Can the token price support the stock price as Strategy gains popularity?

TechFlow Selected TechFlow Selected

Can the token price support the stock price as Strategy gains popularity?

The companies that will survive are those leveraging this window to create enduring value beyond their cryptocurrency holdings.

Author: Saurabh Deshpande

Translation: TechFlow

Hello!

Newton is famous for discovering gravity, but in his time, he was more deeply obsessed with another pursuit: the alchemy of finance—essentially, trying to turn lead into gold. This fascination even led him into theological studies. Modern finance seems to echo his interests—through financial engineering, we’re now in an era where “turning lead into gold” is possible by simply combining the right elements.

In today’s article, Saurabh unpacks how companies are achieving premium valuations by adding cryptocurrencies to their balance sheets. Take MicroStrategy, for example—a company with quarterly revenue just over $100 million, yet holding nearly $10.9 billion worth of Bitcoin. Globally, 80 companies are exploring ways to include crypto on their balance sheets. Traditional financial institutions are showing strong interest and paying a premium for the volatility and potential returns these stocks offer.

Saurabh also analyzes the rise of convertible bonds, the financial instruments fueling this booming ecosystem, while discussing the risks involved and other companies attempting to add various cryptocurrencies to their balance sheets.

Let’s dive in!

A software/business intelligence company with only $111 million in quarterly revenue has a market cap of $109 billion. How is that possible? The answer: it used other people’s money to buy Bitcoin. And now, the market is assigning a 73% premium to its Bitcoin holdings. What exactly is this “alchemy”?

MicroStrategy (now called Strategy) has created a financial mechanism allowing it to borrow almost at zero cost to purchase Bitcoin. Consider its $3 billion convertible bond issuance in November 2024—the structure works as follows:

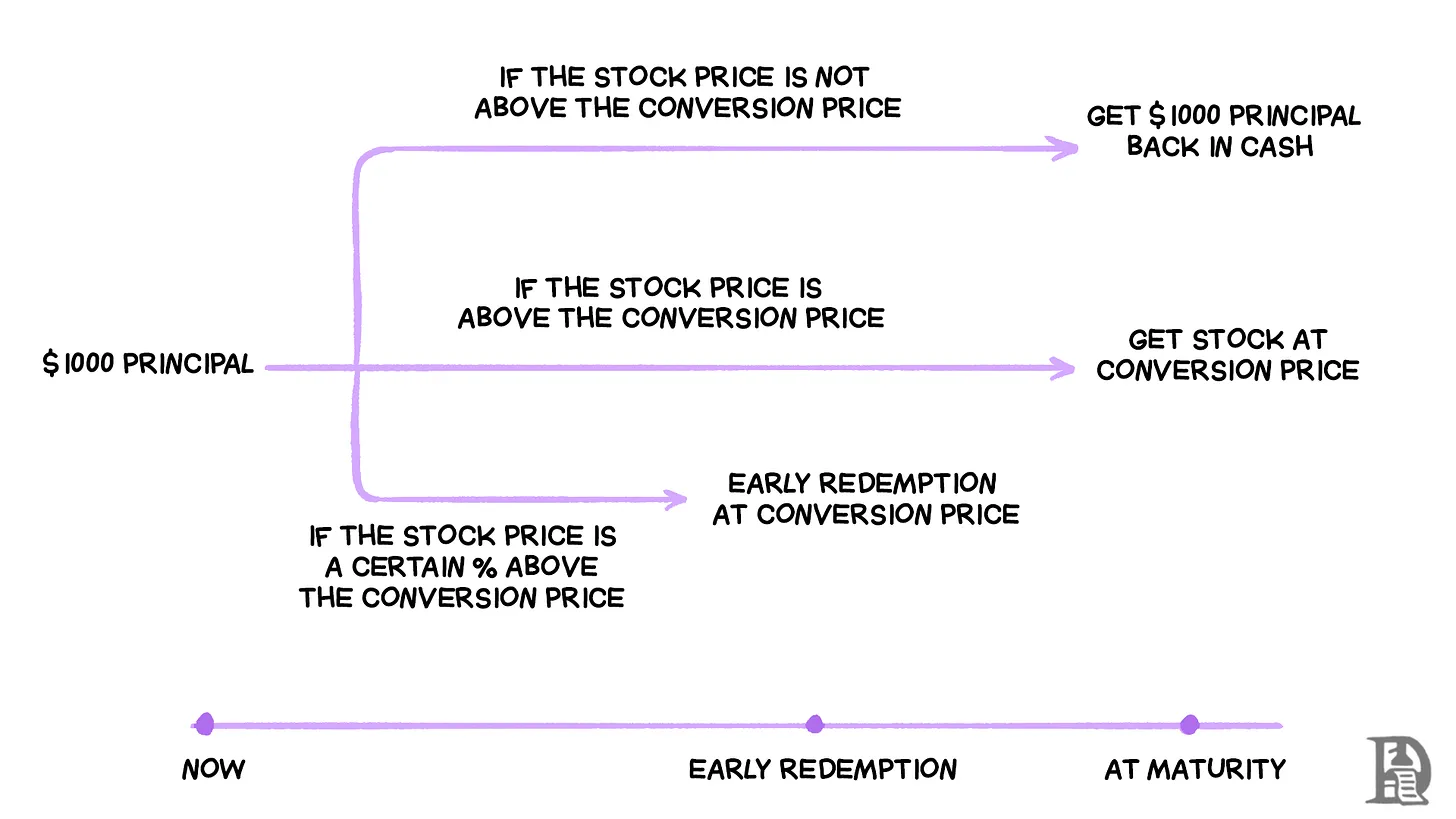

The company issued 0% coupon convertible bonds, meaning bondholders receive no periodic interest payments. Instead, each $1,000 bond can be converted into 1.4872 shares of Strategy stock—but only if the share price rises to $672.40 or higher before maturity.

