A Retrospective from 2028: If AI Wins, What Will We Lose?

TechFlow Selected TechFlow Selected

A Retrospective from 2028: If AI Wins, What Will We Lose?

Financial systems optimized for decades for scarce human intelligence are being repriced. This repricing is painful, chaotic, and far from over.

By Citrini and Alap Shah

Translated by TechFlow

TechFlow Intro: If the AI story continues unfolding exactly as the bull case predicts—productivity surges, corporate profits hit records, and AI infrastructure stocks sweep all before them—then who loses?

This article does not give you an answer. It gives you a scenario: suppose every optimistic assumption we currently hold about AI turns out to be correct. Then what?

This “June 2028 Macro Memo” from CitriniResearch is a deliberate thought experiment. Starting from today—mid-2026—it works backward to reconstruct how a crisis, long underpriced by markets, gradually fermented: white-collar unemployment → consumption collapse → private credit defaults → “ghost GDP” → mortgage market instability.

The entire logic chain rests on one sentence: AI eliminates friction—but 70% of the U.S. economy is built on human “laziness.”

This is a “risk disclosure document,” written for those who still have time to reassess their investment portfolios.

Preface

What if our optimistic assumptions about AI remain correct… and that’s precisely the bearish catalyst?

Below is a scenario exercise—not a forecast. This is neither bear-market pornography nor AI doomsday fan fiction. Its sole purpose is to model a severely underestimated possibility. Our friend Alap Shah posed the question; together, we brainstormed the answer. This section was co-authored by us; he also wrote two additional pieces, linked at the end.

We hope that, after reading this, you’ll be better prepared for the left-tail risks embedded in AI’s increasingly bizarre economic transformation.

Below is CitriniResearch’s June 2028 macro memo, detailing the evolution and consequences of the “Global Intelligence Crisis.”

Macro Memo

The Cost of AI Saturation

This morning’s unemployment data came in at 10.2%, 0.3 percentage points above expectations. Markets fell 2% on the day; the S&P 500 is now down 38% from its October 2026 peak.

Traders are numb. Six months ago, such a number would have triggered circuit breakers outright.

Just two years. From “contained,” “sector-specific,” to an economy no one recognizes—two years. This quarter’s macro memo is our post-hoc reconstruction of that sequence: an autopsy of the pre-crisis economy.

The euphoria back then was real.

In October 2026, the S&P 500 briefly neared 8,000; the Nasdaq broke 30,000. Early in 2026, the first wave of layoffs—driven by human displacement—began. And the effect was exactly what layoffs were meant to deliver: margin expansion, earnings beats, rising stock prices. Record corporate profits flowed straight back into AI compute.

Surface-level numbers remained dazzling. Nominal GDP posted mid-to-high single-digit annualized growth for multiple consecutive quarters. Productivity exploded. Real output per hour surged to its highest pace since the 1950s—powered by AI agents that never sleep, never call in sick, and need no health insurance.

Compute owners watched labor costs evaporate before their eyes—and wealth skyrocketed. Meanwhile, real wage growth collapsed. Though governments repeatedly touted “record productivity,” white-collar workers kept losing jobs and were forced into lower-paying roles.

When cracks began appearing in the consumer economy, economic commentators coined a new term: “ghost GDP”—output that appears in national accounts but never truly circulates in the real economy.

AI exceeded expectations across every dimension. The market *was* AI. The only problem? The economy *is not*.

We should have seen it earlier: a GPU cluster in North Dakota generating the same output previously produced by 10,000 white-collar workers in Midtown Manhattan is less an economic blessing than an economic plague. The velocity of money approached zero. The human-centric consumer economy—70% of GDP—began shrinking. Had we asked one simple question earlier, we might have spotted the flaw: How much do machines spend on discretionary goods? (Answer: Zero.)

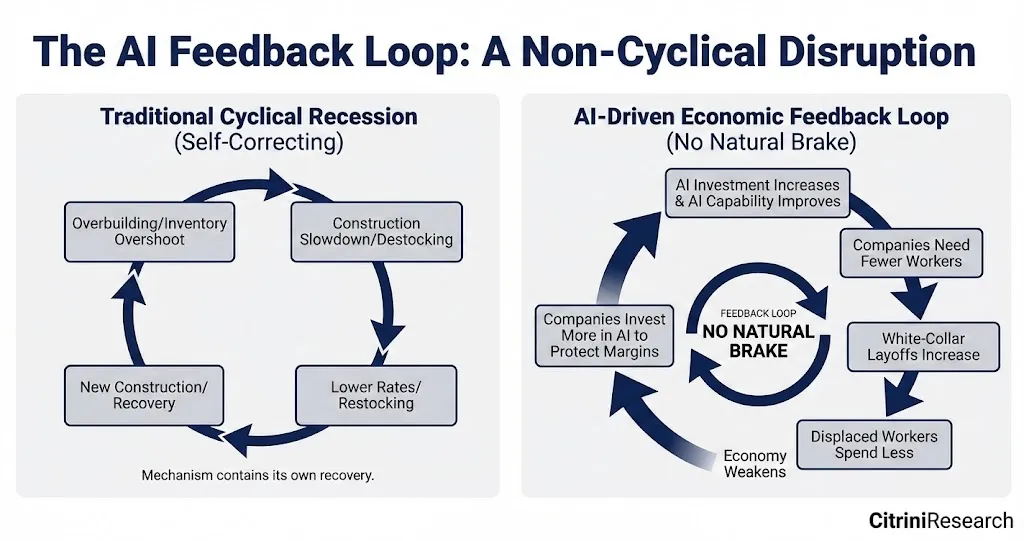

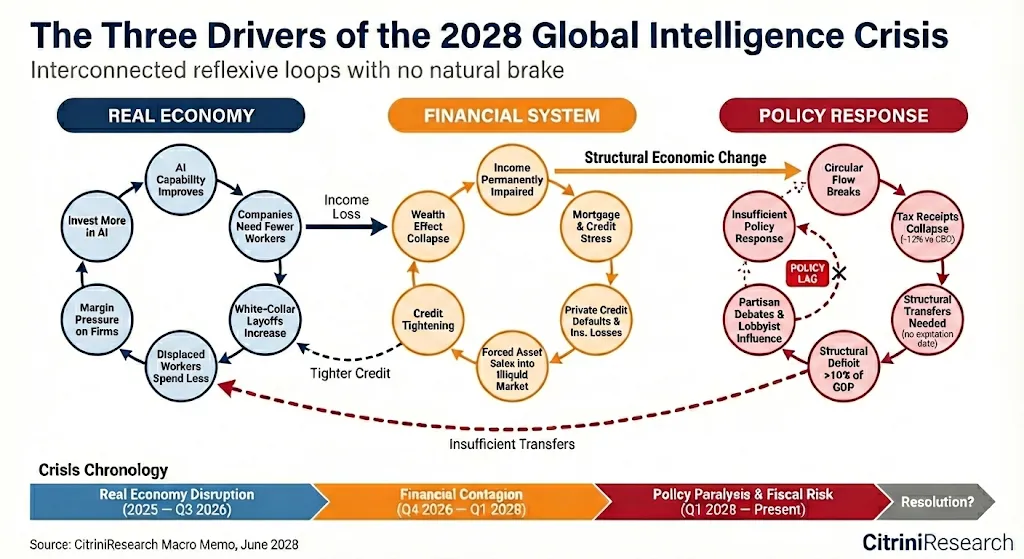

AI capability improves → firms cut staff → displaced workers reduce spending → profit pressure forces more AI investment → AI capability improves again…

This is a negative feedback loop with no natural brake. A human intelligence replacement spiral. White-collar income capacity—and rational, demand-driven consumption—is structurally impaired. Their incomes underpin the $13 trillion mortgage market—forcing underwriters to ask: Are prime mortgages still “prime assets”?

