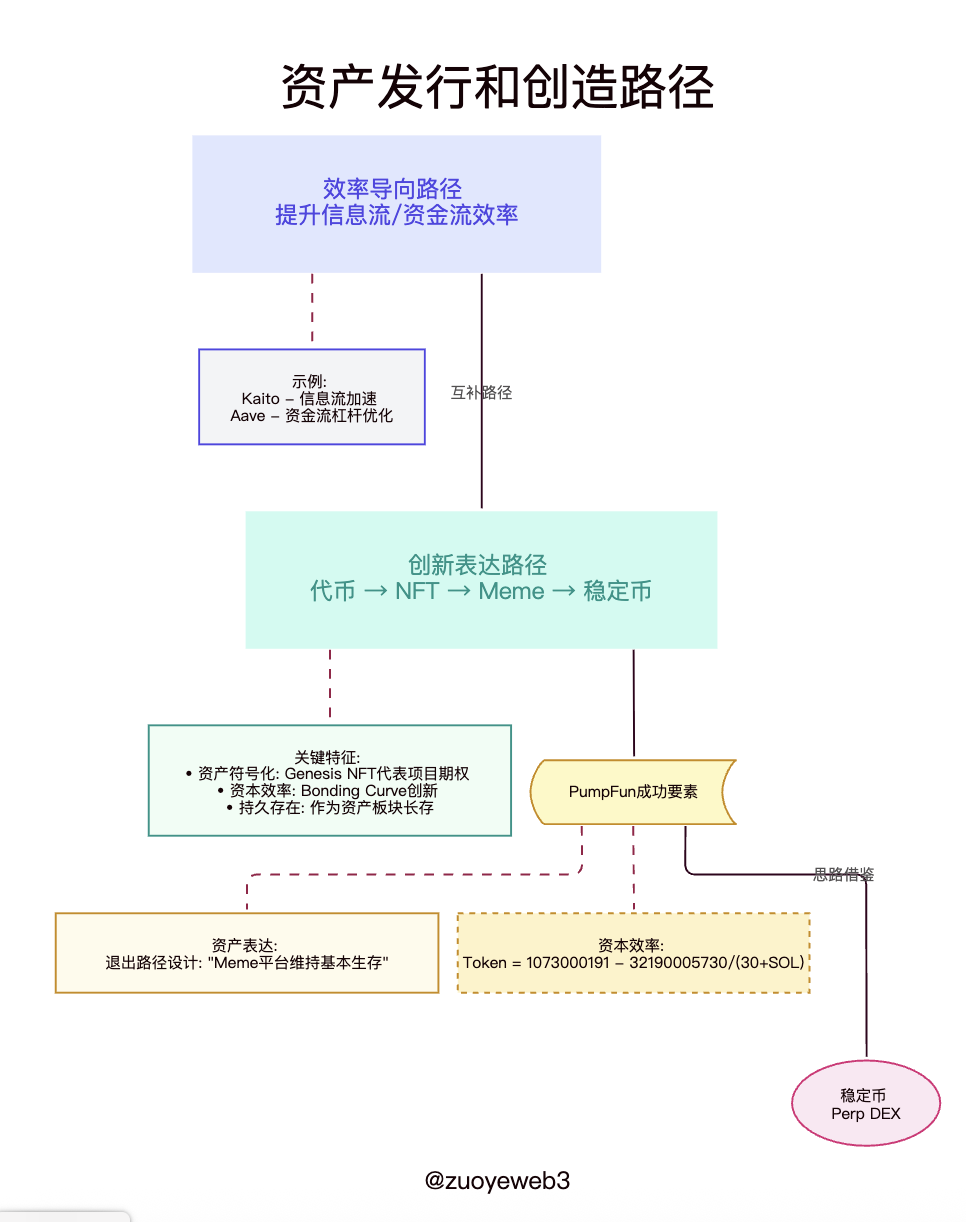

In crypto asset creation and expression, there are two paths: efficiency-driven models that accelerate information flow (Kaito) or capital flow (Aave), and innovation in expression, evolving along the path of token → NFT → Meme → stablecoin.

To understand how PumpFun succeeded, let’s revisit the successes and failures of NFTs. Unlike proven-dead sectors like inscriptions or BTCFi, NFTs found a lasting niche among project creators.