At issuance, Strategy’s stock traded at $433.80, so the price needed to climb 55% for conversion to become profitable. If the stock never reaches that level, bondholders get their $1,000 back after five years. But if Strategy’s stock surges—typically when Bitcoin rises—bondholders can convert into equity and capture all the upside.

The brilliance lies here: bondholders are effectively betting on Bitcoin’s performance while enjoying downside protection not available from direct Bitcoin ownership. If Bitcoin crashes, they still get their principal back, since bonds rank above equity in bankruptcy. Meanwhile, Strategy borrows $3 billion at zero cost and immediately uses it to buy more Bitcoin.

The key trigger in this mechanism comes starting December 2026—just two years after issuance. If Strategy’s stock trades above $874.12 (130% of the conversion price) for a sustained period, the company can force early redemption of the bonds. This “call provision” means that if Bitcoin drives the stock high enough, Strategy can compel bondholders to either convert or allow the company to refinance under better terms.

This strategy works because Bitcoin has delivered about 85% average annual growth over the past 13 years, and 58% over the past five. The company bets Bitcoin’s growth will far outpace the 55% stock appreciation required for conversion. They’ve already proven success by redeeming earlier bonds ahead of schedule, saving millions in interest expenses.

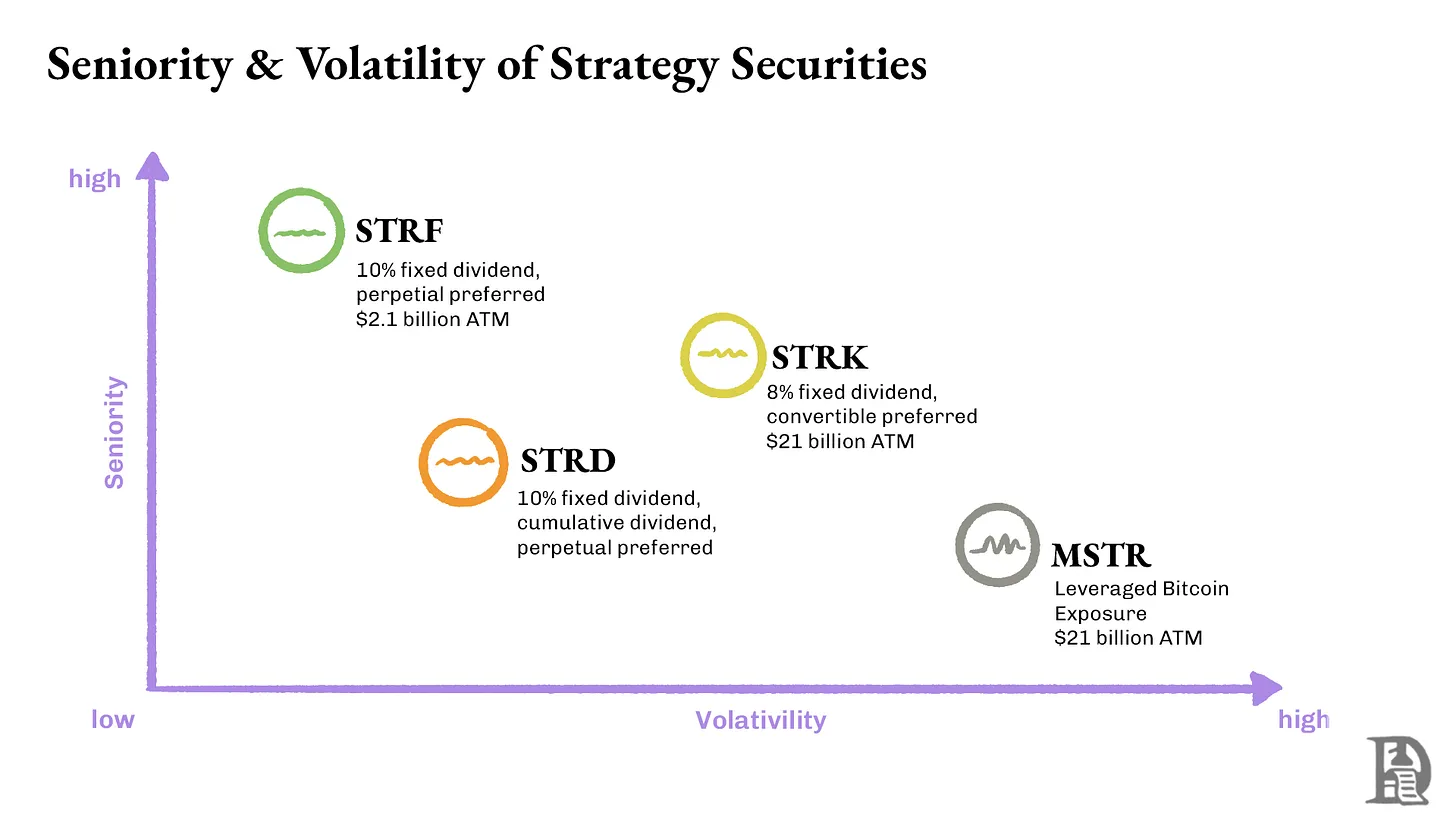

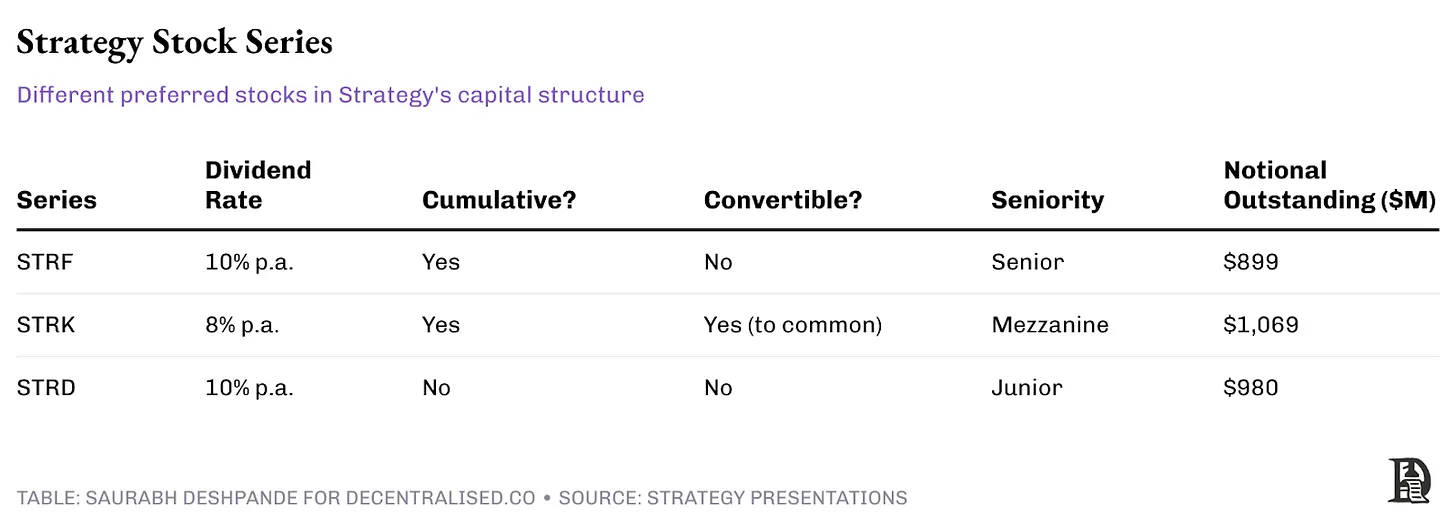

At the core of this structure are three distinct series of perpetual preferred stock—STRF, STRK, and STRD—each tailored to different types of investors.

STRF: Perpetual preferred stock offering a 10% cumulative dividend with the highest priority. If Strategy fails to pay dividends, it must settle all unpaid STRF dividends before paying any other shareholders. Additionally, the dividend rate increases as a penalty.

STRK: Perpetual preferred stock with an 8% cumulative dividend and medium priority. Unpaid dividends accumulate and must be fully settled before common shareholders receive anything. STRK also includes the right to convert into common stock.

STRD: Perpetual preferred stock offering a 10% non-cumulative dividend, lowest in priority. The higher dividend compensates for greater risk—if Strategy skips a payment, those dividends are permanently lost with no make-up obligation.

These perpetual preferred shares allow Strategy to raise equity-like capital while paying bond-like perpetual dividends. Each series is custom-designed for investor risk appetite. Cumulative dividends protect STRF and STRK holders, ensuring eventual receipt of all missed payments, while STRD offers higher current yield without safeguards on skipped dividends.

