Hotcoin Research | Stablecoins Enter the Regulatory Era: Analyzing the Impact of the GENIUS Act on U.S. Treasuries, Stablecoins, and RWAs

TechFlow Selected TechFlow Selected

Hotcoin Research | Stablecoins Enter the Regulatory Era: Analyzing the Impact of the GENIUS Act on U.S. Treasuries, Stablecoins, and RWAs

The GENIUS Act represents a redefinition of U.S. financial sovereignty: embedding stablecoins within the Treasury bond structure, integrating on-chain assets into the dollar system, and evolving the "dollar anchor" from a price peg to a liquidity and value anchor.

Author: Hotcoin Research

I. Introduction

On May 19, the U.S. Senate passed a procedural vote on the GENIUS Act by a wide margin, marking America's imminent arrival at its first nationwide, unified stablecoin regulatory framework—seeking to legally define and regulate the operational mechanisms of a "digital dollar." This development will not only reshape the power structure of the U.S. stablecoin market but may also trigger far-reaching policy, economic, and geopolitical monetary chain reactions globally, redrawing the future landscape of financial markets.

The GENIUS Act represents a redefinition of U.S. financial sovereignty: embedding stablecoins into the national debt structure, integrating on-chain assets into the dollar system, evolving the "dollar peg" from price anchoring to liquidity and value anchoring. By legislating to channel global demand for stablecoins into demand for U.S. Treasury bonds, it aims to consolidate the dollar’s anchoring role in the restructuring of the new financial system. Stablecoins are no longer merely the "shadow dollars" of the crypto world—they are becoming sovereign currency "extensions" linking the crypto market with traditional finance. Once implemented successfully, this regulation could usher in a new cycle dominated by the dollar, potentially accelerating mass adoption of stablecoins while providing institutional support for the next wave of RWA and digital treasury innovations.

This article analyzes the legislative content and institutional design of the GENIUS Act, systematically outlining its core provisions regarding regulatory definitions, licensing mechanisms, reserve requirements, and legal status. It also examines current limitations such as political negotiations, scope applicability, and enforcement challenges within the bill’s existing version. Based on this analysis, the article evaluates the direct and indirect impacts of the act on the U.S. Treasury market, the crypto stablecoin market, and the RWA sector, aiming to fully reveal the underlying financial logic and profound real-world implications of this so-called “genius legislation.”

II. Overview of the GENIUS Act

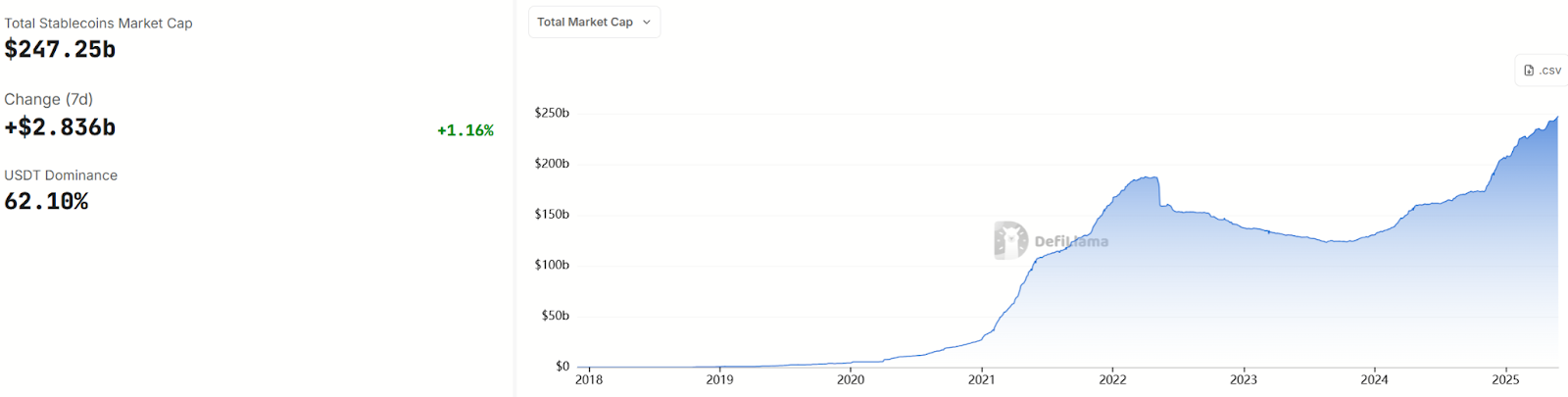

Stablecoins have existed for over a decade. Since Bitcoin’s inception, their characteristics of “pegging to fiat currencies and being redeemable at par” have enabled them to evolve globally—from speculative instruments into payment tools, liquidity bridges, and even store-of-value assets. As of May 29, 2025, the total market capitalization of stablecoins has approached $250 billion. However, stablecoin assets have long operated in a regulatory gray zone, lacking clear standards in legal definition, risk isolation, and reserve disclosure.

