A Ten-Thousand-Word Review of U.S. Tariff History: History Doesn't Repeat Itself, but It Rhymes

TechFlow Selected TechFlow Selected

A Ten-Thousand-Word Review of U.S. Tariff History: History Doesn't Repeat Itself, but It Rhymes

Was the Trump administration's imposition of tariffs a masterstroke or a blunder?

Author: Citrini, Analyst

Translation: Felix, PANews

Amid the U.S. tariff hikes, the global economy appears to have entered a state of disorder. Are the Trump administration's tariff moves a masterstroke or a blunder? Analyst Citrini examines past tariff events through a historical lens to gradually unpack future economic trends. Below is the full article.

"This may perhaps be a mistaken view."

Benjamin Franklin wrote in 1781:

"But I find myself more inclined to adopt the more modern opinion, that it is best for every country to let trade proceed entirely without obstruction. On the whole, I only wish to point out that commerce is the mutual exchange of life’s necessities and conveniences; the freer and less restricted it is, the more prosperous it becomes, and the happier all participating nations will be. Restrictions imposed by nations on commerce seem to be enacted under the guise of public interest, but really serve their own private interests."

In the two weeks since "Liberation Day" (PANews note: Trump referred to April 2 as "Liberation Day" and announced his global tariff plan), I spent one week in the United States and one week in China. In both countries, I spoke with entrepreneurs affected by tariffs.

Whether importers or exporters, companies engaged in international trade to varying degrees across these two distinct regions share one thing in common: uncertainty.

Why this sense of uncertainty? Quite simply, nearly everyone alive today has only experienced a world of rising globalization, relatively free trade, and American dominance as the global superpower and reserve currency issuer.

As this assumption is now being challenged, investors and business operators are clearly seeking frameworks to navigate the future. For systems built on just-in-time principles, “wait-and-see” is a fatal strategy—but at present, there is no alternative.

For example, when speaking with a top 100 Chinese company by trade volume, they said: "We should normally be rushing to fulfill holiday orders right now. But so far, we haven’t received a single order." Anyone unfamiliar with how imported goods operate should understand two things: first, ordering products for an event typically happens eight months in advance. Second, we are undergoing a significant shift.

Chinese enterprises have long believed they could adapt to tariffs. In the past, a 10% tariff might prompt buyers to ask Chinese factories for price reductions (which was easily achievable). While factories clearly cannot offset tariffs exceeding 100% through pricing alone, they did believe they could still maintain cost advantages over domestic U.S. manufacturing after tariff hikes. But none of that matters when no transactions are taking place.

I haven't published a historical piece in over two years. Such articles aren't necessarily actionable. But this one feels timely. Sometimes, the only way to understand the future is to study the past.

Terms like mercantilism, isolationism, and protectionism are thrown around carelessly, with little regard for their meanings. Though not an economist, I am a student of economic history. Consider this piece educational—it doesn’t discuss which stocks to buy or sell, nor does it make directional calls on forex, equities, or interest rates.

Understanding Tariffs Through History

Few people today have directly experienced economic conditions similar to those shaped by tariffs in earlier eras. The definitive work on U.S. tariff history is Clashing over Commerce, which I’ve been rereading repeatedly over the past few weeks.

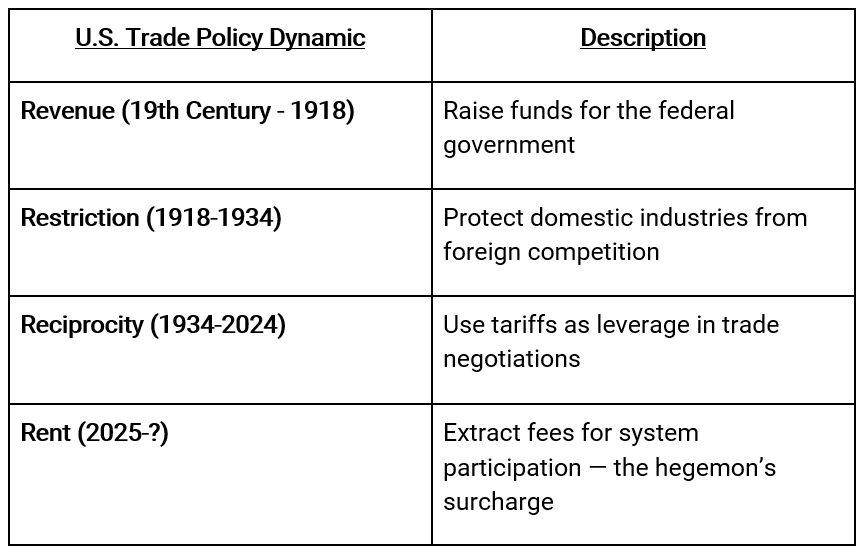

Authored by Douglas Irwin, a renowned historian and scholar of U.S. trade policy, the book introduces a “3R” framework for understanding the political economy of tariffs.

Historically, the U.S. tariff “3R” framework consists of:

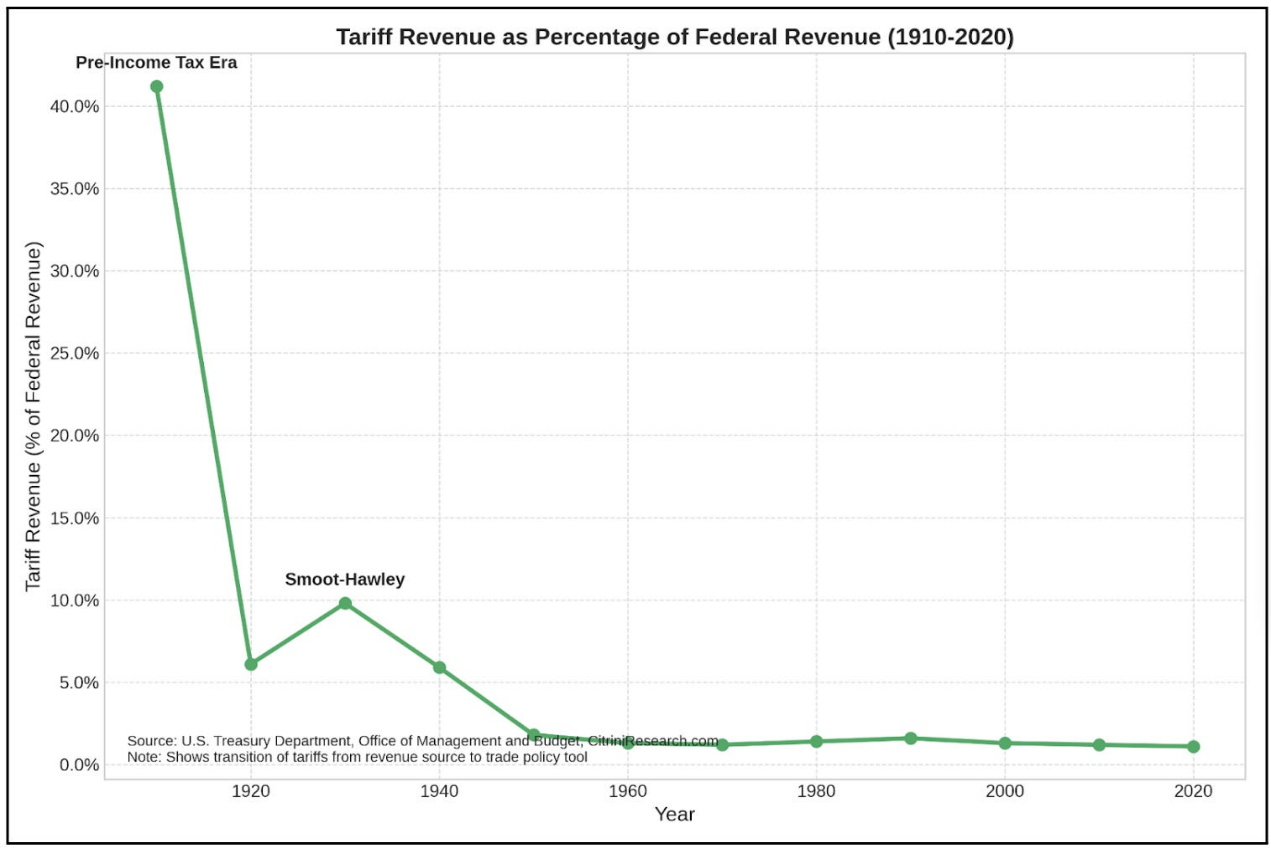

Revenue

Tariffs as a primary source of government income. This was especially true in the 19th and early 20th centuries.

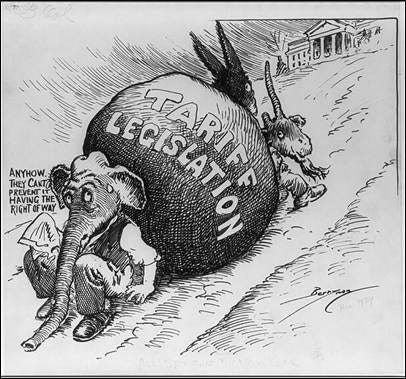

Tariff bills have long been criticized as opaque and difficult-to-manage policy tools—even as they served as the main source of government funding, as illustrated by this 1883 political cartoon.

