Huobi Growth Academy | Cryptocurrency Market Macro Research Report: Opportunities Amid Monetary Policy Tug-of-War and Global Turmoil – Latest Outlook for the Second Half of the Year

TechFlow Selected TechFlow Selected

Huobi Growth Academy | Cryptocurrency Market Macro Research Report: Opportunities Amid Monetary Policy Tug-of-War and Global Turmoil – Latest Outlook for the Second Half of the Year

Systematically assess opportunities and risks in the cryptocurrency market for the second half of the year by integrating on-chain data with financial models.

1. Executive Summary

In the first half of 2025, the global macro environment remained highly uncertain. The Federal Reserve’s repeated pauses on rate cuts reflect a monetary policy now in a phase of "hesitant tug-of-war," while escalating geopolitical tensions—such as U.S.-Iran hostilities, Middle East energy corridor crises, and the destruction of Russian military aircraft—and tariff hikes under a Trump-led administration have further fractured global risk appetite structures. We analyze opportunities and risks in the crypto market for the second half of the year through five macro dimensions—interest rate policy, dollar credibility, geopolitics, regulatory trends, and global liquidity—integrating on-chain data and financial models, and propose three core strategic recommendations covering Bitcoin, stablecoin ecosystems, and DeFi derivatives.

2. Global Macro Review (First Half of 2025)

The first half of 2025 continued the pattern of multifaceted uncertainty that began in late 2024. Amid sluggish growth, persistent inflation, ambiguous Fed policy outlooks, and intensifying geopolitical tensions, global risk appetite contracted significantly. The dominant logic of macroeconomic and monetary policy has evolved from “inflation control” to “signal博弈” and “expectations management.” As a leading indicator of global liquidity shifts, the crypto market exhibited typical synchronous volatility within this complex backdrop.