Source:https://defillama.com/stablecoins

The passage of the GENIUS Act will establish comprehensive definitions, entry thresholds, operational boundaries, and reserve management rules for stablecoins, formally legitimizing this key financial innovation through regulation. The GENIUS Act (full name: “Guiding and Establishing National Innovation for U.S. Stablecoins Act”) is the Senate version, introduced by bipartisan senators including Republican Senator Bill Hagerty, aiming to create the first federal regulatory framework for payment stablecoins. Meanwhile, the House advances the STABLE Act (Stablecoin Transparency and Accountability for a Better Ledger Economy Act of 2025), proposed by Republican Representative Bryan Steil, which shares similar content and seeks to establish a comprehensive regulatory mechanism for stablecoin issuance.

1. Core Regulatory Provisions

The GENIUS Act requires any entity issuing payment stablecoins in the United States to obtain either a federal or state license. Institutions without such authorization cannot issue stablecoins. The act defines a “payment stablecoin” as a digital asset pegged to a fixed fiat currency (e.g., USD) and redeemable at a fixed value (e.g., $1). It explicitly states that these stablecoins do not benefit from federal deposit insurance. Issuers must hold 100% equivalent high-quality reserve assets—issuing one dollar of stablecoin requires holding at least one dollar of compliant reserves.

Permitted reserve assets are limited to: cash and coins, demand deposits at banks or credit unions, short-term U.S. Treasuries (≤93 days), repo/reverse-repo agreements collateralized by Treasuries, government money market funds, central bank reserves, and other low-risk government-like bonds approved by regulators. The act strictly prohibits the misuse or rehypothecation of reserve assets. Reserves can only be used under limited circumstances, such as for stablecoin redemptions or as collateral in repos. These rules ensure a solid asset backing for the 1:1 peg and prevent risks arising from reserve misappropriation.

2. Disclosure and Auditing Requirements

To enhance transparency, the act mandates issuers to publish monthly reports on stablecoin circulation volume and reserve composition, detailing the number of stablecoins issued and the structure of corresponding reserve assets. Reports must be certified by the issuer’s CEO and CFO and subject to periodic audits by registered accounting firms. Issuers with a market cap exceeding $50 billion must additionally submit annual audited financial statements.

Furthermore, issuers must establish clear redemption mechanisms ensuring holders can quickly redeem stablecoins at face value. These frequent disclosures and external audit requirements shift stablecoin operations from past “opaque black boxes” into the sunlight, aiming to eliminate user concerns about reserve adequacy.

3. Licensing System and Tiered Regulation

The GENIUS Act establishes a dual-track regulatory system comprising both federal and state licenses. Both banks and non-bank institutions may apply to become stablecoin issuers but must register with the appropriate regulatory authority. State regulators may oversee issuers meeting federal standards, provided their state frameworks are “substantially equivalent” to the federal standard.

For issuers opting for a federal license, oversight depends on the institution type: non-banks fall under the Office of the Comptroller of the Currency (OCC); banks or their subsidiaries are regulated by the relevant federal banking regulator (OCC, Fed, or FDIC).

State-licensed issuers are primarily supervised at the state level, though states may enter cooperation agreements with federal bodies (such as the Federal Reserve) for joint supervision. For interstate operations, licensed stablecoin issuers will gain mutual recognition across U.S. states, avoiding previous constraints tied to single-state money transmission licenses—helping foster a unified national market.

4. Tiered Oversight by Scale

The act introduces a tiered requirement based on the "$10 billion threshold" for different-sized issuers:

The Senate version (GENIUS Act) stipulates that if a state-regulated issuer reaches a circulating market value of $10 billion in stablecoins, it must transition to federal oversight or cease further issuance. Upon crossing this threshold, non-bank issuers come under federal OCC supervision, while bank-affiliated issuers are jointly regulated by federal and state authorities.

The House version (STABLE Act) differs here—it allows state-regulated issuers to remain under state oversight regardless of size, without mandatory federal conversion. This divergence reflects differing views between the two chambers on the balance between federal and state regulatory authority, requiring reconciliation during final legislative coordination.