Prior to the establishment of the IRS in 1913, the U.S. had no federal income tax. In the 19th century, tariffs accounted for over 90% of government revenue. At the time, tariffs were primarily used to generate revenue rather than for protectionist purposes—they were seen as a more palatable way to tax the population without provoking rebellion. For the first third of the 20th century, fewer than 15% of Americans paid income tax. The rest paid indirectly through higher prices on imported sugar, timber, and wool. Tariffs were the original invisible tax: collected at ports, paid at checkout.

Initially, they served as a means of funding the nation while avoiding internal taxation that might trigger political backlash—a lesson drawn from events like the Whiskey Rebellion. In Irwin’s account, revenue concerns dominated early republican trade policy, and even protectionist arguments had to be framed through a revenue-first lens.

Restriction

Tariffs as protection for domestic industries.

After World War I, tariffs became increasingly political tools aimed at shielding domestic industries from foreign competition—driven by protectionist motives.

Irwin notes that as revenue motives declined (thanks to the income tax), restriction-based motivations rose. After WWI, tariffs increasingly served industrial lobbying groups rather than the Treasury Department.

Reciprocity

Tariffs as bargaining chips in international trade negotiations.

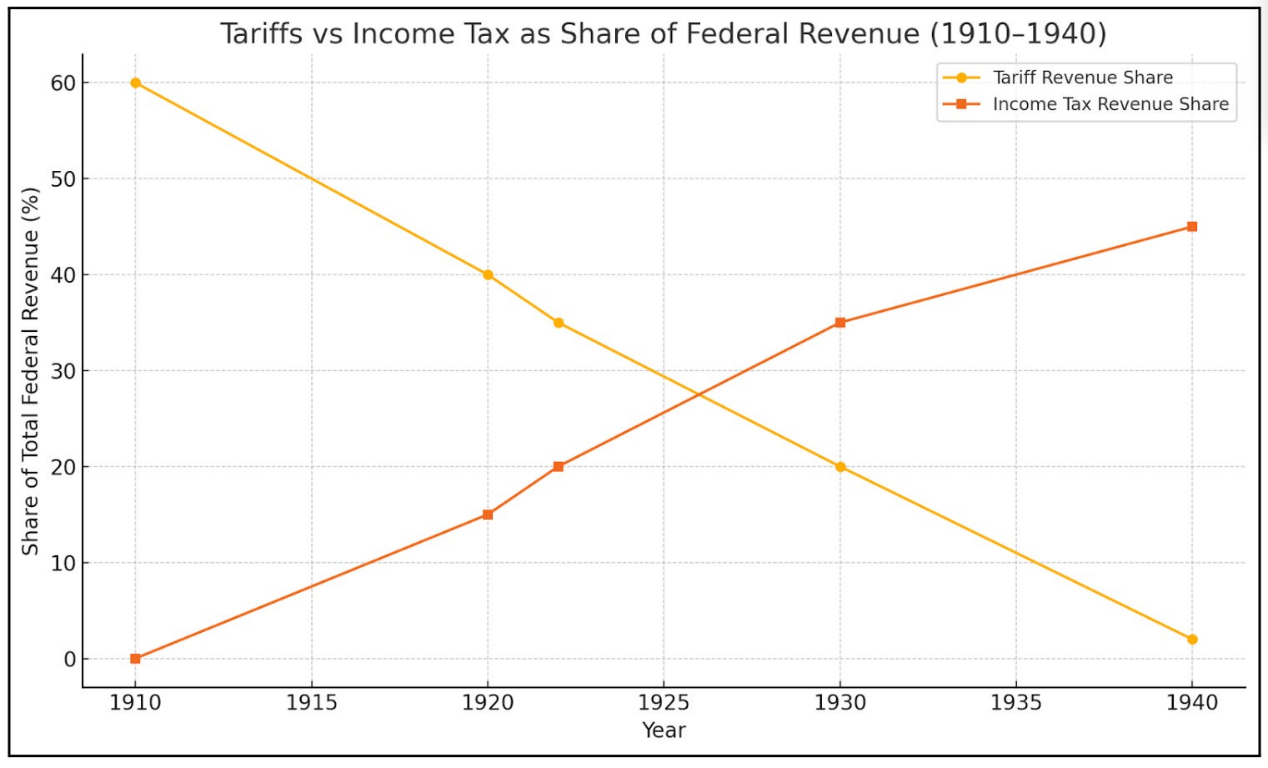

By 1934, income taxes had gradually replaced tariffs as the primary source of federal funding—the New Deal and WWII accelerated this shift. Tariffs evolved into leverage within global trade talks.

This is precisely the logic behind the 1934 Reciprocal Trade Agreements Act (RTAA), the General Agreement on Tariffs and Trade (GATT), and later, the World Trade Organization (WTO). The reciprocity era marked a turn toward liberalization and away from isolationism. The hegemonic power (the U.S.) lowered its tariffs in exchange for access to foreign markets. Tariffs ceased to be walls and instead became levers. Voluntary Export Restraints (VERs)—backroom deals pressuring countries to limit exports—replaced tariffs, eventually giving way to broader free trade agreements. This ushered in the multilateral free trade era of the late 20th and early 21st centuries.