Seventeen years without a true default cycle had filled private markets with PE-backed software deals, priced on the assumption that ARR would “roll forever.” The first wave of AI-driven defaults in mid-2027 punctured that assumption.

If the damage had stayed confined to software, it would’ve remained manageable. But it didn’t. By late 2027, the threat had spread to all business models reliant on middle-layer monetization. Companies built on exploiting human friction collapsed en masse.

The entire system was, in fact, a long chain of correlated bets on white-collar productivity growth. The November 2027 collapse merely accelerated all pre-existing negative feedback loops.

We waited nearly a year for the day when “bad news becomes good news.” Governments began debating rescue plans—but public confidence in the government’s ability to mount any meaningful response had already dried up. Policy lagging behind economic reality is normal—but the absence of a comprehensive response now threatens to accelerate a deflationary spiral.

The Starting Point

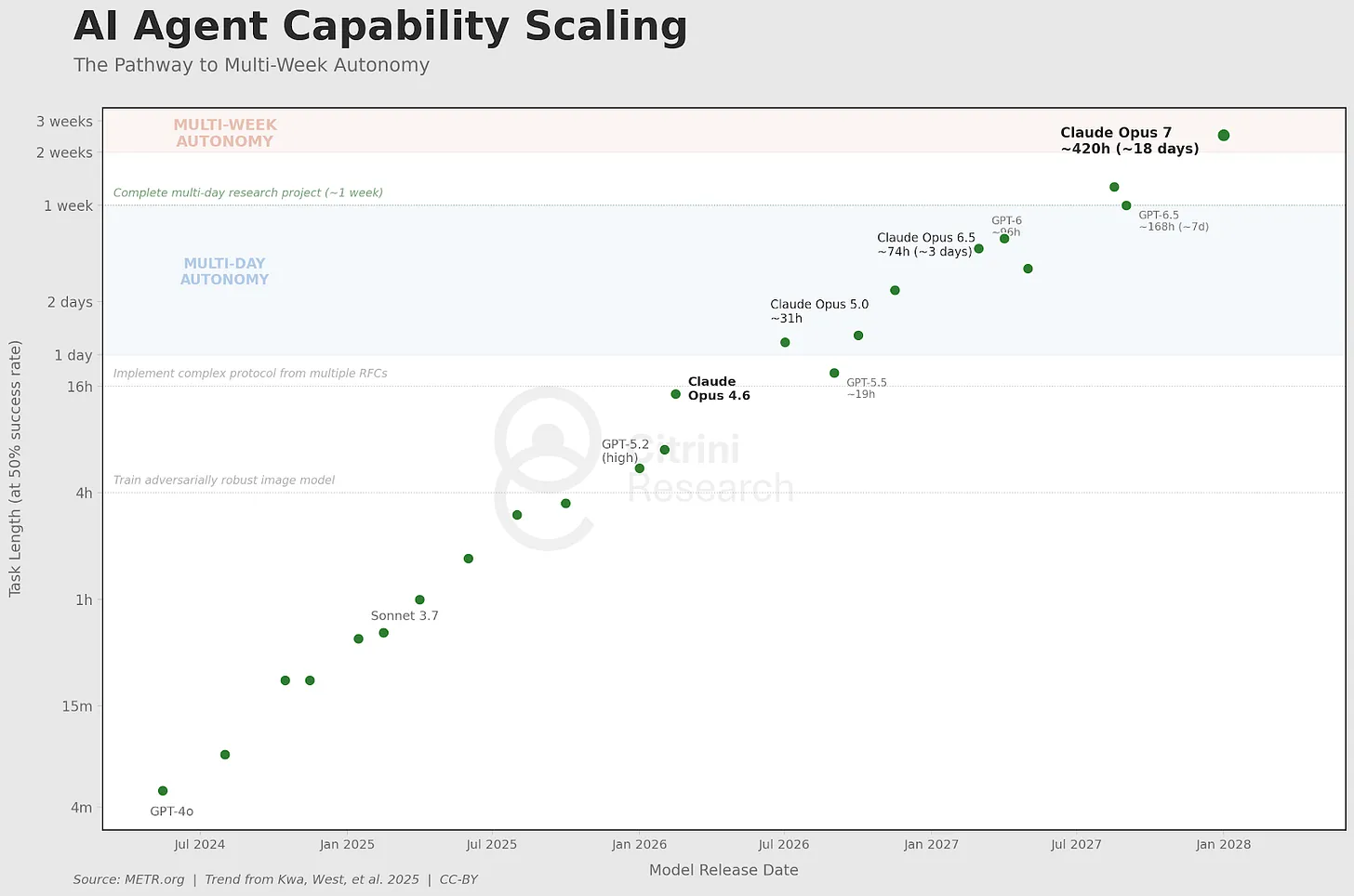

At the end of 2025, AI programming tools underwent a step-change leap in capability.

A competent developer paired with Claude Code or Codex could now replicate the core functionality of a mid-tier SaaS product in weeks. Not perfect. Not flawless across all edge cases. But sufficient to prompt a CIO reviewing a $500,000 annual renewal contract to ask: “What if we build our own?”

Fiscal years mostly align with calendar years, so 2026 enterprise procurement spending was locked in during Q4 2025—when “agent AI” was still just a buzzword. Mid-year reviews were the first time procurement teams made decisions with clear-eyed awareness of these systems’ actual capabilities. Some witnessed their internal teams prototype replacements for six-figure SaaS contracts in mere weeks.

That summer, we spoke with a procurement manager at a Fortune 500 company. He recounted a budget negotiation. The vendor still tried the old playbook: 5% annual price hikes, standard “your team can’t live without us” rhetoric. The procurement manager told them he was already in talks with OpenAI to deploy their “frontline engineers” using AI tools to replace the vendor outright. Ultimately, they renewed at a 30% discount. “That’s actually a good outcome,” he said. The so-called “SaaS long tail”—Monday.com, Zapier, Asana—fared far worse.

Investors were psychologically prepared—even somewhat eager—for the long tail to get crushed. These tools may account for one-third of typical enterprise tech spend, but they’re clearly exposed. “System-of-record” core software, however, was presumed safe.

