Interview with Tom Lee and “The Big Short” Author: Buying Gold Is a Bet on “Global Anxiety”; the Crypto Bear Market Is a Cleanup and Reorganization Before Institutional Takeover

TechFlow Selected TechFlow Selected

Interview with Tom Lee and “The Big Short” Author: Buying Gold Is a Bet on “Global Anxiety”; the Crypto Bear Market Is a Cleanup and Reorganization Before Institutional Takeover

A true bubble emerges precisely when everyone believes, “This is definitely not a bubble.”

Compiled & Translated by TechFlow

Guests: Tom Lee, Co-Founder and Head of Research at Fundstrat; Michael Lewis, author of *Moneyball*, *The Big Short*, *The Blind Side*, and *Going Infinite*

Moderator: Liz Thomas, Head of Investment Strategy at SoFi

Podcast Source: SoFi

Original Title: AI Boom or Bubble? Michael Lewis and Tom Lee on the Risks and Rewards | The Important Part LIVE

Air Date: February 19, 2026

Key Takeaways

In a special live recording of *The Important Part*, SoFi’s Head of Investment Strategy, Liz Thomas, posed a question preoccupying many investors: Will the market’s rapid ascent slow—or will it continue? To answer this, she invited two leading financial thinkers: Tom Lee, Co-Founder and Head of Research at Fundstrat, and Michael Lewis, bestselling author of *Moneyball*, *The Big Short*, *The Blind Side*, and *Going Infinite*. Together, they explored core investment questions facing markets in 2026.

In this captivating conversation, they dissected several hot topics: Why have retail investors outperformed hedge funds in recent years? Has gold peaked? Does Bitcoin’s 40% plunge signal the onset of a “crypto winter”? Tom Lee explained that although AI-driven software stocks recently declined, this may actually reflect rising corporate productivity. Meanwhile, Michael Lewis shared his contrarian bet on gold—and why he “buys fear” as an investment strategy.

They also examined other major themes in today’s financial markets: Will Kevin Warsh’s nomination as Federal Reserve Chair threaten the Fed’s independence? Could the rapid advancement of AI lead to massive job losses? And might the federal government step in to take over distressed AI firms?

Finally, they turned their attention to cryptocurrency, analyzing potential “black swan” events—and valuable lessons about technological disruption drawn from the history of the frozen food industry.

