Tokenized Stocks: A Financial Efficiency Revolution in an Old Bottle

TechFlow Selected TechFlow Selected

Tokenized Stocks: A Financial Efficiency Revolution in an Old Bottle

Can This Financial 'Skin-Deep' Game Replicate the SP 500 ETF's Rags-to-Riches Myth?

By: PRATHIK DESAI

Translated by: Saoirse, Foresight News

In the late 1980s, Nathan Most worked at the American Stock Exchange. He wasn't a banker or trader, but a physicist with years of experience in logistics, specializing in metal and commodity transportation. His focus wasn’t on financial instruments, but on practical systems.

At that time, mutual funds were the mainstream way for investors to gain broad market exposure. While they offered diversification, they suffered from trading delays—investors couldn't buy or sell during the trading day, and only learned their execution price after markets closed (a model still used today). For those accustomed to real-time stock trading, this lagging experience already felt outdated.

To address this, Nathan Most proposed a solution: create a product that tracks the S&P 500 Index but trades like an individual stock. Specifically, structurally package the entire index into a new instrument listed on exchanges. The idea was initially met with skepticism—the design logic of mutual funds differed fundamentally from stock trading, the legal framework didn't exist, and there seemed little demand.

Yet he pushed forward anyway.

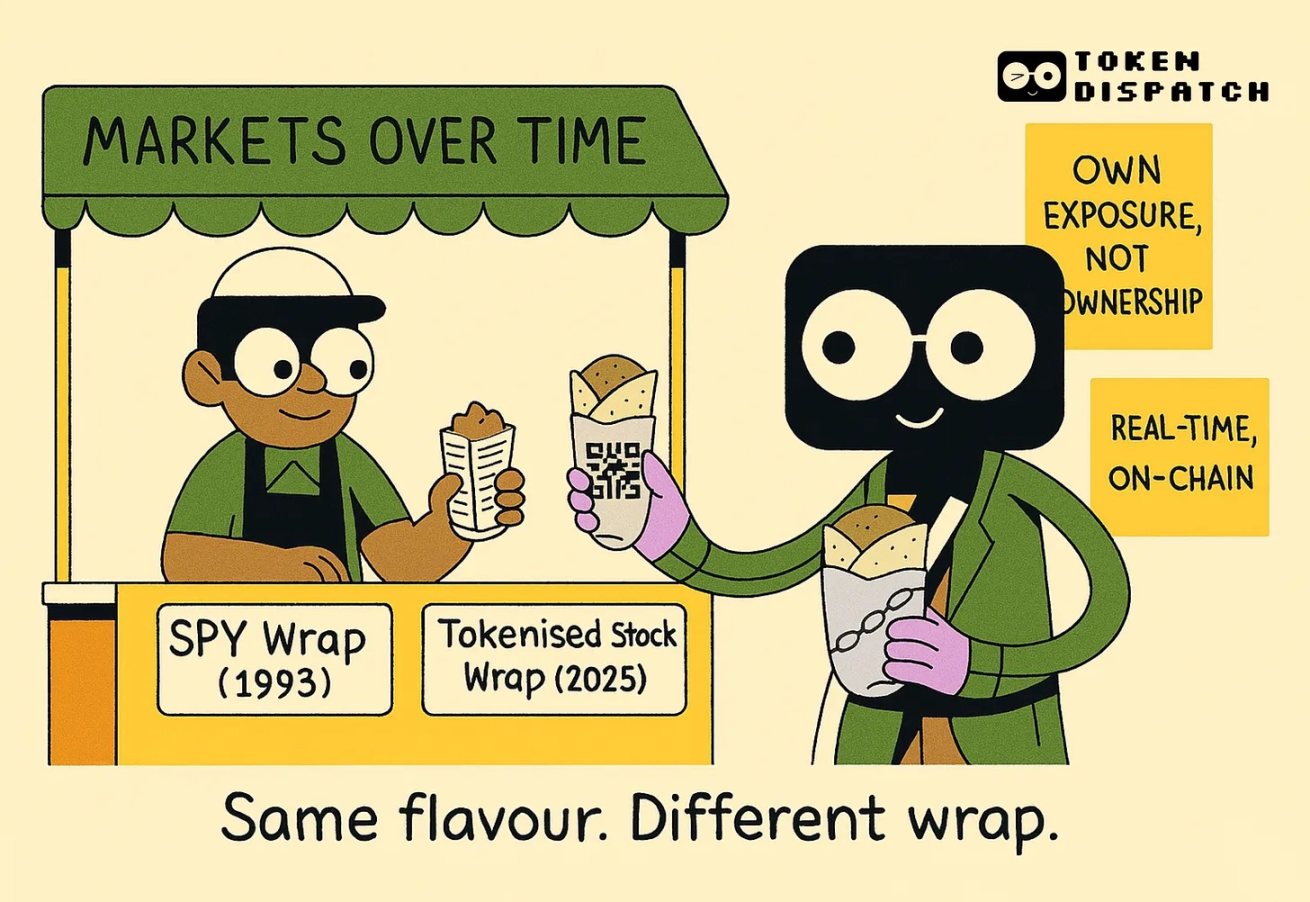

In 1993, the Standard & Poor's Depositary Receipt (SPDR), ticker symbol SPY, launched—a de facto first exchange-traded fund (ETF): an investment vehicle representing hundreds of stocks. Initially seen as niche, it gradually became one of the world’s most actively traded securities. On most trading days, SPY’s volume exceeds that of its underlying component stocks. This synthetic product achieved greater liquidity than its base assets.

Today, this history feels relevant again—not because another new fund has emerged, but due to transformations unfolding on blockchains.

Investment platforms such as Robinhood, Backed Finance, Dinari, and Republic are rolling out tokenized stocks. These blockchain-based assets aim to mirror share prices of companies like Tesla, NVIDIA, and even private firms like OpenAI.

Positioned as “exposure tools” rather than ownership certificates, holders aren’t shareholders and have no voting rights. This isn’t traditional equity purchase, but holding a token pegged to a stock’s price. That distinction is crucial—and controversial. OpenAI and Elon Musk have both expressed concerns about Robinhood’s tokenized offerings.

Robinhood CEO Tenev later clarified these tokens are meant to give retail investors access to otherwise hard-to-reach private assets.

Unlike company-issued equities, these tokens are created by third parties. Some platforms claim 1:1 backing via custody of actual shares; others are purely synthetic. Despite familiar trading experiences—matching price movements, brokerage-like interfaces—the underlying legal and financial foundations are often weaker.