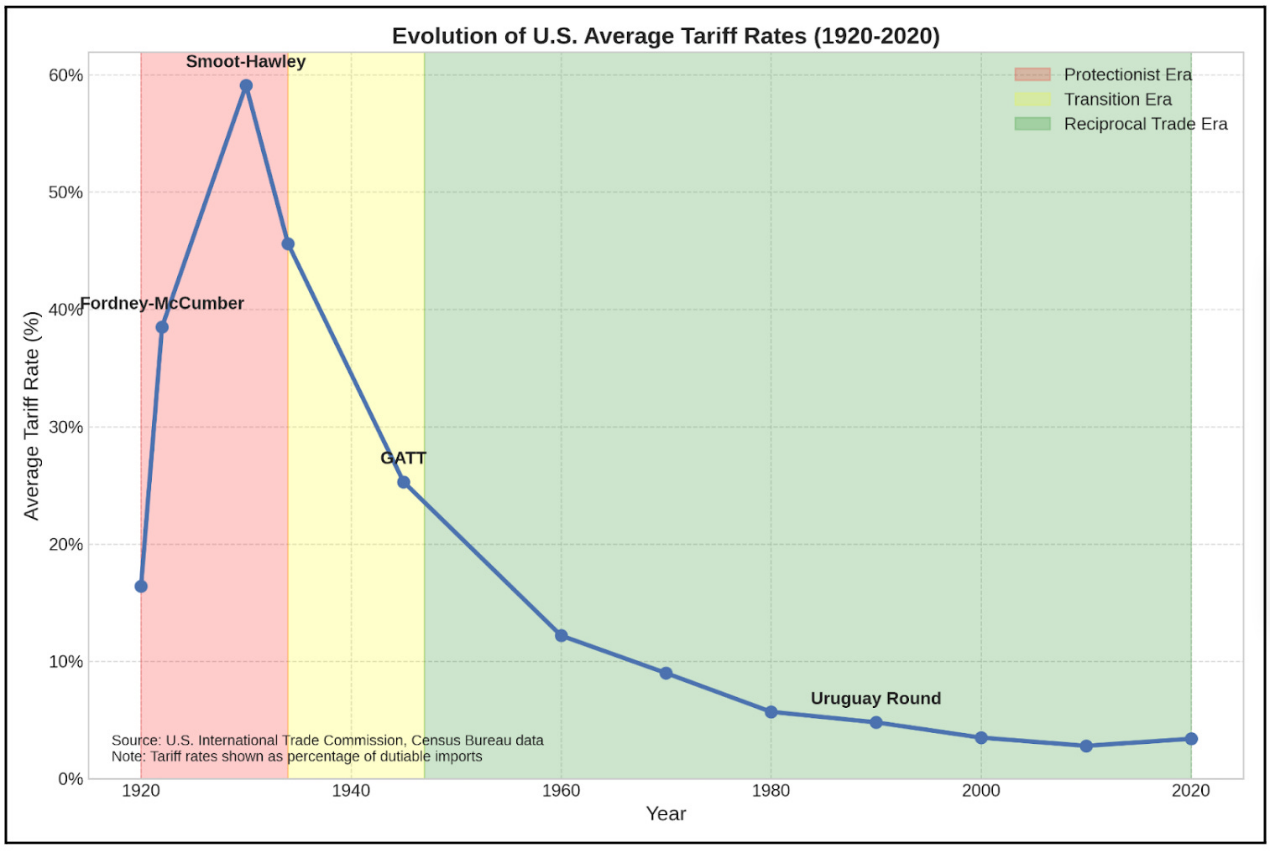

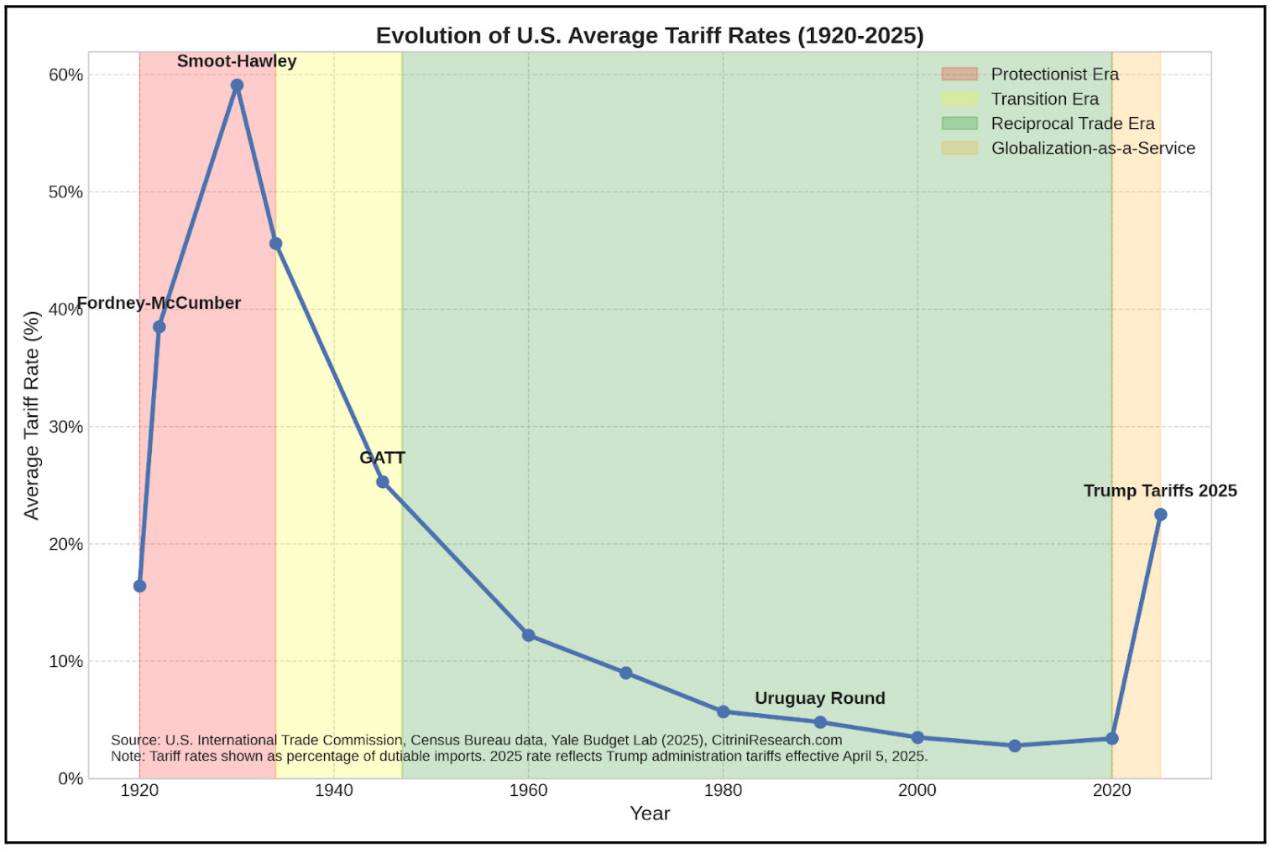

1922: The Fordney-McCumber Tariff

The Fordney-McCumber Tariff Act was an early prototype of excessive protectionism and the first real instance of tariffs levied for non-revenue purposes.

Picture post-WWI America: booming industrial output, yet struggling farmers. The biggest concern was cheap European competition—but Europe still owed the U.S. large war debts and couldn’t export to America due to rising U.S. tariffs. So naturally, the U.S. raised tariffs again.

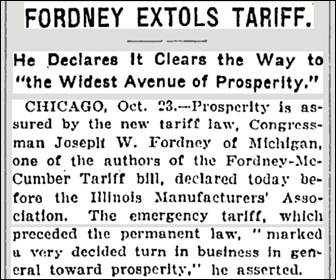

In 1921, Congress passed an emergency tariff bill, followed by the comprehensive 1922 Fordney-McCumber Tariff Act signed by President Warren Harding.

The law sharply increased tariffs well above the low levels set by the 1913 Underwood Tariff and higher than post-Civil War rates (though roughly comparable to the 1909 Payne-Aldrich Tariff on dutiable imports). It also granted the president authority to adjust rates up to 50% to “equalize domestic and foreign production costs.”

The results? Urban industry thrived in the 1920s while agriculture sank into prolonged depression. European trade surpluses shrank—surpluses they needed to repay wartime supplies purchased from the U.S.

For American industry, the 1920s were golden. Manufacturing output grew nearly 50% between 1922 and 1929. Unemployment dropped from 6.7% in 1922 to 3.2% in 1923. Industries like steel, chemicals, and automobiles flourished behind tariff walls. Protected sectors expanded, hired more workers, and profited. Corporate profits nearly doubled during this period.

Agriculture, however, faced the opposite fate. Farm income plummeted from $22 billion in 1919 to $13 billion in 1922. As cities prospered, rural America entered a decade-long depression—ten years before the Great Depression. Why? European markets closed in retaliation, while American farmers who had expanded production during the war now faced collapsing demand and prices.

In the 1920s, protectionism delivered concentrated benefits. If you were an urban industrial worker, it was a great time. If you were a farmer, it marked the beginning of two decades of hardship. Protectionist momentum had begun—and succeeded for some, at great cost to others.

1930: The Mistake

Massive tariffs, massive depression.

In 1928, Herbert Hoover was riding high. The great engineer won the presidency overwhelmingly: 444 electoral votes to Al Smith’s 87, winning more counties than even Warren Harding in 1920, and capturing 58% of the popular vote. The “prosperity president” promised Americans the “final triumph over poverty” in his inaugural address—words that would soon haunt him.

Stocks soared, unemployment was low, and Americans bought cars, radios, and refrigerators at unprecedented rates. The Republican-dominated Fourth Party System (PANews note: U.S. political landscape from 1896–1932) seemed as entrenched as ever.

Like his Republican predecessors, Hoover was a staunch supporter of protective tariffs. During his campaign, he declared: “For seventy years the Republican Party has stood for a tariff policy that gives adequate protection to American labor, American industry, and the American farm against foreign competition.” He made tariff protection—especially for agriculture—the cornerstone of his economic agenda.

As Secretary of Commerce under Harding and Coolidge, Hoover developed a clear protectionist philosophy: the U.S. should restrict imports mainly to goods it couldn’t produce domestically. This wasn’t radical—it was the pinnacle of McKinley-era Republican tradition, a natural extension of the Fourth Party System’s economic orthodoxy.

Hoover cited the “success” of the Fordney-McCumber Tariff (since its passage, total U.S. imports had grown) as proof that America could protect domestic industry while expanding sales in Canada. In 1926, he wrote: “Given the broad prospects of our trade, we can dismiss the fear that raising tariffs would greatly reduce our total imports and thereby destroy other countries’ ability to buy from us.” In a 1928 campaign speech, he stated: “The idea that we cannot have both protective tariffs and growing foreign trade is baseless. Today, we have both.”

Then came Black Thursday, October 24, 1929, followed five days later by Black Tuesday, when stock market value evaporated by over $30 billion—nearly twice what the U.S. spent in WWI. The Roaring Twenties ended abruptly. Amid the turmoil, tariff debates didn’t subside—they intensified:

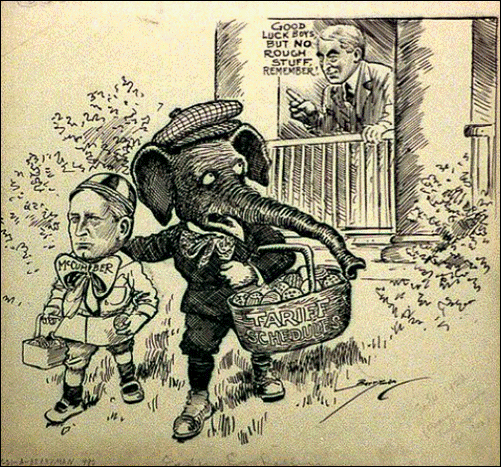

Rather than reconsidering tariff legislation in light of economic shock, Congress doubled down. An initial agricultural tariff bill morphed into what became known as the Smoot-Hawley Tariff Act, named after its chief sponsors—Senator Reed Smoot of Utah and Representative Willis C. Hawley of Oregon. A bill initially meant to aid farmers transformed into an industrial protectionist monstrosity.

A targeted effort to protect American farmers spiraled into a protectionist free-for-all. Between 1929 and early 1930, the number of protected industries grew exponentially during congressional deliberations. Ultimately, the act raised tariffs on over 20,000 imported goods, setting the highest tariff rates in U.S. history since the infamous 1828 “Tariff of Abominations.”

Cartoon depicts a weary Republican elephant sitting in the middle of the road leaning on a large rock labeled “Tariff Bill”

The market wasn’t convinced. Despite deep disagreements among economists about how to escape the Depression, they agreed on one thing: passing this bill would be disastrous.

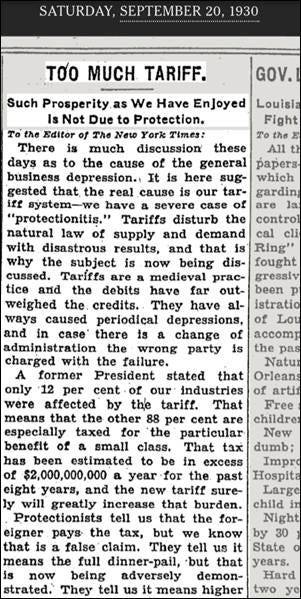

They wrote to Hoover, pleading for a veto:

Front-page news, May 8, 1930

Thomas Lamont, partner at J.P. Morgan, later recalled: “I almost went down on my knees to beg Herbert Hoover to veto the stupid Hawley-Smoot Tariff Act. That measure intensified nationalistic feelings all over the world.”