5. Legal Status and Consumer Protection

The act clarifies the legal nature of stablecoins: compliantly issued payment stablecoins are excluded from the definitions of securities and commodities, thus exempting them from SEC and CFTC oversight. At the same time, stablecoins are not considered bank deposits (and therefore do not enjoy FDIC insurance). The U.S. Bankruptcy Code will also be amended to prioritize stablecoin holder rights: in the event of issuer bankruptcy, claims by stablecoin holders on reserve assets take precedence over those of general creditors. This bankruptcy priority ensures users’ right to full redemption remains legally protected even if the issuing entity collapses—an essential consumer safeguard.

In addition, the act bars individuals with prior financial crime convictions from serving as issuer executives and mandates full compliance with U.S. anti-money laundering (AML) and sanctions regulations. Issuers are deemed financial institutions under the Bank Secrecy Act and must implement KYC procedures, maintain transaction records, and report suspicious activities. The Financial Crimes Enforcement Network (FinCEN) will develop specific AML rules for digital assets and require issuers to have technical capabilities to freeze, destroy, or block specific stablecoin transfers upon receiving lawful orders from courts or regulators.

6. Other Key Provisions

The GENIUS Act includes several provisions aimed at long-term market development:

-

Custody and Payment Integration: Banks are allowed to offer custody services for stablecoins and their reserve assets, use blockchain for settlement, and issue their own tokenized deposits. In other words, traditional banks can legally issue customer deposits in token form, enabling bank deposits to circulate on-chain like stablecoins. This opens the door for banks to participate in blockchain innovation and promotes RWA tokenization.

-

Prohibition of Fund Mixing: For institutions providing stablecoin or reserve custody, the act requires they be regulated financial entities and prohibits commingling client stablecoin reserves with proprietary funds except in specific exceptions. Custodians must treat client-held stablecoin assets as client property and protect them, preventing claims by other creditors should the custodian go bankrupt.

-

Interest Payments to Holders Prohibited: Both the GENIUS and STABLE Acts explicitly prohibit stablecoin issuers from paying interest or returns of any kind to holders. Stablecoins cannot offer interest returns like bank deposits or money market funds. This provision aims to prevent direct rate competition with bank savings and remains one of the more controversial clauses.

-

Transition Period Arrangements: Acknowledging existing market realities, the act grants existing stablecoin issuers up to an 18-month grace period for compliance adjustments. For example, major incumbents like USDT and USDC must apply for licenses or adjust organizational structures to meet regulatory requirements within a specified timeframe after enactment. Failure to comply by the end of the grace period would prohibit them from offering stablecoin services to U.S. users. This “amnesty-style” clause ensures a smooth market transition, allowing currently operating stablecoins to integrate into the new regulatory framework.

III. Limitations and Progress of the GENIUS Act

After intense bipartisan negotiations, the bill text underwent multiple revisions due to concerns over inadequate consumer protection, AML and foreign stablecoin (e.g., USDT) regulatory loopholes, and potential benefits to Trump-family-linked cryptocurrency ventures. Subsequently, both parties engaged in intensive talks, amending the bill to strengthen consumer safeguards. For instance, it added clauses reinforcing the applicability of existing federal and state consumer protection laws, making clear that stablecoin issuers remain subject to state-level anti-fraud and financial consumer laws—even with a federal license, they are not exempt from state legal liability. Additionally, ethics provisions were included to ensure government officials cannot participate in stablecoin issuance, addressing accusations of “conflict of interest.”

1. Differences Between Bill Versions

The House’s STABLE Act and the Senate’s GENIUS Act share the same core principles but differ in several clauses:

-

Issuer Size and Regulatory Limits: The Senate version mandates that state-regulated issuers exceeding $10 billion in issuance must switch to federal oversight; the House version imposes no such requirement, allowing indefinite continuation of state-level regulation.

-

Licensing and Geographic Restrictions: The GENIUS Act permits only U.S.-based entities to become licensed issuers and bans unlicensed foreign stablecoins from public sale in the U.S. after a three-year transition period, unless an equivalence agreement exists between the foreign regulator and the U.S. This means overseas-issued stablecoins like Tether would be deemed “non-compliant” if they fail to establish a regulated U.S. entity. In contrast, the House STABLE Act is relatively open to foreign compliant stablecoins: issuers from countries whose regulatory regime is deemed “equivalent” by the U.S. Treasury may circulate their stablecoins in the U.S., provided they accept U.S. regulatory inspections and reporting obligations.