Strategy’s Track Record

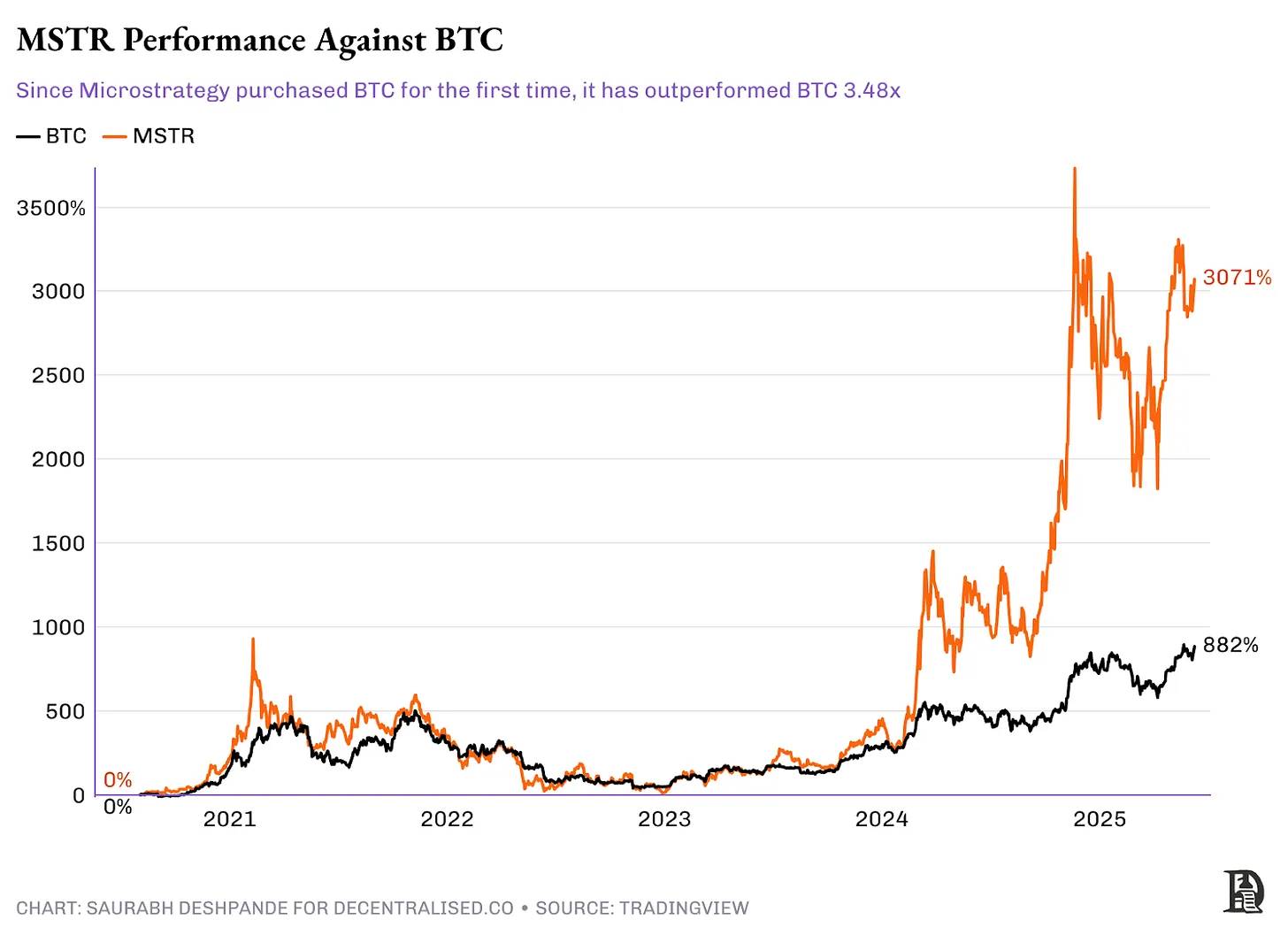

MicroStrategy began raising funds to buy Bitcoin in August 2020. Since then, Bitcoin has risen from $11,500 to $108,000—an approximately ninefold increase. Over the same period, MicroStrategy’s stock climbed from $13 to $370—nearly a 30x gain.