Henry Ford spent an entire night at the White House trying to convince Hoover the tariff would cause severe economic damage.

Yet on June 17, 1930, Hoover signed the bill. Political suicide wasn’t immediate—but this move was enough. Public disdain grew rapidly, evident in the flood of reader letters in The New York Times:

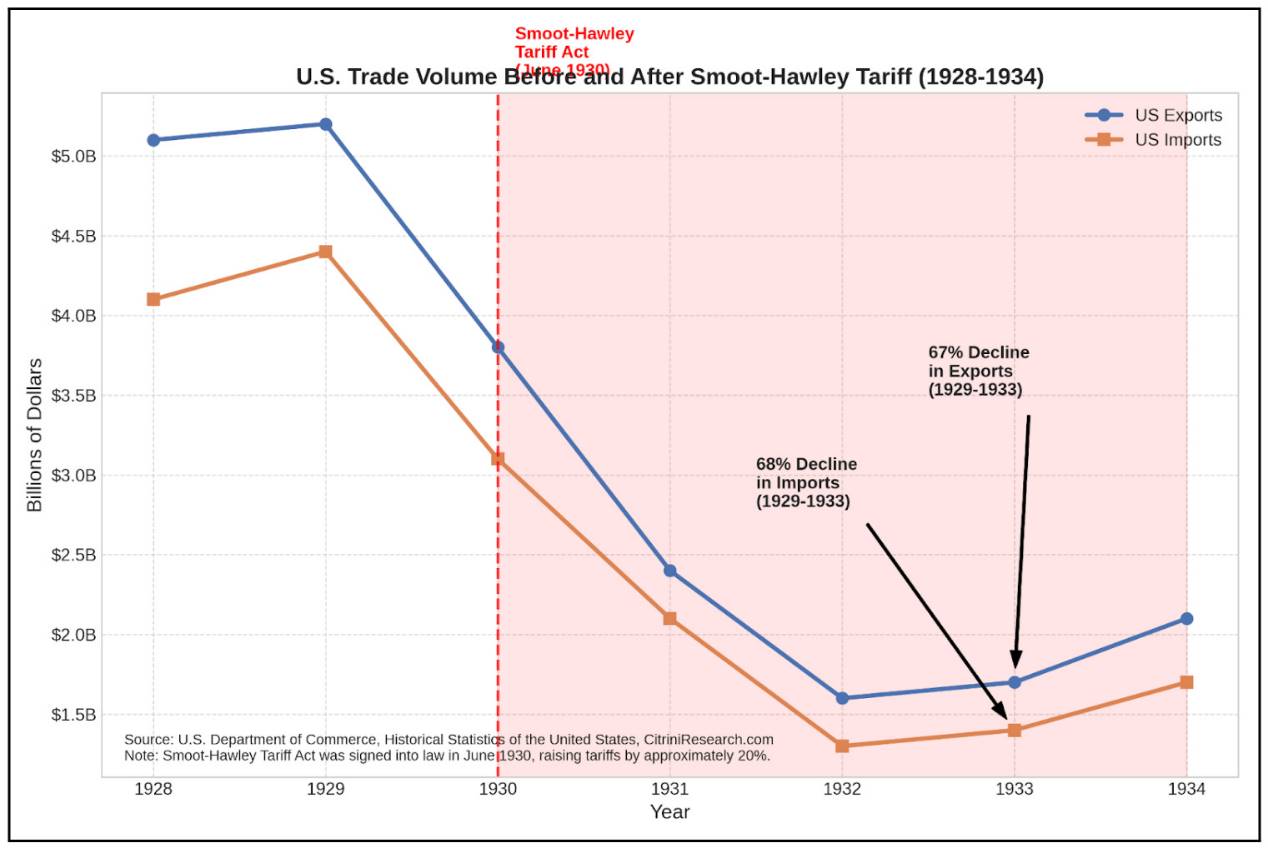

What followed was exactly as predicted: over 25 countries retaliated. Global trade collapsed.

U.S. imports fell from $4.4 billion in 1929 to $1.3 billion in 1932. Exports dropped from $5.4 billion to $1.6 billion in the same period. World trade declined by roughly two-thirds between 1929 and 1934.

The 1929 stock crash triggered recession, but tariffs turned it into the Great Depression.

It started as a financial shock but became systemic because policy—especially the Smoot-Hawley Tariff—strangled supply just as demand was falling.

As economists predicted, American consumers and businesses paid the price. Tariffs may have preserved some jobs in protected sectors, but they destroyed far more by raising input costs and closing foreign markets to U.S. exports.

Democrats recognized the disaster and made tariff reform a centerpiece of their 1930 midterm campaign—the first time since 1918 they gained control of both houses of Congress. Roosevelt later said of the Smoot-Hawley Tariff: “It forced世界各国 to erect such high tariff barriers that world trade is being reduced to the vanishing point.”

The outcome was clear: the Smoot-Hawley Tariff was a complete failure.

How Was the 1922 Tariff Different From 1930?

First, the starting point: the Fordney-McCumber Tariff was implemented during a period of relative global growth, particularly in the U.S. The prosperity of the Roaring Twenties masked many inefficiencies. In contrast, the Smoot-Hawley Tariff passed after the 1929 stock crash, when global demand was already weakening. It made a bad situation worse. From a protectionist standpoint, tariffs acted as a catalyst for depression—but they still required a triggering event.

In 1922, business and consumer confidence was high, credit abundant, and financial conditions loose. By 1930, bank failures, plunging stock prices, and credit crunches were widespread. Enacting Smoot-Hawley—raising rates across 20,000 items—was pouring gasoline on fire, signaling reckless policy at a critical moment and further spooking investors fearing escalating protectionism.

Second, retaliation. Fordney-McCumber provoked limited retaliation (e.g., France in 1928, selective tariffs by some European nations), but global trade continued expanding in the 1920s. One can easily measure the direct economic damage of Smoot-Hawley—raising average U.S. tariffs on dutiable imports to 59.1%, the highest since 1830. But the real catastrophe wasn’t the tariffs themselves, but the global retaliation they triggered.

Canada, then America’s largest trading partner, hadn’t retaliated significantly to prior U.S. tariff hikes. The 1922 Fordney-McCumber Tariff raised duties on key Canadian exports like wheat, cattle, and milk, but producers viewed them as returning to pre-WWI levels—bearable.

Smoot-Hawley was different. With the global economy deteriorating, Canadian exporters were already suffering. Just one month after Smoot-Hawley passed in July 1930, Canada’s Liberal government lost to Conservative leader Richard Bennett, who fulfilled his campaign promise to “force open” world markets via tariffs. Push a country to desperation, and its reaction becomes unpredictable.

In September 1930, Canada sharply raised tariffs on 16 U.S. products, accounting for about 30% of U.S. exports to Canada. Not satisfied, it negotiated preferential trade deals with other Commonwealth nations, further undermining U.S. competitiveness.

Retaliation didn’t stop at Canada. By 1932, at least 25 countries had retaliated against U.S. goods. Spain introduced the “Veri Tariff” targeting American cars and tires. Switzerland boycotted U.S. products. France and Italy imposed quotas. Britain abandoned its traditional free-trade stance and adopted protectionism. This created a downward spiral, freezing global trade amid uncertainty and escalating tit-for-tat policies.

Third, global financial conditions. In 1922, the U.S. was an emerging creditor nation, but the gold standard wasn’t fully restored, and many countries were recovering from WWI. There was no tightly integrated global financial system. By 1930, however, the gold standard had been reestablished globally. Links between international trade and debt flows were tighter.

Finally, symbolism. While poorly designed, the Fordney-McCumber Tariff was expected. Since the Civil War, tariffs had been normal in the U.S.; many trade partners saw it as a return to pre-WWI levels. But Smoot-Hawley was perceived as escalation during obvious global fragility. It signaled America turning inward just as it solidified its creditor status. It undermined confidence in global coordination and may have prompted many countries to abandon the gold standard shortly afterward.

Markets and policymakers interpreted Smoot-Hawley not just as a tariff issue, but as a worldview: isolationist, chaotic, irrational. Uncertainty crushed business investment.

It was a unique, unprecedented disaster of protectionist trade policy—one that paved the way for Roosevelt’s election. Roosevelt swiftly repealed the tariffs and passed the Reciprocal Trade Agreements Act (RTAA).