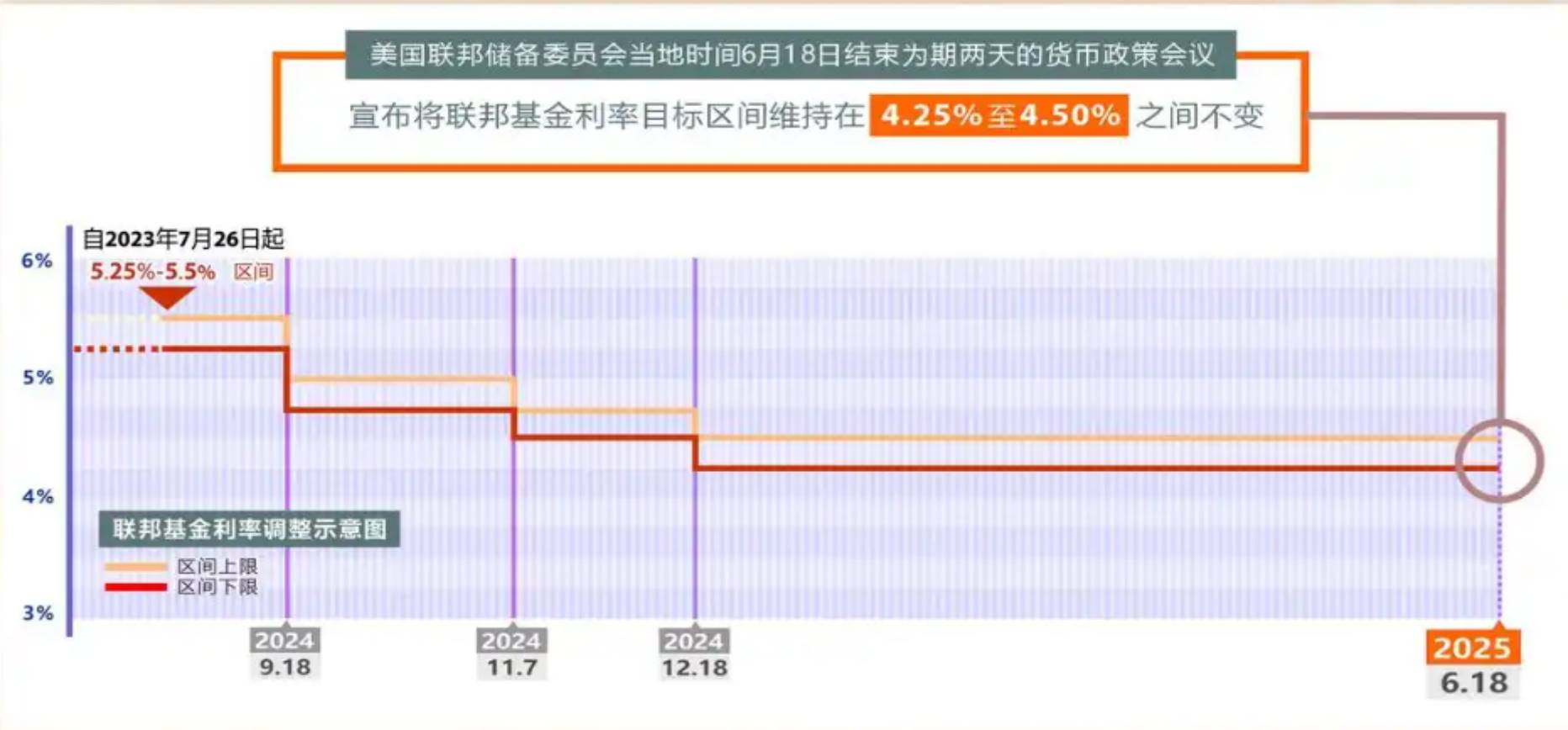

At the start of 2025, markets widely expected three rate cuts over the year, particularly following a clear decline in Q4 2024 PCE growth, fueling hopes for a soft-landing scenario ushering in a new easing cycle. However, this optimism was dashed at the March 2025 FOMC meeting. Although rates were held steady, the post-meeting statement emphasized that “inflation remains far from target” and highlighted ongoing tightness in the labor market. Subsequently, April and May saw CPI readings rebound above expectations (3.6% and 3.5%, respectively), with core PCE staying above 3%, underscoring the persistence of “sticky inflation.” Structural drivers—such as rigid housing rents, wage stickiness in services, and temporary energy price shocks—have not fundamentally abated.

Faced with renewed inflationary pressure, the Fed opted once again to “pause rate cuts” in June, lowering its projected number of 2025 cuts from three to two via the dot plot, with the year-end federal funds rate expected to remain above 4.9%. More critically, Chair Powell signaled during the press conference that the Fed had entered a “data-dependent, wait-and-see” phase—not the “confirmed easing cycle” many had anticipated. This marks a shift from directional guidance to timing-based management, significantly increasing policy path uncertainty.

Meanwhile, fiscal and monetary policies grew increasingly divergent. As the Trump administration accelerated its “strong dollar + strong borders” strategy, the U.S. Treasury announced in mid-May plans to “optimize debt structure” through various financial tools, including advancing regulatory frameworks for dollar-pegged stablecoins. The goal: leveraging Web3 and fintech products to inject liquidity into the global system without visibly expanding the balance sheet. These fiscally driven stabilization measures starkly contrasted with the Fed’s high-rate stance aimed at curbing inflation, complicating market expectations.

Trump’s tariff policy also emerged as a key driver of market turbulence. Starting in mid-April, the U.S. imposed new tariffs of 30%-50% on Chinese high-tech goods, EVs, and clean energy equipment, with threats of broader expansion. These moves went beyond trade retaliation—they reflected a strategic attempt to generate “imported inflation” pressures to force the Fed into cutting rates. In this context, the tension between dollar credibility and interest rate anchoring came to the forefront. Some market participants began questioning the Fed’s independence, triggering repricing in long-term Treasury yields. The 10-year yield briefly spiked to 4.78%, while the 2s-10s yield curve inverted again in June, reigniting recession fears.

Geopolitical escalation also materially impacted market sentiment. Ukraine’s successful destruction of a Russian TU-160 strategic bomber in early June triggered sharp rhetoric between NATO and Moscow. In the Middle East, a suspected Houthi attack on critical Saudi oil infrastructure at the end of May disrupted supply expectations, sending Brent crude above $130—the highest since 2022. Unlike in 2022, however, this round of geopolitical shocks did not lift Bitcoin or Ethereum. Instead, safe-haven capital flowed heavily into gold and short-term Treasuries, with spot gold briefly exceeding $3,450. This structural shift indicates that Bitcoin is still primarily viewed as a liquidity trading asset, not a macro-level safe haven.

