Citigroup's Stablecoin Report: Digital Dollar, From Cypherpunks to Government Banks

TechFlow Selected TechFlow Selected

Citigroup's Stablecoin Report: Digital Dollar, From Cypherpunks to Government Banks

Driven by regulatory changes, 2025 could become the "ChatGPT moment" for blockchain applications in finance and the public sector.

Compiled & Translated by: Web3 Lawyer

The origins of public blockchain networks can be traced back to the release of the Bitcoin white paper in 2008 and the creation of the genesis block in 2009. However, the conceptual foundations of blockchain were actually being laid decades earlier, starting from the 1970s. Despite this long evolution, blockchain applications in finance and the public sector remain relatively limited so far.

The open-source and decentralized nature of blockchain is rooted in a core idea: mathematics and code can guarantee privacy and freedom. From its cypherpunk origins, blockchain is not merely a technological innovation—it carries strong political overtones, representing an anti-establishment philosophy that opposes existing institutions, whether banks or governments. Cypherpunks are a group advocating for social and political change through encryption technologies and privacy-enhancing tools.

Public-key cryptography first emerged in the mid-1970s, while hash functions and Merkle trees originated in the late 1970s. Meanwhile, the development of the modern internet is also noteworthy. In the 1980s, ARPANET began adopting TCP/IP protocols, and by the early 1990s, the World Wide Web was officially born. However, during the rapid growth of the internet in the 1990s, a key missing component was “digital money.”

The Bitcoin white paper released in 2008 proposed establishing a "peer-to-peer electronic cash system," a vision that gradually gained traction in the following years, leading to significant growth in Bitcoin adoption. As of April 2025, Bitcoin remains one of the dominant cryptocurrencies in the ecosystem, holding a market share as high as 64%.

In the 2020s, the narrative around blockchain has undergone an almost 180-degree shift. A movement once defined by anti-establishment ideals is now moving into the mainstream. Between 2023 and 2024, "real-world asset tokenization (RWA)" became one of the dominant narratives in the crypto ecosystem. By the end of March 2025, one of the largest holders of Bitcoin was the U.S. Bitcoin ETF fund. Additionally, other American institutions, including the U.S. government, ranked among the top ten Bitcoin holders. Just days before the inauguration of the 47th U.S. President in 2025, the $TRUMP meme coin launched on the Solana blockchain.

Stablecoins—digital currencies built on blockchain networks—have tremendous potential for growth. In recent years, stablecoin usage has already shown rapid expansion. It is expected that between 2025 and 2030, with increasing regulatory clarity—especially in the United States—the volume of stablecoin use could grow significantly further.

Moreover, public blockchains offer greater transparency and enhanced trust. Both wealthy and poorer nations see public institutions struggling to improve their trust ratings, precisely where the features of public blockchains are most needed. Blockchain adoption continues to advance alongside regulatory developments and rising demands for transparency and accountability.

This retrospective on blockchain history in 2025 leads us to ask: how should we look ahead to the future of stablecoins and blockchain? Citi GPS’s latest report, *Digital Dollars——Banks and Public Sector Drive Blockchain Adoption*, may offer answers, focusing particularly on two key areas: new financial instruments (e.g., stablecoins) and legacy system modernization.

Therefore, we have compiled a detailed translation of this report, especially its analysis of the “GPT moment” for stablecoins, which offers valuable insights.

Coincidentally, two years ago on Labor Day, we translated Citi GPS’s article titled *Money, Tokens, and Games (Blockchain's Next Billion Users and Trillions in Value)*, whose subtitle was *Blockchain's Next Billion Users and Trillions in Value*.

In its 2023 report, Citi predicted that by 2030, the billion users would come from: money, social, and gaming. Looking back from 2025, aside from the fleeting popularity of SocialFi and GameFi, this gap will instead be filled by users holding cryptocurrencies—or more specifically, stablecoins—thus forming the basis of Citi’s 2025 stablecoin research report.

The full text spans 18,000 words. Enjoy the following:

Key Takeaways

1. Driven by regulatory changes, 2025 could become the “ChatGPT moment” for blockchain adoption in finance and the public sector.

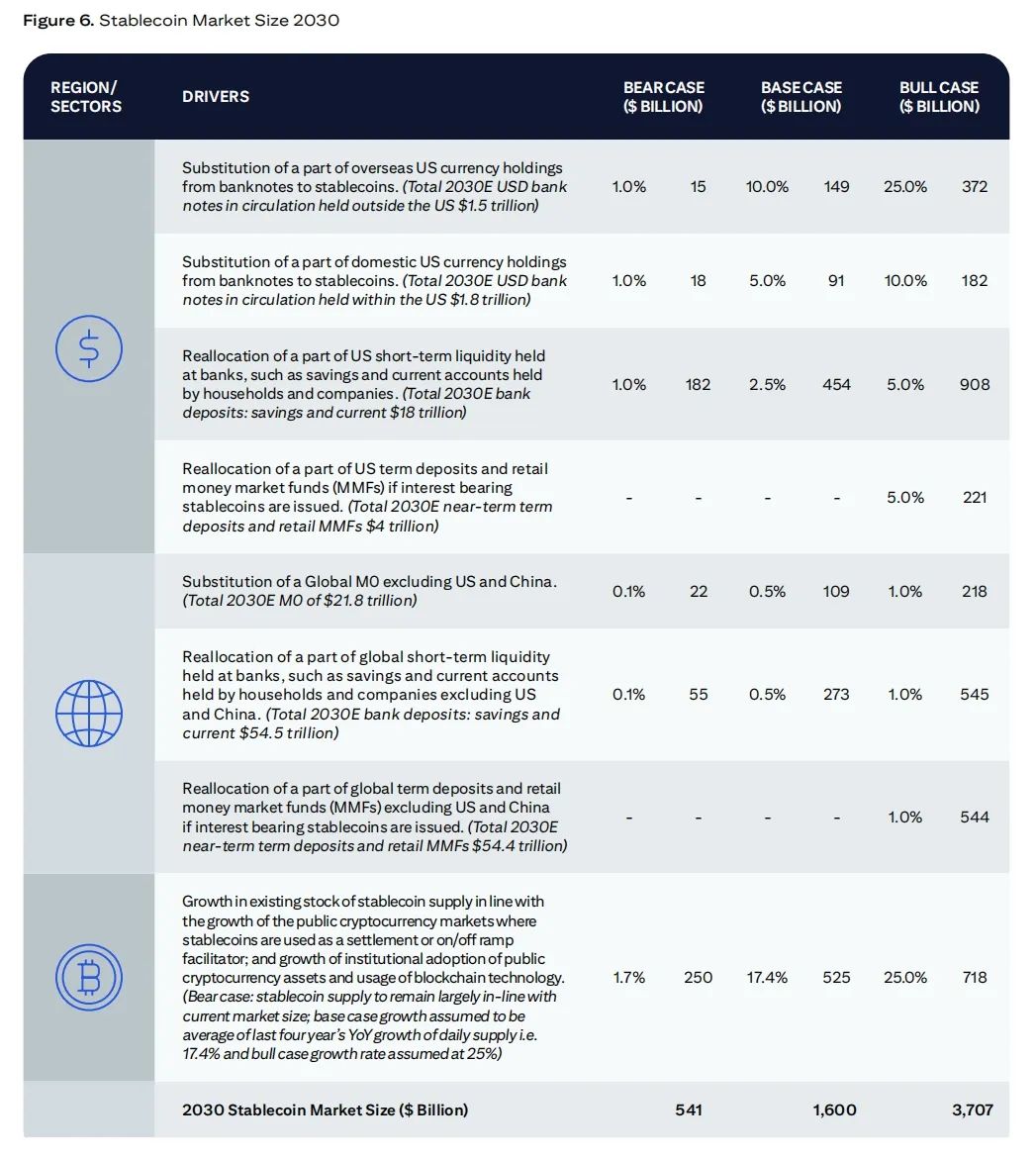

2. By 2030, total stablecoin circulating supply could reach $1.6 trillion under our base-case scenario and $3.7 trillion under the optimistic case. Even so, if integration challenges persist, it might settle closer to $500 billion.