1934: RTAA – The Dawn of Reciprocity

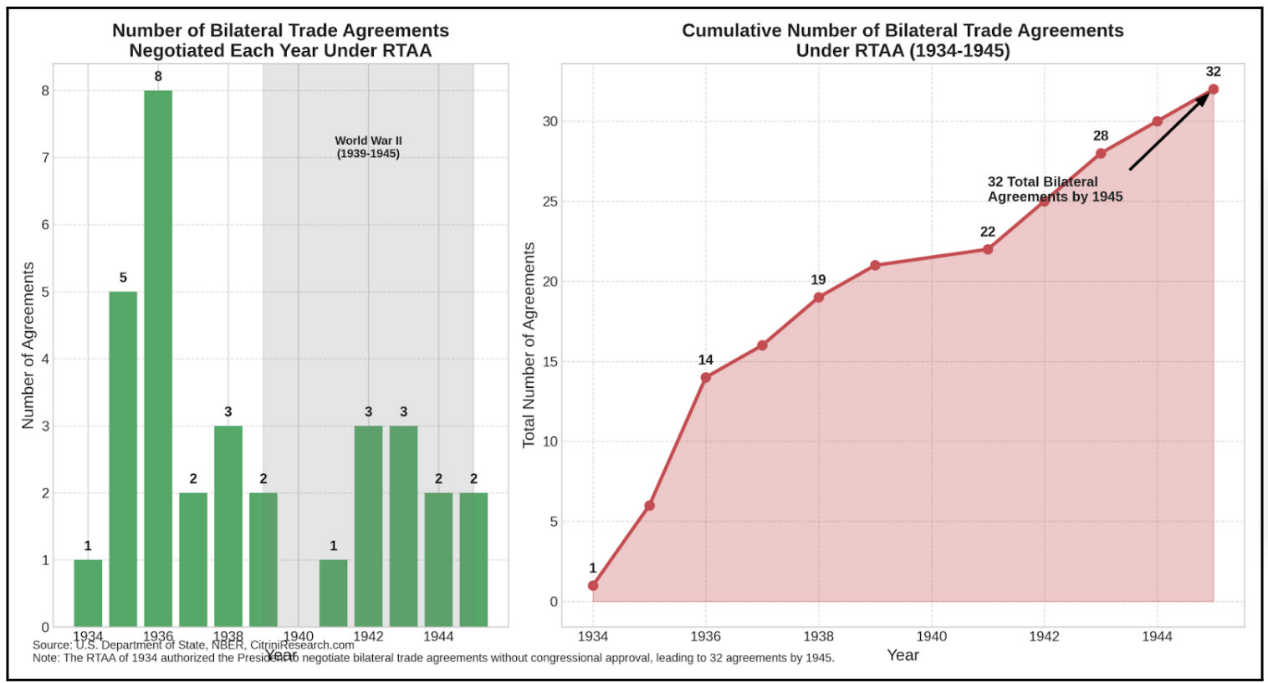

After the protectionist disaster of Smoot-Hawley, U.S. trade policy reached a crossroads. The 1934 Reciprocal Trade Agreements Act (RTAA) marked a shift of trade decision-making power from Congress to the executive branch, initiating the transition from “restriction” to “reciprocity.” This institutional change fundamentally reshaped how trade policy was made and laid the foundation for the freer postwar trade regime.

Modern international trade history begins with Cordell Hull, a Democrat from Tennessee who became the longest-serving U.S. Secretary of State. His roots in agrarian southern politics deeply shaped his views on tariffs and trade. Unlike Northern colleagues focused on protecting manufacturing, Hull understood high tariffs hurt agricultural exports.

Signing the U.S.-Canada Trade Agreement. (Front row, left to right): Cordell Hull, W.L. Mackenzie King, Franklin D. Roosevelt, Washington, D.C.

November 16, 1935

Hull’s understanding of trade’s international dimension developed gradually. He later recalled that before coming to Washington, he “had personally participated in bitter tariff wars—but they were domestic battles, debating whether high or low tariffs were good for the home country. Little thought was given to their impact on others.”

The RTAA emerged from the wreckage of Smoot-Hawley. While Smoot-Hawley, as a protectionist act, severely hindered world trade through retaliatory tariffs, the RTAA opened a new path for international cooperation. It introduced three revolutionary concepts that defined the reciprocity era:

-

Executive Authority: For nearly 150 years, Congress jealously guarded its constitutional power to “regulate commerce with foreign nations,” resulting in trade policy driven by local interests. The RTAA transferred substantial negotiating power to the president, allowing him to reduce tariffs by up to 50% without requiring item-by-item congressional approval.

-

Bilateral Reductions: The act enabled targeted negotiations with individual trading partners, creating a more strategic approach to trade liberalization and giving export-oriented industries equal footing with import-competing ones at the negotiating table.

-

Most-Favored-Nation (MFN) Clause: Any tariff reduction negotiated with one country would automatically apply to all nations with commercial agreements with the U.S., creating a multiplier effect that accelerated global trade liberalization.

Though initially focused on bilateral deals, the act created a template later used as a reference for global trade architecture

1947: Bretton Woods and GATT – Rules for a War-Torn World

As WWII ended, architects of the postwar economic order gathered at a resort hotel in New Hampshire’s White Mountains. The Mount Washington Hotel in Bretton Woods lent its name to the system they designed—an architecture intended to prevent the economic nationalism and financial instability that contributed to WWII.

The July 1944 Bretton Woods Conference brought together 730 delegates from 44 Allied nations for three weeks of intense negotiations. It reflected two competing visions for the postwar economy. On one side was British economist John Maynard Keynes, representing a war-ravaged UK dependent on U.S. financial aid. On the other was Harry Dexter White, representing the now-dominant U.S. economic powerhouse.

Keynes proposed an ambitious “International Clearing Union” featuring a global currency (“bancor”) that would automatically balance trade and prevent excessive surpluses or deficits. White’s plan was more conservative: preserving national monetary sovereignty while establishing stable exchange rates anchored to the dollar, convertible to gold at $35 per ounce.

White’s plan largely prevailed, though it incorporated important concessions to Keynes’ concerns about adjustment flexibility. The final agreement created two key institutions: the International Monetary Fund (IMF), tasked with monitoring exchange rates and providing short-term financing to countries facing balance-of-payments difficulties; and the International Bank for Reconstruction and Development (IBRD, now part of the World Bank), focused on long-term lending for reconstruction and development.

The Bretton Woods system represented a compromise between the rigidity of the pre-1914 gold standard and the chaotic currency wars of the interwar period. Countries maintained fixed but adjustable exchange rates against the dollar, which served as the anchor through its gold link. The IMF provided short-term liquidity to nations with temporary balance-of-payments problems, allowing adjustments without immediate austerity or competitive devaluations.

The system was explicitly designed to prevent the catastrophic economic nationalism of the 1930s. By offering liquidity and support, it aimed to give countries breathing room to maintain domestic stability and international cooperation. The architects knew that the tension between domestic goals and international obligations had torn apart the interwar economic order. Crucially, they recognized that monetary stability alone wasn’t enough.

A complementary trade framework was needed. This materialized in the 1947 General Agreement on Tariffs and Trade (GATT).

While the U.S. and UK agreed on the overall framework, they clashed on core issues. The U.S. wanted to eliminate Britain’s Imperial Preference system. Britain demanded significant U.S. tariff reductions, which had remained high since Smoot-Hawley. The compromise? Multilateralization—to depoliticize, diffuse pressure, and spread risk.

Its core pillars:

-

Most-Favored-Nation (MFN): Every trade concession granted to one member must be extended to all.

-

Tariff Bindings: Once tariffs are reduced, they cannot be raised unilaterally.

-

Elimination of Quotas (mostly): Because nothing screams “central planning” quite like chicken import restrictions.

In the following decades, successive GATT rounds (Annecy, Torquay, Dillon, Kennedy, Tokyo, Uruguay) progressively reduced global tariffs, transforming a temporary postwar truce into a functioning world order. By 1994, GATT evolved into the WTO, with average global tariffs falling from 22% to below 4%. Starting with 23 founding members, it expanded to include most of the world’s trading nations, witnessing explosive growth in international trade over the postwar decades.

GATT’s brilliance lay in its simplicity. It treated tariffs like nuclear weapons: dangerous to use, contagious when retaliated against. Its core principle wasn’t that all trade is beneficial, but that any retaliatory protectionism is harmful. Effectively, it was a behavioral pact: no weaponized tariffs. No trade collapse. If you raise barriers, you pay. If you make a deal, you share.

That’s why GATT proved unexpectedly durable. For decades, it worked simply because when it failed, everyone remembered what happened.

However, the Bretton Woods monetary system proved less resilient. Facing persistent balance-of-payments deficits and declining gold reserves, President Nixon suspended dollar convertibility to gold in August 1971, effectively ending the fixed-exchange-rate Bretton Woods system.

1971: End of Dollar-Gold Convertibility

From the Age of Exploration to the colonial era (roughly 1400s to mid-1900s), gold and silver widely served as currencies for international trade settlement. Spanish silver dollars were especially common (the word “dollar” originates from silver mines). Generally, fiat money based on IOUs functioned well locally (where trust and enforcement were feasible), but failed internationally.

For example, during the Golden Age of Piracy, the Caribbean was a melting pot of European colonial empires (Britain, France, Netherlands), all using Spanish silver dollars for trade. The Spanish Empire was the largest silver source, minting standardized, ubiquitous coins. Even on the other side of the globe, China accepted only silver—particularly Spanish silver dollars—in exchange for tea sold to Britain.

During the era when the pound (backed by gold) was the dominant reserve currency, the U.S. became the world’s largest economy during its late 19th-century industrial revolution and emerged as the acknowledged military superpower by 1944. After 1971, the dollar became the first true fiat global reserve currency. One could say that due to winner-takes-all network effects, the dollar became—and remains—the dominant global reserve currency.