Genesis NFTs represent project options—or something akin to CoinList, depending on how they’re structured. NFTs as fashion statements or event tickets failed, but they succeeded as asset symbols.

The NFT trend won’t return, but in my view, memes as an asset class will endure.

Just like the altseason may never fully return, yet people still launch alts and farm Alpha points.

So it is with memes. Valuation frameworks evolve. PumpFun won’t become Binance or Hyperliquid, but then again, Uniswap didn’t dominate everything either—and it’s still alive.

Beyond total failure or ultimate success lies a third option: landing safely. History will judge whether that was right or wrong.

The Next Viable Use Case

Previously, "real-world adoption" meant mass consumer use;

Now, in crypto, "adoption" means successfully completing a token launch.

Caption: Paths of asset creation and issuance

Image source: @zuoyeweb3

Not everyone will remain obsessed with memes, but as long as some people participate, the asset class and launch platforms can survive. There must always be places to buy digital Maotai or virtual $LABUBU.

From blue-chip NFTs to Genesis NFTs, from $TRUMP to $PUMP, one era has ended. Within a single crypto cycle, memes lasted six months—longer than many 2–3 month technical narratives.

What remains is the mystery of the bonding curve. We understand AMM DEXs with x*y=k, but no one truly knows how bonding curve parameters are derived.

A little-known fact: FriendTech also used a bonding curve. Back in DeFi Summer 2020, it was actually a three-way battle between AMMs, order books, and bonding curves. Uniswap won AMMs, dYdX took order books, and bonding curves only found real success when they met PumpFun.

Another key insight from PumpFun: bonding curves improve capital efficiency. Memes were never just a new asset type—PumpFun’s capital-efficiency-first design philosophy was the product-level winning move.

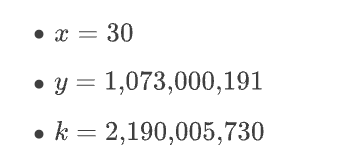

Referencing @CuntouErjiu’s algorithm, PumpFun heavily modified the standard x*y=k formula into a bonding curve equation:

Quantity Quantity

With parameter values:

Other meme launch platforms can reverse-engineer and copy PumpFun’s parameters, but the derivation process itself has become one of crypto’s unsolved mysteries—much like AI large models. Open-sourcing code alone is meaningless; true openness requires sharing training methods and datasets.

Unfortunately, no one has yet reverse-engineered PumpFun’s original formula. As a result, its moat in boosting capital (meme) efficiency remains strong. Even as memes cool down, residual traffic continues to underpin $PUMP’s value.

In this sense, PumpFun is far more reliable than many ghost chains. The fact that USDT exited Algorand and EOS shows that what gets forgotten isn’t necessarily memes.

Still, we must acknowledge: memes as a cultural phenomenon are over. Having had their moment in the sun is achievement enough. Only BTC and ETH enjoy lasting dominance; SOL still faces major hurdles to join them.

Notably, SOL isn’t even embraced by PumpFun—the team converts all earned SOL into USD-denominated capital. Meanwhile, EOS held onto its BTC proceeds until today. Where does Ethereum Foundation selling ETH fit into this picture?

Conclusion

Current hot topics are RWA and stablecoins. Focusing on PumpFun may seem outdated, but compared to single-hit products like FriendTech or Blur, PumpFun—and memes in general—will outlive NFTs or BTCFi. Its approach offers valuable lessons.

Design with the end in mind: founders must plan an exit strategy from day one—not just listing and token launch, but answering: after the spotlight fades, can you still find a sustainable role behind the scenes?

We can predict the same fate for Perp DEXs, since we still struggle to uncover off-chain order book matching algorithms.

Similarly, consider:

1. Routing algorithms for DEX aggregators

2. Matching algorithms for dark pool DEXs

3. Liquidity “ignition” algorithms for on-chain options

Especially for on-chain options—they currently face the same low-liquidity challenge that plagued pre-PumpFun meme trading. Traditional LP token incentives don’t seem effective.

One more thought: on-chain options need reinvention—either as natively crypto-native products like memes, or as circle-native adaptations like perpetual contracts. Maybe VIX-style indices are worth exploring?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News