3. We expect stablecoin supply to remain predominantly denominated in U.S. dollars (~90%), while non-U.S. nations promote central bank digital currencies (CBDCs) in their own currencies.

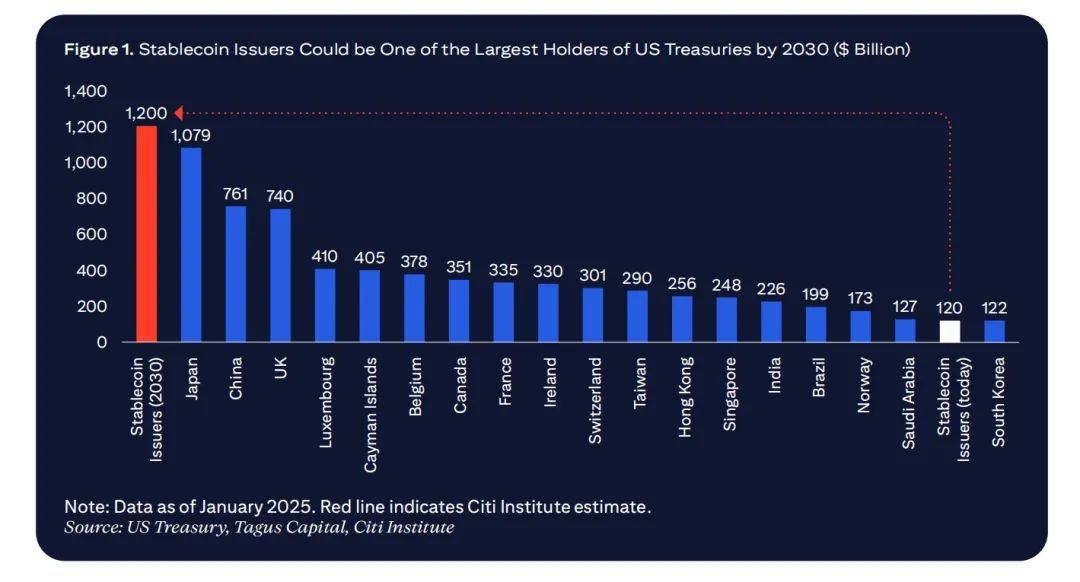

4. The U.S. stablecoin regulatory framework could drive net new demand for U.S. Treasuries, making stablecoin issuers one of the largest holders of U.S. debt by 2030.

5. Stablecoins pose some threat to traditional banking via deposit substitution but could also create new service opportunities for banks and financial institutions.

6. Public-sector interest in blockchain is growing, driven by persistent focus on transparency and accountability in public spending—evident in initiatives like the U.S. government’s DOGE (Department of Government Efficiency) and blockchain pilots led by central banks and multilateral development banks.

7. Key public-sector blockchain use cases include: expenditure tracking, subsidy disbursement, public records management, humanitarian aid operations, asset tokenization, and digital identity.

8. While initial on-chain transaction volumes in the public sector may be small and risks remain high and numerous, increased public-sector interest could signal broader blockchain adoption.

1. Why Now for Mass Blockchain Adoption?

Why might 2025 be the “ChatGPT moment” for blockchain in finance and the public sector?

-

A supportive stance from U.S. regulators is expected to transform the industry landscape, potentially accelerating the adoption of blockchain-based money and stimulating additional use cases across both private and public sectors in the U.S.

-

Another potential catalyst is sustained attention to transparency and accountability in public spending.

These shifts build upon developments over the past 12–15 months, including the EU’s Markets in Crypto-Assets (MiCA) regulation, growing user demand reflected in crypto ETF launches, institutionalization of crypto trading and custody, and the U.S. government building a strategic Bitcoin reserve.

Although participation in blockchain by banks, asset managers, public-sector entities, and government agencies has increased, it still lags behind some optimistic projections. The reality is: digital finance already exists atop proprietary databases and centralized systems such as internet banking. We are now witnessing accelerated convergence between internet-native technology, money, and blockchain-native use cases.

Government blockchain adoption falls into two categories: enabling new financial tools and modernizing systems. Systems are upgraded by integrating shared ledgers to enhance data synchronization, transparency, and efficiency.

Stablecoin issuers are currently major holders of U.S. Treasuries and beginning to influence global financial flows. The growing popularity of stablecoins reflects sustained demand for dollar-denominated assets.

Artem Korenyuk, Digital Assets – Client, Citi

1.1 The Rise of Stablecoins

Stablecoins are cryptocurrencies pegged to stable assets such as the U.S. dollar. A key driver for broader acceptance may be clearer U.S. regulation, which could help integrate stablecoins—and blockchain more broadly—into the existing financial system.

Given the U.S. dollar’s dominance in international finance, changes in U.S. policy toward stablecoins will impact the broader global system.

The U.S. government appears eager to foster domestic digital asset industries as part of its focus on enhancing innovation and efficiency. In January 2025, a U.S. presidential executive order titled “Strengthening American Leadership in Digital Financial Technology” established a digital asset task force responsible for developing a federal regulatory framework for the industry.

In this regulatorily favorable environment, digital assets are increasingly converging with existing financial institutions, laying the groundwork for stablecoin growth—further supported by macroeconomic factors such as emerging and frontier markets’ demand for the U.S. dollar.

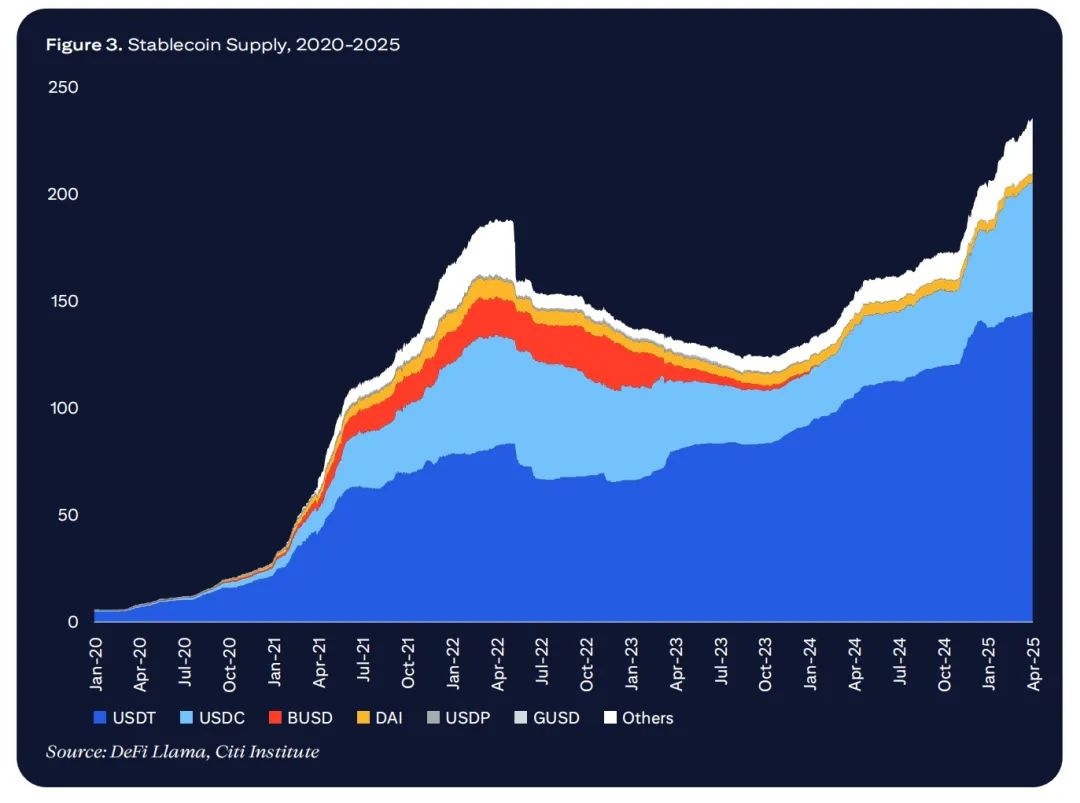

According to DefiLlama data, as of end-March 2025, the total value of stablecoins exceeded $230 billion—30 times higher than five years ago. This partly reflects overall growth in cryptocurrency market value (up 1400% over five years as of end-March 2025) and rising institutional demand. Our analysis suggests that under a base case, total stablecoin supply could reach $1.6 trillion, ranging from ~$0.5 trillion in a bear case to $3.7 trillion in a bull case.