The implications for the U.S. economy aren’t hard to grasp:

Because gold and silver deposits are globally distributed, even the Bretton Woods system meant no single country was the sole source of global reserve assets. Under Bretton Woods (1944–1971), currencies were pegged to the dollar, which was convertible to gold at a fixed rate. Thus, besides gold itself, currencies like the pound and Swiss franc served as functional alternatives to reserve assets.

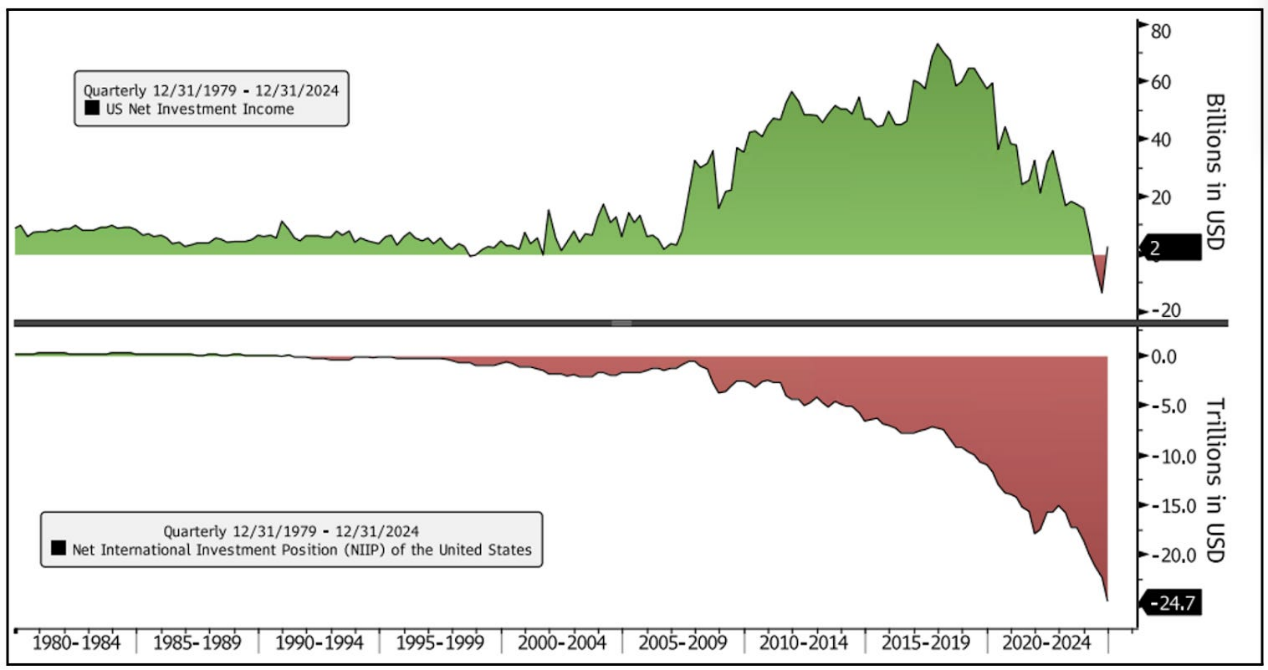

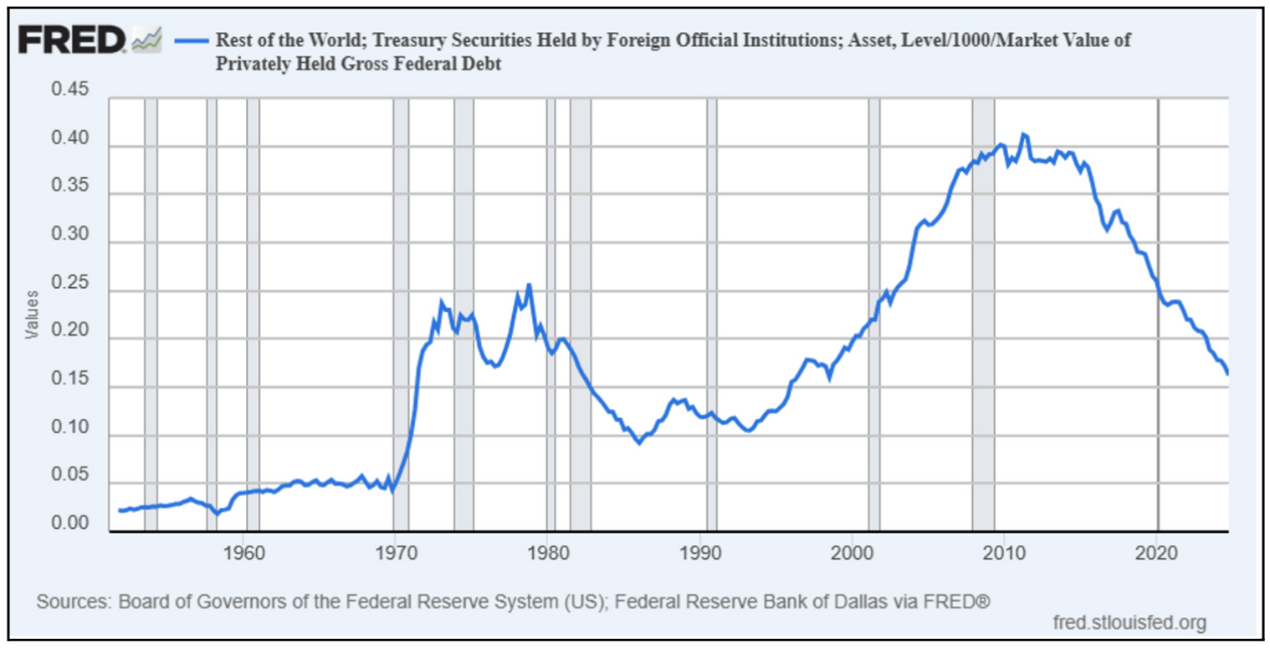

Somewhat surprisingly, the 1971 collapse of Bretton Woods actually strengthened the dollar’s role as the world’s reserve currency. As the sole major provider of reserve currency, the U.S. settled into a dynamic of persistent trade deficits to supply liquid reserve assets to the rest of the world. This seems paradoxical—initially, the dollar was abandoned in favor of “real” things like gold. But in the 1980s, Volcker reestablished the dollar’s global reserve status. By 1980, gold was no longer a one-way bet against the dollar. It was exposed as a volatile commodity prone to speculative booms and busts—not a stable store of purchasing power. Since the 1980s, the U.S. has struggled to achieve trade surpluses (given the natural tendency of the rest of the world to accumulate financial wealth denominated in reserve currencies).

Still, the dollar’s reserve status hasn’t come without benefits for the U.S. The concept of “exorbitant privilege” means that despite the rest of the world holding more U.S. assets than vice versa, the U.S. actually earns higher returns on its overseas investments. This is because much of what foreigners hold in the U.S. takes the form of high-quality, low-yielding dollar-denominated balances and fixed-income securities (e.g., U.S. Treasuries, agency MBS).

When international trust and enforceability exist (and they have, for decades), IOU-based fiat systems can function globally. But the U.S.-led global order is now being questioned—not by others, but by the U.S. itself.

Where Do We Go From Here?

Although the world has changed dramatically since the post-WWII reciprocity era, the fundamental tensions shaping U.S. tariff history remain. Today stands at a juncture akin to 1930, 1947, and 1971—moments that reshaped trade policy. Just as those turning points were driven by shifts in America’s position within the global order, today’s tariff resurgence reflects another recalibration of economic power. Yet there’s a crucial difference: America is now actively dismantling the very system it built.

This crisis won’t end in three months.

Everything the U.S. does in the next three months isn’t about easing trade burdens or reverting to rational models (like a flat 10% tariff with targeted reciprocity). This is the opening shot. The focus will center on isolating China, attempting to force it to the negotiating table. If you’re not with us, you’re against us.

U.S. warehouses hold 2–3 months’ worth of inventory—enough to buffer or distort the initial impact of disrupted global trade. As these stocks deplete, we’ll begin to see the true effects of frozen global trade and its ripple consequences. Foreign exchange reserve managers will continue reducing dollar allocations as the dollar enters a long-term bear market.

A tariff pause is a tactical move in ongoing negotiations. A permanent U.S.-China resolution within the next 2–3 months is unlikely, but indirect progress may occur in trade talks with Europe or Latin America. Markets may interpret this as de-escalation, but reality is it heightens business uncertainty. To survive the next 90 days, clarity is essential…

How to Understand the Government’s View?

In this context, understanding the government’s perspective is valuable. In Trump’s view, American hegemony and reserve currency status are unfair burdens—not only costing the U.S. advantages in trade and manufacturing but also forcing it to “freely” maintain the global trade system. Hence, the current U.S. stance can be summarized roughly as:

The strange thing isn’t the use of tariffs—that’s not surprising. Trump has long loved tariffs. If you’re shocked that the “tariff man” uses tariffs, you should probably find another job.

What’s surprising is that all three “Rs” have returned simultaneously—yet still don’t tell the full story.

Revenue: Billions in new federal income, not called a tax hike but functionally equivalent.

Restriction: Not just an industrial strategy, but a populist aesthetic—a wall erected at ports instead of borders, applicable to everything.