From a global capital flow perspective, the first half of 2025 showed a clear “de-emerging market” trend. IMF data and JPMorgan cross-border capital tracking revealed that Q2 emerging market bond outflows hit the highest quarterly level since March 2020, while North American markets attracted relatively strong inflows due to ETF-driven stability. The crypto market was not immune. While Bitcoin ETFs recorded over $6 billion in net inflows year-to-date—demonstrating resilience—small-cap tokens and DeFi derivatives suffered massive capital outflows, revealing pronounced “asset stratification” and “structural rotation.”

In sum, the first half of 2025 unfolded within a deeply structural and uncertain environment: volatile policy expectations, fiscal attempts to extend dollar credit, recurring geopolitical shocks, capital repatriation to developed markets, and a restructured safe-haven landscape. This sets a complex stage for the second half. It is no longer simply about “whether rates will be cut,” but rather a multi-front battle involving the reconstruction of dollar credibility, competition for global liquidity dominance, and the integration of digital assets into the formal financial system. Within this struggle, crypto assets will seek structural opportunities amid institutional gaps and liquidity reallocation. The next phase will not reward all coins equally—it will favor investors who understand the macro framework.

3. Restructuring of the Dollar System and the Evolution of Cryptocurrencies

Since 2020, the dollar system has undergone its most profound structural transformation since the collapse of Bretton Woods. This restructuring is not driven by technical evolution in payment tools, but by instability in the global monetary order and a crisis of institutional trust. Amid the volatile macro environment of early 2025, dollar hegemony faces both internal imbalances in policy coherence and external challenges from multilateral currency experiments—shaping the market position, regulatory logic, and asset role of cryptocurrencies.

Internally, the biggest challenge to dollar credibility lies in the erosion of the Fed’s anchoring logic. For over a decade, the Fed operated as an independent inflation manager with clear, predictable rules: tighten when overheated, ease during downturns, prioritizing price stability. But in 2025, this logic is being undermined by the “strong fiscal, weak central bank” approach associated with the Trump administration. The Biden-era commitment to fiscal restraint and monetary independence has given way to a “fiscal-first” strategy, leveraging the dollar’s global dominance to export domestic inflation and indirectly pressure the Fed to align with fiscal cycles.

The clearest manifestation of this policy split is the Treasury’s growing influence over dollar internationalization—bypassing traditional monetary tools. For example, the Treasury’s May 2025 “Compliant Stablecoin Strategic Framework” explicitly supports issuing dollar-denominated assets on Web3 networks to achieve global spillover. This reflects a shift from a “financial state machine” to a “technological platform state,” aiming to build a “distributed monetary expansion capability” for the digital dollar—one that supplies liquidity to emerging markets without requiring central bank balance sheet expansion. This path integrates dollar stablecoins, on-chain Treasuries, and U.S. commodity settlement networks into a “digital dollar export system,” amplifying the dollar’s network effects in the digital realm.

Yet this strategy raises concerns about the blurring line between fiat and crypto. As dollar stablecoins like USDT and USDC strengthen their dominance in crypto trading, they are increasingly becoming “digital representations of the dollar” rather than “crypto-native assets.” Meanwhile, decentralized assets like Bitcoin and Ethereum are seeing declining relative weight in transaction systems. From late 2024 to Q2 2025, CoinMetrics data shows that USDT’s share of total trading volume on major exchanges rose from 61% to 72%, while BTC and ETH spot volumes declined. This liquidity shift signifies that the dollar system has partially “absorbed” the crypto market, making dollar stablecoins a new source of systemic risk.

Externally, the dollar system faces growing probing from multilateral currency initiatives. China, Russia, Iran, and Brazil are accelerating efforts in local-currency settlements, bilateral clearing agreements, and commodity-backed digital asset networks—all aimed at weakening dollar dominance and advancing de-dollarization. While no viable alternative to SWIFT yet exists, their “infrastructure substitution” strategy exerts marginal pressure on the dollar’s settlement network. For instance, China’s e-CNY is rapidly expanding cross-border payment links with Central Asia, the Middle East, and Africa, exploring CBDC use in oil and commodity trades. In this context, crypto assets find themselves caught between two competing systems, their “institutional affiliation” becoming increasingly ambiguous.