U.S. Treasury Demand: Establishing a U.S. stablecoin regulatory framework would support domestic and international demand for risk-free dollar assets. Stablecoin issuers must purchase U.S. Treasuries or similar low-risk assets as proof of secure backing. In the base case, we project over $1 trillion in U.S. Treasury purchases. By 2030, stablecoin issuers could hold more U.S. Treasuries than any single jurisdiction currently does.

1.2 Future Challenges

Stablecoins face resistance and challenges. Although the dollar’s dominance may evolve over time—with the euro or other currencies promoted via national regulations—many non-U.S. policymakers may view stablecoins as tools of dollar hegemony.

Blockchain aims to align monetary flows with the speed of the internet and global commerce. Stablecoins can be key enablers. The first step is legislative and regulatory clarity, supplemented by legal safeguards.

Ryan Rugg, Digital Assets – Services, Citi

Geopolitical tensions remain volatile. If the world moves toward a multipolar system, Chinese and European policymakers will likely push for CBDCs or domestically issued stablecoins. Policymakers in emerging and frontier markets will also remain cautious about local risks associated with dollarization.

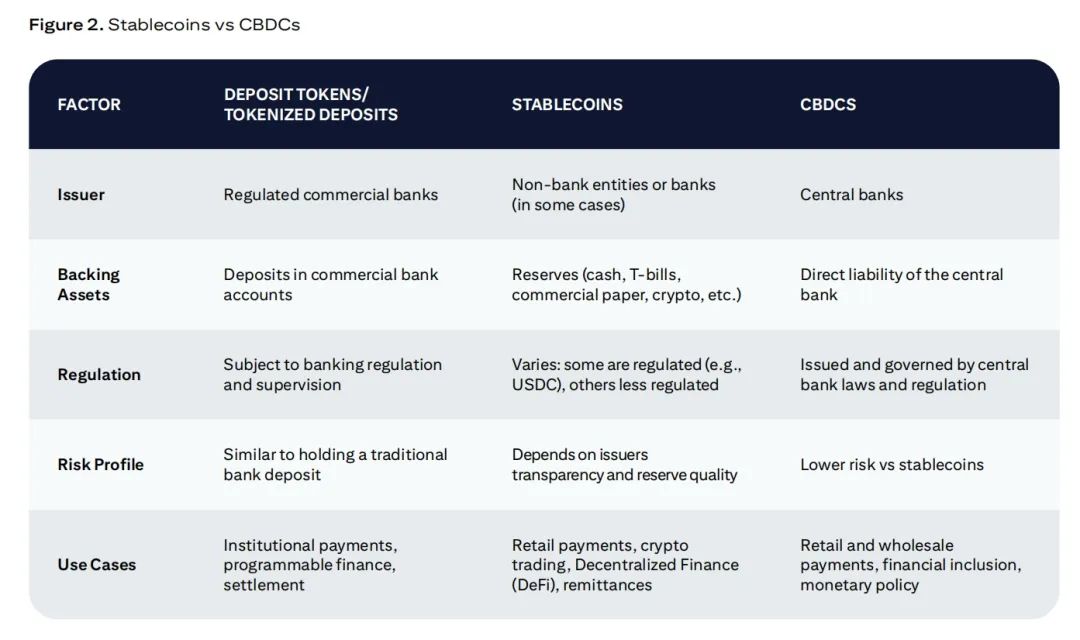

Both stablecoins and central bank digital currencies (CBDCs) represent attempts to create digital money, but differ in technical architecture and governance. CBDCs are issued by central banks, whereas private entities issue stablecoins. CBDCs are often inspired by blockchain principles but typically do not run on public chains. Given the demand for dollars in wholesale and financial transactions—especially in jurisdictions with volatile currencies—stablecoins may play the role of Eurodollar 2.0.

Hence, we expect the stablecoin market to remain dollar-dominated in the coming years. In the base case, we project ~90% of stablecoin supply to be dollar-denominated by 2030, down from nearly 100% today.

Stablecoins carry run risks and potential spillover effects. In 2023, stablecoins depegged approximately 1,900 times, with around 600 involving large-cap coins. Major depegging events could suppress liquidity in crypto markets, trigger automatic liquidations, weaken exchange redemption capacity, and potentially cause broader financial contagion. For example, news of Silicon Valley Bank’s collapse in March 2023 triggered massive redemptions of USDC.

A recent Galaxy Digital report noted that Tether provided about $8 billion in loans—roughly 25% of total crypto lending—and warned that if Tether used customer deposits for these loans, it “would violate fractional banking principles and pose serious systemic risks.”

Note: Tokenized deposits represent commercial deposits on-chain, each backed by retail or institutional deposits. Deposit tokens are native blockchain tokens directly representing retail or institutional deposits. Most bank projects to date fall under “tokenized deposits.” Deposit tokens are mostly in pilot or early stages—for example, Guardian, Regulated Liability Network (RLN), or Helvetia projects.

1.3 Does the Public Sector Need Blockchain?

Trust and transparency are critical to maintaining public support for governments and institutions.

Trust is the new currency of government—they need to build confidence and trust with citizens. Governments can continue using centralized databases and traditional software solutions, but they may miss out on fundamental transformations enabled by blockchain.

Saqr Ereiqa, Secretary General, Dubai Digital Asset Association

Blockchain introduces a decentralized, trust-based approach to public-sector data management. Traditional systems derive trust from authority—such as a government verifying its own records—whereas blockchain enables cryptographic proof of authenticity. Trust is rooted in the technology itself.

Immutability ensures that once information is recorded, it cannot be altered, providing tamper-proof records for sensitive public data such as land registries, voting systems, and financial transactions. While other technologies can achieve immutability, they often rely on trusted third parties.

Cross-border activities—especially international fund transfers through institutions like the World Bank or humanitarian aid programs—are important use cases for blockchain. International flows can lack transparency and make it difficult to verify whether resources reached intended recipients. Blockchain can bring transparency to complex transactions, even in remote or unstable regions where financial infrastructure is weak.

Building blockchain when a simple database suffices is like driving a Ferrari to the corner store—expensive, inefficient, and unnecessary. If all inputs and outputs are controlled by a single entity, blockchain offers no real advantage. Its true value emerges only when trustless value exchange is required.

Artem Korenyuk, Digital Assets – Client, Citi

1.4 Expert Perspectives

A. The Digital Trust Revolution

Siim Sikkut served as Chief Information Officer for the Estonian government (2017–2022) and is now a member of the Estonian President’s Digital Advisory Council. He is also Executive Partner at Digital Nation.

Q: What prompted Estonia to adopt blockchain?

Estonia’s digital transformation stemmed from practical necessity. As a small country with just over a million people, efficiency and productivity were crucial. In the late 1990s, with the rise of the internet, Estonia began experimenting with digital solutions in government and banking.

These early efforts demonstrated clear advantages, allowing the country to operate beyond its physical size and resource constraints. This success led Estonia to strategically commit to digital innovation. Estonia adopted an iterative approach—testing emerging technologies, identifying what worked, and scaling successful solutions. This method gave rise to pioneering initiatives like online voting and e-residency, initially experimental but now integral parts of Estonia’s digital infrastructure. Blockchain followed a similar path. Estonia did not adopt blockchain in response to a crisis, but to ensure efficient digital governance.

Q: How does Estonia use blockchain in government operations, and why?

Estonia primarily uses blockchain to ensure data integrity within government systems. The key challenge is maintaining trust—ensuring citizens can rely on the security and accuracy of their data. While encryption and cybersecurity address confidentiality and availability, governments need a solution to verify the integrity of their records.

