The Battle for Full-Chain Stablecoins: Circle, Tether, and Frax's Digital Dollar Gambit

TechFlow Selected TechFlow Selected

The Battle for Full-Chain Stablecoins: Circle, Tether, and Frax's Digital Dollar Gambit

If you launch an attack against the king, you'd better not miss.

Author: jin, crypto KOL

Translation: Felix, PANews

If you ignore this struggle, others will set the rules that govern your money. Most people may not realize it, but we’re witnessing the largest on-chain power struggle in recent years.

"The Ambassadors" by Hans Holbein (1533)

In Hans Holbein’s 1533 masterpiece "The Ambassadors," two powerful figures stand confidently, surrounded by the cutting-edge technology of their time.

On the left is inherited power and global influence: royalty.

On the right is institutional authority and structure: a bishop, symbolizing officialdom.

Between them lies an alchemist’s table—featuring globes, sundials, and scientific instruments—symbolizing their attempt to mechanize and control complex innovation.

But Holbein hid a warning. At their feet, distorted and visible only from a specific angle, is a massive human skull. The skull foreshadows rupture: beneath calm appearances, a high-stakes conflict lurks, ready to upend order.

Today, the same drama unfolds in the world of digital currency.

The battle for omnichain stablecoins is a clash among three forces: the reigning monarch with a vast global empire (Tether's USDT); the institutional player selling architecture and compliance (Circle's USDC); and the disruptive alchemist—the idea and technology of “omnichain” itself—that both breaks and threatens the balance between the two. This is the story of that conflict—a war for control over the digital dollar where everything seems at stake.

