Interpreting Solana SIMD 228 Proposal: Reducing SOL Inflation and Reshaping Staking Economics

TechFlow Selected TechFlow Selected

Interpreting Solana SIMD 228 Proposal: Reducing SOL Inflation and Reshaping Staking Economics

SIMD 228 proposes a static curve to reduce SOL issuance based on staking participation rate.

Author: Carlos

Translation: TechFlow

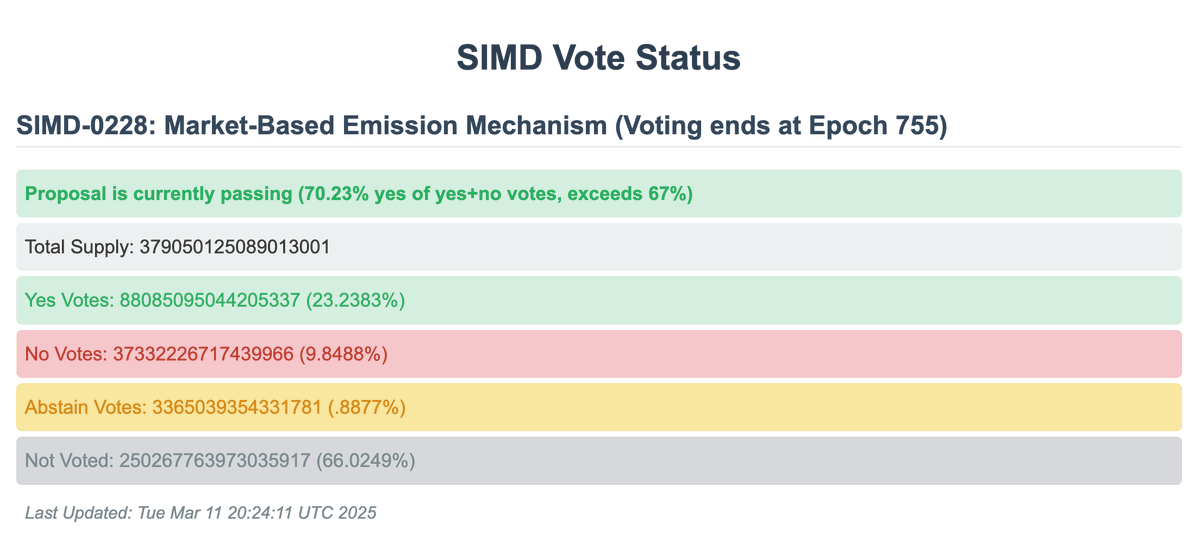

@solana SIMD 228 proposal has reached quorum, with 70% of voters in support. Voting will conclude at epoch 755, approximately 52 hours from now.

What is SIMD 228?

Why support it?

Why oppose it?

Let’s take a closer look.