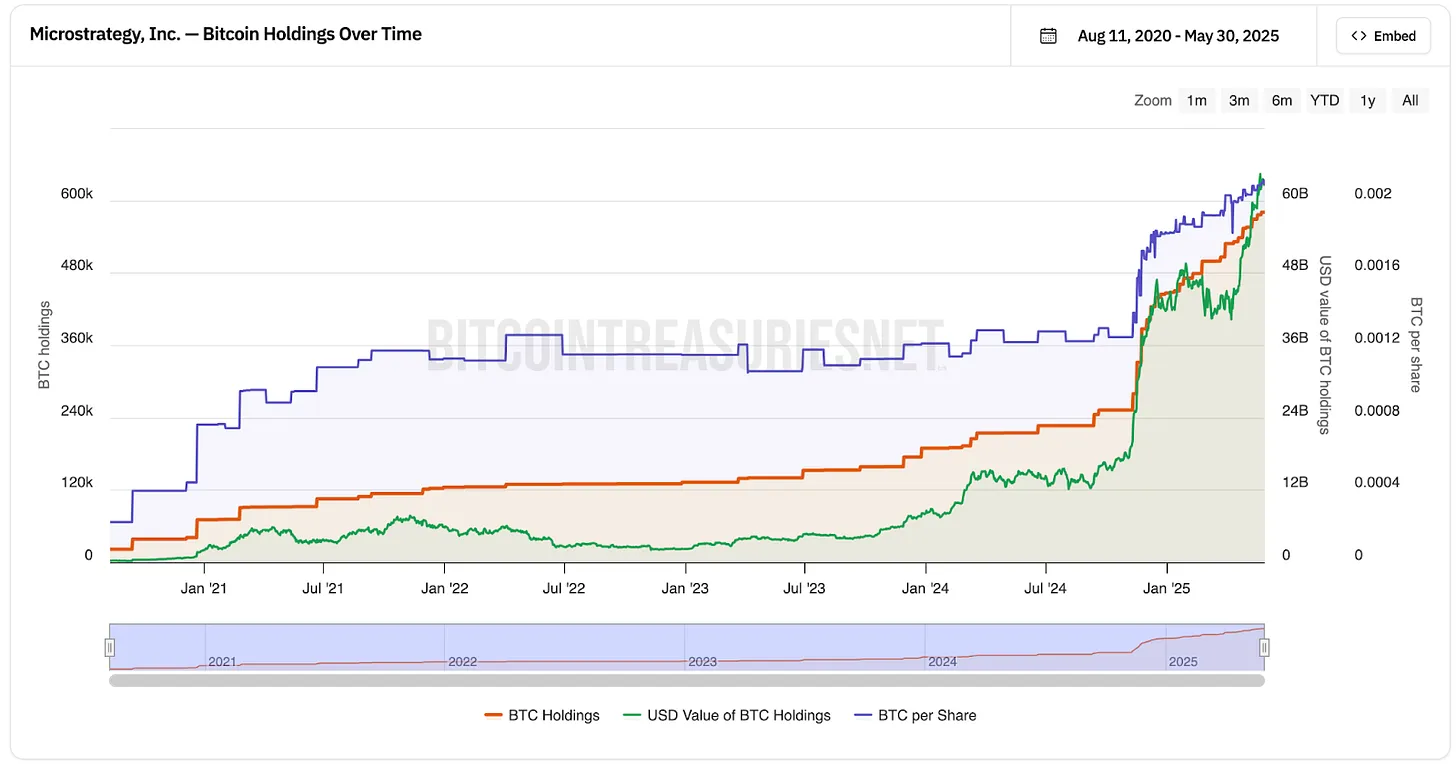

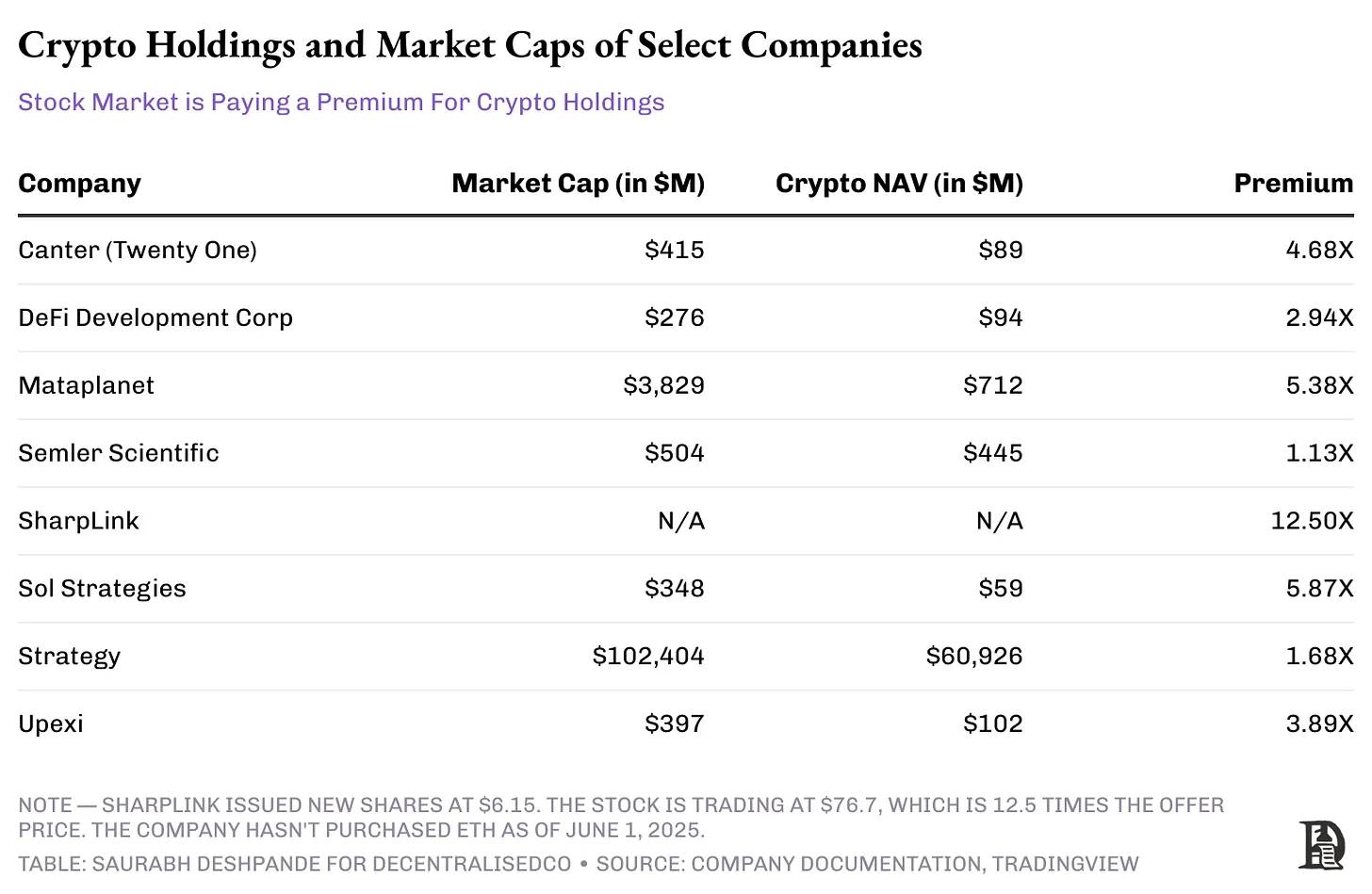

Notably, MicroStrategy’s core business has seen no growth. Its quarterly revenue remains flat between $100 million and $135 million, unchanged from before. The only difference is borrowing to buy Bitcoin. Today, it holds 582,000 BTC, valued at around $63 billion. Its market cap stands at approximately $109 billion—73% above the actual value of its Bitcoin holdings. Investors are paying a significant premium just for indirect exposure to Bitcoin via MicroStrategy shares.

