Viewpoint: U.S. legislation banning Tether would pose a threat to national monetary security

TechFlow Selected TechFlow Selected

Viewpoint: U.S. legislation banning Tether would pose a threat to national monetary security

Banning offshore stablecoins like Tether could undermine the global dominance of the U.S. dollar, trigger inflationary risks, and pave the way for geopolitical rivals to fill the market void.

Author: Tom Howard

Translation: TechFlow

The following is an opinion piece by CoinList's Head of Financial Products and Regulatory Affairs, Tom Howard.

The current draft of the Stablecoin Bill circulating in Congress could effectively ban Tether and other non-U.S. stablecoin issuers from operating in the United States due to offshore operations.

This would be a significant policy mistake.

The strength of a global reserve currency lies in its ability to expand overseas—not in pulling it back domestically.

Attempting to force all dollar-denominated stablecoins to hold deposits in U.S. banks ignores a key monetary principle—the "Triffin Dilemma." This theory states that exporting currency abroad increases international demand, but if too much flows back domestically, it risks inflation.

While bringing innovation home is sound economic policy, repatriating dollars falls under monetary policy—and is generally not ideal for a nation.

In fact, stablecoin innovation offers the U.S. dollar an opportunity to push more dollars overseas, thereby strengthening the dollar’s role as the world’s dominant reserve currency and enhancing its global liquidity.

But why can't this goal be achieved through U.S.-based issuers alone?

Markets Prefer Non-U.S. Issuers

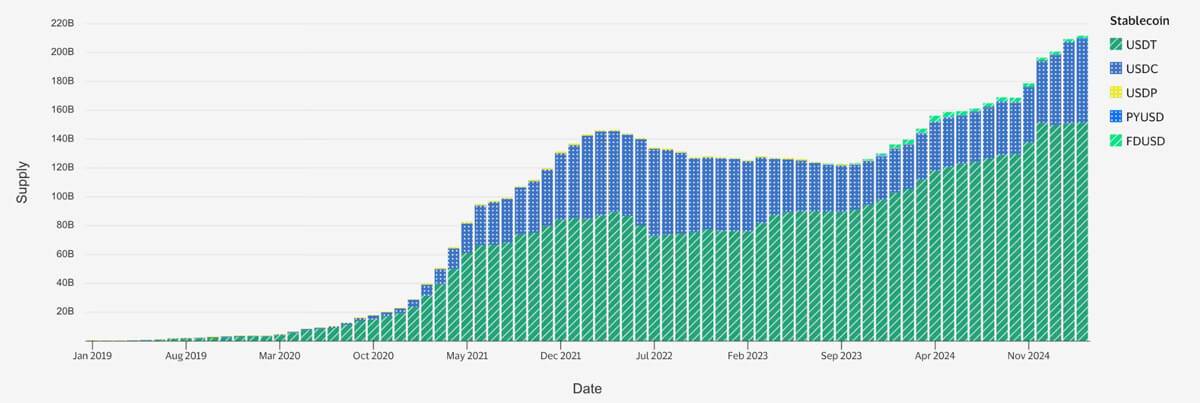

Clearly, in non-U.S. markets—from Asia to Africa to Latin America—USDT is the dominant stablecoin of choice. This isn’t because competitors like Circle (the second-largest issuer) haven’t tried to enter these regions. In fact, Circle has made substantial efforts.

In my user research on stablecoin and stablecoin wallet developers, I found that stablecoins backed by U.S. banks are often perceived as direct extensions of the U.S. government, while non-U.S. issued stablecoins are seen as more autonomous. Regardless of technical accuracy, this perception is widespread in the market.

Many users adopt stablecoins because their local governments have oppressive monetary or banking policies, and they fear potential government overreach. They want access to the U.S. dollar—but without being subject to the U.S. banking system.

These concerns have been amplified by major incidents such as the overuse of sanctioning power and frequent issues like frozen funds in cross-border payments or remittances.

Stablecoins give users greater confidence in financial sovereignty, and real-world usage data shows clear market preference for non-U.S. issued stablecoins—even before Tether began disclosing audited reserve reports.