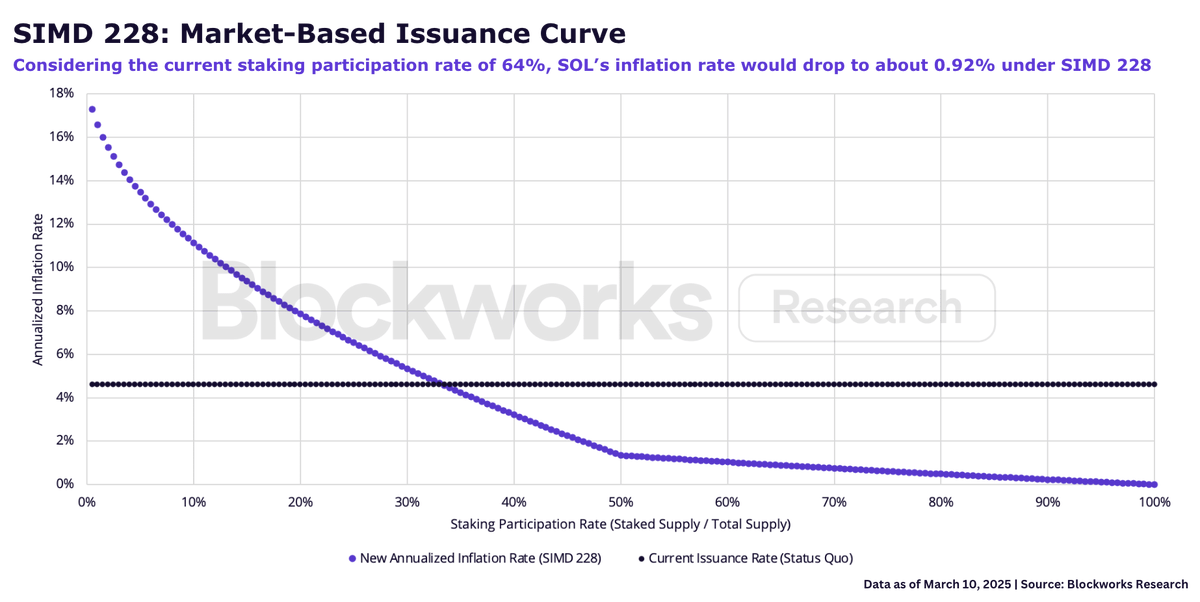

SIMD 228 proposes a static curve that reduces SOL issuance based on staking participation rate. With the current staking rate at 64%, after implementation and a smoothing period, the inflation rate of SOL would drop to approximately 0.92%. Notably, the curve becomes more aggressive when the staking rate falls below 50%, resulting in higher new issuance rates compared to the current fixed schedule—this is especially evident when the staking participation rate reaches one-third (about 33.3%).

Arguments in Favor

Reason 1: Solana currently pays excessive costs for security.

The optimal token issuance rate is the minimum level required to secure the network. The original authors of the proposal (@TusharJain_, @kankanivishal) argue that a fixed issuance schedule was reasonable when Solana was an emerging ecosystem without real economic value (REV). At that time, relying on token issuance to attract staking and ensure security was necessary.

However, given the current level of network economic activity and fees (REV), the fixed issuance schedule has become less justifiable, as it issues more SOL than needed to secure the network today. This is known as the "leaky bucket problem," which @MaxResnick1 defines as value leakage caused by taxes or intermediaries with market power (such as high-commission validators like Coinbase or Binance).

Reason 2: Nominal yield vs. real yield.

As @y2kappa points out, SOL issuance is an accounting trick that dilutes non-staked SOL holders and creates artificially high yields. Without distinguishing between nominal (issuance-based) and real (REV-based) yields, this incentivizes indiscriminate staking. As Solana matures, the network should become economically sustainable and run entirely on fees, reflecting true economic demand for using the network.

Reason 3: Markets are the best mechanism to determine pricing, and Solana's issuance should be no exception.

The conclusion from the above arguments is that even if SIMD 228 isn't perfect, a market-driven approach represents a significant improvement over the current fixed issuance schedule, which is arbitrary, inefficient, and increases selling pressure.

Arguments Against

Reason 1: SOL inflation subsidizes institutional distributions.

While token holders should only care about real yield, custodians and ETP issuers have different incentives. They are motivated to maximize nominal yield because they charge commission fees without exposure to the underlying asset (credit to @smyyguy for this framework).

Take staked SOL ETPs as an example: ETP issuers take a cut of staking rewards but bear no risk from holding the underlying SOL. Therefore, high nominal yields incentivize these players to sell more SOL products to clients, increasing their own revenue. From this perspective, what Resnick calls the "leaky bucket problem" is actually a distribution expense (@calilyliu). In my view, this is the strongest argument against SIMD 228.

Reason 2: Institutional appeal.

This relates directly to the previous point. According to @calilyliu, changing the fixed issuance model right before institutional interest peaks and a Solana ETF launches (possibly later this year) would be a strategic mistake. Liu argues that a market-based approach makes inflation unpredictable and unstable, reducing SOL’s attractiveness as an asset.

A counterargument is that SOL is already a highly volatile asset, and its 7–8% yield isn’t the main reason people buy it. Those who stop buying SOL due to lower nominal yields likely never understood its investment thesis in the first place.

Reason 3: Impact on validator profitability / reduction in validator count.

Voting fees denominated in SOL are currently the largest expense for validators. Some (@David_Grid) worry that SIMD 228 could affect small validators’ profitability, particularly if network activity and REV decline from current levels. In other words, the inflation curve under SIMD-228 might lead to a shrinking validator set, although some estimates suggest limited impact (under a 70% staking scenario, according to @0xIchigo and @__lostin__, the number of profitable validators is expected to decrease by 3.4%).

There are also secondary concerns about potential impacts of SIMD 228, including effects on Solana DeFi interest rates, whether reduced inflation might increase SOL selling pressure, and insufficient discussion around the proposal.

Regardless of how validators vote, understanding both sides is crucial for making informed decisions.

If passed, SIMD 228 would be implemented several months later, followed by a 50-epoch (approximately 100-day) transition period to smoothly bridge the old and new issuance curves.

Note: At the time of publication, the SIMD-0228 proposal has concluded voting and has not been approved. It received 61.39% support (counting only yes and no votes), falling short of the required 66.67% threshold to pass.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News