How to Achieve "Perpetual Earnings" with Perpetual Contract Arbitrage, Regardless of Bull or Bear Markets?

TechFlow Selected TechFlow Selected

How to Achieve "Perpetual Earnings" with Perpetual Contract Arbitrage, Regardless of Bull or Bear Markets?

A Practical Guide to Perpetual Contract Funding Rate Arbitrage

Author: HangukQuant

Translation: Luffy, Foresight News

About a year ago, we first came up with the idea of exploiting funding rate arbitrage using perpetual contracts. Since then, we’ve published multiple articles exploring this trading strategy and related derivative topics—one of which discussed the value proposition and sources of returns for this strategy. We've also developed a fully systematic perpetual arbitrage bot, turning theory into practice.

Today, we'd like to discuss some implementation details and extensions of this trading strategy.

Stacking Expected Value

Let’s assume you understand funding rate differentials and how to profit from positive funding rates. If not, please refer to our earlier articles. The following discussion applies to both systematic and manual trading.

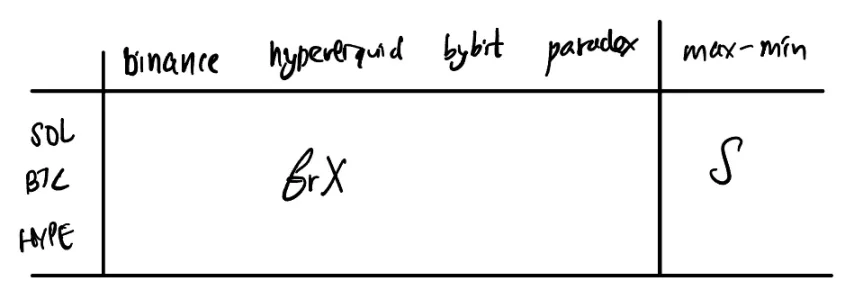

We start with a table. The leftmost column lists assets, and the rows represent n exchanges. We denote fr’X’ as the standardized funding rate, adjusted for differing time intervals. Our focus is on combinations with large discrepancies (difference between maximum and minimum), where we go long at the exchange with the lowest rate and short at the one with the highest.

Here are some important extensions. Typically, an exchange may offer different quote assets—such as USD stablecoins USDC, USDT, USDE, etc. If you choose to arbitrage pairs that aren't quoted in the same asset, you're effectively engaging in implicit triangular arbitrage. This is usually beneficial. For example, consider comparing prices across:

BTC/USDT, BTC/USDC, USDC/USDT

You might discover valuation misalignments. While these discrepancies are typically too small to exploit within a single platform, stacking them onto cross-exchange arbitrage can boost overall returns. In such cases, you’ll need a price oracle to assist with valuation conversion—for instance, needing USDC/USDT pricing on Binance or USDC/USD on Paradex.

The point is, you can stack funding arbitrage, triangular arbitrage, and price arbitrage within a single trade. However, for manual traders, it's best to stick with pairs using the same quote asset, since humans struggle with high-dimensional decision-making.

By the way, while you can layer multiple independent funding-related strategies, the funding rate itself is often a key feature of perpetual market-making operations (and interacts with other factors).

Break-Even Analysis

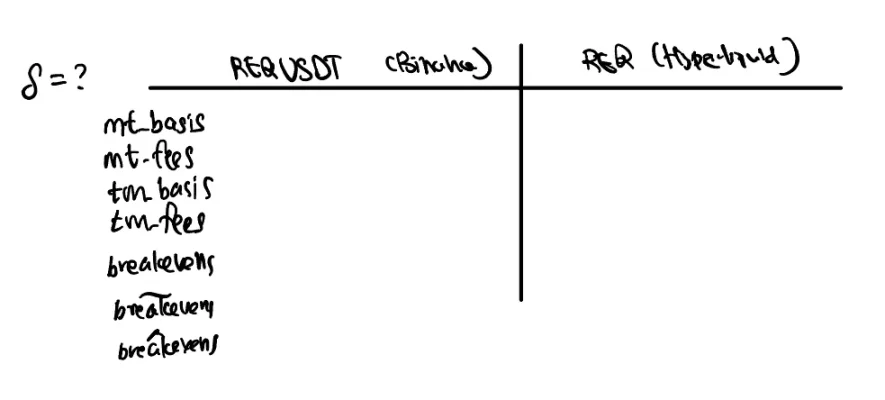

From these combination options, you should now have candidate pairs for arbitrage. Let's say we're interested in going long REQ/USDT on Binance and long REQ on Hyperliquid.