Bitcoin, as a unique variable in this dynamic, is shifting from a “decentralized payment tool” to a “sovereign-free anti-inflation asset” and a “liquidity channel within institutional gaps.” In the first half of 2025, Bitcoin was widely used in several countries to hedge against currency depreciation and capital controls—especially in Argentina, Turkey, and Nigeria. There, the grassroots “dollarization network” formed by BTC and USDT became a vital tool for risk hedging and value storage. On-chain data shows that in Q1 2025 alone, BTC inflows to Latin America and Africa via peer-to-peer platforms like LocalBitcoins and Paxful surged over 40% YoY, largely evading domestic central bank oversight and reinforcing Bitcoin’s role as a “gray-zone safe haven.”

However, precisely because Bitcoin and Ethereum remain outside national credit systems, their resilience under “policy stress tests” remains limited. In the first half of 2025, the SEC and CFTC intensified scrutiny of DeFi projects and anonymous protocols, launching new investigations into Layer 2 cross-chain bridges and MEV relays—prompting some capital to exit high-risk DeFi positions. This highlights that as the dollar system regains narrative control, crypto must redefine itself—not as a symbol of “financial independence,” but more likely as a tool for “financial integration” or “institutional arbitrage.”

Ethereum’s role is also evolving. As it advances toward becoming both a verifiable data layer and financial execution layer, its function is shifting from “smart contract platform” to “institutional access platform.” Whether issuing RWAs or deploying government- or enterprise-grade stablecoins, more and more entities are incorporating Ethereum into compliant architectures. Traditional institutions like Visa, JPMorgan, and PayPal have deployed infrastructure on Ethereum-compatible chains such as Base and Polygon, creating a “regulatory sandwich” with native DeFi ecosystems. This means Ethereum’s institutional role as “financial middleware” has been redefined—not by decentralization, but by institutional compatibility.

The dollar system is reclaiming dominance in digital assets through three paths: technological spillover, institutional integration, and regulatory penetration. Its goal is not to eliminate crypto, but to embed it within the “digital dollar world.” Bitcoin, Ethereum, stablecoins, and RWA assets will be reclassified, revalued, and re-regulated, forming a “Pan-Dollar System 2.0”—anchored in the dollar, settled on-chain. In this system, true crypto assets are no longer “rebels,” but “arbitrageurs in institutional gray zones.” Future investment logic will shift from “decentralization drives revaluation” to “whoever integrates into the dollar’s restructuring gains institutional dividends.”

4. On-Chain Data Insights: New Shifts in Capital Structure and User Behavior

The first half of 2025 revealed a complex picture of “structural accumulation intertwined with marginal recovery” in on-chain data. Long-term holder (LTH) ratios for Bitcoin hit record highs, stablecoin supply underwent significant repair, and while DeFi activity recovered, risk appetite remained cautious. These indicators reflect investor sentiment oscillating between caution and exploration, and a capital structure highly sensitive to policy rhythms.

The most telling structural signal is the sustained rise in Bitcoin’s long-term holder ratio. By June 2025, over 70% of Bitcoin had remained unspent for more than 12 months—a historical high. This growing LTH concentration signals not only enduring confidence among long-term investors, but also shrinking liquid supply, providing latent price support. According to Glassnode, Bitcoin’s holding-time distribution is shifting “rightward,” with increasing amounts locked for two, three, or more years. This behavior reflects more than just “HODL culture”—it reveals structural capital, including family offices and pension funds, now shaping BTC’s chain distribution. Correspondingly, short-term activity has declined. Lower on-chain transaction frequency and falling Coin Days Destroyed metrics confirm a shift from “high-frequency speculation” to “long-term allocation.”

This structural accumulation aligns closely with institutional behavior. Analysis of multisig wallets and entity addresses suggests that over 35% of Bitcoin is now controlled by large, concentrated addresses that have remained inactive since building positions in Q4 2023 or early 2024. Their presence has transformed the previous retail-driven, coin-denominated speculation model, laying the foundational chip structure for the next bull-bear cycle.