2. Limitations of the GENIUS Act

Despite being hailed as a milestone in U.S. crypto policy, the GENIUS Act has several limitations and concerns:

-

Narrow Scope: The act focuses solely on fiat-collateralized payment stablecoins, leaving other types of crypto assets unaddressed. Algorithmic stablecoins fall outside the definition of “payment stablecoin,” remaining in a legal gray area. Decentralized stablecoins like DAI, lacking a centralized issuer, would struggle to meet licensing, AML, and compliance requirements. Thus, while encouraging centralized compliant stablecoins, the act objectively suppresses decentralized alternatives.

-

Enforcement Challenges: The act requires foreign stablecoins to achieve regulatory equivalence within three years to operate in the U.S. But in practice, monitoring and enforcing against offshore entities using decentralized exchanges or peer-to-peer wallets to serve U.S. users remains difficult. Given the vast number of permissionless global trading venues and wallets, the U.S. cannot fully prevent their usage.

-

Political Risks: From proposal to passage, the act carries strong political backing from the Trump administration, aiming to leverage stablecoins to reinforce dollar dominance. Although ethics clauses were later added, changes in party leadership could still affect its longevity. If Democrats regain power in 2028, they might reconsider stablecoin policy. Therefore, the long-term stability of the GENIUS Act depends on stablecoins proving their value and securing stakeholder support within the coming years.

-

International Coordination: Stablecoins are inherently cross-border. U.S. legislation alone cannot resolve all issues. The EU has already adopted MiCA to regulate crypto assets, including stablecoin issuance and reserve requirements. China’s central bank strictly prohibits domestic issuance or trading of any stablecoin. While the U.S. GENIUS Act may become a global reference, divergent international attitudes could lead to coexisting—and possibly conflicting—regulatory models.

3. Legislative Progress of the GENIUS Act

On May 19, several previously观望“crypto-friendly” Democratic senators announced acceptance of the revised bill and pledged to vote in favor. That evening, the Senate broke a filibuster with a 66–32 vote, advancing the bill to full chamber debate and voting.

In early June, the Senate is expected to formally pass the GENIUS Act by simple majority, sending it to the House for consideration. On the House side, the Financial Services Committee passed the STABLE Act with bipartisan support in March and forwarded it to the full chamber, now awaiting scheduling for a vote. Since both versions need reconciliation, lawmakers plan to finalize a merged bill before the summer recess and send it to President Trump for signature. President Trump has repeatedly expressed public support for stablecoin legislation, stating “crypto will expand global dollar dominance.” It is anticipated that the GENIUS Act will officially become law around August 2025—marking the first codified U.S. law specifically targeting stablecoins.