Still, they attract certain investors, especially non-U.S. residents who can’t easily access U.S. markets. Imagine being in Lagos, Manila, or Mumbai wanting to invest in NVIDIA. Typically, you’d need a foreign brokerage account, meet high minimum deposit requirements, and endure long settlement cycles. Tokenized stocks eliminate these barriers. No wire transfers, no paperwork, no entry restrictions—just a wallet and a marketplace.

This investment channel may seem novel, but its mechanics echo traditional financial instruments. Yet real-world hurdles remain: most platforms—including Robinhood, Kraken, and Dinari—don’t operate in emerging markets outside U.S. equities. For Indian users, for example, it remains unclear whether buying such tokenized stocks is legally or practically feasible. If tokenized stocks are to broaden global market participation, challenges will extend beyond technology to include regulation, geography, and infrastructure.

How Derivatives Work

Futures contracts long enabled trading based on expectations without owning the underlying asset; options allow investors to bet on volatility, timing, or direction without buying shares. In each case, these tools serve as alternative pathways to access core assets.

Tokenized stocks follow similar logic. They don’t aim to replace traditional stock markets, but offer excluded populations a new way to participate.

New derivatives often evolve predictably: early confusion over pricing, traders wary of risk, regulators观望; then speculators enter, test boundaries, exploit inefficiencies; if proven useful, mainstream adoption follows, eventually integrating into market infrastructure. Index futures, ETFs, and even Bitcoin derivatives on CME and Binance followed this path. Originally playgrounds for speculators—fast, risky, flexible—they weren’t built for average investors.

Tokenized stocks may follow suit: retail investors start trading hard-to-access assets like OpenAI or pre-IPO companies; arbitrageurs spot price discrepancies between tokens and real shares and join in; if volume stabilizes and infrastructure improves, institutions may enter—especially in jurisdictions with clear compliance frameworks.

Early markets may look messy: low liquidity, wide bid-ask spreads, sudden weekend price jumps. But all derivative markets start imperfectly. They’re less perfect replicas than stress tests—ways to gauge demand before the actual asset adapts.

One interesting aspect—could be seen as strength or weakness depending on perspective—is the time gap.

Traditional markets have opening and closing hours. Most stock derivatives trade within those windows. But tokenized stocks play by different rules. Say a U.S. stock closes Friday at $130, then a major news event hits Saturday—like leaked earnings or geopolitical developments. While the stock market is closed, the token might already reflect the impact. Investors can thus price in off-hours information.

The time gap becomes problematic only when token trading volume significantly exceeds traditional volume. Futures handle this via funding rates and margin adjustments; ETFs rely on designated market makers and arbitrage mechanisms. But tokenized stocks lack such safeguards today—prices may diverge, liquidity may dry up, tracking accuracy depends entirely on issuer reliability.