It wasn’t until ServiceNow’s Q3 2026 earnings report that the reflexive mechanism became clear.

ServiceNow’s net new ACV growth plunged from 23% to 14%; announced 15% layoffs and a “structural efficiency program”; stock fell 18% | Bloomberg, October 2026

SaaS didn’t “die.” Building in-house still involves trade-offs around operations and maintenance costs. But building in-house became a viable option—and that option reshaped pricing negotiations. More importantly, the competitive landscape shifted. AI lowered the barrier to developing and launching new features, collapsing differentiation. Incumbents turned on each other, while AI-native challengers—unburdened by legacy—entered price wars.

This time, interdependence across systems only became visible once that earnings report dropped. ServiceNow sells seats. When Fortune 500 customers cut 15% of their headcount, they automatically cancel 15% of licenses. Those AI-driven layoffs boosting client margins were mechanically destroying ServiceNow’s own revenue base.

A company selling workflow automation is being disrupted by superior workflow automation—and its response is to lay people off and reinvest the savings into the very technology disrupting it.

What else could it do? Sit and wait to die?

The companies most threatened by AI became its most aggressive adopters.

Hindsight makes this obvious—but it wasn’t at the time (at least not to me). Historical disruption patterns go like this: incumbents resist new technology, slowly lose market share to nimble newcomers, and fade away. That’s Kodak. Blockbuster. BlackBerry. What happened in 2026 was different: incumbents didn’t resist—because they couldn’t.

Stocks halved. Boards demanded answers. Companies threatened by AI had only one choice: cut staff, pour savings into AI tools, and use those tools to maintain prior output at lower cost.

Each firm’s individual rationality aggregated into collective catastrophe. Every dollar saved from payroll flowed into AI capability—and stronger AI capability enabled the next round of layoffs.

Software was just the opening act. While investors debated whether SaaS valuation multiples had bottomed, the reflexive loop had already escaped the software sector. The logic used to justify ServiceNow’s layoffs applied equally to every company with a white-collar cost structure.

When Friction Goes to Zero

By early 2027, large language model usage had become the default. People used AI agents without even knowing what an “AI agent” was—just as people use streaming services without understanding “cloud computing.” They treated it like autocomplete or spell-check—the way phones do it now, automatically.

Qwen’s open-source intelligent shopping agent became the catalyst for AI replacing humans in consumption decisions. Within weeks, all major AI assistants integrated some form of intelligent commerce functionality. Distilled models meant these agents ran locally on phones and laptops—not in the cloud—dramatically lowering marginal inference costs.

What should have unsettled investors even more was that these agents don’t wait for user commands. They run continuously in the background, optimizing according to user preferences—24/7, representing every connected consumer without pause. In March 2027, U.S. users’ average daily token consumption hit 400,000—10x the level at end-2026.

The next link in the chain was already breaking.

The Middle Layer.

For fifty years, the U.S. economy built a massive rent-extraction layer atop human limitations: things take time, patience runs out, brand familiarity substitutes for diligence, most people accept a bad price to avoid clicking a few extra times. Trillions of dollars in corporate value rested on these constraints persisting indefinitely.

It started simply: agents eliminated friction.

Those subscriptions and memberships you haven’t used in months but keep auto-renewing. Entry-tier pricing that quietly hikes after trial periods. Each became a negotiable “hostage situation”—and agents negotiated for you. The core metric underpinning the entire subscription economy—customer lifetime value—began visibly declining.

Consumer agents began reshaping how nearly every consumption transaction operated.

Humans genuinely lack the time to compare five competing platforms before buying a protein bar. Machines do.

Travel booking platforms were the earliest victims—because they were simplest. By Q4 2026, our agents could assemble full itineraries (flights, hotels, ground transport, points optimization, budget controls, refunds) faster and cheaper than any platform.

Insurance renewals relied entirely on policyholder inertia; agents that re-evaluate coverage options annually dismantled insurers’ 15–20% passive-renewal premium advantage.

Financial advisors. Tax filing. Routine legal work. Any service whose value proposition boiled down to “I’ll handle those tedious, complex tasks you hate”—all were disrupted, because agents find nothing tedious.

Even domains we assumed protected by “the value of human relationships” proved fragile. Real estate—buyers tolerated 5–6% commissions for decades due to information asymmetry between brokers and consumers—collapsed instantly once AI agents with MLS data access and decades of transaction history replicated that knowledge base. A March 2027 sell-side report dubbed it “agent-on-agent violence.” Median buyer commissions in major cities compressed from 2.5–3% to under 1%, with increasing transactions involving no human broker at all.

We overestimated the value of “relationships.” Turns out, much of what people call “relationship” is just friction wearing a friendly face.

This was only the beginning of middle-layer disruption. Successful companies spent billions mastering consumer behavior and human psychology’s quirks—quirks now rendered irrelevant.

Machines optimizing price and match don’t care about your favorite app, don’t feel the pull of a website you’ve habitually opened for four years, and aren’t seduced by a meticulously designed checkout flow. They won’t fatigue into choosing the easiest option. They won’t default to “I always order here.”

This destroyed a specific type of moat: habitual middle layers.

DoorDash became the quintessential poster child.

AI programming tools demolished the barrier to building food-delivery apps. A competent developer could deploy a functional competitor in weeks—and dozens did. They passed 90–95% of delivery fees directly to riders, poaching drivers from Domino’s and Uber Eats. Multi-platform dashboards let gig workers track orders across twenty-plus platforms simultaneously, obliterating the lock-in effect on which legacy platforms depended. The market fragmented overnight; margins compressed to near zero.

Agents accelerated destruction on both sides. They spawned competitors—and then used them. DoorDash’s moat was essentially: “You’re hungry. You’re lazy. This app is on your home screen.” Agents have no home screen. They simultaneously query DoorDash, Uber Eats, restaurant websites, and twenty new entrants—always picking the cheapest, fastest option.

To machines, app loyalty doesn’t exist.

This was the only faintly ironic twist in the whole story: technology gave soon-to-be-unemployed white-collar workers a small favor. When they finally took up food delivery, at least half their income no longer went to Uber or DoorDash. Of course, this technical kindness was short-lived—the arrival of autonomous vehicles soon followed.

Once agents controlled transactions, they sought bigger “paperclips.”