Reciprocity: Shifted from mutual barrier reduction to score-settling based on trade deficit calculations.

Other forces are at play too—this isn’t merely about revenue, but about the nature of the act and the uniquely globalized world in which it occurs. A fourth “R” is needed to define the transformation represented by seemingly simple tariff hikes. Because we aren’t truly reverting to past dynamics—we’re entering a new paradigm.

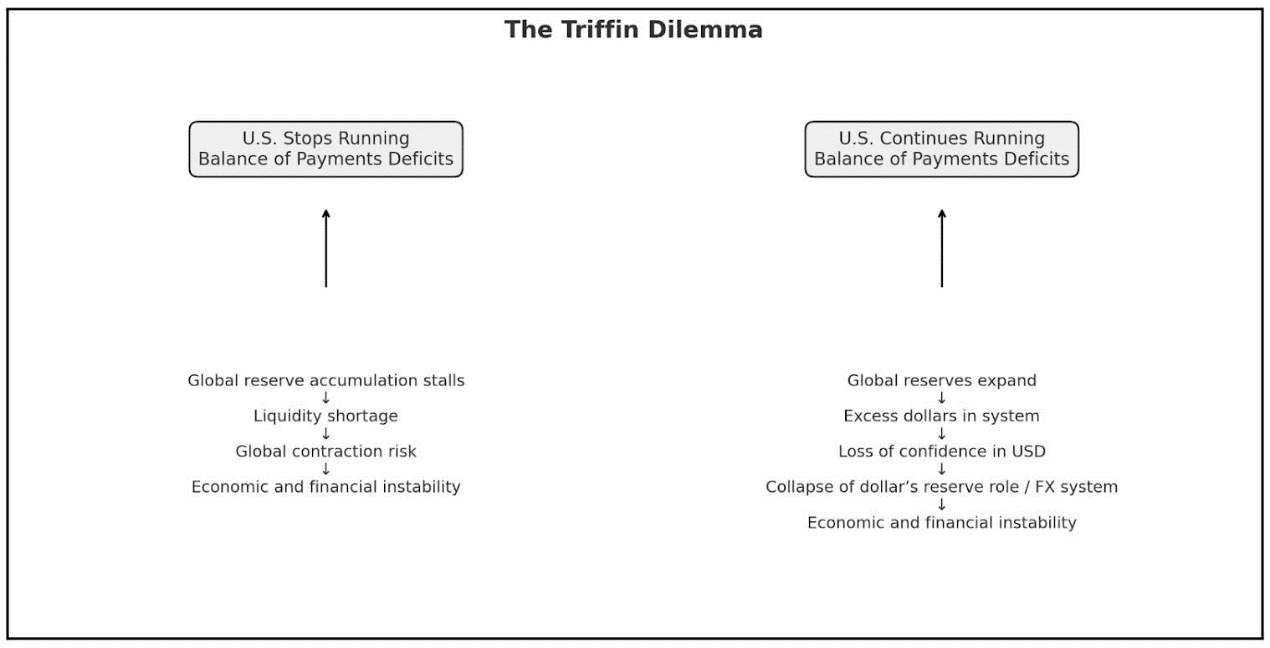

To grasp this, one must fully understand the government’s viewpoint. In our earlier article “Seeing the Stag,” we discussed challenges in rebalancing global trade by targeting other nations’ deficits. The “Triffin Dilemma” describes the paradox faced by a reserve currency nation (present even before the end of dollar-gold convertibility):

“It is too much to expect a single country and currency to provide the world with reserves and convertibility.” — Henry H. Fowler, U.S. Treasury Secretary

Unsurprisingly, the Trump administration interprets the Triffin Dilemma less as an IMF white paper and more as an overdue invoice. They believe America has been exploited, forced into running external trade surpluses, and want to correct it. By imposing tariffs based on bilateral trade deficits, they clearly signal their priorities and concerns.

From the Trump administration’s perspective, what has occurred/continues to occur in the existing system includes:

-

Foreign central banks buy dollars not out of preference, but obligation—if you want to suppress your currency and boost exports, you must hoard dollars.

-

Those dollars end up in U.S. Treasuries, conveniently funding the very same U.S. government that complains about being taken advantage of.

-

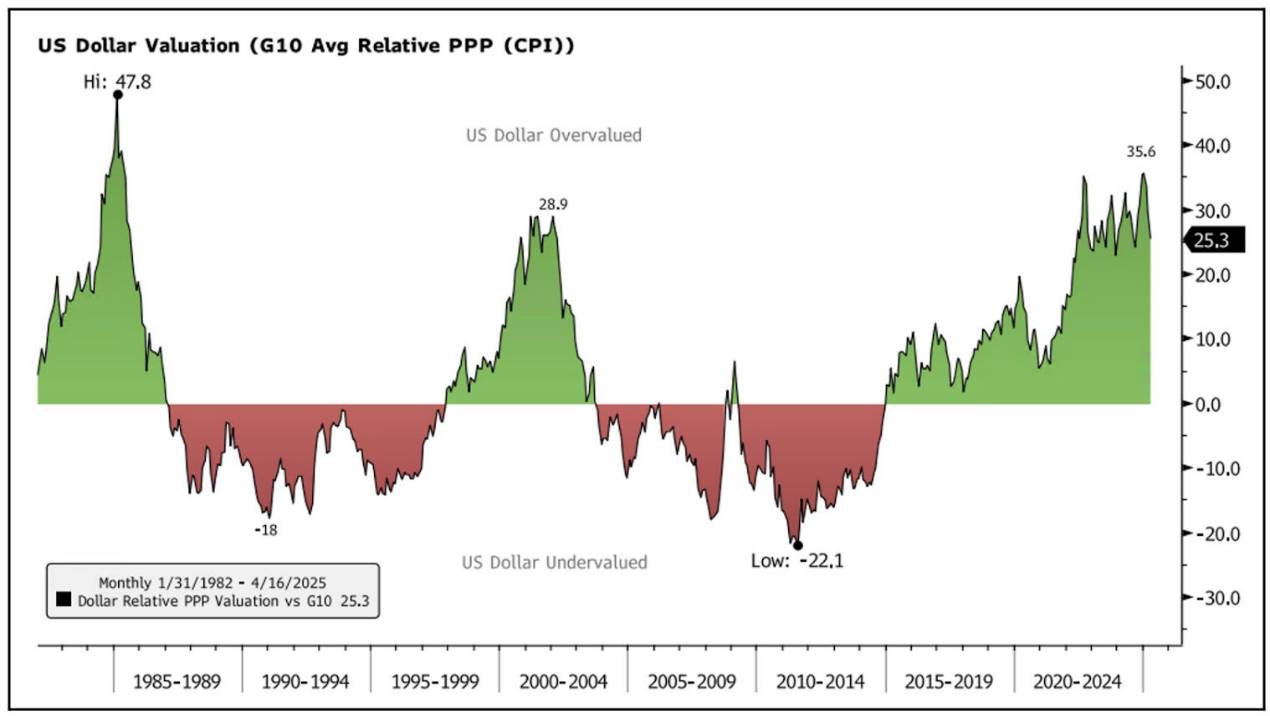

The dollar remains structurally overvalued—a direct result of its role as everyone else’s savings account and lifeboat.

-

U.S. manufacturing has been hollowed out—not because China cheated, but because America plays system administrator in a network it can’t fully control.

-

Trade deficits keep widening. Trump dislikes the word “deficit” and the idea of being the world’s biggest “debtor.” The reserve currency role is increasingly seen as a liability, not a privilege.

From this angle, tariffs aren’t merely about protecting factories or funding government. They’re overdue maintenance fees for the system. In effect, they’re geopolitical “rent”—like forgetting your subscription and getting charged $14.99 monthly. Simpler still, the government’s view is:

“We manage this system—regulating flows, securing shipping lanes, buying your exports, issuing your reserve assets. Now we’re charging you for it.”

The Fourth R: Rent

Rent redefines tariffs as a pay-for-service model for global economic participation, rather than tools for generating national revenue (revenue), protecting domestic producers (restriction), or ensuring reciprocal access (reciprocity). This new model is essentially…

Globalization-as-a-Service

Tariffs, NATO threats, opposition to foreign acquisitions—are forming a deliberate pattern: leveraging every available tool to extract national wealth from dependent foreign states. Even if doing so undermines global trade and the dollar’s reserve asset status.

Tariffs are crude tools, but Trump clearly sees them as part of a broader negotiation to dismantle the existing system. The 125% tariff on China is the clearest example. Such a high tariff disrupts trade. So why not use sanctions or quotas? Because opening negotiations from a “pay the fee” perspective is crucial.

Negotiations during the 90-day tariff pause could yield various outcomes. The main goal will be building a coalition to force China to the table, but we may also start hearing discussions about permanently instituting this “fee.”

How Is the Rent Paid?

I’ve always been skeptical of the “Mar-a-Lago deal” idea, and it’s extremely unlikely to happen. Still, analyzing it is instructive. A proposed issuance of 100-year bonds might bring unintended negative consequences, but it perfectly illustrates how the fourth “R” (Rent) could function.

The idea: issue 100-year U.S. Treasuries with negative real yields, and encourage (or force) countries to swap existing long-dated bonds into these new instruments. This would allow the U.S. to extract additional economic benefit from maintaining its role as global reserve currency issuer and trade facilitator.