Highlights of Key Insights

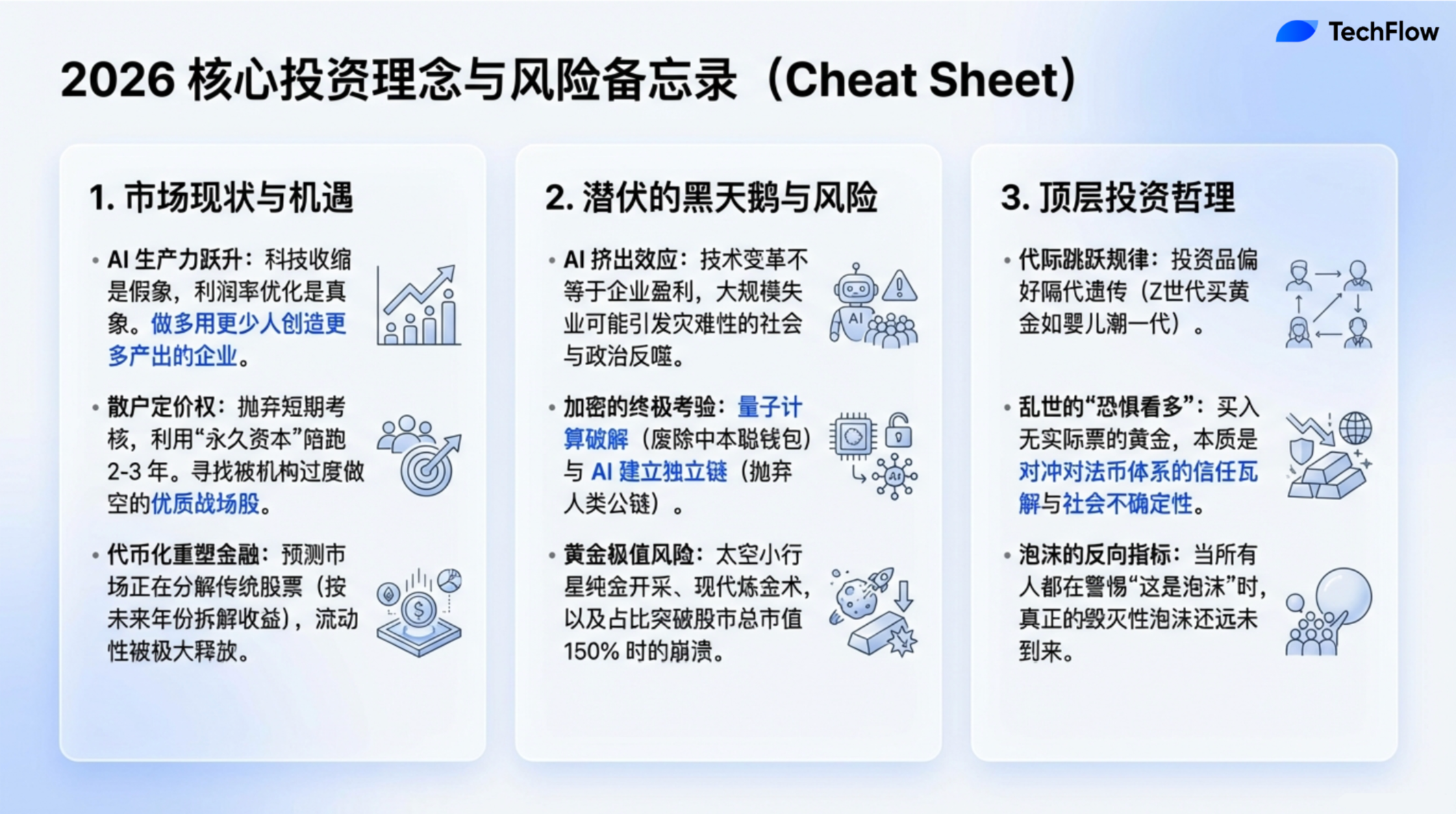

- A true bubble emerges precisely when everyone is convinced “this absolutely isn’t a bubble.”

- The unemployment rate among college graduates even exceeds that of their non-college-educated peers… but viewed differently, this may actually signal rising economic productivity—since productivity is typically measured by generating more output with fewer inputs.

- AI may indeed be as revolutionary as widely claimed—but that doesn’t guarantee broad-based equity market gains. There’s no necessary causal link between technological transformation and market returns.

- Retail investors pick winning stocks largely because their incentive structures differ fundamentally from those of institutional investors… They invest their own capital, making them far more willing to hold a stock for two to three years.

- When I hold gold, I’m investing in “fear.” I buy gold because it hedges against current uncertainty… It’s insurance against future anxiety and unease.

- Historically, gold has surged more than 9% in a single day only three times—and each time marked a peak in gold prices. If history is any guide, gold may already have topped out.

- A well-known Wall Street adage from the late Art Cashion: “Bull markets don’t die of old age—they’re killed by the Fed.”

- Although operational methods have changed, human nature hasn’t. That primal instinct—“I want to earn more, faster, than others”—remains the core engine driving this industry.

- Over the next decade, whoever controls AI—and its associated ecosystem—may become the world’s dominant superpower. If AI funding truly starts to dry up, I believe even the Department of Defense is already simulating contingency plans.

- Since 1974, roughly 40,000 companies have gone public or spun off. Of these, 90% saw their stock prices fall more than 50%; and of those, 90% ultimately went to zero. In other words, most stocks eventually become worthless.