Omnichain War: The Fight for the One True Dollar

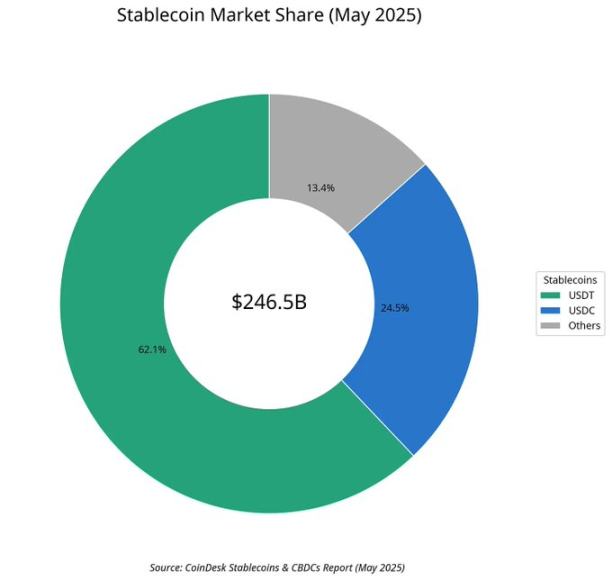

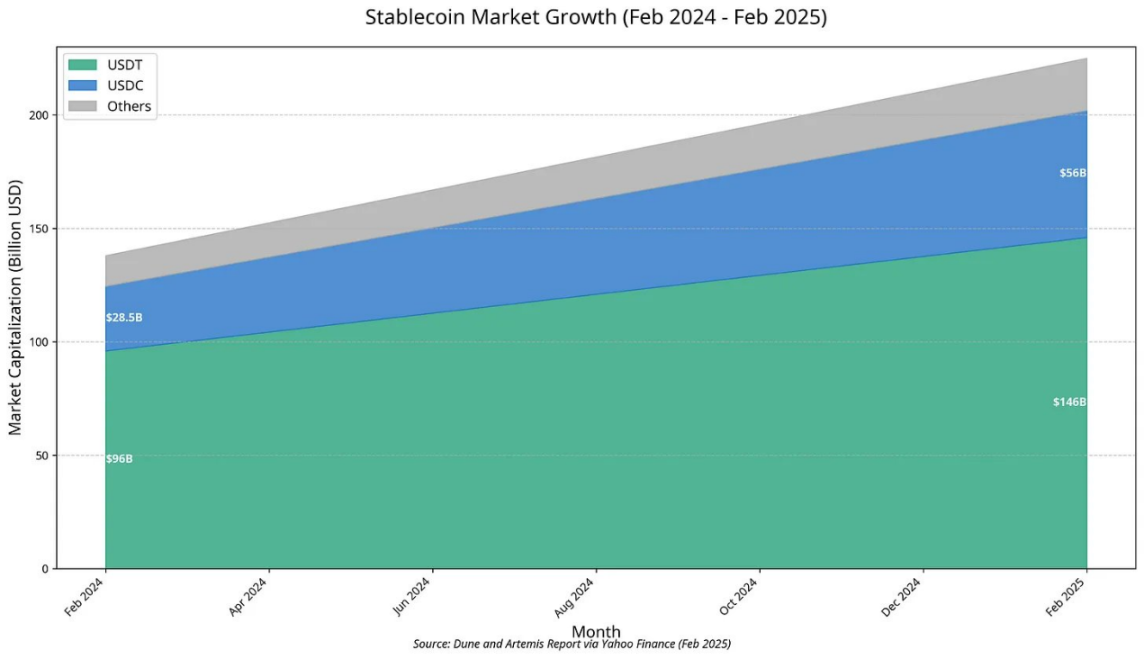

In 2024, an invisible financial empire processed more transactions than Visa. At its core stands Tether’s USDT, a $144 billion kingdom with one fatal flaw.

As Niccolò Machiavelli once said: “If trouble can be foreseen, it can easily be avoided; if left until it appears, every remedy will come too late, because the disease will have become incurable… The same applies to politics.”

Niccolò might not have known about stablecoins, but he understood power. Data on payment flows suggest even deeply entrenched dominance can be shaken.

Each blockchain acts like a customs checkpoint; dollars move across chains as if goods were being manually loaded before container shipping.

This fragmentation is a weakness—and in crypto, weaknesses invite competition. A gradient descent-style war driven by incentives; a fight for control over the digital dollar itself.

The prize? To become the single, real, universal, cross-chain dollar.