You'll need a fee schedule—fees vary by individual (VIP level) and exchange. Funding rate differentials generate positive cash flow, but actual trades are still required to establish positions.

Due to exchange incentive structures, the sum of maker and taker fees is often asymmetric. This creates a bias influencing where you place orders. Additionally, order book liquidity is asymmetric. Depending on execution venue, you may achieve better base pricing. The combined effect determines your entry cost.

Generally, you’re compensated for providing liquidity, so you might prefer placing limit orders in less liquid venues and taking liquidity in more liquid ones.

Break-even refers to the time duration or number of funding intervals needed to cover entry costs (some exchanges settle funding every 8 hours).

This is a crucial metric. Since funding profits are realized over time, various estimation methods are useful. I use "~" to denote break-even estimated from historical data, and "^" for regression model predictions.

So far, we’ve identified target pairs and where to submit quotes. Now, how do we execute?

Trade Execution

If you're using systematic trading, computational power allows frequent real-time calculation of core metrics. When liquidity anomalies occur, you might even capture pure price arbitrage opportunities. Most of the time, however, your targets are structural arbitrage opportunities lasting at least several minutes. Your task is ensuring the arbitrage condition holds during the seconds to minutes it takes to establish positions.

The core concept is Stacked Expected Value (EV)—this is our source of P&L. Profit equals expected gains minus costs, and break-even analysis simplifies complexity, especially relevant for manual trading.

These are nuanced details, but iterative refinement leads to more robust strategies. Similar principles apply regardless of automation. Ideally, if you have a target position size and can activate a market-making engine to accumulate it, everything is in place. More commonly, we rely on a mix of maker and taker orders. With automation, dynamic selection of maker roles is possible; otherwise, heuristic rules work well.

We need to define:

-

Target position size

-

Maximum order size

-

Minimum order size

-

Dynamic order sizing rules

Each has associated considerations. Target position size depends on risk appetite, funding costs, and available capital.

Maximum order size is constrained by taker-side liquidity. After a maker order fills, the offsetting taker trade incurs (linear or quadratic) price impact. Capping order size reduces slippage.

Minimum order size relates to target size—it sets a lower bound on aggressiveness when accumulating.

Between max and min lies dynamic sizing. With smaller capital, you could choose sizes minimizing market impact (e.g., only pulling liquidity from best bid/ask on taker side). A common rule of thumb for manual trading is dividing the total order into chunks.