The critical question: How can you trust system administrators and their log files?

In the early 2000s, Estonia adopted a custom blockchain—KSI (Keyless Signature Infrastructure)—as an additional layer of trust. Today, it is applied to various government databases, including the national health registry.

Notably, blockchain does not store actual records but logs metadata about who accessed or modified a record and when. For example, it doesn’t store a person’s blood type but records when and by whom that entry was accessed or changed. This approach has two key benefits: it protects user privacy and ensures regulatory compliance. Also, storing large datasets on-chain is impractical from cost and performance perspectives.

Q: What potential use cases do you see for blockchain in the future?

A promising area is digital documents, where blockchain can enhance the security, transparency, and efficiency of welfare, grants, and public resource allocation. By providing an immutable ledger, blockchain can reduce fraud, strengthen accountability, and enable seamless cross-institutional verification.

Another potential application is managing and safeguarding stored value, particularly in government programs distributing fiscal aid or subsidies. Tokenization also holds promise, especially for government departments involved in fiscal redistribution.

B. Holistic Digital Policy

Julie Monaco is Global Head of Public Sector Banking at Citibank.

Q: What does a successful national digital policy look like?

A successful national digital policy is not just about technology—it’s about vision and goals. It starts with bold leadership and a commitment to building an inclusive, human-centered digital economy. Appointing a digital czar to coordinate priorities across AI, data privacy, and cybersecurity is essential.

Strategic investment in digital ID systems could unlock access for 1.7 billion people, save 110 billion labor hours annually, and add 6% to emerging market GDP. According to Juniper Research, 3.6 billion people globally are already registered—a strong momentum. Countries like Estonia, India, and Singapore demonstrate what’s possible when policy drives innovation.

Q: What role should blockchain play as part of a successful digital policy in achieving accountability, transparency, and efficiency?

Blockchain absolutely has a role in successful digital policy, especially in enhancing accountability, transparency, and efficiency. By creating immutable records and automating audit trails via smart contracts, blockchain could reduce fraud, improve regulation, and build trust in public systems. On efficiency, it can streamline services like tax collection or benefit distribution by reducing bureaucracy.

But it’s not a panacea. If applied wisely, however, blockchain can be a powerful tool helping governments operate with greater integrity, responsiveness, and efficiency.

2. The Stablecoin GPT Moment

2.1 How Do Stablecoins Work?

Stablecoins are cryptocurrencies designed to maintain stable value by pegging their market value to underlying assets. These assets can include fiat currencies (e.g., USD), commodities (e.g., gold), or baskets of financial instruments.

Key components of the stablecoin ecosystem include:

-

Stablecoin Issuers: Entities that issue stablecoins and manage their underlying assets, typically holding value equivalent to the circulating supply of stablecoins.

-

Blockchain Ledger: After issuance, stablecoin transactions are recorded on a blockchain ledger, providing transparency and security by tracking ownership and flow among users.

-

Reserves and Collateral: Reserves ensure each token can be redeemed at its pegged value. For fiat-backed stablecoins, reserves typically include cash, short-term government bonds, and other liquid assets.

-

Digital Wallet Providers: Offer digital wallets—mobile apps, hardware devices, or software interfaces—that allow stablecoin holders to store, send, and receive their currency.

How Do Stablecoins Maintain Their Peg?

Stablecoins rely on different mechanisms to keep their value aligned with the underlying asset. Fiat-backed stablecoins maintain their peg by ensuring every issued token can be exchanged for an equivalent amount of fiat currency.

Major Stablecoins in the Market

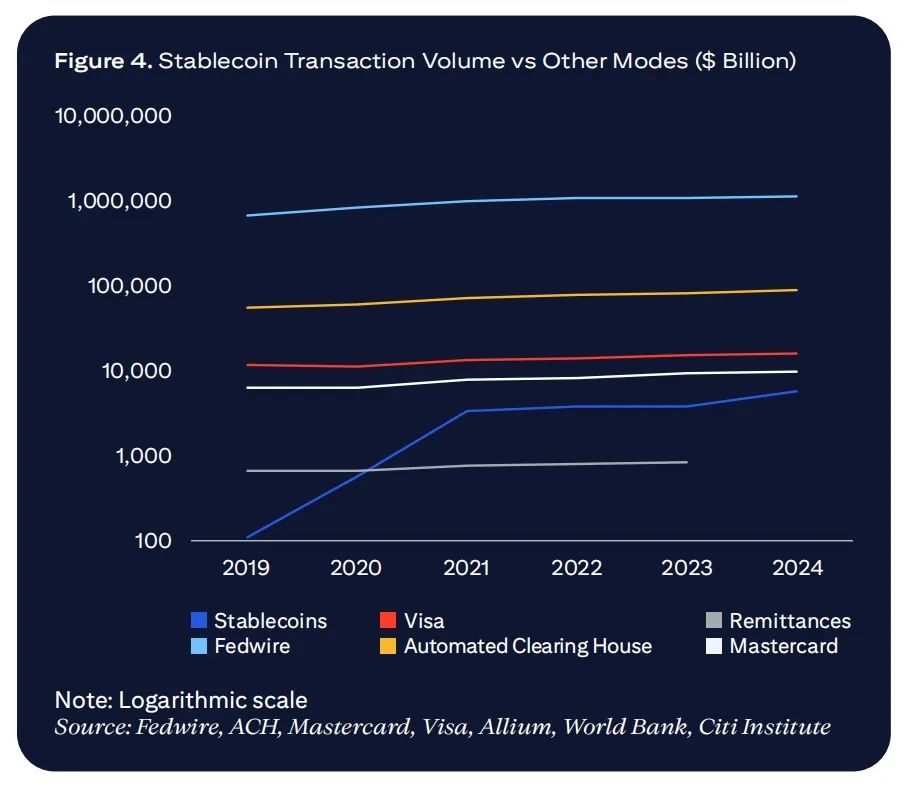

As of April 2025, total stablecoin circulation exceeds $230 billion—an increase of 54% since April 2024. The top two stablecoins dominate the ecosystem, accounting for over 90% of market value and transaction volume, with Tether (USDT) leading, followed by USD Coin (USDC).

Stablecoin transaction volumes have grown rapidly in recent years. Adjusted by Visa Onchain Analytics, Q1 2025 saw monthly stablecoin transaction volumes of $650–700 billion—about double the levels seen from H2 2021 to H1 2024. Transactions supporting the crypto ecosystem remain the primary use case for stablecoins.

The largest stablecoin by market cap, USDT, launched on the Bitcoin blockchain in 2014 and expanded to Ethereum in 2017, enabling DeFi applications. In 2019, due to faster speeds and lower costs, USDT expanded to the Tron network, widely used in Asia. USDT primarily operates overseas—but times are changing.

We will certainly see more participants—especially banks and traditional players—entering the market. Dollar-backed stablecoins will continue to dominate. Ultimately, the number of participants will depend on how many distinct products are needed to cover major use cases—and there may be more players than in the credit card network market.

Matt Blumenfeld, Global and U.S. Digital Assets Lead, PwC

2.2 Drivers of Stablecoin Adoption

According to Erin McCune, Founder & Principal Consultant, Forte FinTech, the drivers of stablecoin adoption are:

-

Practical Advantages (speed, low cost, 24/7 availability) are creating demand in both developed and emerging economies. Especially in countries where instant payments aren't widespread, underserved SMEs and multinational corporations seeking easier global treasury management drive demand. Cross-border transaction costs remain high in these countries, with immature banking tech and/or lagging financial inclusion.

-

Macro Needs (inflation hedging, financial inclusion) are driving stablecoin adoption in high-inflation regions. Consumers in Argentina, Turkey, Nigeria, Kenya, and Venezuela use stablecoins to protect their savings. Increasingly, remittances are sent in stablecoins, enabling unbanked consumers to access digital dollars.