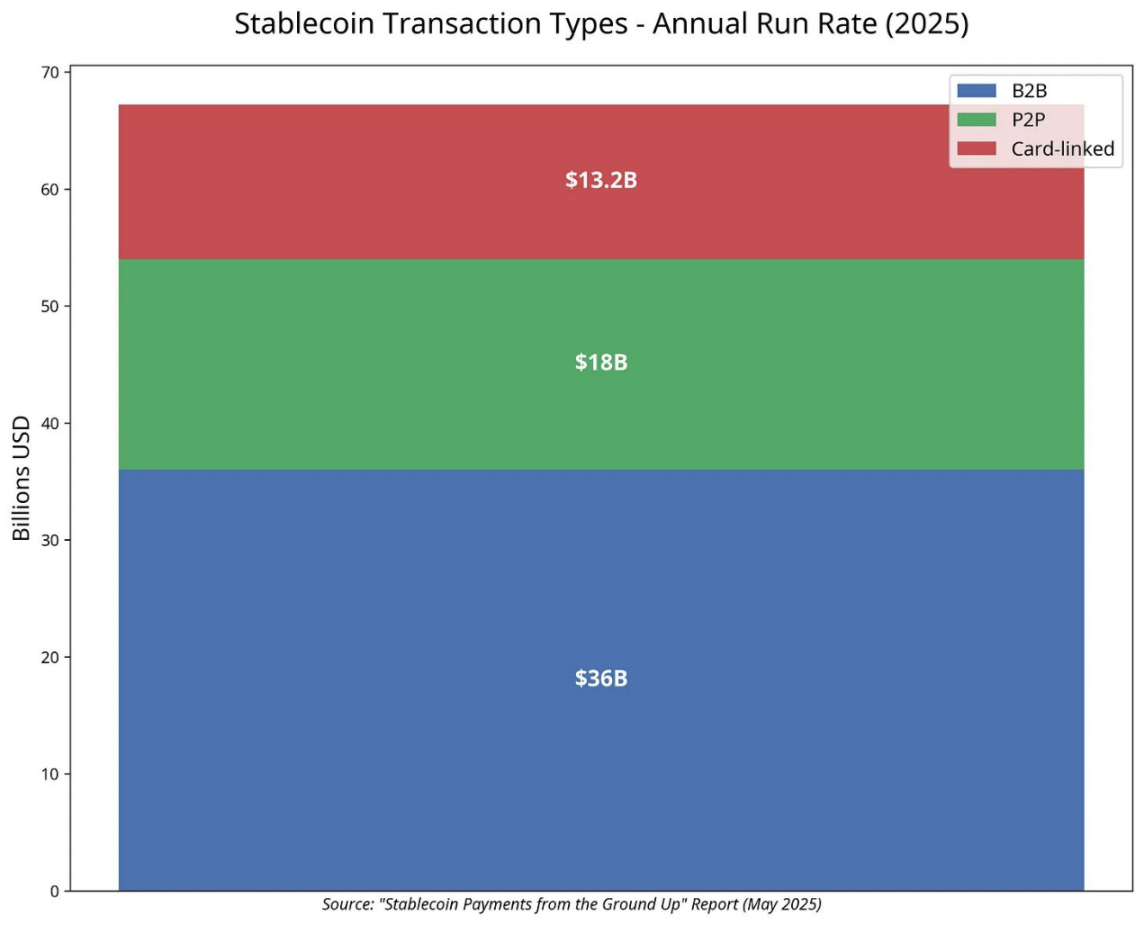

A groundbreaking new report titled *“Stablecoin Payments from the Bottom Up”* (the “report”), jointly released by Artemis, Castle Island Ventures, and Dragonfly, provides hard data. Co-authored by industry veterans including Nic Carter, the report analyzes $94.2 billion in real-world payment volume across 31 companies, revealing stablecoins have evolved from speculative trading tools into high-volume global settlement networks.

This is the story of how the king of stablecoins uses battlefield intelligence to wage war for a unified empire—armed with a new weapon called USD₮₀ (USDT0).

USDT is reserve; USDT0 is channel.

Contenders: A King, a Suit, and an Alchemist

The omnichain stablecoin war is a strategic game, shaped by philosophies of power and fully revealed through data.

1. The King: USDT / USDT0

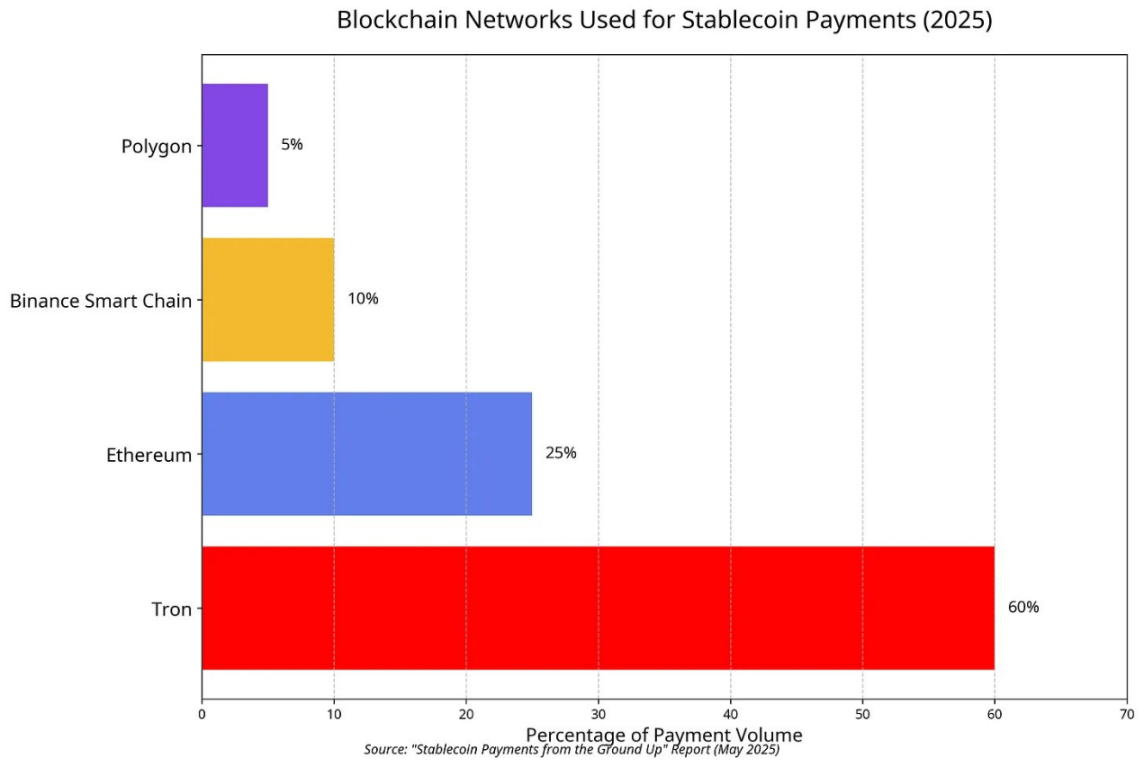

The Stablecoin Payments report confirms what many suspected: Tether’s USDT reigns supreme as the digital dollar—and as the monarchy itself. In the extensive sample of real-world payments analyzed, USDT commands a staggering 90% share of transaction volume. These are payments from streets around the world, not Wall Street. The report reveals its empire is built on the Tron network, which it identifies as the most popular blockchain for payments—and far ahead of the rest.