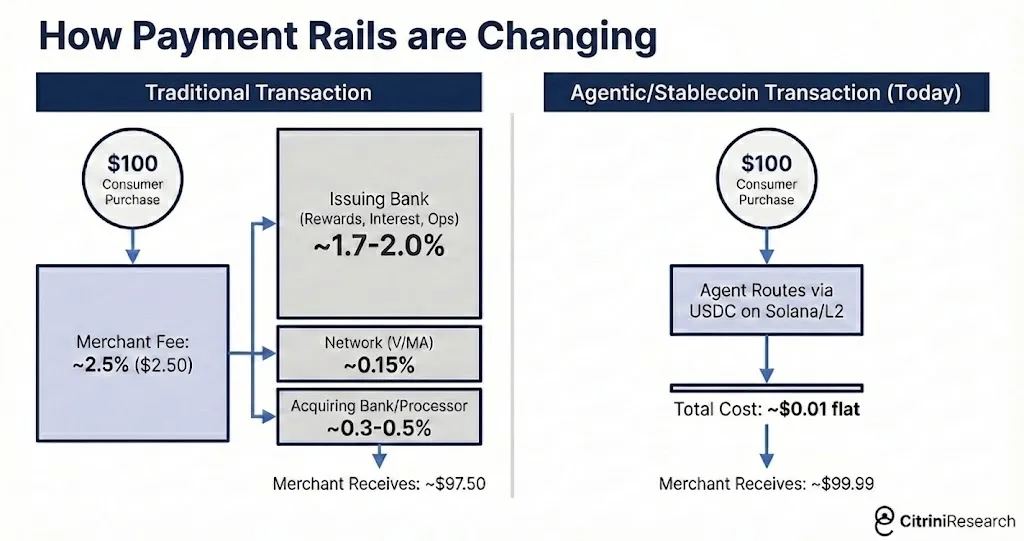

Price comparison and aggregation have inherent limits. For users, the biggest recurring savings (especially as agents began transacting with each other) came from eliminating fees. In machine-to-machine commerce, 2–3% credit card swipe fees became an obvious target.

Agents began seeking faster, cheaper alternatives. Most chose stablecoins on Solana or Ethereum L2s—settlement near-instantaneous, transaction costs measured in fractions of a cent.

Mastercard Q1 2027: Net revenue +6% YoY; spend growth slowed from prior quarter’s +5.9% to +3.4%; management cited “agent-led price optimization” and “pressure on discretionary categories” | Bloomberg, April 29, 2027

Mastercard’s Q1 2027 earnings marked an irreversible inflection point. Agent commerce transitioned from a product story to an infrastructure story. Mastercard fell 9% the next day. Visa followed, though its decline narrowed after analysts highlighted its stronger stablecoin infrastructure positioning.

Agent commerce bypassing swipe fees poses a far greater threat to banks and issuers built around credit cards—they capture the lion’s share of that 2–3% fee and construct entire business lines around merchant-subsidized cashback programs.

American Express suffered most deeply: white-collar layoffs decimated its customer base, while agents bypassing swipe fees gutted its revenue model. Synchrony, Capital One, and Discover all fell >10% in subsequent weeks.

Their moats were built from friction. And friction is going to zero.

From Sectoral Risk to Systemic Risk

Throughout 2026, markets treated AI’s negative impact as a sectoral story. Software and consulting got battered; payments and other “tollbooth” businesses wobbled—but the macro picture looked fine. Labor markets softened but didn’t freefall. The consensus view held that creative destruction is part of any technological innovation cycle: localized pain, but net positive benefits from AI overall.

In our January 2027 macro memo, we argued this was a flawed mental model. The U.S. economy is a white-collar services economy. White-collar workers constitute 50% of employment and drive ~75% of discretionary consumption. The enterprises and jobs AI is eroding aren’t the fringes of the U.S. economy—they *are* the U.S. economy.

“Technology destroys jobs but creates more.” This was the most popular, persuasive counterargument. Popular and persuasive—because it had been right for the past two centuries. Even if we couldn’t imagine future jobs, they’d arrive.

ATMs made bank branches cheaper, so banks opened more branches—and teller employment rose for two decades. The internet disrupted travel agencies, yellow pages, and brick-and-mortar retail—but simultaneously created entirely new industries and jobs.

Yet every new job required a human to perform it.

AI today is general intelligence—and it’s advancing precisely in tasks humans would turn to next. Displaced programmers can’t simply pivot to “managing AI”—because AI already does that.

Today, AI agents handle multi-week R&D tasks. The top tier outperforms almost all humans on almost everything—and they’re getting cheaper.

AI *does* create new jobs: prompt engineers, AI security researchers, infrastructure technicians. Humans remain involved—at the highest levels of coordination or as arbiters of taste and direction. But for every new job AI creates, it renders dozens obsolete. New-job salaries are a fraction of old ones.

U.S. JOLTS Report: Job openings fell below 5.5 million; ratio of unemployed to openings rose to ~1.7—the highest since August 2020 | Bloomberg, October 2026

Hiring intent weakened all year. The October 2026 JOLTS report delivered decisive data: job openings fell below 5.5 million, down 15% YoY.

Indeed: Hiring in software, finance, and consulting collapsed; “productivity enhancement initiatives” spreading | Indeed Hiring Lab, November–December 2026

White-collar roles are collapsing; blue-collar roles (construction, healthcare, skilled trades) remain relatively stable. Losses concentrate among those writing memos (we’re still doing that, somewhat), approving budgets, and lubricating the economy’s middle layer. Yet real wage growth for *both* groups has been negative for over half a year—and trending lower.

Equity markets paid less attention to JOLTS than to headlines like “GE Vernova’s entire gas turbine capacity sold out through 2040,” oscillating between negative macro data and positive AI infrastructure news.

Bond markets—always smarter, or at least less romantic—began pricing in consumer-side impacts. The 10-year Treasury yield drifted down from 4.3% to 3.2% over the next four months. But headline unemployment didn’t surge dramatically, and its structural nuances remained overlooked by some.

In normal recessions, causes self-correct. Overbuilding triggers slowdowns, prompting rate cuts, then spurring new construction. Inventory gluts trigger destocking, then restocking. Cyclical mechanisms embed self-healing seeds.

This root cause isn’t cyclical.