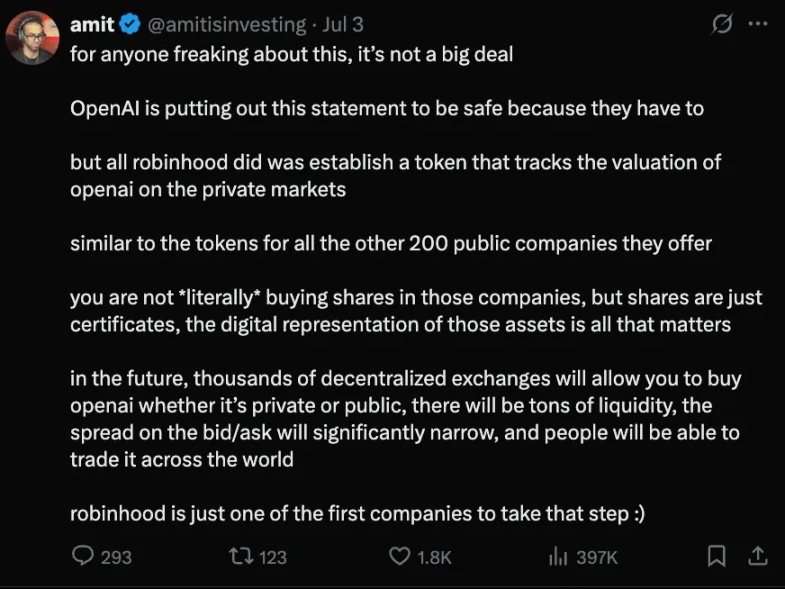

And that trust is shaky. When Robinhood launched OpenAI and SpaceX tokenized stocks in the EU, both companies denied involvement, stating they had no collaboration or formal ties.

This isn’t necessarily a flaw of tokenized stocks themselves, but raises a key question: what exactly are you buying? Price exposure—or a synthetic derivative with ambiguous rights and recourse?

To those anxious: relax. OpenAI issued that statement for caution—it had to. Robinhood simply launched a token tracking OpenAI’s private-market valuation, just like over 200 other company tokens on its platform. You're not buying real stock—but stocks are just certificates. The digital form of these assets matters more. Thousands of decentralized exchanges will emerge where you can trade OpenAI regardless of its public or private status. Liquidity will grow, spreads narrow, access globalize. Robinhood is just taking the first step~

Underlying architectures vary widely. Some tokens launch under European regulatory frameworks; others rely on smart contracts and offshore custodians. A few platforms like Dinari are attempting more compliant models, while most continue probing legal boundaries.

U.S. regulators haven’t taken a clear stance. Though the SEC has voiced views on token issuance and digital assets, tokenized versions of traditional stocks remain in a gray area. Platforms tread carefully—Robinhood, for instance, launched in the EU, not domestically.

But demand is evident.

Republic offers synthetic investments in private firms like SpaceX; Backed Finance packages public stocks and issues them on the Solana blockchain. These efforts are early but persistent, targeting participation barriers—not reengineering finance itself. Tokenized stocks won’t increase investment returns—that’s not their goal. Perhaps their sole ambition is simplicity: making participation easier for ordinary people.

For retail investors, accessibility often trumps everything. Viewed this way, tokenized stocks aren’t competing with traditional equities—they’re competing on ease of access. If investors can click a few times within a stablecoin app to gain exposure to NVIDIA’s price moves, they likely won’t care whether it’s synthetic.

This preference has precedent. SPY proved packaged products can dominate trading volumes. Contracts for difference (CFDs), futures, and options followed similar paths—initially tools for traders, later serving broader audiences.

Such derivatives often lead underlying assets in price action, capturing sentiment faster than sluggish traditional markets during volatility, amplifying fear or greed.

Tokenized stocks may follow the same trajectory.

Current infrastructure remains nascent—liquidity fluctuates, regulations unclear. But the core logic is clear: build something that reflects asset value, is easy to acquire, and appeals to everyday users. If this substitute stabilizes, more volume will flow in. Eventually, it won’t merely shadow the underlying asset—it could become the market signal.

Nathan Most never set out to reshape stock markets. He saw inefficiencies and sought smoother interactions. Today’s token issuers are doing the same—only replacing yesterday’s fund structures with smart contracts.

What remains to be seen is whether these new tools can maintain trust during market crashes. After all, they’re not real stocks, not regulated, just “stock-like instruments.” But for many far from traditional finance—or living in remote regions—being “close enough” may be sufficient.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News