AI: Crisis or Opportunity? The Dual Nature of Productivity Transformation

Liz Young:

Global markets have experienced sustained growth in recent years. Though volatility has emerged over the past few weeks, the overall trend remains strong—largely propelled by artificial intelligence (AI). AI has driven innovation, spawned new products, and attracted massive capital inflows. Yet many investors are growing uneasy, questioning whether markets have overheated or advanced too rapidly. This concern is spreading globally—and lies at the heart of our discussion today.

To better understand this phenomenon, we’ve invited Tom Lee, Co-Founder and Head of Research at Fundstrat. He’s long been bullish on markets and is widely regarded as a leading “bullish” voice. Tom, why do you remain optimistic amid current conditions?

Tom Lee:

There’s a famous Wall Street saying by the late Art Cashion: “Bull markets don’t die of old age—they’re killed by the Fed.” In other words, strong stock market performance doesn’t mean it can’t continue. In fact, I see two powerful catalysts emerging: First, AI’s returns are beginning to materialize—reshaping winners and losers. Second, the Fed’s policy pivot could provide fresh tailwinds for markets. So there remain compelling reasons for investors to stay long equities this year.

Liz Young:

Let’s talk about recent market shifts: sharp declines in software stocks and a notable pullback across crypto. Does such turbulence worry you—and does it shake your bullish outlook?

Tom Lee:

I think many are watching closely. Over the past two years, AI has surged like an unstoppable force, drawing intense investor attention and capital. Yet—as you noted—things feel different this year. We’re seeing contraction across numerous stocks and sectors. Software, for example, now faces falling demand and service repricing. Moreover, research reports suggest Agentic AI and other AI technologies are gradually displacing traditional software solutions.

Additionally, reports indicate tech-sector employment has declined since ChatGPT’s launch three years ago. More surprisingly, the unemployment rate among college graduates now exceeds that of their non-college-educated peers. These figures appear as “bad news”—and dominate headlines today. But viewed differently, this may actually signal rising economic productivity, typically measured by generating more output with fewer labor inputs.

From this angle, AI adoption is revealing its productivity-enhancing potential. For software firms serving enterprises, reduced enterprise software spending reflects margin optimization. In short, AI-driven efficiency gains are increasingly translating into real earnings. While these shifts may cause short-term pain, they powerfully affirm AI’s productivity advantages over the longer term.

Early Warning Signs of Market Overheating—and Collapse Risks

Liz Young: Michael, your prior works chronicle periods where markets surged relentlessly before suddenly collapsing—each preceded by signals like excessive speculation or risk-taking. Across the market collapses you’ve studied, what common traits mark such reckless behavior—and do you see them present in today’s markets?

Michael Lewis:

That’s a fascinating question. Frankly, I’ve never accurately predicted a market collapse before it happened. My work is more like arriving after the storm has subsided—to sort through the wreckage. Reflecting on my career, my first book, *Liar’s Poker*, documented Wall Street in the 1980s; later, I chronicled the dot-com bubble and the 2008 financial crisis. But honestly, I never knew exactly when those events would unfold—and I don’t believe anyone truly can. More importantly, markets always allow multiple interpretations—and my personal investment strategy is simply to allocate capital to index funds.

Still, I’ve observed that after every market collapse, someone always claims to have seen it coming—but intriguingly, those same people rarely predict the next crisis correctly. For instance, Michael Burry rightly called the subprime crisis—but that doesn’t guarantee all his future forecasts will be right. He recently tweeted that he’s shorted Nvidia and Palantir, sparking widespread market attention. I interviewed him; his logic rests on the capital expenditure cycle—arguing these firms’ valuations have reached bubble-like extremes. Yet he candidly admits he can’t pinpoint the timing of a collapse. So he adopts a conservative approach: purchasing two-year put options. Puts are low-cost; even if wrong, losses remain limited. This shows—even visionary figures like Burry cannot fully grasp short-term market dynamics.