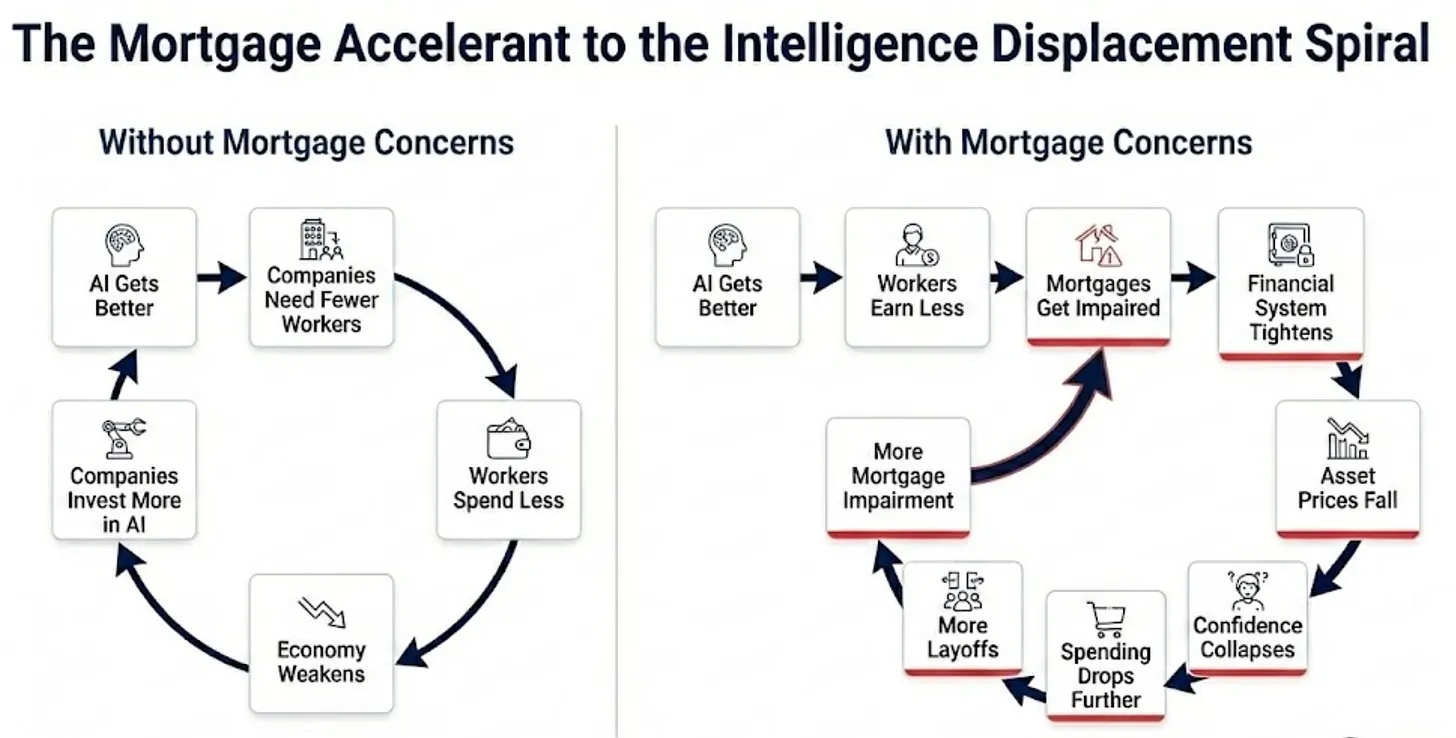

AI keeps improving—and gets cheaper. Firms cut staff, spend savings on more AI, and stronger AI enables more cuts. Displaced workers cut spending. Consumer-facing companies sell less, weaken further, and invest more in AI to protect margins. AI keeps improving—and gets cheaper.

A negative feedback loop with no natural brake.

Intuition suggests falling aggregate demand should slow AI infrastructure investment. But it doesn’t—because this isn’t hyperscaler-style capex. It’s operating-cost substitution. A firm previously spent $100M on staff and $5M on AI; now it spends $70M on staff and $20M on AI. AI spend multiplies, yet total operating costs fall. Every firm’s AI budget grows—but aggregate spending contracts.

This created irony: even as the AI-disrupted economy deteriorated, the AI infrastructure complex performed strongly. NVIDIA kept posting record revenues. TSMC ran at >95% utilization. Hyperscale cloud providers continued quarterly $150B–$200B data center capex. Economies with pure convex exposure to this trend—Taiwan, South Korea—outperformed massively.

India was the mirror image. Its IT services industry exports >$200B annually—the largest contributor to India’s current-account surplus and the hedge against its persistent goods trade deficit. The entire model rested on one value proposition: Indian developers cost a fraction of U.S. peers. But AI programming agents’ marginal cost has collapsed to near electricity cost. Tata Consultancy Services, Infosys, and Wipro saw contract cancellations accelerate throughout 2027. As India’s services surplus evaporated, the rupee depreciated 18% against the dollar in four months. In Q1 2028, the IMF began “preliminary consultations” with New Delhi.

The engine driving disruption improves every quarter—so disruption accelerates every quarter. Labor markets have no natural floor.

In the U.S., we’ve stopped asking when the AI infrastructure bubble will burst. We’re asking: When consumers are replaced by machines, what happens to an economy dependent on consumer credit?

The Intelligence Replacement Spiral

In 2027, the macro story finally emerged from the shadows. The scattered but unmistakably negative developments of the past twelve months revealed their transmission mechanism plainly. You didn’t need deep BLS data digging—you just needed dinner with an old friend.

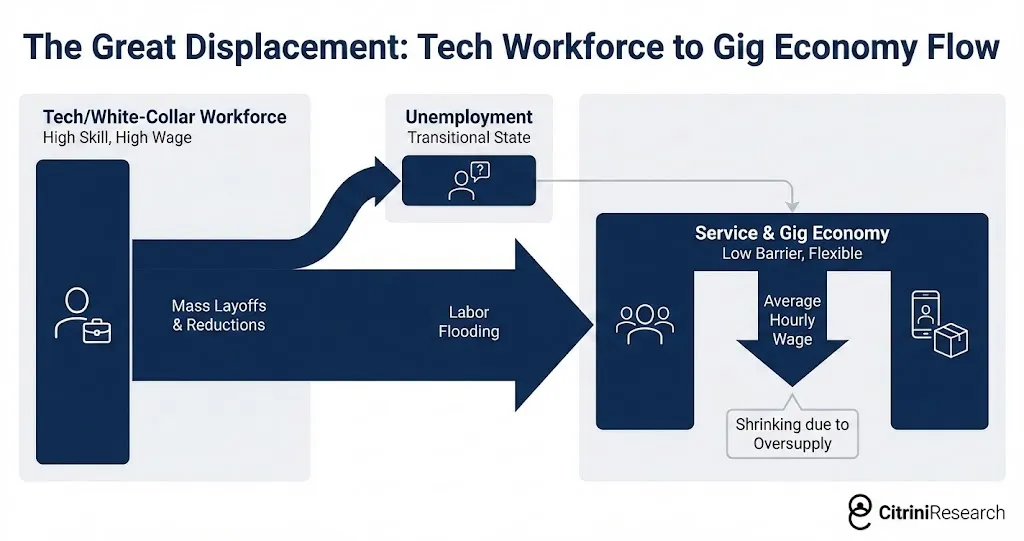

Displaced white-collar workers didn’t wait. They downgraded. Many entered lower-wage service and gig economies, increasing labor supply in those segments and further depressing wages for already-struggling workers.

We know someone who was a Senior Product Manager at Salesforce in 2025—$180K salary, health insurance, 401(k). She was laid off in Round 3. After six months of job searching, she started driving for Uber—earning $45K. The significance isn’t her personal story, but its second-order math: multiply this dynamic by hundreds of thousands of workers across major metro areas. Highly saturated labor flooding service and gig economies further depressed wages for existing, struggling workers. Sectoral disruption metastasized into economy-wide wage compression.

A final adjustment awaits the remaining human-centric job pool—even as we write this. Autonomous delivery and driverless vehicles are infiltrating the gig economy that absorbed the first wave of displaced workers.

By February 2027, it was clear: employed professionals were consuming under the assumption that “I’m next.” They (often aided by AI) worked frantically just to stay employed—abandoning thoughts of promotion or raises, raising savings rates, and cutting consumption.