USDT0 is a native Omnichain Fungible Token (OFT) built by Everdawn Labs on LayerZero. It’s a brilliant integration: traditional USDT is locked in a vault on Ethereum, while an equivalent amount of fresh, fully fungible USDT0 is minted on the destination chain. It creates a single, standardized asset that can flow anywhere. Market demand was immediate. Within months of its 2024 launch, USDT0 enabled over $2 billion in cross-chain transfers.

2. The Suit: USDC / CCTP

If USDT is the king of the people, then USDC is the polished challenger eyeing the throne in institutional realms. The report confirms USDC trails but firmly holds second place—an advantage that makes its strategic choices critical. USDC draws strength from trust, compliance, and deep ties to traditional finance. Notably, Circle’s IPO was highly successful.

Circle’s Cross-Chain Transfer Protocol (CCTP) directly targets Tether’s weakness—fragmentation.

By allowing users to burn real USDC on one chain and mint equivalent native USDC on another, Circle establishes a clean, high-integrity standard for value transfer. This strategy has already shown traction in specific markets. While USDT dominates globally, the report shows USDC captures significant volume—nearly half in places like Argentina and India—indicating its compliance-first approach resonates with emerging venture-backed fintech firms in these regions. Single-signer risks and other trade-offs are topics unto themselves.

3. The Alchemist: FRAX

FRAX and other alternatives are “almost non-existent” in the payment report’s dataset.

This isn’t failure—it clarifies their role. Frax isn't fighting to rule payments today; it’s the alchemist in the lab, probing the boundaries of digital dollars and pressuring giants to evolve—or risk obsolescence.

FRAX blends algorithmic mechanisms with institutional backing, though memories of UST keep many cautious.

Like many closed financial systems lacking violence (*FreedomTM), this quote fits perfectly: “In a closed financial system, the one with more money decides the outcome.”

Frax USD is now minted as frxUSD, backed by reserves held by governance-appointed “Sacred Custodians.”

BlackRock’s BUIDL, Superstate’s USTB, and Janus-Henderson’s JTRSY lock verifiable Treasuries and cash—one token minted per dollar locked. When tokens are burned, the vault must return that dollar, so the peg depends on on-chain auditable reserves.

So far, these projects have seen major success. How does it work?

Yield-seekers deposit frxUSD into sfrxUSD vaults, which allocate underlying assets into high-yield strategies—short-term Treasuries, DeFi arbitrage, or AMO market making—pushing rates up while maintaining par value.

Long-term investors participate in FXB auctions, exchanging existing FRAX for larger future shares, sketching out a native on-chain yield curve free from external credit risk. On Fraxtal, every transaction is transparent; the renamed FRAX token fuels gas and, via veFRAX locking, controls the entire lab.

All this happens on the Fraxtal L2 chain, where the commodity token FRAX (formerly FXS) pays gas fees and anchors broader ecosystem governance through veFRAX locking.

Still, every pegged asset invites its “Soros.”

Who plays Soros? Any well-funded platform with on-chain leverage. Jump Crypto, Wintermute, or similar entities fit the mold.

They could borrow large amounts of frxUSD or legacy FRAX, dump them below peg, layer short positions, and later redeem against still-solvent custodial vaults.

Profit comes from the spread between discounted tokens bought on-market and full-dollar redemptions. If oracles lag or bridges clog, spreads widen. Accumulating veFRAX during calm periods could accelerate systemic stress.

This may oversimplify, but skeptics might say: it’s like building a high-convexity bond market atop a fragile yield curve.

Time will tell. Experiments like this often yield incredible long-term benefits.

After all, this is crypto—until people actually use it, money is just an empty shell. What turns hollow code into daily currency?