Regarding the traits of reckless behavior you mentioned, I’d highlight FOMO above all. Take my recent book *Going Infinite*, about Sam Bankman-Fried and FTX: FTX’s collapse was a textbook case of FOMO. One hundred eighty venture capital firms invested in SBF without proper due diligence—some didn’t even understand his business model before committing huge sums. This “act first, understand later” mindset is a hallmark of excessive risk-taking.

Another common trait is distorted incentives. When writing *The Big Short*, I interviewed traders who made disastrous subprime bets. They told me they joined high-risk trades because “everyone else was doing it”—and opting out meant being labeled laggards. Plus, they were lured by outsized bonuses—unrecoverable even if investments failed. Such flawed incentives drove people to chase short-term gains despite knowing the risks.

If I dare forecast, I believe today’s markets show some bubble-like signs. While AI is undeniably transformative, that doesn’t mean everyone profits. In fact, technological progress can sometimes compress corporate margins. AI may indeed be revolutionary—but that doesn’t guarantee broad equity-market gains. Technological transformation and market returns lack a necessary causal link.

Why Retail Investors Are Outperforming Institutions

Liz Young: Tom, I know you have unique insights on this. Could you discuss internet slang like FOMO and HODL—which reflect the retail-institutional tug-of-war?

In this economic cycle—since COVID—we’ve seen retail investors repeatedly anticipate market direction correctly, while institutions sometimes appear overly cautious. How do retail investors achieve this—and why are their judgments more accurate? Who holds the edge now—retail or institutions?

Tom Lee:

At Fundstrat, our clients fall into two main categories. One group comprises institutional research clients—including roughly 400 hedge funds. The other includes family offices, financial advisors, and high-net-worth individuals served via FS Insight. Each month, we survey these clients to identify their top five most-bullish and most-bearish stocks. We’ve conducted this analysis since 2019—with striking results: retail investors consistently choose correctly—their top five holdings perform exceptionally well. We’re even considering packaging this data into an investment product.

I believe retail investors succeed primarily because their incentive structures differ radically from institutions’. Their livelihoods aren’t tied to daily or weekly P&L swings. They invest their own capital—what we call “permanent capital”—so they’re comfortable holding stocks for two to three years.

When I started, institutional holding periods were typically one year—that counted as “long-term.” Today, most institutions hold positions for just 30 days or less. Data shows the average stock holding period is around 40 seconds; some hedge funds consider 1–5 seconds “long-term.” This high-frequency trading model forces institutions to focus solely on highly liquid, quickly rewarding stocks—while retail investors pursue long-growth opportunities.

Liz Young: But won’t this fuel more FOMO? If retail picks are right, won’t institutions chase them—overheating markets further?

Tom Lee:

Yes—this happens. Markets often feature “battlefield stocks”: popular with retail yet heavily shorted by institutions. Palantir is a prime example; so was Netflix in the mid-2000s, trading at $2–$4 before surging to $20. Back then, many institutions shorted Netflix aggressively—while retail bought steadily. Another famous case is GameStop. Stocks like Palantir and Tesla became classic battlefield names—retail betting on long-term potential, institutions treating them as short-term arbitrage tools. Once prices hit critical thresholds, revaluation triggers rapid rallies. For instance, Tesla’s inclusion in the Russell 1000 Index in 2017 sparked just such a surge.

Michael Lewis: May I ask a question? You mentioned developing a product based on retail stock picks?

Tom Lee:

We’ve collected 60 months of data—tracking retail investors’ top and bottom picks—and especially “battlefield stocks” favored by retail but shorted by institutions. We plan to launch an ETF that automatically buys the stocks retail investors deem most promising each month. Think of it as a professionally vetted WallStreetBets. Unlike random Reddit chatter, our data comes from paying customers—real clients expressing actual investment views. Crucially, our data undergoes strict screening and verification—no bots or fake accounts—only genuine investors.