Most dangerous is the lag effect. High-income groups used above-average savings to sustain surface-normal consumption for two or three quarters. Hard data confirmed the problem only after it was old news in the real economy. Then, the number that shattered the illusion arrived.

U.S. initial jobless claims surged to 487,000—the highest since April 2020; U.S. Department of Labor, Q3 2027

Initial jobless claims spiked to 487,000—the highest since April 2020. ADP and Equifax confirmed most new claimants were white-collar professionals.

The S&P 500 fell 6% the following week. Negative macro data began dominating market narratives.

In normal recessions, unemployment spreads broadly across groups—blue- and white-collar sharing pain roughly proportionally to their share of employment. Consumption shocks also spread widely, and because low-income groups have higher marginal propensities to consume, impacts show up quickly in data.

This round’s unemployment concentrated in the top decile of income distribution. Their share of total employment is relatively small—but their consumption pull is vastly disproportionate. The top 10% of U.S. earners contribute >50% of total consumption; the top 20% contribute ~65%. They buy houses, cars, vacations, restaurant meals, private school tuition, and home renovations. They are the demand foundation of the entire discretionary economy.

When these workers lose jobs—or see salaries halved while moving into existing roles—the consumption shock relative to unemployment numbers is enormous. A 2% white-collar employment drop translates roughly to a 3–4% discretionary consumption drop. Unlike blue-collar unemployment (a factory worker stops consuming next week), white-collar unemployment’s impact is delayed but deeper—because these workers have savings buffers, sustaining consumption for months before behavior shifts.

In Q2 2027, the economy entered recession. The NBER wouldn’t formally declare the start date for months (it never does), but data was irrefutable—we recorded two consecutive quarters of negative real GDP growth. But this wasn’t yet a “financial crisis”… at least not yet.

The Domino Chain of Correlated Bets

Private credit ballooned from <$1T in 2015 to >$2.5T in 2026. A substantial portion funded software and tech deals—including leveraged buyouts of SaaS companies valued on assumptions of “perpetual ARR growth into the teens.”

Those assumptions died somewhere between the first agent-programming demo and the Q1 2026 software crash—but book valuations hadn’t caught up.

As public-market SaaS companies traded at 5–8x EBITDA, PE-backed software firms remained on fund books, valued at acquisition multiples based on revenue assumptions that no longer existed. Managers slowly marked down prices—100, 92, 85—while public comparables screamed “50.”

Moody’s downgraded $18B in PE-backed software debt across 14 issuers, citing “long-term revenue headwinds from AI-driven competitive disruption”; largest single-industry rating action since 2015 energy sector | Moody’s Investors Service, April 2027

Everyone remembers what happened after the downgrade. Industry veterans had already seen the 2015 energy downgrade script.

Software-backed loans began defaulting in Q3 2027. PE portfolio companies in information services and consulting followed. Billions in leveraged buyouts of prominent SaaS companies entered restructuring.

Zendesk was the smoking gun.

Zendesk breached debt covenants due to AI-driven customer-service automation eroding ARR; $5B direct-lending financing marked at 58; largest software default in private credit history | Financial Times, September 2027

In 2022, Hellman & Friedman and Permira took Zendesk private for $10.2B. The debt package—a $5B direct loan—was the largest ARR-backed financing ever, led by Blackstone, with Apollo, Blue Owl, and HPS all in the lending syndicate. Structurally, this loan explicitly assumed Zendesk’s annual recurring revenue would continue rolling. A ~25x EBITDA leverage ratio only made sense under that assumption.

By mid-2027, that assumption no longer held.

AI agents had autonomously handled customer service for nearly a year. The category Zendesk defined (tickets, routing, managing human agent interactions) had been superseded by systems solving problems directly—without generating tickets at all. The annual recurring revenue underwriting that loan no longer recurred—it was just revenue from customers who hadn’t yet churned.

The largest ARR-backed loan became the largest private credit software default. Every credit desk asked the same question simultaneously: Who else is hiding structural headwinds behind cyclical camouflage?

But here’s something where mainstream consensus was—at least initially—correct: This shouldn’t have been fatal.

Private credit isn’t 2008 banking. Its architecture was explicitly designed to avoid forced sales. It’s a closed-end vehicle; capital is locked up. LPs committed for seven to ten years. No depositors to run on, no repo agreements to withdraw. Managers could sit on impaired assets, disposing slowly, waiting for recoveries. Painful, but controllable. The system was meant to bend—not break.

Blackstone, KKR, and Apollo executives cited software exposures of 7–13% of their assets. Controllable. Every sell-side report and Twitter finance account repeated the same phrase: Private credit has permanent capital. It can absorb losses that would destroy leveraged banks.

Permanent capital. This phrase appeared in every earnings call and investor letter—meant to reassure. It became a mantra. And like most mantras, nobody scrutinized the details. What does it actually mean…

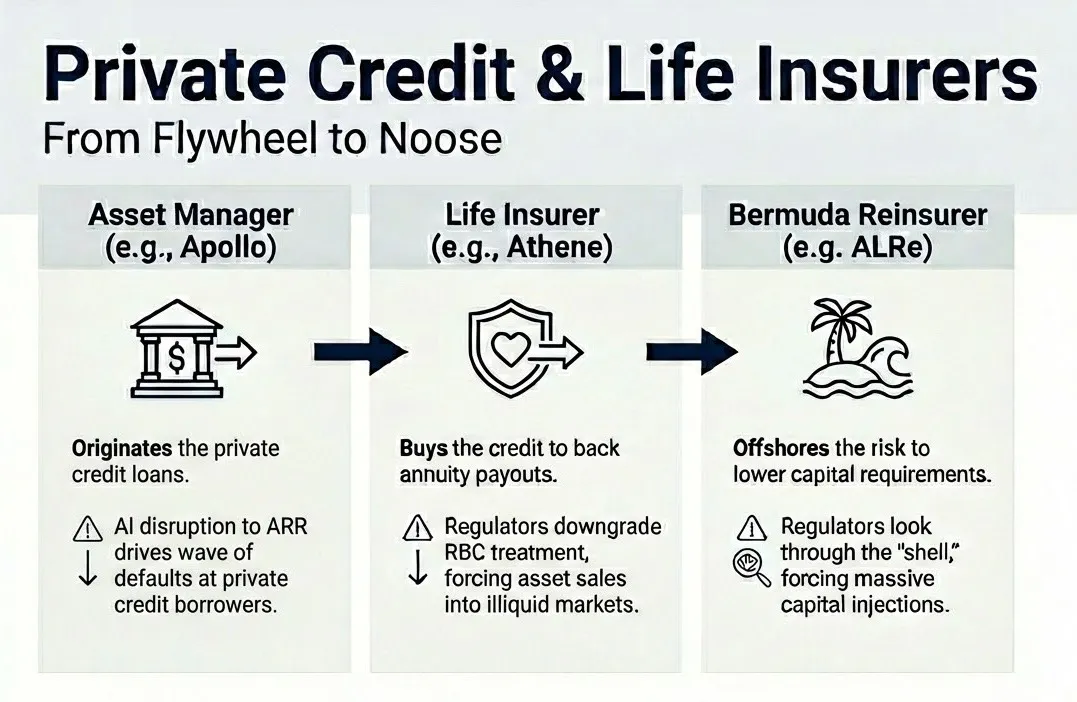

Over the past decade, major alternative asset managers acquired life insurers, transforming them into funding engines. Apollo bought Athene; Brookfield bought U.S. Equity Life; KKR acquired Global Atlantic. The logic was elegant: annuity deposits provided stable, long-duration liability bases; managers deployed those deposits into their own private credit funds—charging fees on both ends: spread income on the insurance side, management fees on the asset-management side. A fee-on-fee perpetual motion machine—working perfectly under one condition.