IV. Impact of the GENIUS Act on the U.S. Treasury Market

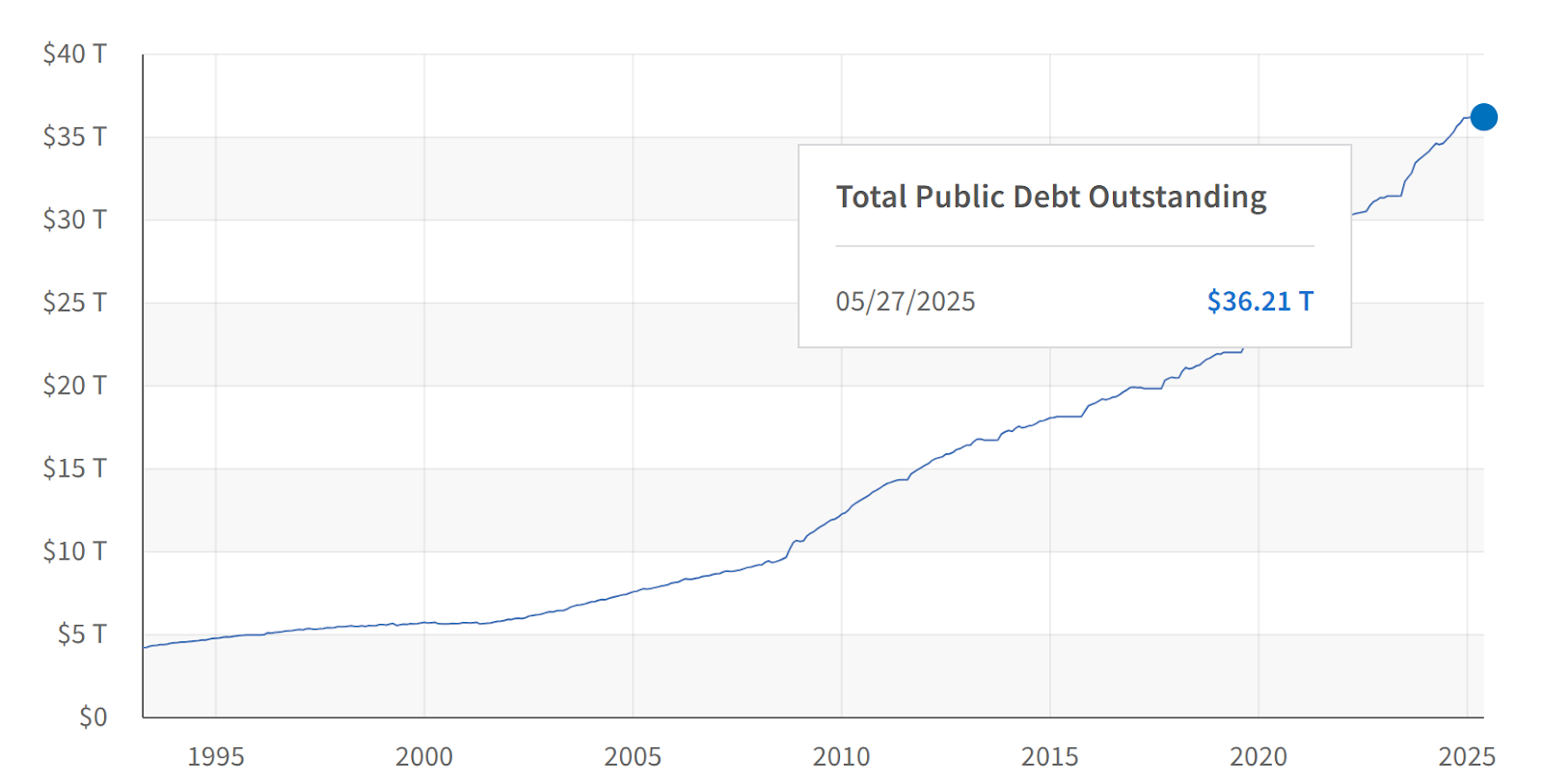

As of May 2025, total U.S. federal government debt exceeds $36 trillion—approximately 123% of GDP—reaching record highs. With chronic fiscal deficits and rising interest burdens, the Treasury market faces ongoing expansion pressure and funding shortages. By mandating that stablecoin reserves primarily invest in short-term U.S. Treasuries and other highly liquid assets, the act channels global demand for digital dollars into real demand for U.S. debt, potentially easing financing pressures and strengthening the dollar’s dominance in crypto finance.

Source:https://fiscaldata.treasury.gov/datasets/debt-to-the-penny/

-

Increased Treasury Demand: Major global dollar-pegged stablecoins (e.g., USDT, USDC) already allocate significant portions of their reserves to U.S. Treasuries. Once the law takes effect, this massive crypto capital pool will be directed toward U.S. government bonds. For example, as of Q1 2025, Tether held approximately $120 billion in U.S. Treasuries—ranking it the 19th-largest institutional holder globally. The growth of stablecoins offers the U.S. Treasury a new, stable source of funding, presenting a strategic opportunity to strengthen dollar hegemony and reduce government borrowing costs—effectively converting global demand for digital dollars into actual purchases of U.S. debt.

-

Capital Flows and Banking Impact: Widespread stablecoin adoption could affect traditional bank deposits and money market flows. When users move funds from banks into stablecoins, issuers reinvest the equivalent amount into Treasuries or keep it in demand accounts at large banks. This may trigger deposit outflows from smaller banks, potentially causing cascading liquidity risks. To mitigate direct competition with bank savings, the GENIUS Act prohibits stablecoins from paying interest. Additionally, the act grants intervention powers to regulators like the Fed and OCC: in cases of violation or abnormal activity, they may act under “extraordinary emergency conditions,” including halting new stablecoin issuance. This enables monitoring of large-scale stablecoin capital movements, allowing early warnings and interventions against systemic risks.

-

Potential Risks: Currently, the scale of short-term Treasuries held by stablecoins remains small relative to the $36 trillion total U.S. debt. However, if a major stablecoin collapses and dumps its short-term Treasury holdings, it could trigger fire sales and disrupt short-term bond market liquidity. The GENIUS Act attempts to minimize such credit and spillover risks through requirements like 100% high-quality reserves and senior claim rights. Overall, implementation will transform stablecoins into highly transparent, regulated pools akin to money market funds—providing steady buyer support for U.S. Treasuries and further aligning U.S. government interests with global demand for digital dollars.