Two Dollars, One Story: Unifying Street Dollar and Enterprise Dollar

The true significance of USDT0 lies in connecting two distinct worlds: the world of Street Dollar and the world of Enterprise Dollar. Nathan’s “value realization hierarchy” framework helps clarify this divide: stablecoin users fall into two groups—“those who need stablecoins and those who don’t.”

Street Dollar is where USDT thrives.

Ana, a freelance designer in Bolivia, uses it to fight inflation exceeding 100% annually. David, a small business owner in Lagos, uses it to pay Chinese suppliers, bypassing strict central bank forex controls.

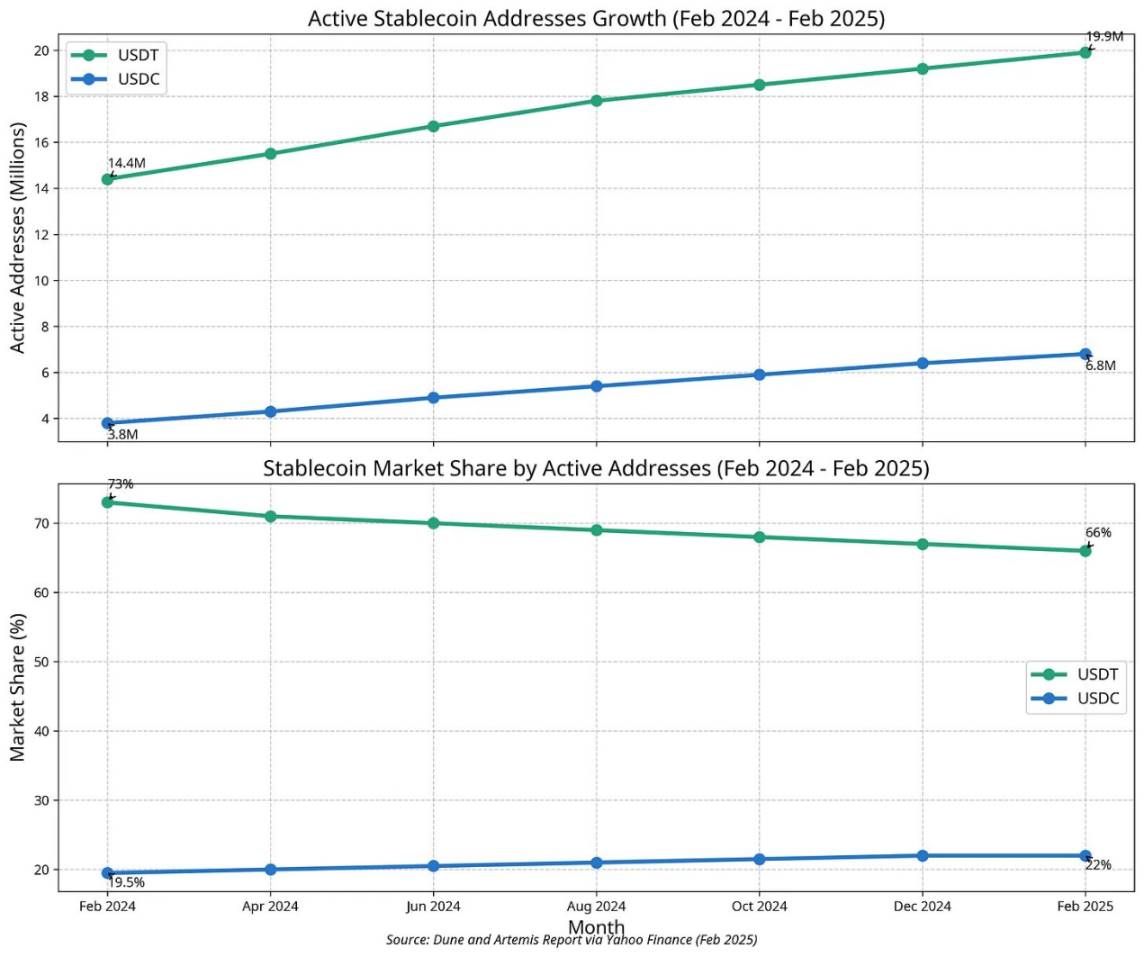

To them, USDT is a tool. As Nathan explains, for users in emerging markets, “permissionless access is a transformative unlock.” It grants them access to stable money that was previously unimaginable. This is Tron’s economic model: the report shows over 52 million addresses hold less than $1,000 worth of USDT.