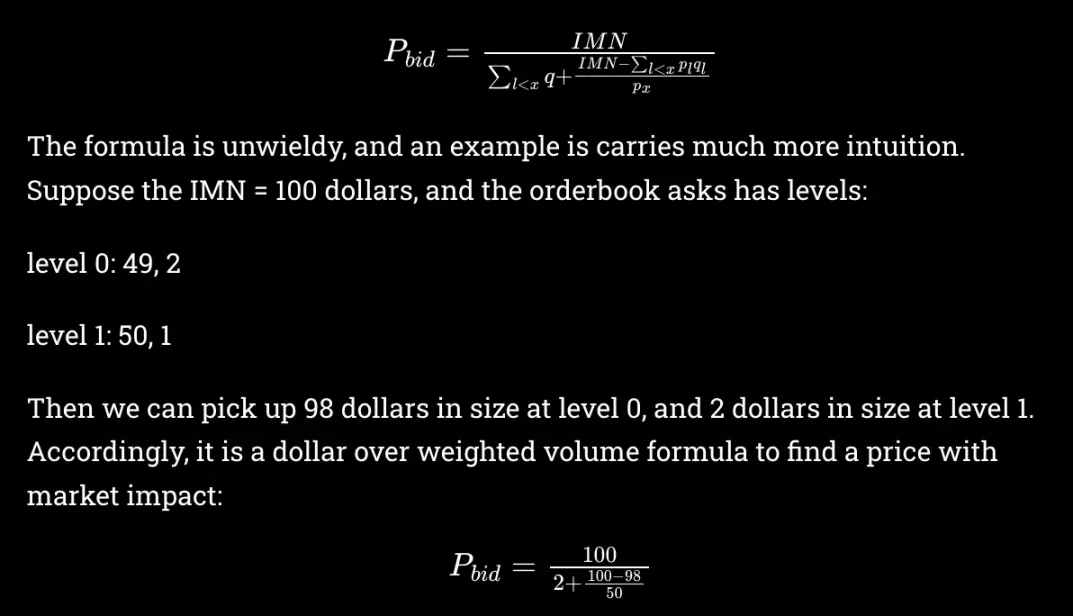

To be more aggressive, reverse-engineer from a break-even threshold. Forward explanation is clearer, so let’s walk through it: suppose you filled a $x short position and now want to hedge with a long. The effective taker price is the nominal weighted sum across depth—a concept explained in prior posts:

This affects the maker-taker spread and thus break-even. You can back out desired aggressiveness from acceptable break-even thresholds.

When rolling existing trades into new ones, break-even must include exit costs.

Risk

External risks include counterparty risk, hacking risk, etc. These require little commentary—they're hard to quantify and inherent in any risk-premium business. That’s a feature, not a bug.

More critical are internal risks, particularly margin risk. These mostly stem from underestimating market volatility and overconfidence. Sharpe ratios above 10 aren’t rare here—the expensive part is volatility.

High Sharpe and costly volatility (low capital efficiency) form a perfect recipe for overtrading—the simplest yet most dangerous pitfall. LTCM’s collapse, the subprime crisis—we repeatedly fail self-control. Human irrationality often exceeds even the most sophisticated models.

The primary operational risk is margin shortfall. Regardless of position structure, transferring margin from profitable to losing exchanges is wise. But this remains vulnerable to market crash scenarios—when you need transfers most, network congestion might prevent them.

One way to mitigate crash risk is beta hedging. Several approaches exist. Assume beta comes from a single-factor risk model. One method is selecting pairs so that beta exposure per exchange is roughly neutral.

This becomes easier with more exchanges—more combinations allow satisfying neutrality constraints. The trade-off is reduced search space.

Another approach: build portfolios normally, then apply beta hedges using major assets to neutralize beta per exchange. Since hedges are applied per exchange, net portfolio delta remains neutral. Cost: additional capital.

Less conventional methods include pairing Bitcoin with other assets purely for funding yield. Trade-off: taking on delta risk.

If managed well, portfolio risk is largely controllable. Worst-case scenario engines can still handle tail risks. Single positions can destabilize markets—especially true in crypto.

When margin reaches certain thresholds, proactively reduce positions instead of waiting for liquidation. Benefit: you control the pace; exchanges won’t.

Related Arbitrage Methods

Last but not least, there are other forms of funding rate arbitrage worth noting. We’ve focused on perpetual-perpetual cross-exchange arbitrage, but others exist (from 0xLightcycle’s tweet):

-

Same exchange — short perpetual, long spot

-

Same exchange — short quarterly futures, long spot

-

Same exchange — borrow/sell short spot, long perpetual

-

Two exchanges — short perpetual on one, long perpetual on another

-

Statistical factor arbitrage — short all high-funding contracts, long low-funding ones

-

Dynamic funding rate arbitrage

0xLightcycle provides rough comparisons for each method—we won’t repeat them here.

One advantage of perpetual-perpetual arbitrage is no long/short constraints, meaning performance relies less on market direction and more on structural differences in funding flows across venues. Spot-perpetual arbitrage tends to perform better in bull markets, relying on price-insensitive, leveraged longs who provide liquidity compensation.

On boosting arbitrage yields, two final points:

Exchanges often offer yield-bearing collateral and margin options. For example, holding USDE as collateral on Bybit earns yield. Yield-generating synthetic collateral is also coming soon on Paradex.

Lastly, spot-perpetual arbitrage is often combined with spot staking to enhance yield. This resembles what Resolv does. For instance, buy spot HYPE, short perpetual HYPE to earn funding, and stake the spot for additional yield.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News