BTC Reclaims 94,000, But Spring Won't Return for Early-Stage Investors

TechFlow Selected TechFlow Selected

BTC Reclaims 94,000, But Spring Won't Return for Early-Stage Investors

One group's spring is inevitably another group's winter.

By TechFlow

On April 23, market sentiment was reignited as Trump announced reduced tariffs on China.

Investor confidence in risk assets quickly rebounded. BTC quietly surged 7%, reclaiming $94,000.

Overnight, it felt like everything had come back.

BTC is now one step closer to surpassing its all-time high of $100,000 set at the beginning of the year. X (formerly Twitter) is flooded with optimism about a new bull run, and secondary-market traders are busy chasing momentum. The market seems to have returned to the frenzied spring of 2021.

Yet this resurgence of sentiment does not belong to everyone.

The noise belongs to them—while primary investors may remain silent in the face of signs of a bull return.

Bull Back, Dead from Lockups

The news of BTC reclaiming $94,000 brought cheers from secondary-market investors. But for those in the primary market, this rally feels like a distant illusion.

Their tokens are mostly locked up, unable to be freely traded, and last year’s market performance has already inflicted heavy losses.

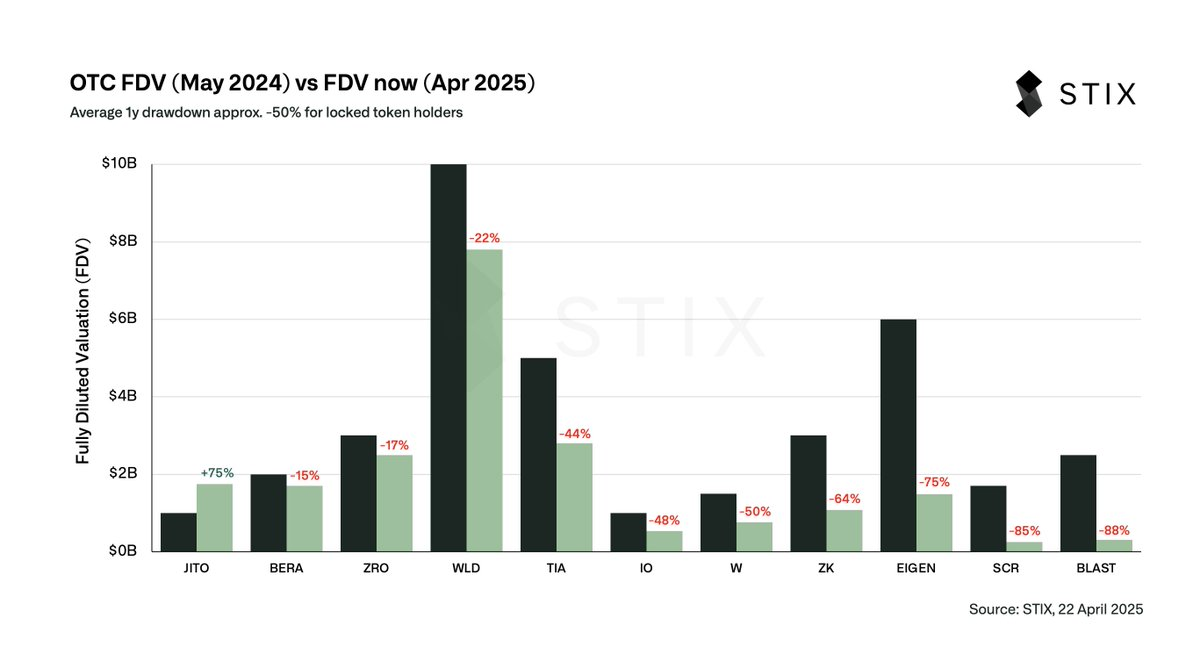

A chart from STIX (@stix_co) reveals this harsh reality.

@stix_co is a platform specializing in OTC (over-the-counter) crypto trading, providing liquidity for locked tokens.

The chart above compares valuations of several tokens in May 2024 and April 2025: May 2024 represents their OTC valuation (i.e., what primary investors could sell them for when locked), while April 2025 reflects their actual public market valuation today.

The result: on average, these tokens lost 50% of their value over the past year.

Let’s look at some specific examples.