As Paolo Ardoino (Tether CEO) puts it, digital dollars fill market voids left by fiscal incompetence and corruption. Permissionless truly means permissionless.

Trust gives value; real, sustained adoption is earned.

Enterprise Dollar is USDT’s opportunity. It’s the dollar used in Ethereum and its L2s’ high-tech financial cloud. It’s programmable—used as loan collateral, generating yield in complex liquidity pools, or as a tool for high-frequency arbitrage. For Western users, Nathan argues: “programmability is the main catalyst for stablecoin innovation in the West.”

Prior to USDT0, these two worlds were separate. This created a serious problem, as Sam Broner of a16z also emphasized.

He calls it the challenge of achieving “monetary singularity”—the idea that all forms of money should be perfectly interchangeable. Tron-based USDT locked in the Street Dollar world is not the same as Ethereum-based USDT circulating in the DeFi dollar world.

USDT0 attempts to solve this.

USDT is reserve; USDT0 is channel.

Ana can take her earned street dollars and, with one simple transaction, send them to a savings protocol on Arbitrum to earn 5% yield. David’s company can use the same asset to pay a supplier $219,000—a transfer that would’ve cost $26 in fees before. USDT0 connects the raw, chaotic energy of the street with the powerful, efficient mechanics of DeFi, unifying Tether’s dollar.

The chart above illustrates this clearly. Tron, the top blockchain for stablecoin payments, exemplifies this. Tron offers the lowest fees and enjoys broad adoption in emerging markets.

LegacyMesh locks each Tron or TON network token. Then, Arbitrum mints a one-to-one USDT0 twin, natively circulating on Ethereum, Berachain, and any chain connected via LayerZero.

In short, this design compresses dozens of bridged versions into a single canonical token and expands Tether’s reach into DeFi and beyond.

Dollars leaving the street arrive intact at yield farms and credit markets, moving at block speed—not via custodial detours. With Tron, TON, Ethereum, and Arbitrum already connected, the network now wraps most USDT into a single circuit, granting it a “gas-saving passport” to broader domains.

This is a crucial addition to Tether’s arsenal.

Endgame: The Battle for Stablecoin Channels

The rise of omnichain technology signals a new endgame. Tether’s USDT0 strategy now reveals a dual-pronged approach:

-

Core Defense: On low-cost chains like Tron, traditional USDT continues defending its vast empire of Street Dollar users, leveraging network effects through planned migration via LegacyMesh.

-

Offensive Expansion: USDT0 acts as a vanguard force aiming to conquer new frontiers—high-end DeFi, institutional platforms, and next-gen mobile payment apps.

Three key battlegrounds remain open:

Where is the next critical front? While Tether dominates in transaction volume, Circle wins in the race among venture-backed startups. Will the next generation of high-growth payment companies and neobanks choose USDC’s compliance or the tactical flexibility of assets like USDT0? The fight for next-gen fintech infrastructure remains pivotal.

Can CCTP win on user experience? USDT0 achieves its omnichain vision through third-party protocols (LayerZero). CCTP, in contrast, is a first-party, vertically integrated solution. Can Circle offer developers and institutions a safer, faster, or simpler experience through tighter integration? In a world plagued by bridge hacks, a fortress built and controlled by the issuer is a strong selling point.

Will “Enterprise Dollar” choose another path? The report highlights B2B payments as the largest and fastest-growing segment, with average transaction sizes exceeding $219,000. These flows are precisely the most sensitive to counterparty risk and regulatory scrutiny. As this market matures, will enterprises and financial institutions naturally favor the “suit” (USDC) over the “king” (USDT) and its special forces?

What happens when the West awakens? The report focuses heavily on emerging market payments, where USDT dominates. But what happens when use cases in the U.S. and Europe begin rising—driven by programmability and yield? That’s Circle’s home turf. When these markets go live, can Circle convert its strong position among Western developers and institutions into broader network effects?

As Chuk noted in his article *“Stripe, Stablecoins, and the $100 Billion Race to Remake Finance,”* the dollar is unbundling from the old world and rebundling on-chain.

Another notable contender is Plasma. Backed by Bitfinex, Founders Fund, and others, Plasma is a sidechain that anchors state to Bitcoin while running an EVM-compatible, zero-fee environment optimized for stablecoin transfers.