Gold’s Surge—and the Underlying Crisis of Trust

Liz Young: How do institutional and retail investors differ in their approach to gold—and how do you view the future of gold and silver? Though I hesitate to call them “meme stocks,” they’ve clearly become speculative assets.

I’ve long believed gold trading is dominated by institutions and central banks—but surprisingly, gold has shined brightly in recent years, even outperforming the S&P 500 for several consecutive years. Years ago, I strongly recommended gold—yet many dismissed me as “a grandma clutching gold bars.” Later, gold surged dramatically—drawing massive retail inflows.

I recall taping a show at the NYSE once, coinciding with GLD’s (gold ETF) bell-ringing ceremony. Outside, giant fake gold bricks lined the street, draped in golden banners. At that moment, I thought: “Retail is flooding in.”

Tom Lee:

Gold’s performance has indeed been stellar. Reviewing 25 years of market cycles, gold’s returns have surpassed the S&P 500. This may tie to demographic shifts. At Fundstrat, we study population trends—and find consumption preferences often skip generations. RV sales illustrate this perfectly: they peak roughly every 50 years. During COVID, RV sales hit record highs.

This “skip-generation effect” stems from children disliking their parents’ passions—but finding grandparents’ interests deeply cool. Example: If your father rode motorcycles, you might not find it cool—but seeing vintage Harley photos of your grandfather might make it iconic. Gold resonated with Baby Boomers; Gen X favored hedge funds. Now, Millennials and Gen Z are rediscovering gold—a generational trade. Gold’s market value stands at ~$35 trillion, while the S&P 500 (excluding the Magnificent Seven) totals ~$40 trillion. Gold’s scale now rivals equities.

Michael Lewis: Do you mean $35 trillion represents all existing gold above ground?

Tom Lee:

Yes—above-ground gold. Roughly 7 billion ounces exist, valued at ~$5,000 per ounce—totaling ~$35 trillion.

On gold, key points stand out. As a researcher, I’ve long studied gold—and appreciate its unique properties. Gold exhibits the Lindy Effect: the longer something exists, the more people believe its value will persist.

Gold has served as a store of value for centuries—its longevity ensures enduring acceptance. Its role as a medium of exchange stems from scarcity. Yet, in my view, gold still faces potential “black swan risks.”

First, above-ground reserves are finite—but underground deposits dwarf them by millions of times. If gold prices soar high enough, mining may attract mass participation. At extreme prices, digging for gold could eclipse all other industries in profitability.

Second, gold’s origin is literally “extraterrestrial.” Imagine SpaceX exploring Mars—and discovering a gold-rich asteroid. If Elon Musk mines it, he could monopolize global gold supplies—or become a de facto central bank. Such asteroids might contain tens of billions of ounces—shocking global gold markets.

Third, alchemy risks. If someone discovers how to transmute lead into gold by altering atomic structure, they might quietly produce gold—never disclosing the method. A sudden flood of supply could crater gold’s value.

So gold remains an excellent investment—but with limits. At $9,000/ounce, its market cap could surpass equities’ total value.

Liz Young: Is there a price point where gold loses investment appeal?

Tom Lee:

We’ve studied this deeply—comparing gold and equity market caps over 100 years. Our research shows gold’s market cap can reach 150% of equities’—but that’s likely its ceiling. For example, on January 30, gold plunged 9% in one day—demonstrating extreme volatility. Historically, gold rose >9% intraday only three times—and each marked a peak. If history repeats, gold may have topped out.

Liz Young: Michael, you previously mentioned investing mainly in ETFs and passive index funds—like Vanguard’s. But you occasionally try other investments, right?

Michael Lewis:

Yes—I sometimes lose my mind. On gold, let me share a story. As a boy, I played poker weekly with friends—including Bobby Klein, a natural poker genius and one of my closest friends. During the financial crisis, he ran a Wall Street fund that shorted subprime mortgages. He was part of *The Big Short* story—profiting massively from the crash—and later founded his own asset management firm.