V. Impact of the GENIUS Act on the Stablecoin Market

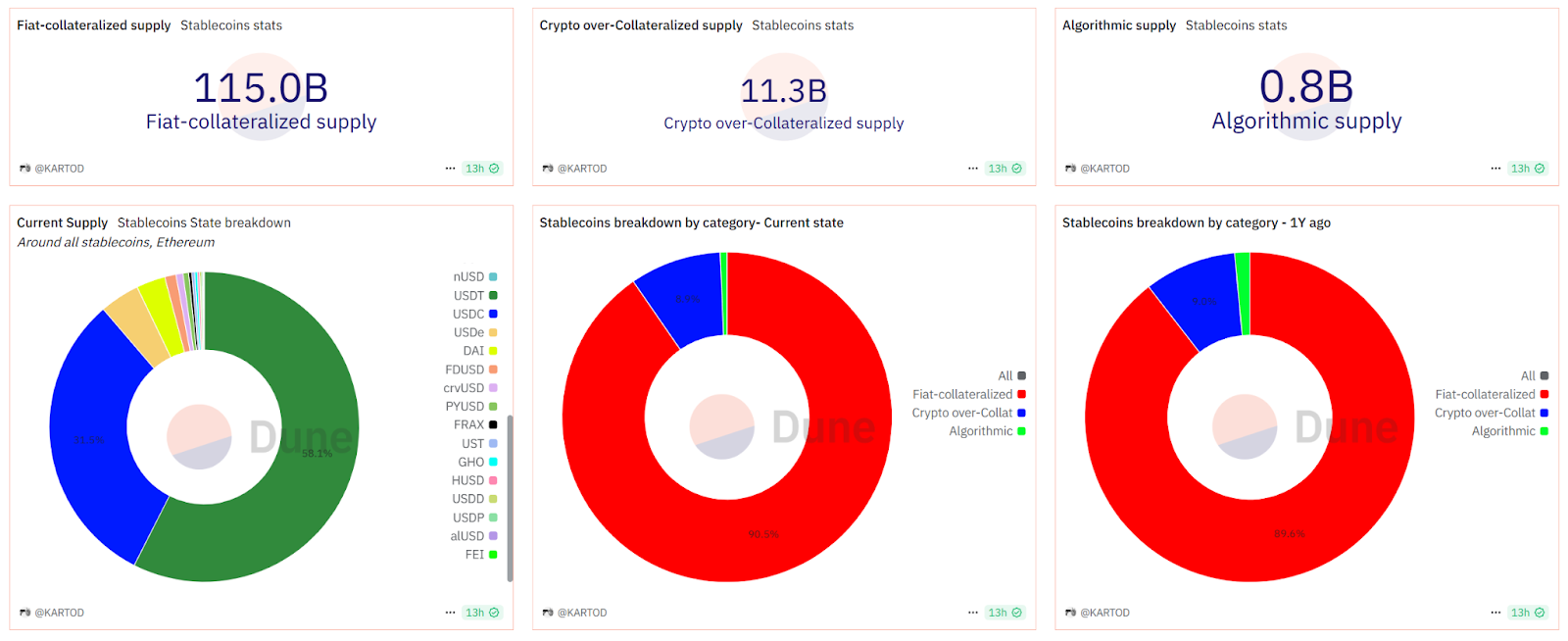

Fiat-collateralized stablecoins dominate current supply, totaling $115 billion (90.5% share); crypto-overcollateralized stablecoins account for $11.3 billion (8.9%); algorithmic stablecoins represent just 0.6%. Among these, USD-pegged fiat stablecoins like USDT and USDC hold overwhelming market share. The GENIUS Act will reshape the competitive landscape and regulatory environment of today’s stablecoin market, with major effects on issuer dynamics, market confidence, and compliance transitions of existing stablecoins.

Source:https://dune.com/KARTOD/stablecoins-overview

-

Issuer Landscape and Competition: Under the new law, stablecoin issuance shifts from unregulated expansion to a licensed, competitive era. Non-bank institutions can now legally issue stablecoins, no longer restricted to banks. Post-enactment, major U.S. financial institutions and tech giants are likely to accelerate entry into the stablecoin space. Dominant players like USDT and USDC may face new challengers from Wall Street, with companies competing via lower fees and better services. For users, this means safer, more diverse stablecoin options and potential cost reductions and service improvements.