Tether likely recognizes that moving its entire system into the U.S. banking framework would cause it to lose a large portion of its user base, creating space for other players to meet this clear market demand.

What Does “Ban” Mean?

Several versions of the current draft could lead to different forms of bans.

First, stablecoins issued by non-U.S. registered entities may be banned from issuance within the United States. That’s reasonable—U.S. issued stablecoins should be under U.S. regulation!

Second, there may be a ban on the “use” of unregistered stablecoins. This could extend from payment processors and exchange trading to peer-to-peer transactions. Such a ban restricts market choice, creates negative externalities internationally, and may even be difficult to enforce.

A third form of restriction could limit any financial services cooperation with U.S. entities. In this case, U.S. financial institutions would be forced to halt all related activities—including purchasing U.S. Treasuries. For Tether, this could mean selling off more than $100 billion in U.S. Treasury holdings.

Any Form of Ban Would Be Counterproductive

-

Reduced Global Dollar Liquidity: A transaction ban would weaken the liquidity between stablecoins and the U.S. dollar, increase transaction costs, harm users, and ultimately reduce global demand for the dollar.

-

Inflation Risk: Reducing dollar reserves held by foreign banks could increase domestic inflationary pressure.

-

Geopolitical Risk: Foreign competitors could exploit unmet market demand by launching dollar-pegged tokens backed by non-dollar assets.

Repatriation of Foreign Banks’ Dollar Reserves

If forced to shift reserves into U.S. institutions, Tether would bring vast amounts of dollars back into the U.S., potentially exacerbating domestic inflation. Meanwhile, international demand for offshore dollar tokens would persist, prompting competitors to quickly fill the gap left by Tether overseas.

When dollars flow back from international circulation into the domestic banking system, it increases loan supply within U.S. banks—potentially fueling inflation.

Additionally, this move would reduce dollar holdings at foreign banks, which are critical for global dollar liquidity and facilitate international trade. It would also decrease demand for U.S. Treasuries, as these banks typically invest their dollar deposits into risk-free assets.

Beyond Tether, other issuers might also expand dollar adoption in specific markets. For example, Cambodia’s economy is already largely “dollarized.” Though the country has its own currency, most economic activity occurs in physical U.S. dollars.

If companies or banks in such countries seek to promote broader digital dollar usage, stablecoin innovation would be an ideal vehicle. These stablecoins might not operate under U.S. or EU regulatory standards, but their existence still benefits the U.S. by increasing dollar reserves held in foreign banks.

Competitors Could Replace the Dollar

As Tether and others have discovered, there is massive global demand for stablecoins issued outside the U.S.

Banning non-U.S. issuers could open the door for foreign competitors to issue dollar-pegged tokens backed by foreign currencies, gold, or other assets—effectively displacing the U.S. dollar.

This would reduce both demand for and supply of the U.S. dollar. If scaled significantly, it could severely undermine the dollar’s global dominance.

Other nations might launch dollar-denominated stablecoins backed by gold or the Chinese yuan.

U.S. policy should instead encourage more dollar reserves to be held in foreign banks—to strengthen the dollar’s global standing.

A Better Path Forward

The above risks can be avoided by amending the Stablecoin Bill to create exemptions for foreign-issued stablecoins.

Allow these stablecoins to operate, trade, and be used within the U.S., but clearly label them as unregistered, higher-risk alternatives—distinct from fully regulated U.S. stablecoins. At the same time, grant U.S.-registered stablecoins corresponding advantages reflecting their lower risk profile.

Such exemptions could:

-

Encourage global innovation to meet offshore dollar demand.

-

Enhance global use of the dollar while avoiding imported inflation pressures.

-

Maintain market-driven competition, allowing consumers to choose based on transparent risk disclosures.

This could be achieved by explicitly excluding foreign-issued stablecoins from the definition of “payment stablecoin,” or by establishing a lighter registration process requiring only disclosure—not the full compliance standards (or associated benefits) required of U.S.-approved stablecoins.

By allowing stablecoins like Tether’s to coexist under regulation rather than banning them outright, the U.S. can strategically reinforce the dollar’s global dominance, mitigate inflation risks, and foster financial innovation worldwide.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News