Four years ago, I visited him. He showed me his collection of ancient Roman coins—and explained how emperors secretly debased currency by reducing silver content in coins. He used this history to justify buying gold. His argument was persuasive—but I wasn’t fully convinced. I felt buying gold sounded downright crazy.

Yet his words lingered. Three years ago, I finally bought gold—substantially—and its price has risen ever since. A month ago, I called Bobby to tell him I’d followed his advice—and profited handsomely. Bobby knows gold markets far better than I do—and focuses on gold-mining stocks, a more cost-effective way to gain exposure. He acknowledges gold’s “black swan risks”—but considers them far lower than Bitcoin’s.

What fascinated me most: When Bitcoin launched, people dubbed it “digital gold.” But I noticed Bitcoin’s price began tracking equities—not gold’s independent path. This made me realize Bitcoin has ceased being digital gold—and may now represent another asset class entirely.

Gold is magical—but its value rests purely on human consensus. We value gold only because we collectively believe it valuable. When I hold gold, I’m investing in “fear.” I buy gold to hedge against uncertainty—global political turmoil, economic crises, or even financial collapse. In short, I’m buying insurance against future anxiety.

Today’s political and economic instability remains acute—and I believe this fear won’t vanish soon. So even if gold falls 60%, I’d still consider it a successful trade. But I must stress: This isn’t a recommended strategy. I bought gold impulsively—and got lucky. Usually, it’s not rational.

Societal Shocks—and Technological Transformation—Driven by the AI Wave

Liz Young: Tom, you’ve compared today’s AI development to telecom in the late 1990s/early 2000s—and suggested we’re still in AI’s early stages. If true, how does this differ from that era?

For instance, today’s capital expenditures (CapEx) dwarf 1990s levels—now a larger GDP share. Crucially, this spending has already begun—whereas in the 1990s, it hadn’t yet accelerated. Are we overspending on CapEx?

Tom Lee:

I agree with Michael: AI will ultimately become a bubble. Yet ironically, when people start calling something a bubble, it usually isn’t yet—a true bubble emerges only when everyone is certain “this absolutely isn’t a bubble.” I was a tech analyst in the 1990s—witnessing telecom’s overexpansion firsthand. Companies like Global Crossing and Quest laid fiber-optic networks wildly. I worked at Solomon Brothers then; Jack Rubman was a key fundraiser.

Then, every company and analyst tweaked models to justify absurd valuations. Funding costs neared zero—exit multiples soared to 20x–30x. Ultimately, when the bubble burst, entire ecosystems collapsed—wireless and beyond—no one escaped.

Yet post-bubble, the best opportunities emerge from rubble. After that crash, cell-tower companies became top performers—returning 10x the S&P 500. Another unexpected winner? Pizza chains—like Domino’s Pizza. Bankers ordering pizza at midnight turned out to be better investments than telecom infrastructure. Those towers—metal structures hanging wireless gear—became optimal investments.

Michael:

You’re right: When everyone declares “this isn’t a bubble,” it truly is. But now everyone debates whether AI is a bubble—making me think it’s not yet. We’re already approaching it cautiously.

Liz Young: Many say “this time is different”—but I’ve long believed economic and business cycles never change fundamentally. Drivers may shift—but outcomes remain similar. Has any cycle truly differed—or does your experience reinforce history’s repetition?

Michael:

Perhaps—but each cycle seems increasingly extreme. We obsess over financial consequences—ignoring broader societal ones. For example, AI’s impact may dwarf financial markets. I’ve spoken with tech experts—some believe AI could cause human extinction. If so, what does stock performance matter? If we’re gone, portfolios are meaningless.

Naturally, I’m skeptical of such extremes. Yet AI’s societal shocks—massive job losses—are undeniable. Intriguingly, Google and OpenAI executives say both: “We must tread carefully—AI could destroy humanity.” And: “In 18 months, AI will outperform humans at everything.” Contradictory, indeed.