Despite unpredictable—and potentially chaotic—effects, including damaged credibility and severe yield curve disruption, Trump might enthusiastically offer tariff relief (or deep cuts) to countries agreeing to swap their debt into century-long, negatively yielding bonds. After all, he’s spent his life restructuring and refinancing debt across his various enterprises.

This is just one example—and an improbable one. Stephen Miran recently stated he doesn’t advocate this idea. But the truth is, Trump is challenging existing international rules and questioning the roles of the dollar and U.S. Treasuries. Why? Because he focuses only on the immediate fiscal impact for America. This view risks missing the forest for the trees.

If the U.S. effectively defaults on foreign-held Treasuries via hostile century-bond swaps/issuances, gold prices could surge and the dollar fall. The impact on the yield curve would be dramatic. Even absent this scenario, official FX reserves will likely diversify further into gold, euros, francs, and yen. Trade settlements in non-dollar currencies may also emerge.

Given this potential reality, it’s unsurprising that official holdings of U.S. Treasuries by foreign nations have been declining for years:

Current U.S. policy can easily be seen by others as extortion. This economic brinkmanship is inherently risky. If it fails, it’s like a bank that’s also its own customer, taking out a loan… then deciding to default unilaterally.

Yet the reality remains: nations are negotiating with someone ready to destroy the entire system regardless of consequences. It’s easy to see why many would rather submit than face a de-globalized world and its hardships.

Can this unfold without severely damaging the global economy? Possibly. But there will be no quick restoration of global trust in America.

No matter how negotiations proceed, it’s clear that trade policy will be the primary driver of cross-asset returns and economic growth this year. Clearly, we’re witnessing an institutional transformation that will shape macroeconomic outcomes for years.

Under this new regime, tariffs are less policy and more precedent. The U.S. has signaled it will treat market access as a dial, tightening or loosening trade terms based on geopolitical compliance rather than economic efficiency. Regardless of whether the government proposes sweeping tax cuts or other supportive measures, the pace and manner of U.S.-China trade negotiations will ultimately determine outcomes.

Right now, nothing matters more. The U.S. and China have rapidly escalated into a Smoot-Hawley-style retaliatory spiral, with tariffs reaching 145%.

Thus, despite vastly different circumstances, it’s not hard to empathize with the despair felt by economists and bankers in 1930 as they watched the Smoot-Hawley trade war erupt. Globalization has become something like economic mutually assured destruction. There might be “winners.” Perhaps one country is only 80% destroyed while others are obliterated. But is this really the world we want?

Unlike the Hoover administration, the Trump administration faces the contradiction of being both a debtor nation and a trade restrictor. While both ignored economists’ warnings and tried to preserve American status via tariffs, Hoover’s policies were mainly defensive (though misguided) attempts to protect U.S. industry. Today’s approach adds an offensive layer: deliberately using America’s debtor status as leverage to transform the global trade and financial system from a public good into a private toll road.

It might be tempting to look back to the last time tariffs were this high and say, “Well, it could happen again,” but that approach is flawed.

The Return of the Tariff Nation?

Today is not the 1890s or 1930s. The world is now globalized and integrated—something never attempted to be reversed.

We’re not far removed from events that starkly revealed how deeply interconnected the world has become. The pandemic didn’t just cause damage—it revealed truths. It vividly showed how fragile the global trade architecture had become. Ships stopped, semiconductors vanished, and the illusion of robust supply chains shattered.

I don’t think we can simply… dismantle supply chains. Nor do I believe the U.S. can use tariffs to escape just-in-time, just-enough, barely-resilient systems built over decades. Trump’s trade policy isn’t Smoot-Hawley, despite many attempts to equate them.

I don’t think we can easily unravel supply chains. Nor do I believe the U.S. can use tariffs to escape decades-old systems designed to be instant, local, and almost entirely inflexible. No matter how many try to draw parallels, Trump’s trade policy is not Smoot-Hawley.

The most troubling aspect is the lack of historical precedent. You can reference the 1970s, 1930s, or any other event that reshaped systemic foundations—but none fully explain today’s situation.

In the 1930s, the world didn’t experience deglobalization because globalization was still minimal. Today, for the first time, we see a superpower deliberately jamming a stick into the spokes of its own globalized wheel.

The key point: it might work. Temporarily. Politically. Until it fails.

Just like Smoot-Hawley “worked” for about three months—until Canada retaliated, Europe raised tariffs again, and global trade fell into a trap. And record numbers of American farmers went bankrupt, yet still voted for those who drove down their crop prices.

Today’s tariffs differ in form but not in function. Both stem from the same belief: that destroying complexity brings stability. Unfortunately, complexity doesn’t yield easily.

To be honest: no one fully understands how this intricate, dynamic global system operates in real time. Not the Fed, not CEOs, not the IMF, and certainly not me or you. Its cascading effects are fundamentally incomprehensible. Yet, given our current trajectory, it seems our collective understanding will only deepen through the most unsettling means possible.

This leads to a straightforward question:

In a world where rules might change next quarter, how can a company commit to a 30-year, capital-intensive investment?

In an environment where tariffs aren’t policy but depend on the next tweet, the next election, the next wave of populism?

This isn’t just a trade issue—it’s a capital formation issue. Long-term investment exists only under rare combinations of conditions: predictability and trust in institutions are the most critical.

Though U.S. markets have shown extraordinary resilience through world wars, the Great Depression, stagflation, tech bubbles, and banking runs, this resilience wasn’t accidental. It rests on a rare and fragile combination of ingredients—most nations can’t assemble it, let alone sustain it for decades.

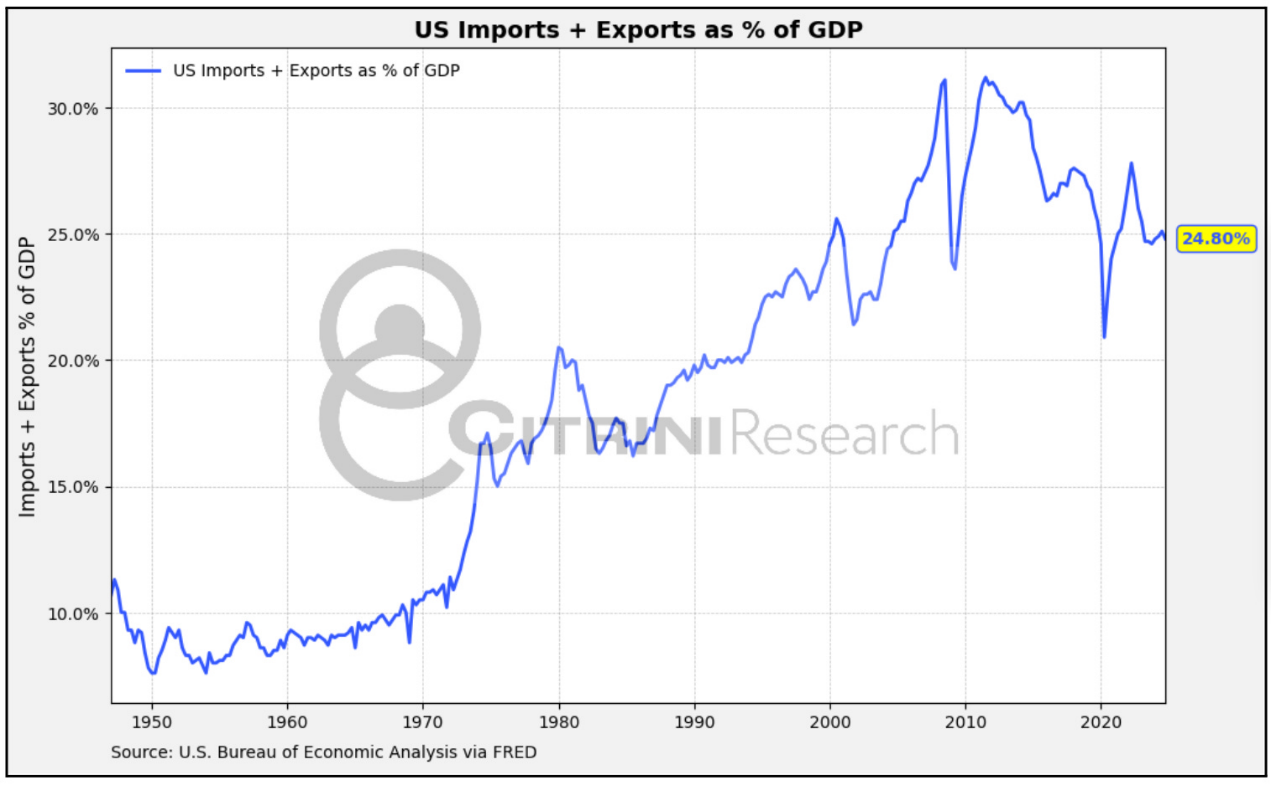

First, global trade. For nearly a century, the U.S. has been the central node in the world’s commercial network—not because it produces the cheapest goods, but because it offers the deepest markets, most trusted currency, and broadest consumer base. Trade has been the silent engine of American prosperity, enabling cheap imports, high-value service exports, and conversion of global surpluses into domestic assets.

Second, political stability. Whatever one thinks of partisan polarization and political absurdities, the peaceful transfer of power every four years, along with predictable contracts, courts

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News