Source: bitcointreasuries.net

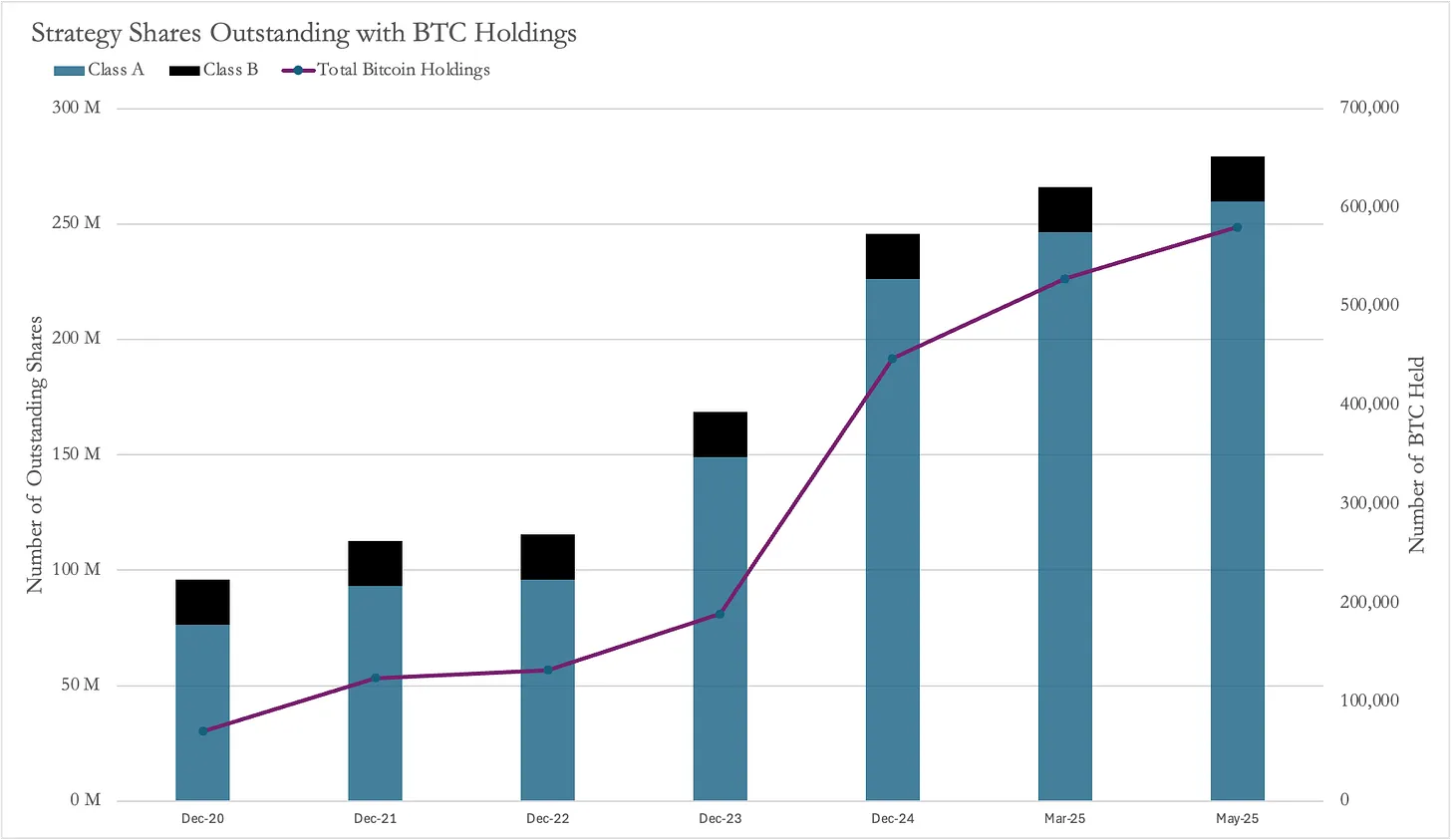

As previously mentioned, MicroStrategy funded its Bitcoin purchases by issuing new shares. Since it began buying, the number of outstanding shares has nearly tripled—from 95.8 million to 279.5 million, a 191% increase.

Source: MicroStrategy filings

Normally, such massive share issuance would dilute existing shareholders. Yet despite a 191% increase in shares, the stock price surged 2,900%. This means that although individual ownership stakes shrank, the value per share rose dramatically—leaving shareholders overall better off.

The MicroStrategy Model Goes Viral

Several companies have begun copying MicroStrategy’s playbook by holding Bitcoin as corporate assets. One recent example is Twenty One (XXI), a SPAC led by Jack Mallers, backed by Brandon Lutnick (son of U.S. Commerce Secretary)—Cantor Fitzgerald, Tether, and SoftBank. Unlike MicroStrategy, Twenty One is not publicly listed. The only public-market access is through Cantor Equity Partners (CEP), which invested $100 million for a 2.7% stake in XXI.