Meanwhile, the stablecoin market completed a clear bottom-recovery phase. From late 2024 to early 2025, USDC saw five consecutive months of market cap decline due to Fed tightening and BSA regulatory uncertainty. But in Q2 2025, USDC resumed growth, reaching $62 billion by June—matching USDT’s pace. This rebound wasn’t isolated, but part of broader ecosystem expansion. Paxos’ USDP and Ethena’s USDe posted strong growth, collectively adding over $3 billion in new supply. Crucially, this expansion was driven more by real-world economic activity than past patterns of yield farming or pure speculation.

Rising on-chain activity confirms stablecoins are returning to their core function—not just as “counterparty assets” on exchanges, but as genuine “payment and transfer tools” among users. On Base chain, for example, monthly active USDC addresses rose 41% QoQ in Q2 2025—outpacing Ethereum mainnet and Tron—highlighting more native, frequent usage within L2 ecosystems. Cross-chain flows also surged: stablecoin transfers via Wormhole and LayerZero peaked in May, indicating capital is seeking efficient deployment routes, not just arbitrage profits. This reinforces the long-term trend of crypto moving toward multi-chain integration with real-world use cases.

Compared to Bitcoin and stablecoins’ “structural rebalancing,” DeFi on-chain data shows a more nuanced “recovered activity with risk neutrality.” In the first half of 2025, decentralized derivatives and perpetual contract platforms outpaced other sub-sectors in activity. Platforms like Abstract, Aevo, and Hyperliquid saw rapid growth in user transactions and contract interactions. Aevo briefly surpassed $1.5 billion in daily volume in May; Abstract’s DAU grew over 60% YoY—evidence of continued demand for low-barrier, high-leverage speculative instruments. Yet beneath this heat lies a reality of low capital utilization. While TVL rose across platforms, average leverage and open interest failed to grow proportionally, suggesting participants are testing the waters but avoiding systemic leverage buildup. This contradiction signals a core truth: while market interest is rising, risk appetite remains suppressed—investors are in a “wait-for-clarity” strategic pause.

Combining Bitcoin’s structural accumulation, stablecoin supply recovery, and DeFi’s risk-averse capital dynamics, the first half of 2025 reveals a crypto market at a complex inflection point: “chip restructuring – compressed expectations – marginal recovery.” Capital structure is shifting from the hot-money dominance of 2023–2024 to a hybrid model—structurally anchored, tactically active. User behavior continues to oscillate between short-term speculation and long-term allocation. Under this structure, sustained one-way rallies remain unlikely in the near term. But once macro clarity emerges—such as a confirmed Fed easing cycle, breakthroughs in stablecoin regulation, or fresh ETF inflows—this pent-up structure could rapidly unleash bullish momentum. Thus, despite surface calm, on-chain data harbors powerful undercurrents—key indicators for anticipating market elasticity and turning points in the second half.

5. Outlook and Strategic Recommendations for the Second Half of 2025

Looking ahead to the second half of 2025, the crypto market approaches a critical inflection point shaped by macro and structural convergence. The key variables are no longer isolated price moves or niche narratives, but the dynamic interplay among multiple macro trajectories, institutional certainty, and on-chain structural shifts. Based on current policy and on-chain signals, the market is nearing a “repricing window”—where revised policy expectations, real interest rate reassessment, and recalibrated risk pricing will define market volatility and trends over the next 6–9 months.

From a macro policy standpoint, the Fed’s rate path and marginal changes in dollar liquidity will remain overarching determinants. The current consensus—“delayed and slow cuts”—is now widely priced in. However, as the U.S. labor market shows signs of loosening, corporate investment wanes, and CPI/PCE hint at deflationary pressures, the probability of the Fed entering a “symbolic” or even “preemptive” easing phase rises. Should the Fed deliver its first cut—however modest (e.g., 25 bps)—between mid-year and early Q3, it could trigger a strong emotional amplification effect in crypto markets. Historically, in early stages of liquidity expansion, crypto assets tend to outperform traditional risk assets due to their nature as “pure liquidity vehicles.” Therefore, once a rate cut signal is confirmed, we may see a replay of the 2020 Q3 playbook: “core assets rise first, followed by thematic rotation.”