-

Recognition and integration by existing banks and payment providers are key to legitimizing stablecoins (especially for institutional and corporate users) and can rapidly expand their usability and reach. Mature, scaled payment network operators and core processors can improve transparency and facilitate integration with digital solutions relied upon by businesses and merchants. Clearing mechanisms between various stablecoins—between banks and non-banks—are also crucial for scalability. Technical improvements—user-friendly wallets for consumers and merchant platforms embedding stablecoin acceptance via APIs—are removing barriers that once confined stablecoins to crypto’s fringes.

-

Long-awaited regulatory clarity will allow banks and the broader financial services industry to introduce stablecoins in retail and wholesale contexts. Transparency (audit requirements) and consistent liquidity management (reliable par value) will also simplify operational integration.

Matt Blumenfeld, Global and U.S. Digital Assets Lead, PwC, notes the following drivers:

-

User Experience: The global payments landscape is shifting toward real-time digital transactions. But adoption of each new payment method faces UX challenges—intuitiveness, visibility of use cases, and clarity of value. Any institution that successfully enhances user experience—whether for retail or institutional users—will emerge as a leader in its domain.

Integration with today’s payment methods will drive the next wave of adoption. For retail, this means integration into cards or mobile wallets. For institutions, it means simpler, more flexible, and cost-effective settlement.

-

Regulatory Clarity: Post-introduction of new stablecoin regulations, we’ve seen severe suppression of innovation and adoption due to global regulatory uncertainty. The rollout of MiCA, Hong Kong’s regulatory clarity, and progress on U.S. stablecoin legislation have triggered surges in activity aimed at streamlining institutional and consumer fund flows.

-

Innovation and Efficiency: Institutions must view stablecoins as catalysts for more agile product development—something hard to achieve today. This means offering a simpler, more creative, or more appealing medium to enhance traditional bank deposits, for example, through yield generation, programmability, and composability.

2.3 Potential Stablecoin Market Size

As noted by Forte Fintech’s Erin McCune, any forecast of stablecoin market potential must be approached cautiously. The market is highly volatile, and our own analysis shows wide ranges.

We constructed a range of forecasts based on the following demand drivers:

-

Converting part of U.S.-based and offshore U.S. dollar holdings from paper currency to stablecoins—offshore-held U.S. cash is often a hedge against local volatility, and stablecoins offer a more convenient way to access such hedges. Domestically, stablecoins could partially serve certain payment functions and be held accordingly.

-

Reallocating part of U.S. and international household and corporate short-term dollar liquidity into stablecoins to support cash management and payment operations. Stablecoins are easy to use (e.g., 24/7 cross-border payments) and, if regulations permit, could partially substitute yield-bearing assets.

-

Additionally, we assume similar trends for euro/pound short-term liquidity substitution by domestic households and enterprises, though on a much smaller scale. In the base case, we project the 2030 optimistic scenario still sees the market primarily driven by the dollar (~90%).

-

Growth in public crypto markets, where stablecoins facilitate settlement or currency clearing; partly driven by rising institutional adoption of public crypto assets and broader blockchain use. In our base case, we assume the issuance trend observed from 2021 to 2024 continues.

-

Our base-case estimate for stablecoin market size in 2030 is $1.6 trillion, optimistic case $3.7 trillion, and pessimistic case $0.5 trillion.

Note: 2030 currency stock estimates (cash in circulation, M0, M1, M2) calculated using nominal GDP growth rates. Eurozone and UK may issue and adopt local-currency stablecoins. China may adopt sovereign CBDC and is less likely to adopt foreign privately issued stablecoins. 2030 non-dollar stablecoin bear case: $21B; base case: $103B; bull case: $298B.

2.4 Stablecoin Market Outlook and Use Cases

Erin McCune is Founder and Principal Consultant at Forte Fintech, with over 25 years of consulting experience in payments. Her work focuses on commercial payments, cross-border transactions, and intersections of corporate finance, banking, and enterprise software. Prior to founding Forte Fintech, she was a partner at Bain & Company and Glenbrook Partners.

Q: What are optimistic and cautious outlooks for near-term stablecoin market size and key growth drivers?

Predicting global stablecoin market growth requires great confidence (or hubris), given many unknowns. Based on this, I offer the following optimistic and pessimistic scenarios:

The most optimistic scenario sees the market expand 5–10x as stablecoins become everyday media for instant, low-cost, frictionless global transactions. A relatively optimistic projection is that by 2030, stablecoin value grows exponentially from today’s ~$200 billion to $1.5–2.0 trillion, penetrating global trade payments, P2P remittances, and mainstream banking.

This optimism relies on several key assumptions:

-

Supportive regulatory environments in key regions—not only North America and Europe but also markets with high demand for local fiat alternatives, such as Sub-Saharan Africa and Latin America.

-

Genuine trust between incumbent banks and new entrants, and broad confidence among consumers and businesses in stablecoin reserve integrity (e.g., 1 USD stablecoin = 1 USD in high-quality fiat reserves).

-

Reasonable revenue sharing across the value chain to encourage cooperation; and

-

Widespread adoption of technologies connecting old and new infrastructures, promoting structural efficiency and scalability. For example, merchant acquirers have begun using stablecoins. For wholesale use, corporate treasury and AP solutions, and commercial banks need adaptation. Banks will need to deploy tokenization and smart contracts.

In the pessimistic scenario, stablecoin use remains confined to the crypto ecosystem and specific cross-border use cases (mainly illiquid money markets, currently a tiny fraction of global GDP). Geopolitical tensions, resistance to digital dollarization, and widespread CBDC adoption would further hinder stablecoin growth. In this case, stablecoin market cap might stabilize between $300–500 billion, playing a limited role in the broader economy.

Factors contributing to a more pessimistic outcome:

-

If one or more major stablecoins suffer reserve failures or depegs, severely undermining trust among retail investors and businesses.

-

High friction and cost in using stablecoins for daily shopping—whether remittance recipients can’t buy groceries, pay tuition, or rent, or businesses can’t easily use funds for payroll or inventory.

-

Retail CBDCs haven’t gained traction yet, but in regions where public-sector digital cash alternatives can scale, stablecoins may be less relevant.

-

In areas where stablecoins gain attention and weaken local fiat correlation, central bankers may respond with tighter regulation.

-

If fully reserved stablecoins grow large enough, they could “lock up” substantial safe assets, potentially constraining economic credit.

Q: What are current and future stablecoin use cases?

Like any payment method, stablecoin relevance and potential growth must be assessed by use case. Some are well-established, others remain theoretical or clearly impractical. Below are current (or near-future) use cases contributing to stablecoin transaction volume (from largest to smallest):

-

Crypto Trading: Individuals and institutions using stablecoins to trade digital assets is currently the largest use case, accounting for 90–95% of stablecoin transaction volume. Much of this activity is driven by algorithmic trading and arbitrage. In maturity, given continued crypto market growth and reliance on stablecoin liquidity, trading (retail + DeFi) may still account for ~50% of stablecoin usage.

-

B2B Payments (Corporate Payments): According to Swift, most traditional correspondent banking transactions now arrive within minutes via Swift GPI. But this mainly occurs between centralized banks, in liquid currencies, and during banking hours. Significant inefficiencies and unpredictability remain, especially when operating in middle- and low-income countries. Businesses using stablecoins to pay overseas suppliers and manage treasury operations could capture a significant share. Given global B2B flows in the tens of trillions, even a small shift to stablecoins could represent 20–25% of total stablecoin market size in the long run.

-

Consumer Remittances: Despite steady migration from cash to digital, regulatory pressure, and focused efforts by new entrants, remittances by overseas workers to families remain costly (averaging 5% on $200 transactions—five times the G20 target). With lower fees and faster speeds, stablecoins are poised to capture a significant share of the ~$1 trillion remittance market. If promised instantaneity and cost reductions materialize, high-adoption scenarios could see stablecoins claim 10–20% market share.