Twenty One holds 37,230 BTC. Since CEP owns 2.7% of XXI, it effectively controls about 1,005 BTC—worth roughly $108.5 million at $108,000 per BTC.

Yet CEP’s market cap is a staggering $486 million—4.8 times its underlying Bitcoin value! After the Bitcoin link was announced, CEP’s share price jumped from $10 to around $60.

This massive premium implies investors are paying $433 million for $92 million worth of Bitcoin exposure. As more such companies emerge and grow their Bitcoin holdings, market forces will eventually bring these premiums down to more reasonable levels—though no one knows when that will happen, or what “reasonable” actually means.

An obvious question arises: why do these companies command premiums? Why are investors willing to pay extra for their shares instead of simply buying Bitcoin directly? The answer may lie in “optionality.” Who is funding MicroStrategy’s Bitcoin purchases? Primarily hedge funds using convertible bond trades to execute “risk-free arbitrage” (delta-neutral strategies).

If you think about it, this setup closely resembles Grayscale’s Bitcoin Trust (GBTC). In the past, GBTC traded at a premium to Bitcoin because it was closed-ended (investors couldn’t withdraw Bitcoin until it became an ETF).

Investors would deposit Bitcoin into Grayscale and sell the publicly traded GBTC shares. As noted earlier, MicroStrategy’s bondholders enjoy an effective compound annual growth rate (CAGR) exceeding 9%.

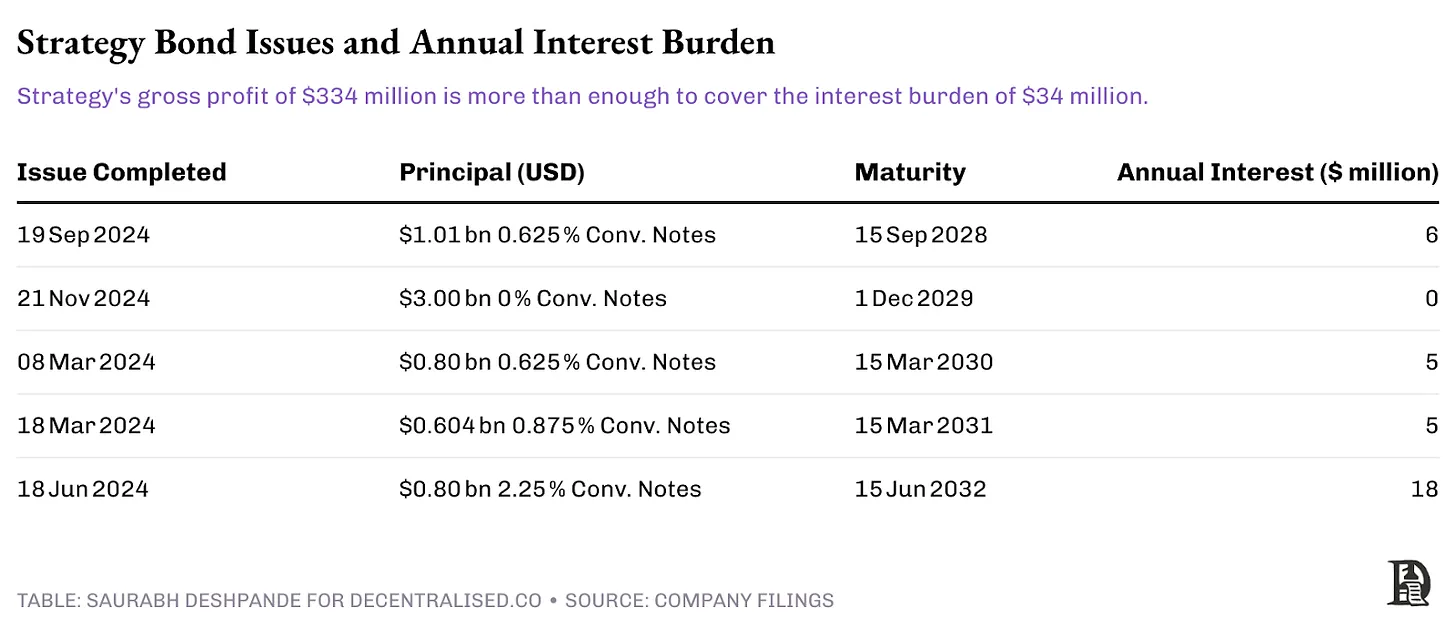

But how risky is this? MicroStrategy’s total annual interest burden is $34 million, while its gross profit in FY2024 was $334 million—more than sufficient to cover debt. The company issues convertible bonds aligned with Bitcoin’s four-year cycle, with maturities long enough to mitigate downside risk. So long as Bitcoin rises over 30% within four years, new share issuances can easily fund redemptions.

When redeeming these convertibles, MicroStrategy can simply issue new shares to bondholders. Bondholders receive payment based on a reference stock price set 30–50% above the original issuance price. This only becomes problematic if the stock price falls below the conversion price. In that case, MicroStrategy must repay in cash—either by refinancing under better terms or by selling some Bitcoin.