-

Shifts Among Existing Stablecoins: As the world’s largest stablecoin by market cap, USDT is issued by Tether Ltd., registered overseas and historically operating outside U.S. regulation. After the GENIUS Act takes effect, unlicensed foreign stablecoins will gradually be marginalized in the U.S. market. During the ~18-month transition period, Tether must establish a U.S. subsidiary and apply for licensing to continue serving American users, complying with U.S. reserve and audit requirements. Otherwise, after the three-year grace period, U.S. institutions (exchanges, brokers, etc.) will be barred from facilitating transactions or settlements for non-compliant foreign stablecoins. Some analysts argue that Tether’s traditionally opaque operations and complex offshore structure, if forced to disclose reserves and submit to U.S. oversight, could expose vulnerabilities and weaken market confidence in USDT. In contrast, Circle’s USDC is poised to emerge as a clear compliance winner. Already U.S.-registered, Circle regularly discloses reserves, undergoes audits, and partners with Coinbase under strict KYC/AML practices—earning it a “model stablecoin” reputation. Circle is expected to apply for a federal OCC issuer license or seek Fed oversight, positioning USDC as one of the first officially recognized compliant stablecoins.

-

Market Confidence and Adoption Scale: Stablecoin legislation will significantly boost public and institutional trust and acceptance. Mandatory reserve and disclosure rules will accelerate mainstream adoption: consumers will feel safer using stablecoins for payments and trading, and businesses will be more willing to accept them. More online platforms and physical merchants are expected to adopt stablecoin settlements. U.S. users could soon pay with digital dollars from their mobile wallets at coffee shops or supermarkets—just as conveniently as using cash or credit cards. Moreover, compliant stablecoins will facilitate fiat-to-crypto conversions, reducing friction and costs, driving financial innovation.

-

Impact of Interest Ban: The prohibition forces stablecoins to forgo interest payments to users, shifting their primary use toward payments, settlements, and short-term value storage rather than long-term yield generation. This makes stablecoins more like “digital cash” than “digital deposits.” Yield-seeking capital may prefer staying in traditional banks or money market funds (~5% annual yield). However, issuers themselves will continue earning returns from reserve assets and may offer indirect incentives—such as trading fee discounts or token airdrops—to attract users.

VI. Impact of the GENIUS Act on the RWA Market

With the passage of the stablecoin bill, the U.S. financial system is quietly opening doors to tokenization of real-world assets (RWA). The GENIUS Act not only regulates stablecoins but sends a clear signal: mainstream financial institutions can engage in blockchain activities—including issuing on-chain financial products—under regulated frameworks. This will drive the tokenization of various real financial assets, bringing structural reforms and new investment opportunities.

-

Tokenized Deposits and Banking Innovation: The act explicitly allows regulated banks to issue tokens representing customer deposits using distributed ledger technology—so-called “tokenized deposits.” This enables banks to experiment with on-chain dollar deposits and on-chain settlements. For the RWA market, active bank participation brings rich real-world assets onto chains: banks could tokenize loans, receivables, real estate investment trusts, and offer these to qualified investors as higher-liquidity, transparent products. The on-chain migration of traditional financial assets is expected to accelerate under regulatory guardrails.

-

Stablecoin Ecosystem Benefits RWA: Stablecoins are often called the “bridge” between the crypto world and real assets. Other RWA tokens (e.g., on-chain bonds, notes) can use stablecoins as value carriers during trading and settlement, eliminating reliance on fiat systems and greatly improving efficiency. For example, a U.S. Treasury token built on Ethereum could be instantly bought or transferred using USDC,不受banking hours. This enables 24/7 bond trading and instant settlement.