-

Institutional Trading and Capital Markets: Use cases for stablecoins in professional investor trading or tokenized securities settlement are expanding. Large capital flows (FX, securities settlement) could begin using stablecoins to accelerate settlement. Stablecoins could also streamline funding for retail stock and bond purchases, currently handled via batch ACH processing. Major asset managers have started piloting stablecoin settlements for funds, laying the foundation for broader capital market use. Given the scale of inter-institutional payments, even modest adoption could represent 10–15% of the stablecoin market.

-

Interbank Liquidity and Funding: Banks and financial institutions using stablecoins for internal or interbank settlement represent a small share but could have outsized impact (likely less than 10% of total market size). Industry leaders like JPMorgan have launched blockchain projects with daily transaction volumes exceeding $1 billion, demonstrating huge potential despite regulatory opacity. This segment could grow substantially, though overlapping with above institutional uses.

2.5 Stablecoins: Cards, CBDCs, and Strategic Autonomy

We believe stablecoin usage will grow, creating space for new entrants. The current duopoly among issuers may persist offshore, but onshore markets in each country could provide platforms for new players.

Just as the card market evolved over the past 10–15 years, the stablecoin market will change. Stablecoins share similarities with card networks or cross-border banking—industries with strong network/platform effects and reinforcing loops. More merchants accepting a trusted brand (Visa, Mastercard) attract more cardholders. Stablecoins exhibit similar usage loops.

In larger jurisdictions, stablecoins have often operated without financial regulation, but this is changing in the EU (MiCA, 2024) and the U.S. (ongoing). Stricter financial regulation and high partner costs may lead to consolidation among stablecoin issuers, as seen in credit card networks.

Ultimately, having a few select stablecoin issuers benefits the broader ecosystem.

While a couple of dominant players may seem concentrated, too many stablecoins lead to fragmentation and non-interchangeable forms. Stablecoins thrive only with scale and liquidity.

Raj Dhamodharan, Executive Vice President, Blockchain & Digital Assets, Mastercard

However, evolving politics and technology have increased differentiation in the card market—especially outside the U.S. Could the same happen with stablecoins?

Many countries have launched national card schemes—Brazil’s Elo (2011), India’s RuPay (2012), etc.—often driven by sovereignty concerns, local regulatory shifts, and political encouragement from domestic financial institutions. They’ve also integrated with new national real-time payment systems like Brazil’s Pix and India’s UPI. While international card schemes continue growing, they’ve lost market share in many non-U.S. markets. Technological shifts have fueled digital wallets, account-to-account payments, and super-apps—all contributing to declining credit card share.

Just as we’ve seen a surge in national card programs, we’re likely to see jurisdictions outside the U.S. continue prioritizing CBDC development as tools for national strategic autonomy—especially in wholesale and corporate payments.

An OMFIF survey of 34 central banks found 75% still plan to issue CBDCs. The share expecting issuance within three to five years rose from 26% in 2023 to 34% in 2024. Yet, practical hurdles are emerging—31% of central banks delayed timelines due to legislative needs or desire to explore broader solutions.

CBDC projects began in 2014 when the People’s Bank of China (PBoC) started researching digital yuan. Coincidentally, Tether was also founded that year. In recent years, private-market forces have propelled rapid stablecoin growth.

In contrast, CBDCs largely remain in official pilot phases. A few small economies that launched national CBDC projects have not seen organic user growth. However, rising geopolitical tensions may boost interest in CBDCs.

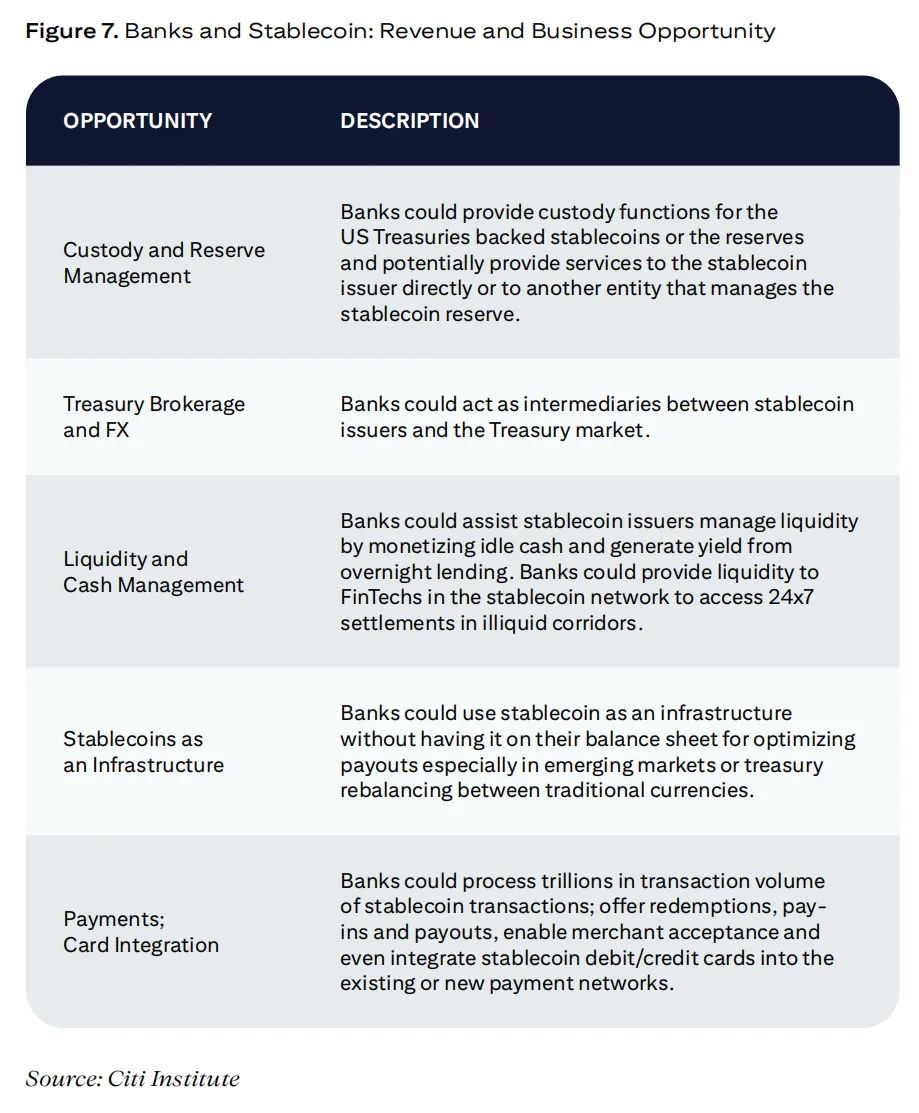

2.6 Stablecoins and Banks: Opportunities and Risks

Adoption of stablecoins and digital assets presents new business opportunities for some banks and financial institutions, driving revenue growth:

Role of Banks in the Stablecoin Ecosystem

Banks have many opportunities to participate in stablecoin development, continuing to act as hubs for monetary flows. This includes direct issuance, involvement in payment rails/solutions, structured products around stablecoins, general liquidity provision, or indirect roles.

As users seek better products and experiences, we’ve seen deposits flowing out of the banking system. With stablecoin technology, banks have a chance to create superior products and experiences while keeping deposits within the banking system—where users generally prefer their funds to be safeguarded.