BLAST was valued at $2.5 billion OTC last year; now its market cap is just $300 million—a drop of 88%. EIGEN fell from $6 billion to $1.5 billion, down 75%. SCR fared even worse, plummeting from $1.7 billion to $255 million, an 85% decline.

Almost all tokens suffered significant drops. JTO is the only exception, rising from $1 billion to $1.75 billion, up 75%.

But this is merely an outlier that cannot mask the overall bleak picture.

In short, if primary investors hadn’t sold their tokens via OTC last year, the average value of their holdings has since been halved—with some worth only 10–20% of their original value.

Here's some context: OTC trading allows primary investors to sell tokens privately before official unlock, usually at a discount.

As Taran noted in the original post, last year these tokens traded at around 80–90% of their valuation in OTC deals.

This means investors who sold then might have lost only 10–20%, or possibly nothing at all. Others chose to hold through the lockup period, only to see token values fall by an average of 50%, with some dropping 70–80%, resulting in massive wealth erosion.

You might argue: their initial cost basis was low, so even after such declines, they’re still profitable.

But economics introduces the concept of opportunity cost. For an investor, what hurts more than underperforming—or possibly losing—is the theoretical loss of opportunity.

In theory, over the past 12 months, Bitcoin (BTC) rose 45%.

If primary investors had sold their tokens last year and bought BTC instead, their capital would now be worth 1.45 times its original value.

Instead, their token holdings are now worth just 0.5 times—and may need to be discounted further upon unlocking, potentially ending up at just 0.25 times.

In other words, compared to BTC’s gains, their relative loss reaches 82.8%; even in absolute dollar terms, they’ve lost 75%.

It’s like watching others make huge profits while your own assets shrink day by day.

For them, the “bull return” may have already died due to lockups.

The most frustrating part? After a year of lockup and a 50% loss:

All the effort spent researching, comparing, identifying, and investing in projects wasn’t even as rewarding as simply holding BTC.

In the classic investment book *A Random Walk Down Wall Street*, there’s a famous “monkey throwing darts” theory.

Author Burton Malkiel suggests that if a monkey were to blindly throw darts at stock listings to pick a portfolio, its long-term returns might not differ much from those of professional investors.

This idea originally mocked the futility of over-analysis in stock markets—but today, in the crypto space, it feels painfully ironic.

Primary investors spend immense time and energy studying whitepapers, analyzing project prospects, and committing to year-long lockups in pursuit of high returns—only to find out they’d have been better off letting a monkey throw a dart at Bitcoin.

BTC gained 45% over the past year, while their locked tokens lost 50%—or more.

The entire valuation and investment logic behind altcoins may urgently need rethinking.

Spring Won't Return

Will the next wave of crypto altcoins follow the same lockup model?

VCs enter at low prices, and lockup mechanisms were originally designed to protect early-stage projects from price crashes caused by mass dumping from early investors. Yet, as last year’s data shows, these mechanisms have also exposed primary investors to enormous risks.

The original post accompanying the chart notes that over $40 billion worth of locked tokens will gradually unlock in the future, indicating potential downward pressure on the market. If new tokens continue launching with high valuations and long lockups, investors could again fall into the vicious cycle of “lock up for a year, lose half.”

Clearly, the lockup model no longer fits the current market environment.

Will primary market investing remain vibrant? Can the spring of primary investing return? Judging from current trends, the answer may not be optimistic.

In recent years, high valuations for altcoins were often built on market frenzy and liquidity premiums. But as the market matures, investors increasingly prioritize real project value and liquidity.

The high risk of locked tokens makes primary investors hesitant. More and more may turn toward projects that offer greater transparency and liquidity.

Emerging trends are already visible: shorter lockup periods, lower valuation multiples, or even launching Meme coins directly to reduce primary investment bubbles.

Of course, it’s also possible that old games are repackaged in new forms—under the fairer appearance of Meme coins, the same primary investment logic persists, with orchestrated groups creating markets that hide the existence of primary rounds.

For the broader crypto market, more transparent mechanisms are becoming crucial. Lockup structures must find a better balance—protecting early project development without exposing investors to excessive risk.

But here’s the question: if primary investors don’t lose, secondary investors don’t lose, and retail doesn’t lose—who bears the loss?

Crypto tokens don’t create value—they redistribute it. For someone to profit, someone else must lose.

One group’s spring is inevitably another group’s winter.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News