-

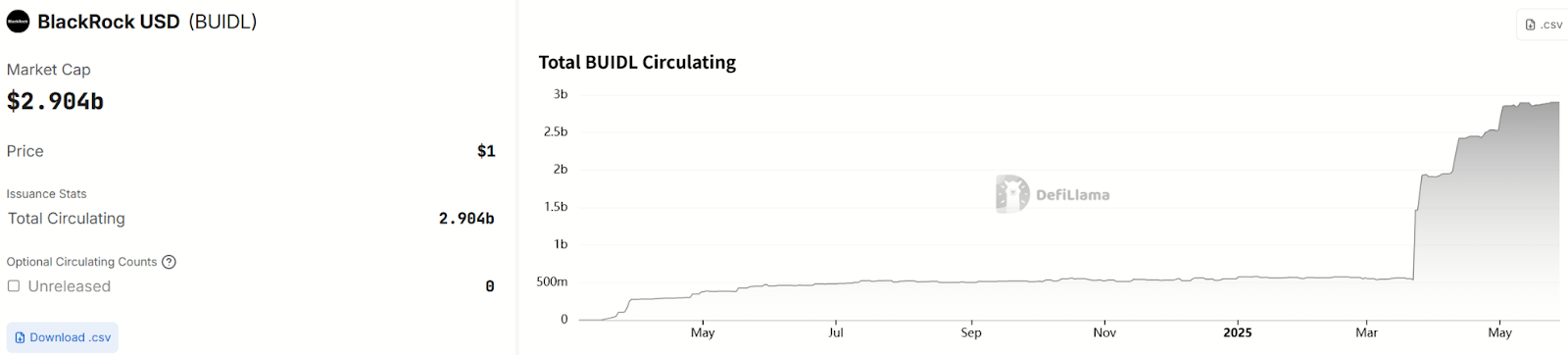

RWA Market Growth and Opportunities: Over the past two years, the RWA concept has gained traction in crypto, with many protocols attempting to bring U.S. Treasuries, corporate bonds, mortgages, and other assets on-chain into DeFi. Though still small in scale, growth has been rapid. BlackRock, the world’s largest asset manager, launched BUIDL—a tokenized money market fund—on Avalanche in March 2024. As of May 29, its assets exceeded $2.9 billion. MakerDAO plans to allocate up to $1 billion to purchase tokenized U.S. Treasuries, showing increasing institutional appetite for on-chain real assets. Major players are entering this emerging field: Goldman Sachs developing digital bond platforms, JPMorgan expanding its Onyx on-chain clearing network, SWIFT testing blockchain-based cross-border asset transfers—indicating exponential growth potential for the RWA market in the coming years.

Source:https://defillama.com/stablecoin/blackrock-usd

-

Risks and Challenges: Compliance costs pose a major bottleneck for RWA tokenization: auditing, reporting, and other requirements under the new stablecoin rules incur significant expenses, potentially burdening smaller innovators. Overly strict rules may stifle creative projects before launch. Additionally, RWA tokens involve unresolved technical and legal issues such as cross-chain governance and proof of legal ownership. If regulators lack flexibility in rulemaking, it could constrain the adaptability of RWA models.

It is foreseeable that more regulatory sandbox initiatives will emerge, allowing financial institutions to pilot various on-chain assets. Following stablecoin success, the next legislative focus may shift to security tokens, decentralized finance (DeFi), and other areas—further refining the digital asset regulatory framework.

VII. Conclusion: Digital Expansion of Dollar Sovereignty

The passage of the GENIUS Act marks not only the first time the U.S. establishes a stablecoin regulatory mechanism through federal law but also a rare strategic alignment between national will and market innovation. It signifies the formal recognition of stablecoins as critical financial infrastructure, building institutional bridges between crypto and traditional finance. From refinancing logic in the Treasury market to reshaping stablecoin competition and incentivizing RWA tokenization, the message sent by the GENIUS Act is clear: the dollar aims to dominate not only real-world settlement systems but also on-chain value flows. Stablecoins have become new “value extension tools” for the dollar, and control over their reserve allocation is emerging as a new lever in U.S. financial policy.

This “genius legislation” is not without flaws. Controversies and uncertainties remain regarding decentralized stablecoins, cross-border issuance oversight, and political neutrality. The ultimate impact—whether it becomes a true global standard or merely a “stablecoin enclave” within the U.S.—will depend on enforcement flexibility, market feedback, and international coordination post-implementation.

Nonetheless, this “genius bill” has legitimized stablecoins and taken a crucial step forward in U.S. digital financial regulation, accelerating broader legislative progress on DeFi, crypto securities, CBDCs, and other digital assets. The ultimate goal of this process extends beyond merely “regulating stablecoins”—it seeks to “stabilize the crypto world within regulation,” profoundly reshaping global financial market structures and the digital economy landscape for years to come.

About Us

Hotcoin Research, as the core research hub of the Hotcoin ecosystem, is dedicated to providing professional, in-depth analysis and forward-looking insights for global crypto investors. We build a three-in-one service system of “trend assessment + value discovery + real-time tracking,” delivering precise market interpretations and practical strategies through deep industry trend analysis, multidimensional project evaluations, and round-the-clock market volatility monitoring. With our weekly《Hotcoin Select》strategy livestreams and daily《Blockchain Headlines》briefings, we empower investors at all levels. Leveraging advanced data analytics models and extensive industry networks, we continuously help novice investors build cognitive frameworks and enable professional institutions to capture alpha returns, collectively seizing value growth opportunities in the Web3 era.

Risk Disclaimer

The cryptocurrency market is highly volatile and inherently risky. We strongly recommend investors fully understand these risks and conduct investments strictly within a sound risk management framework to ensure capital safety.

Website:https://lite.hotcoingex.cc/r/Hotcoinresearch

Mail:[email protected]

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News