Setting aside extinction for now: What if, in 18 months, AI does everything humans do better? How would this nation look? Anger over the economy is already rampant—if AI accelerates this, outrage will spike further—making stock moves seem trivial.

I doubt AI replaces all jobs in 18 months. Personally, I feel no threat. I tried using AI to write a book about Sam Bankman-Fried—or similar topics—but it only scrapes existing web content, failing to grasp human thought. It won’t conduct interviews or reconstruct narrative details and emotions—producing unusable text.

May I share a brief anecdote? While writing *Going Infinite* (about Sam Bankman-Fried), I learned he’d interacted with Sam Altman. So I visited Sam Altman to hear his views. We dined at his home—he’s fascinating, great company. But I sensed subtle intentions: He told me many wanted to write his biography—but he preferred selecting one person, to deter others.

I asked, “Given your AI’s brilliance, why not let it write your biography? Feed it chat logs and documents—it’ll draft it.” He replied, “It’s not smart enough—output would be terrible.” I asked, “When will it write well?” He said, “Maybe in a few years.”

So we struck a deal: When AI is smart enough to write a good book, I’ll challenge it. I’ll write one—and AI will write one—and we’ll compare. Honestly, I still don’t feel AI threatens all jobs.

Liz Young: Every new technology sparks fears of job destruction—but historically, tech creates more jobs than it destroys. Will this time differ?

Tom Lee:

History reveals two distinct tech disruptions with opposite employment impacts. First: 1930s frozen-food technology. Then, 30% of U.S. workers were in agriculture. Frozen tech slashed food spoilage—cutting household food spending from 20% to 5% of income—and agricultural employment fell from 30% to 5%. Though 95% of farmers lost jobs, freed resources fueled economic prosperity.

But the second case reversed this. China’s manufacturing dominance devastated many U.S. states—mass unemployment ensued, with policymakers failing to create replacement jobs.

Wall Street’s Evolution—and the Rise of the Quant Era

Liz Young: Michael, comparing your career start to today—what Wall Street changes surprised you—or remained unchanged? Your daughter works on Wall Street now, right? Has she read *Liar’s Poker*?

Michael:

No. She refuses to read any of my books. Once, her boss—a senior partner—slammed the book on her desk: “If you want to understand this industry’s essence, you must read this.” She told me at home. I asked, “Did you?” She said, “No—I use it as a coaster.”

But seriously, observing her work revealed Wall Street’s extreme quantification and automation. In my day, traders yelled in pits—relying on guts and relationships. Today, everyone stares at algorithms. Though methods changed, human nature hasn’t. That primal urge—“I want to earn more, faster, than others”—still drives the industry. Whether yelling or running AI algorithms, greed remains constant.

Recall when people paid vast sums for my financial advice—Wall Street’s craziest era. I’m amazed stories I lived still resonate. Markets transformed drastically—not just because my old job vanished, but bonds automated too. Trading now relies on robots—not human interaction—trading floors lost their noise and energy—interpersonal dynamics disappeared.

Why do my stories still captivate? One reason: this world remains youth-dominated. Like when I entered—or you did—young people ruled. Princeton, Harvard, or Yale grads earned six-figure salaries within years—radically reshaping elite schools’ ties to finance.

In my father’s generation, average students went to Wall Street—designed for socializers, not geniuses. Smart people pursued other fields—and finance paid little.

Later, finance’s explosive growth and profits drew elite students. Suddenly, half of Ivy League grads aimed for finance—a trend continuing today, though focus shifted to high-frequency trading firms and private equity.

Another striking impact: how this affects lives. Finance rewards youth heavily—so students plan careers early. Today’s undergrads prep for Wall Street in freshman year—a trend just starting when I graduated, now intensified.

Liz Young: Has this ended—or merely shifted? Tom, you noted college grads’ unemployment exceeds non-grads’. Does this mean elites now prefer tech over Wall Street?