This design allows USDT locked on Plasma to transfer at PoS speeds while inheriting Bitcoin’s settlement security—offering Tether a dedicated channel unmatched by either Tron or Ethereum.

If USDT0 becomes the universal wrapper for this liquidity, Plasma can handle bulk settlements of Street-Dollar funds and secure them as they gradually enter higher-yield Enterprise Dollar territories—tying the whole system together in a way Circle’s CCTP cannot easily replicate.

USDT0 is a pivotal move to consolidate Tether’s empire, and Plasma could further extend its influence into new domains.

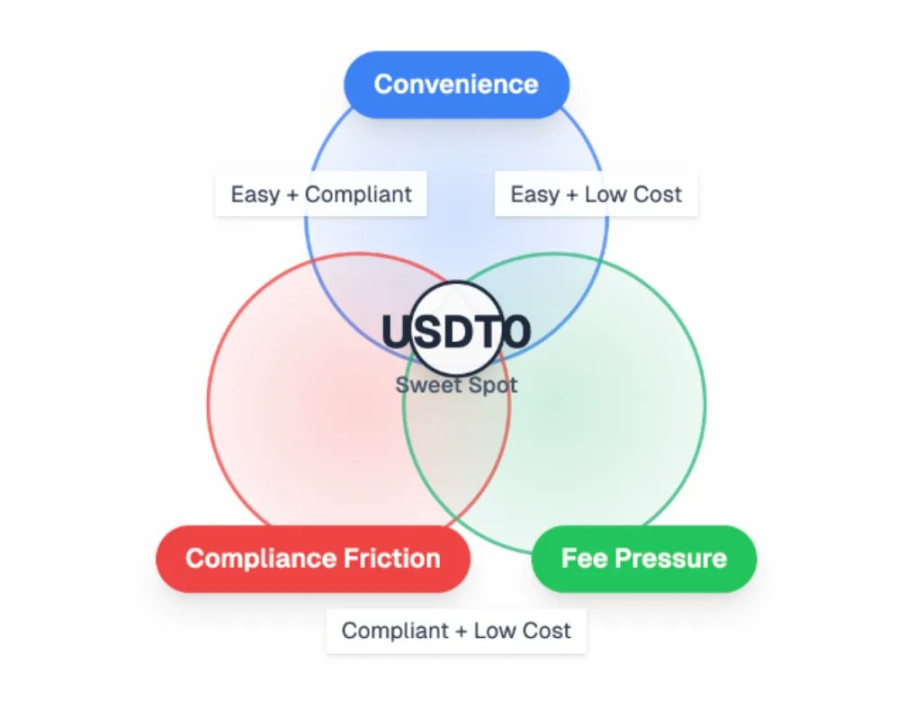

Where USDT0 Can Outpace Circle’s CCTP

USDT0’s clearest opening lies at the intersection of convenience, compliance friction, and fee pressure:

-

Wage and remittance corridors in emerging markets already rely on Tron’s liquidity but crave direct access to DeFi yields.

-

Mid-sized B2B settlements—e.g., $50k–$500k vendor payments—struggle with wire cutoff times and banking limits.

-

DeFi protocols unwilling to use bridges desire a single, low-gas-cost dollar across chains for collateral and liquidity mining.

-

Mobile fintech apps seeking dollar accounts without bank partnerships.

By focusing first on these four real-world niches, USDT0 can solidify its transaction volume lead before Circle catches up.

Tether’s DeFi Strategic Plan

USDT remains king of the street, but USDC rules the dashboards.

To shift this balance, Tether must dismantle the specific moats USDC enjoys.