Matt Blumenfeld, Global and U.S. Digital Assets Lead, PwC

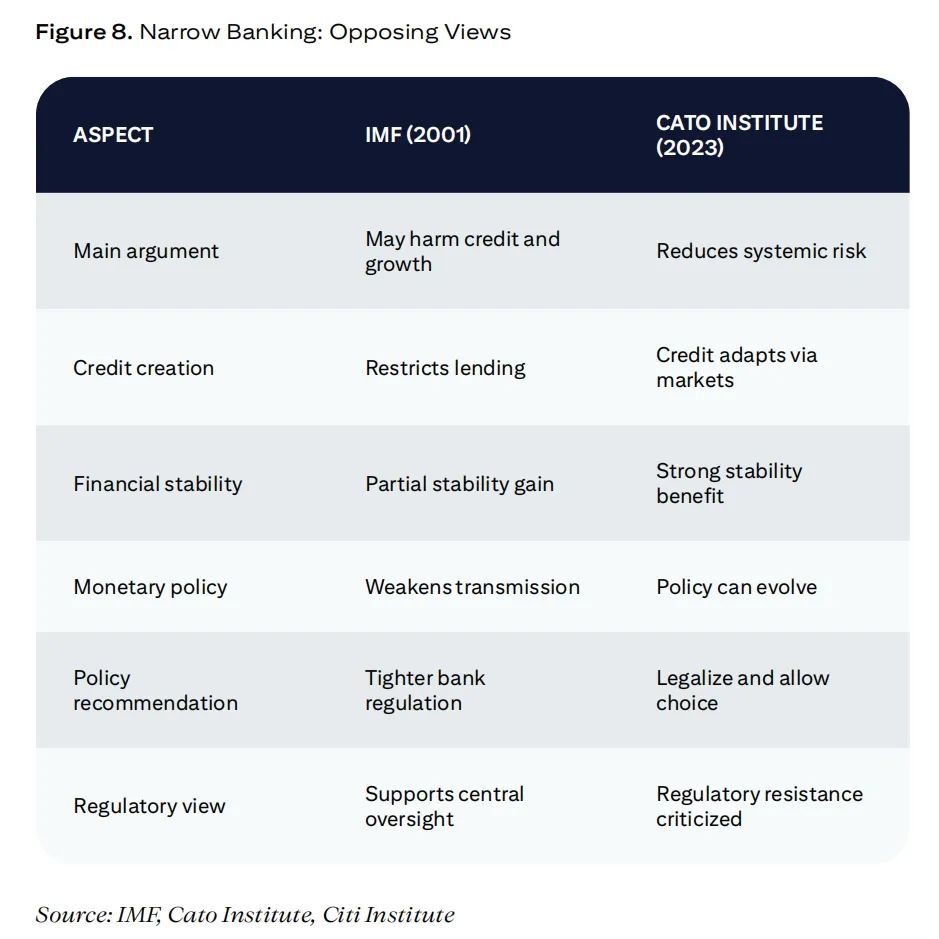

At a systemic level, stablecoins may produce effects similar to “narrow banking,” and debates over such models have long existed in policy circles. The shift of bank deposits to stablecoins could affect banks’ lending capacity. This reduction in lending may dampen economic growth—at least during the transitional adjustment period.

As summarized in IMF Paper No. 9 (2001), traditional economic policy opposes narrow banking due to concerns over credit creation and growth. However, reports from the Cato Institute (2023) and similar institutions argue that “narrow banking” could reduce systemic risk, with credit and other flows adapting accordingly.

3. Public-Sector Perspectives on Blockchain

Trust and transparency are blockchain’s core strengths in the public sector. Blockchain holds immense potential to replace existing centralized systems, improving operational efficiency, enhancing data protection, and reducing fraud.

While public-sector on-chain transaction volumes may initially be smaller than those in the private sector, growing public-sector interest is crucial for broader blockchain adoption.

3.1 Public Spending and Fiscal Management

Blockchain technology has the potential to transform public spending and fiscal management in government services by enhancing transparency, efficiency, and accountability, while significantly reducing reliance on manual and paper-based processes. By integrating financial and non-financial reporting across government agencies and external partners, blockchain enables real-time expenditure tracking.

This should reduce corruption risks and enhance public trust in public institutions. The immutability of blockchain records ensures traceability and verifiability of transactions, simplifying audits and strengthening accountability. Blockchain also allows real-time monitoring of fiscal allocations and provides data-driven insights to assess the impact of public spending.

Smart Contract Applications can improve procurement process efficiency by automating bidding, evaluation, and contract awarding. This reduces human intervention and increases transparency in contract awards, addressing common biases and favoritism in manual selection. Contract payments can also be disbursed in stages tied to milestones, ensuring funds are released only upon achievement of project deliverables.

Integrating blockchain into accounting systems can streamline tax administration and compliance, automating tax calculations and remittances to governments. Since all transactions are permanently recorded on the blockchain, tax evasion becomes more difficult, strengthening tax enforcement.

Blockchain-based digital bonds can also enable faster, more transparent issuance through automated interest payments. They allow fractional ownership, broadening investor participation. Real-time tracking of debt instruments throughout their lifecycle further enhances accountability and investor confidence.

Beyond improving efficiency and accountability, digitizing government services via blockchain can reduce the vast amounts of paper used annually in contracts, records, and transactions. For example, Dubai’s “Paperless Strategy” aims to eliminate billions of sheets of paper annually by digitizing all services—including visa applications, bill payments, and license renewals—securely transacted via blockchain technology.

3.2 Disbursement of Public Funds and Grants

Traditional processes for disbursing government and public-sector funds and grants typically involve extensive manual work—processing forms, verifying claims, and managing cash flows. Blockchain offers a more efficient alternative, streamlining processes and enhancing data security and integrity. Using blockchain can also improve transparency, ensure fair distribution of funds, and reduce opportunities for corruption and fraud. Blockchain can also lower operational costs and improve efficiency in recordkeeping and reconciliation.

Hashed data is integrated into blockchain systems to enhance transaction integrity and prevent unauthorized access. Smart contracts can automate and secure disbursement processes by programming predefined conditions—such as verifying eligibility criteria.

Blockchain technology is well-suited for cross-border applications in many ways. The World Bank’s “FundsChain” initiative, launched in September 2024, is a prime example. The initiative currently runs nine projects in Moldova, the Philippines, Kenya, Bangladesh, Mauritius, and Mozambique.

FundsChain—World Bank’s Blockchain for Tracking Fund Disbursements

The World Bank disburses billions of dollars annually and must ensure funds are used for their intended purposes. With numerous projects across multiple countries, tracking and verifying fund usage has traditionally been a time-consuming manual process. While some tasks are automated, most oversight still requires significant labor. The FundsChain initiative aims to improve transparency and efficiency in fund disbursement.

The World Bank partnered with EY to develop a blockchain-based platform to track fund flows and expenditures in real time. FundsChain provides robust fund-tracking capabilities, enabling stakeholders to view funds in real time, increasing transparency and confidence, ensuring funds truly reach intended beneficiaries, and ultimately helping the World Bank support anti-corruption reform agendas in borrowing countries.

Tokens are generated when funds are credited. These tokens are deposited into each entity’s digital wallet. Transaction automation via smart contracts improves efficiency; security and data integrity are further enhanced by storing and notarizing uploaded resources on the blockchain. Consensus algorithms validate transactions and prevent overspending.

Currently, oversight is achieved by requiring borrowers to submit expense reports and other supporting documents—a highly manual, labor-intensive, and time-consuming process requiring significant coordination, time, and cost. With FundsChain, all project stakeholders—including borrowers, suppliers, auditors, and end beneficiaries—can see where funds go, how they are used, and when, enabling end-to-end transparency. All transactions are recorded on-chain, allowing stakeholders to monitor fund flows in real time.

The World Bank built FundsChain on a private blockchain because it wants control over the platform and its future development. Given the sensitivity of its public-sector mission, it does not want to rely on third-party vendors. It also wants to ensure interoperability with platforms used by other multilateral development banks for seamless integration.

3.3 Public Records Management

Blockchain technology provides a powerful and secure platform for public records management, ensuring authenticity, integrity, and accessibility of critical data. By leveraging an immutable ledger, blockchain maintains record integrity, accuracy, and tamper resistance, thereby enhancing public trust in government systems.

Unlike traditional databases that centrally store records, blockchain distributes data across a network of nodes, ensuring data remains accessible even if individual nodes fail, and reducing the risk of data breaches from cyberattacks. Any modification to records is cryptographically secured and timestamped, creating an auditable trail that enhances accountability while protecting citizen data. Blockchain also improves record accessibility and availability, as records can be easily retrieved and accessed when needed.

Governments are exploring blockchain solutions for public records management. For instance, Singapore’s OpenCerts is a blockchain platform enabling educational institutions to issue and verify tamper-proof academic credentials. This helps reduce document forgery and streamlines credential verification.