Tom Lee:

My kids graduated recently. My daughter initially pursued art history—but met peers aiming for Wall Street, so she joined a business fraternity to enter that circle.

I think Wall Street still attracts a specific type—typically fiercely competitive, seeking to work alongside the best. Perhaps that culture endures because of this. Competition is fiercer now. Today’s high schoolers need business activities to enter Wharton—whereas in my day, showing interest sufficed.

Michael:

Competition among the bright persists—but choices multiplied. At Jane Street, 25-year-olds earn millions. Today’s extremes dwarf my era. Fresh out of college, I knew nothing about finance—yet someone paid me generously. No wonder everyone queued for entry—even ignorance earned paychecks. Now, many bright minds choose Silicon Valley—but much of its capital originates in finance—e.g., venture capital.

Your “change vs. continuity” point reminds me of quant analysts’ rise. When I started, quants were rare—gradually becoming core at firms like Solomon Brothers—but never fully dominant. Now, quants rule everything.

Yet I assumed finance’s GDP share would shrink—but the opposite occurred: finance grew larger. Consider internet-driven tech disruption—supposedly eliminating intermediaries (e.g., travel agents)—yet strangely, this disintermediation didn’t similarly affect Wall Street.

Tom Lee:

Technically, finance mirrors the real economy—every unit of real output needs a corresponding financial unit—and digitization blurs this line. Over 20 years, 50% of GDP growth came from the digital economy—meaning boundaries between money, services, and digital assets are vanishing.

Future definitions of money may blur further—distinctions between rewards, value creation, and monetary units fading. Thus, finance’s GDP share may keep growing—and quant roles gaining importance—providing market liquidity by exchanging assets (dollars, bonds, digital assets). This trend may let Wall Street profit more—and transform firms like JPMorgan into tech-like entities—not just lenders, but market-service providers.

The Fed and the AI Era: Policy Shifts—and Geopolitical Competition

Liz Young: The Fed remains headline news—especially with Kevin Warsh’s nomination as Chair. Tom, assuming he’s confirmed, would this alter the Fed’s intervention policies? I’m not asking about independence—but given his opposition to QE, could this shift intervention approaches?

Tom Lee:

Excellent question. Though not a Fed expert, I’ve researched Kevin Warsh. He’s publicly stated the Fed’s ability to aid the economy is limited. Many think the Fed can “save” economies—but it really only adjusts rates or influences market rates via communication.

If the White House seeks to limit the Fed’s role, Warsh fits perfectly. Treasury and fiscal policy could then wield greater influence—e.g., controlling rates, narrowing mortgage-policy rate gaps, or direct intervention. Yet markets reacted poorly to his nomination—showing little enthusiasm.

Liz Young: Perhaps the bigger question: If the Fed’s market role weakens—say, Warsh reduces intervention—do we possess stronger crisis-response tools than in 2008?

Michael:

You said “not discussing independence”—but that’s the crux. Trump clearly dislikes Fed independence. He yielded only under market pressure—if markets hadn’t collapsed during his attempts, he’d have seized control.

Back in 2008, Fed intervention’s stabilizing role for finance and the economy is undeniable. Those decisions were extreme—but policymakers had studied the 1929 Great Depression, learning from the Fed’s prior mistakes. I believe Fed intervention was essential.

If a similar crisis hit under Trump, I can’t imagine him telling the Fed, “Do nothing—don’t intervene.” Impossible.

Liz Young: Suppose an AI-triggered crisis—e.g., a key AI firm collapses or funding dries up—would the Fed bail out AI firms?

Michael:

Trump never hesitates to deploy government resources for optics—I can’t envision the Fed becoming wholly non-interventionist. That’s not his style.

Tom Lee:

I agree. Facing economic collapse, the Fed will deploy every tool to stabilize. Even a laissez-faire Fed would concur.

If AI firms begin failing, I believe they’ll be nationalized. This transcends normal competition—it’s U.S.-China geopolitical

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News