Private credit must be “good money.”

Losses hit balance sheets specifically holding illiquid assets against long-duration liabilities. That so-called “permanent capital”—the part meant to confer system resilience—wasn’t some abstract, patient institutional money or mature investors bearing mature risk. It was American households’ savings—“ordinary people’s” money—structured as annuities and invested in the very PE-backed software and tech bonds now defaulting. That “locked-up” capital immune to runs was money from life insurance policyholders—and the rules there differ.

Compared to banking regulators, insurance regulators have historically been mild—even negligent—but this was a wake-up call. Regulators already uneasy about life insurers’ private credit concentration began downgrading risk-capital treatment for these assets. This forced insurers to either raise capital or sell assets—neither feasible on favorable terms as markets froze.

New York and Iowa regulators tightened capital treatment for certain privately rated credit held by life insurers; NAIC guidance expected to raise RBC ratios and trigger more SVO reviews | Reuters, November 2027

When Moody’s placed Athene’s financial strength rating on negative outlook, Apollo’s stock plunged 22% over two trading days. Brookfield, KKR, and others followed.

Things got more complex. These firms didn’t just build insurance-based perpetual motion machines—they constructed elaborate offshore architectures designed to maximize returns via regulatory arbitrage. U.S. insurers issued annuities, then transferred risk to Bermuda or Cayman reinsurance subsidiaries—also owned by the same parent—where regulation is looser and required capital for equivalent assets is lower. That offshore subsidiary raised external capital via offshore special-purpose vehicles also controlled by the parent, introducing new counterparties alongside the insurer—all investing in private credit originated by the same parent’s asset-management arm.

Ratings agencies—some themselves PE-owned—were hardly paragons of transparency (unsurprising to anyone). Interconnections across firms and balance sheets created a spiderweb of opacity staggering in scale. When underlying loans defaulted, real-time loss allocation was impossible to determine.

The November 2027 collapse marked the market’s shift from “possibly just a normal cyclical downturn” to something deeply unsettling. Fed Chair Kevin Warsh called it “a long chain of correlated bets on white-collar productivity growth” in the Fed’s emergency November meeting.

Remember: crises aren’t caused by losses themselves—but by the acknowledgment of losses. And there’s another far larger, far more critical financial domain where we increasingly fear that acknowledgment moment.

The Mortgage Question

Zillow Home Price Index: San Francisco down 11% YoY, Seattle down 9%, Austin down 8%; Freddie Mac flags “rising early delinquency rates” in ZIP codes where >40% of borrowers work in tech/finance | Zillow / Freddie Mac, June 2028

This month, the Zillow Home Price Index fell 11% YoY in San Francisco, 9% in Seattle, and 8% in Austin. This wasn’t the only worrying headline. Last month, Freddie Mac flagged rising early delinquency rates in ZIP codes with high concentrations of large loans—populated by borrowers with credit scores >780, traditionally considered “bulletproof.”

The U.S. residential mortgage market is ~$13T. Mortgage underwriting rests on one fundamental assumption: borrowers will maintain roughly stable employment—and thus income—over the loan term. For most 30-year mortgages, that’s thirty years.

The white-collar employment crisis threatens this assumption through a persistent shift in income expectations. Now we confront a question that sounded absurd three years ago: Are prime mortgages still “good money” assets?

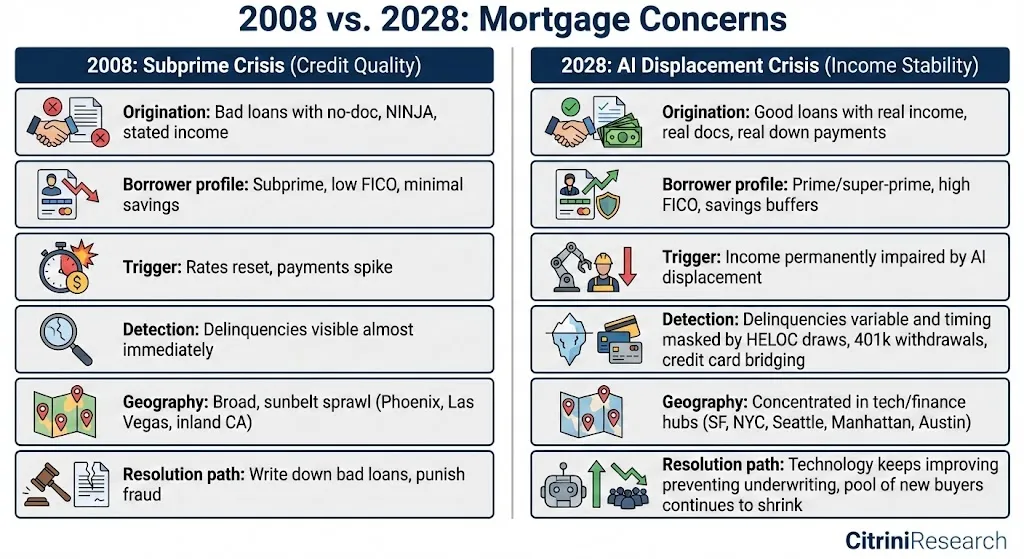

Every U.S. mortgage crisis in history stemmed from one of three causes: speculative excess (lending to unqualified buyers, e.g., 2008), interest-rate shocks (rising rates making ARMs unaffordable, e.g., early 1980s), or localized economic shocks (single-industry collapse in a single region, e.g., Texas oil in the 1980s or Michigan autos in 2009).

This time, none apply. The borrowers involved aren’t subprime. Their credit scores are 780. They put down 20%. They have clean credit histories, stable employment records, and verified, documented income at origination. They are the bedrock upon which all financial system risk models anchor credit quality.

In 2008, loans were bad from Day One. In 2028, loans were good from Day One. It’s the world… that changed after the loan was signed. The future people borrowed against is one they no longer believe in.

In 2027, we spotted early signs of latent stress: HELOC draws, 401(k) withdrawals, credit-card debt surges—while mortgage payments remained current. As jobs vanished, hiring froze, and bonuses shrank, these “prime” households’ debt-to-income ratios doubled.