Another area ripe for significant improvement is land ownership and real estate management—fields often plagued by fragmented recordkeeping, outdated processes, and corruption. Fraud risks are particularly high in countries with rampant public-sector corruption. For example, Georgia has integrated its land registry into the Bitcoin blockchain, improving validation of real estate transactions while enhancing security and service efficiency.

In countries with weak institutional integrity, decentralized ledgers offer opportunities to increase transparency and restore public trust in public institutions. These ledgers are auditable, publicly transparent, maintained by multiple parties, and incentivized against collusion.

Artem Korenyuk, Digital Assets – Client, Citi

3.4 Humanitarian Aid

Effective coordination is critical during crises, as multiple entities deliver aid in food, healthcare, and shelter using different systems. Blockchain can simplify project design, resource allocation, and data sharing by providing a unified shared ledger, avoiding duplication and ensuring aid reaches those most in need. Real-time, verifiable transaction records also foster collaboration among aid agencies, governments, and NGOs, shortening overall response times.

Beyond coordination, blockchain has the potential to reshape crisis crowdfunding by providing a transparent, decentralized mechanism for mobilizing funds. By leveraging digital currencies, blockchain can collect donations and transfer them directly to verified beneficiaries without intermediaries, lowering costs and reducing delays. Smart contracts can further automate fund disbursements based on predefined conditions.

Ensuring the integrity of humanitarian supply chains is another key challenge where blockchain may help. By enabling end-to-end traceability, blockchain allows aid organizations to track the origin, movement, and usage of humanitarian supplies. This breaks down data silos, prevents corruption, and ensures aid effectively reaches affected communities. It also enables real-time inventory tracking, helping organizations respond faster to shortages and avoid logistical bottlenecks.

The UN Refugee Agency (UNHCR) using the Stellar blockchain to distribute humanitarian aid is a compelling example of blockchain’s impact in the public sector. UNHCR implemented blockchain technology to streamline disbursement of financial aid and successfully applied it in Ukraine, Argentina, and elsewhere. A key advantage of blockchain is significant cost savings through holistic digital transformation.

Blockchain also brings greater transparency. In many crisis situations, displaced persons may lack access to traditional banking services. By using blockchain-based wallets, aid recipients can receive and use funds without relying on third parties.

Denelle Dixon, CEO and Executive Director, Stellar Development Foundation

3.5 Asset Tokenization

Tokenization promises to unlock value by digitally representing real-world and financial assets, enhancing efficiency, transparency, and accessibility. In the public sector, tokenization can apply to both financial and physical assets.

Governments can tokenize debt instruments to improve bond issuance efficiency and broaden investor participation. Similarly, natural resources and infrastructure assets—such as roads, bridges, and utilities—can be represented as digital tokens, enabling more efficient tracking, management, and financing.

Beyond investment accessibility and fractional ownership models, tokenization can help financial and public institutions streamline operations, reduce inefficiencies, and lower systemic risk. Automation via smart contracts can minimize intermediaries, improve liquidity, and enhance public trust in public asset management.

Some institutions have already explored blockchain applications for digital bonds. For example, the European Investment Bank (EIB) issued its first blockchain-based digital bond in 2021, worth €100 million. This issuance, conducted with Banque de France, used blockchain for digital bond registration and settlement.

In 2022, EIB launched Project Venus, issuing its first euro-denominated digital bond on a private blockchain using central bank money in the form of wholesale CBDC. Similarly, the city of Lugano issued three bonds between 2023 and 2024 using Swiss National Bank’s wholesale CBDC and distributed ledger technology (DLT)/blockchain.

Promissa – Tokenized Promissory Notes

Many international financial institutions, including multilateral development banks (MDBs), source part of their funding from financial instruments known as promissory notes—most of which still exist in paper form. While the current system provides operational control for member countries to pay subscriptions and dues to public institutions like the World Bank, custodianship of outstanding notes could be digitized to address operational challenges and further improve efficiency.

The Promissa project, initiated by the BIS Innovation Hub, Swiss National Bank, and the World Bank, aims to build a prototype platform for digital tokenized promissory notes. Promissa explores using DLT to streamline promissory note management and provide a single source of truth for all counterparties throughout the note lifecycle. This would give central banks of member countries full visibility into their outstanding notes with MDBs—and vice versa.

The volume of promissory notes among MDBs is enormous: for example, the World Bank’s two largest institutions—the International Bank for Reconstruction and Development (IBRD) and the International Development Association (IDA)—have held large volumes of member commitments since inception. While Project Promissa aims to reimagine a “single source of truth” platform to simplify promissory note management between members and MDBs, it could be extended in the future to include payments related to such notes through integration with tokenization or existing payment systems.

3.6 Digital Identity

A single digital identity can serve as valid proof for public and private transactions, enhancing storage security and convenience. Blockchain-based digital IDs provide a decentralized, tamper-proof authentication mechanism, reducing risks of fraud and identity theft.

Digital identities extend basic services to underserved communities and individuals without official documentation—such as displaced persons. With nearly 850 million people lacking official ID, digital IDs can empower individuals using alternative data like biometrics and community verification.

Blockchain’s immutability creates transparent records for every transaction, forming verifiable digital audit trails that enhance security and accountability. Its decentralized architecture and strong cryptographic protocols protect personal data from leaks and fraud.

Moreover, self-sovereign identity ensures individuals own and control their information, selectively sharing data as needed. Advanced technologies like zero-knowledge proofs can verify identity attributes without revealing sensitive information.

The city of Zug, Switzerland, serves as an early example, using an Ethereum-based self-sovereign digital ID to provide residents with a single, verifiable electronic identity for various applications. Launched in 2017, Zug’s blockchain ID project has seen limited adoption so far due to complexity and usability limitations.

In 2023, Brazil launched a new national ID based on blockchain. The new digital ID can be accessed via mobile devices using facial recognition and QR codes. These IDs are stored on b-Cadastros, a private blockchain built by a Brazilian state-owned IT services company, aiming to improve security and reliability in data sharing among public institutions.

3.7 Challenges in Public-Sector Blockchain Adoption

Blockchain offers immense potential for government services, bringing advantages like transparency, security, and efficiency. However, large-scale adoption faces significant challenges as outlined below.

Developing standardized protocols and practices will help public blockchains gain wider recognition and trust in banking and government. Encouraging collaboration between public and private sectors can drive innovation and ensure blockchain solutions meet all stakeholders’ needs.

Ricardo Correia, Partner, Bain & Company

-

Lack of Trust: Many blockchain solutions remain experimental and unproven, making trust-building difficult. Raising awareness and cultivating skills across the ecosystem requires time and investment.

-

Interoperability and Scalability: For nationwide or global adoption, blockchain solutions must be interoperable and scalable to handle large transaction volumes. Efforts are underway to establish global blockchain standards for broad market recognition.

-

Transformation Challenges: Overhauling existing infrastructure is highly challenging, requiring significant time and resources. Insufficient evidence of tangible benefits, perceptions of technological immaturity, and complex legacy systems further deter new investments.

-

Regulatory Issues: Blockchain’s decentralized nature poses challenges for mass adoption, necessitating regulatory frameworks recognizing blockchain’s legal status, validity of stored documents, and legitimacy of issued financial instruments. Regulatory ambiguity slows adoption.

-

Addressing Abuse Risks: While difficult to quantify, illicit crypto use is estimated at $51 billion received by illegal addresses in 2024—an 11% increase YoY. However, as a percentage of total on-chain transaction volume, this figure is typically under 1%.

Resistance to Change and Public Perception

Implementing blockchain often implies radical reform of existing systems, potentially transforming civil servants’ work in every aspect. While some may welcome blockchain as positive administrative improvement, many resist it, perceiving it as a threat.

Public perception plays a crucial role. Blockchain is sometimes associated with speculative crypto markets and meme coins, overshadowing its underlying technology’s real-world benefits. This skepticism may slow mainstream adoption in the public sector.

Saqr Ereiqat, Secretary General, Dubai Digital Asset Association

4. Appendix

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News