Yet risks remain. Uncertainty from the global political cycle will continue to cloud asset pricing. The U.S. presidential election, European Parliament realignment, financial decoupling between Russia and the West, and renewed U.S.-China trade tensions could all cause temporary disruptions to risk appetite and capital flows. Should Trump win the election, his extreme policy inclinations—tech regulation, weaponization of the dollar, strategic Bitcoin reserves—might offer short-term crypto tailwinds. But these come with heightened geopolitical shocks and financial decoupling risks, potentially triggering a global “risk re-rating.” Thus, the second half will be defined by a “divergence” between mildly accommodative macro conditions and highly uncertain geopolitics, resulting in a “pulse rally – policy suppression – structural rotation” pattern of volatile upward movement.

Structurally, this market cycle is entering a later phase characterized by “ETF-driven flows, stabilizing on-chain structure, and slowing thematic rotation.” Bitcoin spot ETFs have become the primary source of incremental capital, with their net inflow rhythm almost directly dictating BTC price trends. While ETF inflows slowed in May and June, the long-term trend remains intact, reflecting institutional investors waiting for better entry points. Meanwhile, on-chain structure is stabilizing. Reduced liquidity from LTH-dominated holdings, recovering stablecoin usage for payments and deployments, and sustained DeFi expansion under low leverage all point to a more resilient internal system. If supported by favorable macro conditions, the release of structural elasticity could surpass previous speculation-driven cycles.

Notably, thematic rotation is slowing. From late 2024 to early 2025, AI+Crypto, RWA, and Meme2.0 successively captured market attention and capital. But in the latter half of 2025, capital efficiency into theme projects has declined sharply—narratives take longer and deliver smaller price impacts. Investor patience for hype is waning; empty storytelling is no longer sustainable. This implies that structural opportunities in the second half will center on “narrative validation with real-world support”: tangible AI protocol user growth, sustained improvement in Bitcoin on-chain metrics, or unexpected stablecoin (e.g., USDC, USDe) circulation data—only these can drive mid-term momentum.

Tactically, portfolio allocation should emphasize “alignment of structure and timing.” Bitcoin remains the most certain core asset. Its long-term thesis is unchanged—investors should maintain dual-track exposure via ETFs and cold wallets to capture its “digital gold” revaluation during rate cuts. Ethereum offers tactical optionality but risks alpha erosion if on-chain innovation stalls. Focus instead on sub-sectors combining “liquidity + new narrative,” such as RWA derivative protocols or L2 stablecoin growth. High-speed blockchains like Solana and TON offer valuation recovery potential, but participation should be tightly managed to mitigate risks from potential liquidity drawdowns.

In addition, consider allocating a small portion of capital to strategically capture secondary momentum in meme assets. While meme narratives have weakened, short-term sentiment trades fueled by X platform traffic and liquidity resonance still present opportunities. For those monitoring on-chain flows, combining data on SocialFi, cross-chain bridge volume, and whale address movements can enable light-weight, intraday or weekly tactical plays. Risk management is essential—meme allocations should not exceed 10% of total portfolio value.

Finally, from an institutional and strategic research perspective, the second half of 2025 favors a “defensive bull framework” over aggressive bullish expectations. While upside momentum exists, external variables are too complex—any policy shift, war shock, or regulatory reversal could reverse the trend. Therefore, focus on three key leading indicators for potential market inflection: First, shifts in the Fed’s policy path and dot plot—do they signal sustained rate cuts? Second, whether ETF inflows resume strength, particularly if daily net inflows return above $500 million. Third, on-chain circulation and activity trends for stablecoins (especially USDC and USDe)—can they sustain monthly growth and surpass 2024 highs? When all three converge, it would confirm a transition into a “trend re-pricing phase,” potentially accelerating the upward trajectory.

The second half of 2025 will mark a mid-cycle recovery phase transitioning from structural consolidation to policy-driven momentum. While not a one-way bull run, the confluence of macro easing, on-chain optimization, and rotational repair provides a strategic foundation for a “slow breakout within range-bound consolidation.” The key lies in whether investors can decode the rhythm of macro changes, anchor to on-chain trends, and thereby construct high-probability, long-term strategies amid volatility and stalemate.

6. Conclusion

In 2025, the crypto market enters a new cycle defined by institutional博弈 and liquidity restructuring. We recommend adopting “finding structural opportunities within defense” as the core strategy, capturing new alpha paths arising from the重构 of U.S. monetary tools and the revival of U.S.-China capital arbitrage chains. Patience will be the strongest strategy this year; understanding institutions will be the true skill to survive the cycle.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News