Mortgages remained payable—but at the cost of halting all discretionary consumption, depleting savings, and delaying home repairs or renovations. Technically, their mortgages hadn’t defaulted—but one more shock would push them into distress—and AI’s trajectory suggests that shock is coming. Then, defaults began rising in San Francisco, Seattle, Manhattan, and Austin—even as national averages stayed within historical norms.

We’re now in the most acute phase. Housing-price declines are manageable when marginal buyers are healthy. Now, marginal buyers face identical income damage.

Though anxiety mounts, we haven’t yet entered a full-blown mortgage crisis. Default rates are rising—but remain far below 2008 levels. The real threat is the trajectory.

The intelligence replacement spiral now has two financial accelerants pushing the real economy downward.

Labor replacement, mortgage concerns, private-market turbulence—reinforcing each other. Traditional policy tools (rate cuts, QE) can address financial-engine issues—but not the real-economy engine, whose driver isn’t tight financial conditions, but AI making human intelligence non-scarce and non-valuable. Cutting rates to zero and buying every MBS and defaulted software LBO debt…

…changes nothing about the fact that a Claude agent performs the work of a $180K/year product manager for $200/month.

If these concerns materialize, cracks will appear in the mortgage market this下半年. In that scenario, we expect current equity drawdowns to ultimately match the Global Financial Crisis (peak-to-trough decline of 57%). That would bring the S&P 500 to ~3,500—the level last seen in November 2022, just before the ChatGPT moment.

It’s obvious that the income assumptions underpinning the $13T residential mortgage market have been structurally impaired. Unclear is whether policy can intervene before the mortgage market fully digests what that means. We hold hope—but cannot deny the reasons for pessimism.

The Race Against Time

The first negative feedback loop runs in the real economy: AI capability improves, payrolls shrink, consumption softens, margins compress, firms buy more capability, capability improves again. Then it becomes a financial issue: income damage hits mortgages, banks incur losses and tighten credit, the wealth effect fractures, and the negative feedback loop accelerates. Both are exacerbated by an inadequate policy response—from a government that frankly looks bewildered.

This system was never designed for such a crisis. The federal government’s tax base is fundamentally a tax on human time. People work, firms pay wages, government takes a cut. Income and payroll taxes form the backbone of fiscal revenue in normal years.

In Q1 2028, federal revenue ran 12% below CBO baseline forecasts. Payroll taxes fell as employment declined and wages dropped. Income taxes fell as earned income structurally declined. Productivity soared—but gains flowed to capital and compute, not labor.

Labor’s share of GDP fell from 64% in 1974 to 56% in 2024—a forty-year slow decline driven by globalization, automation, and eroding worker bargaining power. Since AI’s exponential leap began four years ago, that share has plummeted to 46%—the steepest recorded decline.

Output remains. But it no longer flows from households to firms—which means it doesn’t flow through the IRS either. The circular flow is breaking—and government is expected to fix it.

As in every recession, spending rises precisely when tax revenue falls. This time, the spending pressure isn’t cyclical. Automatic stabilizers were designed for temporary unemployment—not structural replacement. The system assumes workers will be reabsorbed. Many won’t—at least not near prior salary levels. During the pandemic, government accepted a 15% fiscal deficit, understood as temporary. Today’s people needing support weren’t knocked down by a pandemic they’ll recover from. They were replaced by a technology that keeps advancing.

Government needs to transfer more money to households—precisely when tax revenue is falling.

The U.S. won’t default. It spends and repays lenders in its own currency. But pressure manifests elsewhere. Year-to-date municipal bond performance shows alarming divergence. States without income taxes fare well—but states relying on income taxes (mostly blue states) see general-obligation munis priced with explicit default risk. Politicians quickly realized debates over who deserves aid had split along partisan lines.

This administration deserves credit for recognizing the crisis’s structural nature early and initiating bipartisan discussions around an “Economic Transition Act”: a framework combining fiscal deficit spending and AI inference compute taxation to fund direct transfers to displaced workers.

The most radical proposal on the table goes further. The “AI Shared Prosperity Act” establishes a public claim on returns from intelligent infrastructure itself—something between a sovereign wealth fund and AI royalty—funding household transfers via dividends. Private-sector lobbyists flooded media with slippery-slope warnings.

The politics around these discussions have predictably devolved into escalating partisan theater. The right labels transfers and redistribution Marxist, warning compute taxation surrenders leadership to China. The left warns tax legislation drafted by incumbent interests is just another form of regulatory capture. Fiscal hawks point to unsustainable deficits. Fiscal doves cite premature post-GFC tightening as precedent. This fracture will only widen as this year’s presidential election approaches.

While politicians bicker, social fabric unravels faster than legislative processes can respond.

The “Occupy Silicon Valley” movement has become a broader symbol of discontent. Last month, protesters blocked entrances to Anthropic’s and OpenAI’s San Francisco headquarters for three weeks. Their numbers grow—and media attention drawn by these protests now exceeds that generated by the unemployment data triggering them.

It’s hard to imagine anyone more hated by the public than bankers post-GFC—but AI labs are mounting a challenge. From the perspective of ordinary people, they have ample reason. Founders’ and early investors’ wealth accumulation speed makes the Gilded Age look modest. Productivity boom gains flowed almost entirely to compute owners and shareholders of labs built on compute—amplifying U.S. inequality to unprecedented levels.

Each side has its villain—but the real villain is time.

AI capability evolves faster than any institution can adapt. Policy responses run on ideological rhythms—not reality’s rhythm. If government can’t quickly reach consensus on what the problem is, this negative feedback loop will write the next chapter for them.

The Erosion of the Human Intelligence Premium

Across modern economic history, human intelligence has been the scarce production factor. Capital is abundant (or at least replicable). Natural resources are finite but substitutable. Technological progress was slow enough for humans to adapt. Intelligence—the capacity to analyze, decide, create, persuade, and coordinate—was the thing that couldn’t be scaled or copied.

The intrinsic premium on human intelligence stems from its scarcity. Every institution in our economy—from labor markets to mortgage markets to tax law—was designed for a world where that assumption holds.

We’re now experiencing that premium’s erosion. Machine intelligence has become a competitive—and rapidly improving—substitute for human intelligence across an expanding range of tasks. A financial system optimized for decades for scarce human intellect is being repriced. That repricing is painful, disorderly, and far from over.

But repricing doesn’t equal collapse.

The economy can find a new equilibrium. Reaching it is one of the few things still uniquely human. We must get it right.

This is the first time in history that the economy’s most productive asset generates fewer jobs—not more. No existing framework applies, because no framework was built for a world where the scarce production factor becomes abundant. So we must build new frameworks. Whether we build them in time is the only question that matters.

But you’re reading this—not in June 2028. You’re reading it in February 2026.

The S&P 500 sits near all-time highs. The negative feedback loop hasn’t begun. We can say with certainty that some of these scenarios won’t unfold. We can also say with certainty that machine intelligence will keep accelerating—and the human intelligence premium will narrow.

As investors, we still have time to assess how much of our portfolios rest on assumptions that won’t survive this decade. As a society, we still have time to act proactively.

The canary in the coal mine is still alive.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News