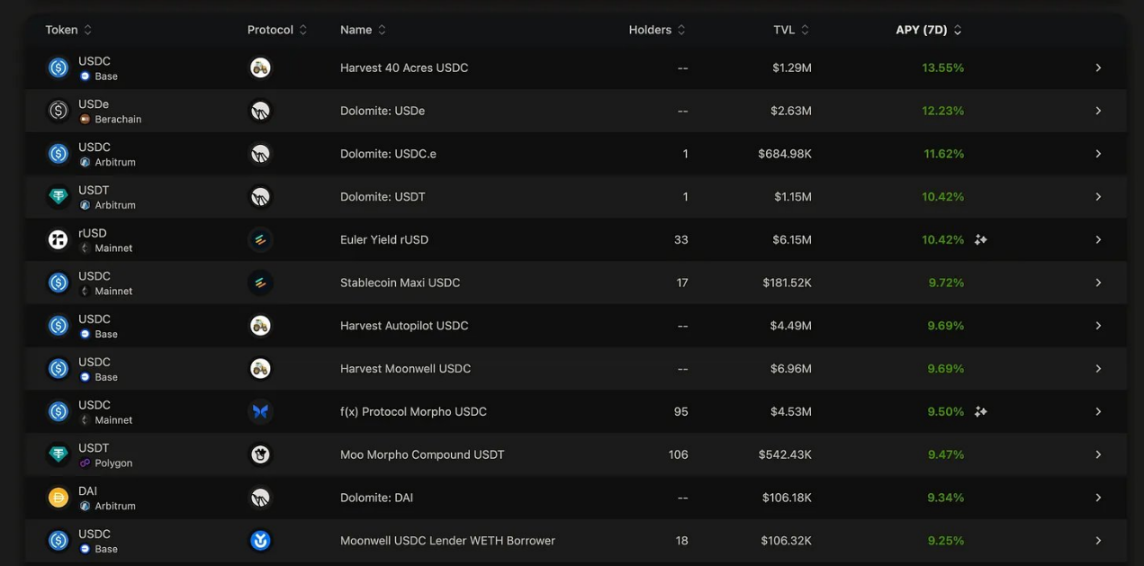

Dashboards like Vault heavily favor USDC: in January 2025, the top 10 highest-yielding strategies on vaults.fyi were all USDC, with Revert Lend USDC yielding 14.9% APY and Gauntlet USDC Core at 14.7%.

This changed by June 2025—2 out of 10 platforms now support USDT.

This dashboard dominance rests on three practical advantages:

-

Most yield strategies (Maker DSR, Aave, Morpho, Compound, Ethena hedging) accept or return USDC.

-

Traders view USDC as the cleanest accounting dollar on-chain.

-

Its bridge is first-party (CCTP), so wrapped versions rarely fragment liquidity.

Here’s how to tackle each:

-

Strategy coverage. Maker, Aave, Morpho, Compound, and Ethena all settle in USDC, so builders default to it. Tether can counter by funding pathways such as USDT0 → sUSDe → Ethena or USDT0 → Fraxlend → Curve stables. Wrap them in ERC-4626 and add temporary 50–100 bp incentives. Once Yearn, Beefy, and Enzyme list these vaults, the habit of using USDC will fade.

-

Perceived compliance. Maker and Morpho still apply haircuts to USDT. Since each USDT0 token is backed by vaults on Ethereum and natively minted on each chain, Chainlink’s proof-of-reserves oracle will allow risk committees to adjust these haircuts. The borrowing fee gap remains stark: on June 10, 2025, borrowing USDT on Aave v3 carried ~4.9% fees, versus just 0.6% for USDC on the same platform. Still, this doesn’t change trust in the reserves themselves.

-

Bridge convenience. Developers love Circle’s first-party bridge. USDT0 can match this via OFT and LegacyMesh: token addresses appear natively on every major rollup, so vaults rebalancing between Arbitrum, Optimism, and Base only need to hold one ERC-20 token—no repeated burn-and-mint cycles.

-

Liquidity depth. Curve and Balancer still anchor to USDC. USDT can use market maker book capital to bootstrap omnichain tri-pools and refund 100–150 bps in LP fees quarterly. On Balancer, weekly 30–40 bps in vlBAL or implicit incentives can attract equivalent depth.

-

Dashboard inertia. Aggregators like vaults.fyi display only what’s indexed. USDT0 or LayerZero can host open JSON sources for every audited USDT0 vault. Once strategies pass security reviews, they earn equal visibility with USDC.

If Tether pulls all five levers—reference strategies, proof-of-reserves oracles, cross-chain native assets, subsidized deep pools, and public indexing—annualized yields should tilt toward USDT0.

Yield hunters chase numbers, not loyalty; once that spread opens, USDC’s dashboard lead could vanish within a quarter, and the “alchemist’s” experiments will gain fresh liquidity.

The future of money will be fought on more fronts. The outcome will depend not just on who owns the past and present, but on who can unite Street Dollar and Enterprise Dollar to create the true dollar—and thus claim the most valuable territory of the future.

As Omar Little wisely said: “You come at the king, you best not miss.”

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News