Value Chain

This process clearly starts with companies acquiring Bitcoin, but ultimately relies on exchanges and custodians. For instance, MicroStrategy is a client of Coinbase Prime, purchasing Bitcoin through Coinbase and storing it across Coinbase Custody, Fidelity, and its own multi-sig wallets. While it's hard to precisely estimate how much Coinbase earns from MicroStrategy’s execution and storage, we can make educated guesses.

Assume Coinbase charges 5 basis points for OTC trades executed on MicroStrategy’s behalf. Buying 500,000 BTC at an average price of $70,000 generates $17.5 million in execution fees. Custodians typically charge 0.2% to 1% annually. Assuming the lower end, storing 100,000 BTC at $108,000 generates $21.6 million per year in custody fees.

Beyond BTC

To date, financial instruments designed to provide exposure to Bitcoin (BTC) in capital markets have performed well. In May 2025, SharpLink raised $425 million through a PIPE (private investment in public equity) round led by ConsenSys founder Joe Lubin, who also became Executive Chairman. The financing issued ~69 million new shares at $6.15 each, with proceeds used to buy ~120,000 ETH and potentially stake them. Currently, ETH ETFs are not allowed to stake.

This structure offering 3%-5% yield is more attractive than standard ETFs. Prior to the announcement, SharpLink traded at $3.99 with a market cap of ~$2.8 million and only 699,000 shares outstanding. The issuance priced at a 54% premium. After the news, its share price briefly spiked to $124.

Notably, the newly issued 69 million shares represent about 100x the prior float.

Another company, Upexi, plans to acquire over 1 million Solana (SOL) tokens by Q4 2025 while remaining cash-flow neutral. The plan began with a private placement led by GSR, where Upexi raised $100 million by selling 43.8 million shares. Upexi expects to fund preferred dividends and future SOL purchases using 6%-8% staking yields and MEV (Maximal Extractable Value) rebates. On the day of the announcement, its stock jumped from $2.28 to $22, later settling around $10.

Prior to fundraising, Upexi had 37.2 million shares outstanding, so the new issuance diluted existing shareholders by about 54%. However, the nearly 400% surge in share price more than offset the dilution.

Sol Strategies is another firm raising capital to buy SOL. It operates Solana validator nodes, with over 90% of revenue coming from staking rewards. It currently stakes 390,000 SOL, with another ~3.16 million SOL delegated by third parties. In April 2025, Sol Strategies entered a convertible bond agreement with ATW Partners, securing up to $500 million in financing, with the first $20 million used to purchase 122,524 SOL.

Recently, Sol Strategies filed a shelf registration, planning to raise another $1 billion through common stock (“at-the-market” offerings), warrants, subscription receipts, units, debt securities, or any combination—providing significant financing flexibility.

Unlike MicroStrategy’s convertible bond model, SharpLink and Upexi raised capital by directly issuing new equity. In my view, MicroStrategy’s approach better serves different investor groups. Investors seeking indirect exposure via stocks take on additional risks—for example, intermediaries may leverage beyond their risk tolerance. Therefore, unless there's added service value, the convertible bond model—with sufficient operating profits to buffer interest payments—is more sustainable.

When the Music Stops

These convertible bonds primarily target hedge funds and institutional bond traders seeking asymmetric risk-reward profiles—not retail investors or traditional equity funds.

From their perspective, these instruments offer “heads I win big, tails I lose little”—a perfect fit for their risk frameworks. If Bitcoin delivers the expected 30%-50% gains over two to three years, they convert; if the market falters, they still get 100% principal back (though possibly eroded by inflation).

The advantage lies in solving real problems for institutional investors. Many hedge funds and pension funds lack the infrastructure to hold crypto directly or face investment mandates prohibiting Bitcoin ownership. These convertibles offer a compliant “backdoor” into crypto markets while maintaining the downside protection required of fixed-income assets.

But this edge is temporary. As regulation clarifies and more direct crypto investment vehicles emerge—such as custodial solutions, regulated exchanges, and clearer accounting standards—the need for these complex workarounds will fade. The 73% premium investors currently pay for Bitcoin exposure via MicroStrategy could shrink as simpler alternatives appear.

We’ve seen this before. Opportunistic managers once exploited GBTC’s premium—buying Bitcoin, depositing it into Grayscale, then selling GBTC shares at 20%-50% above NAV. But as more players copied the move, by late 2022, GBTC flipped from peak premium to a record 50% discount. This cycle shows that stock plays backed solely by crypto assets—and lacking sustainable earnings to support repeated financings—will eventually be arbitraged away.

The key question is: how long can this last, and who will survive when the premium collapses? Companies with strong fundamentals and conservative leverage may weather the shift. Those without durable income streams or competitive moats—relying purely on crypto asset accumulation—could face heavy selling pressure post-dilution once speculation fades.

For now, the music is still playing, and everyone is dancing. Institutional capital is flooding in, premiums are expanding, and more companies announce crypto asset strategies every week. But smart investors know this is a trade, not a long-term investment thesis. The survivors will be those using this window to build lasting value beyond mere crypto holdings.

The transformation in corporate treasury management may be permanent. But the extraordinary premiums we see today? Not so much. The real question is: are you positioned to profit from this trend—or just another player hoping to find a seat when the music stops?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News