Confessions of a Market Maker: A Self-Help Guide for Projects Navigating the Dark Forest

TechFlow Selected TechFlow Selected

Confessions of a Market Maker: A Self-Help Guide for Projects Navigating the Dark Forest

In this dark forest of market makers, holding onto one's底线 is difficult—charming frauds who pretend to be profound will always attract more attention than honest, down-to-earth people.

Author: Maxxx

A confession from a market maker on the front lines, and a survival guide for project teams navigating crypto's dark forest—hope this helps you a little bit :)

Let me introduce myself: I'm Max, a 00s-born individual who already feels ancient. Originally a struggling finance student in Hong Kong, I've been living in the crypto space since 2021 (thank you, industry, for rescuing me). Though my time in the industry hasn't been long, I started as a founder, then went on to build a developer community and accelerator—keeping me close to early-stage founders. Now I lead the market-making business line at @MetalphaPro. My boss kindly gave me the title "Head of Ecosystem," though in reality, I handle BD and sales. Over the past year or so, I’ve worked with@binance, @okx, @Bybit_Official, and several tier-two exchanges, handling listings and subsequent market making for over a dozen coins—so I’ve picked up some modest experience.

Here’s my dog’s photo to anchor the post

Starting with GPS's "Observation Tag"...

I was chatting with a founder—a bright, capable young man I've known for over a year and who plans to list his token in Q2—when news broke that GPS had received an “observation tag” from @binance. He sounded exhausted despite his success: raised several million dollars, achieved solid milestones, yet behind the scenes carried the weight of investor expectations. To founders, every dollar raised is debt owed. After more than a year pivoting narratives in brutal markets, he juggles closing another funding round, negotiating with top-tier exchanges, and watching recent tokens crash at listing—worrying how his token will perform, how to answer to investors. Only those who’ve built projects truly understand this pain, anxiety, and confusion. As we chatted, Binance’s announcement popped up. Though we weren’t working together on market making, both of us had interacted with the team over the years—and instantly felt a wave of emotion.

I won’t analyze or comment further—gossip is tiresome. We should wait for official statements from Binance and the project team. But having seen too many projects and retail investors burned by market makers, I’m using this moment to write down my thoughts, hoping to help fellow builders and professionals. Enough rambling—let’s get into it.

Market Maker Business Models: Not as Magical as You Think—Just “Order Placers”

“Market maker” isn’t a new term in crypto—it exists in traditional finance too, where it’s often called Greenshoe (or green shoe), named after the U.S.-based Green Shoe Manufacturing Company, which first used this mechanism during its 1963 IPO. While details differ slightly, the core responsibility remains the same: provide two-sided quotes during an IPO to maintain liquidity and price stability. However, due to strict compliance regulations, Greenshoe operations are low-margin, standardized desk activities—no major trading desk would ever promote them publicly. Yet paradoxically, in crypto, this standard service has become mythologized as a powerful force that manipulates markets and controls prices.

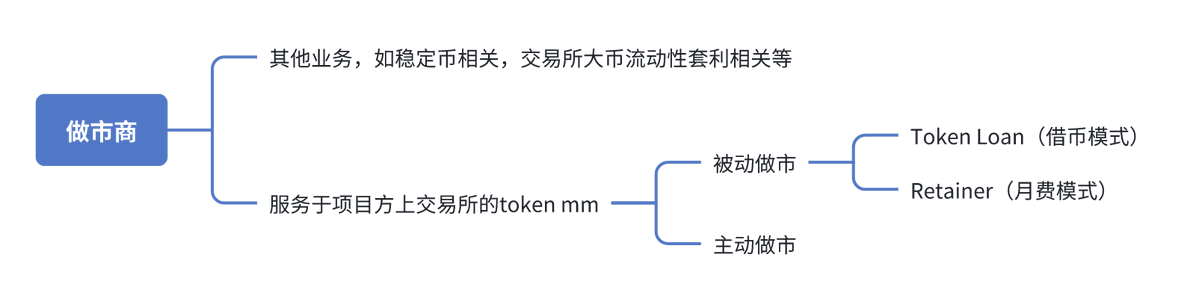

But if market makers actually followed industry norms and provided neutral liquidity, they wouldn’t be “slicers.” Providing liquidity simply means placing two-sided maker orders on order books. Of course, crypto broadly includes various types of market makers—but today we’ll focus only on the narrow category serving project teams during exchange listings. These can be categorized into several models:

Active Market Makers

Much of the demonization around market makers stems from the presence and practices of active market makers in crypto’s early days. In Cantonese, there’s a phrase “做厨房” (“running the kitchen”), Mandarin equivalent being “坐庄” (“acting as the house”). Active market makers fulfill all popular fantasies about what a market maker “should” do. They typically partner with projects to manipulate prices directly—pumping and dumping—for profit, splitting gains with the project while exploiting retail traders. Their deal structures vary widely, involving token loans, API access, margin financing, and revenue sharing. Some rogue operators even bypass the project entirely, using their own capital to accumulate large positions before running the show themselves.

Who are these active market makers? The ones you hear about—the ones doing PR, hosting events, building public profiles—are mostly passive market makers (or at least claim to be, to avoid compliance issues). Openly marketing as an active market maker would invite regulatory scrutiny.

Most active market makers operate quietly, often without names, because their work is inherently non-compliant. As the industry matures, previously high-profile players like ZMQ and Gotbit have been named by the FBI, facing serious legal consequences. Remaining active players stay underground. Some larger ones have built reputations through so-called “successful cases,” gaining informal “street cred,” and rely heavily on referrals from trusted insiders.

Passive Market Makers

Passive market makers—including ourselves and many peers—fall under this category. Our main job is placing maker orders on centralized exchange order books to provide genuine liquidity. There are two primary business models:

-

Token Loan (token borrowing)

-

Retainer (monthly fee)

Token Loan Model

This is currently the most common and widely adopted model. Simply put: the project lends tokens to the market maker for a fixed period, and the market maker provides liquidity services.

A typical token loan deal consists of several components:

Borrowed amount x%: usually a percentage of the total token supply

Loan duration x months: length of the agreement; upon expiry, services end and settlement occurs per agreed terms

Option structure: defines the settlement price between the project and the market maker at contract end

Liquidity KPIs: specify depth and spread across exchanges and price ranges

How does the market maker profit?

The market maker earns from two sources: first, the bid-ask spread generated while quoting; second (and more significantly), from the option granted by the project.

If you're familiar with finance, you know that every option has intrinsic value on day one. This value is typically a percentage of the borrowed token’s worth. For example, if $1M worth of tokens are borrowed and the option is valued at 3%, then by strictly following delta-hedging algorithms, the market maker locks in ~$30K in relatively certain profits. Under normal conditions (excluding extreme scenarios like moonshots or instant crashes where hedging fails), the desk’s expected return is $30K plus minor gains from spreads.

Doesn’t sound like much? Actually, this margin isn’t unrealistic—market makers are highly competitive now, and attractive option terms have little room for excess.

Retainer Model

The second mainstream model. Here, the project doesn’t lend tokens but retains them in its own trading account. The market maker accesses the account via API to provide liquidity. A key benefit: the project keeps custody of its tokens, and all activity is transparent—funds can theoretically be withdrawn anytime. Thus, there’s minimal risk of malicious behavior by the market maker. However, the project must fund the account with both tokens and stablecoins for two-sided quoting, and pay a monthly service fee.

In this setup, the market maker earns solely from the monthly fee. All funds in the account belong to the project. During periods of poor liquidity or sharp volatility ("pinning"), losses from quoting fall entirely on the project.

Both Token Loan and Retainer models have pros and cons. Some desks specialize in one; others (like us) offer both. Projects should choose based on their specific needs and circumstances.

Common Misconceptions

-

Market makers are responsible for “pumping,” “drawing charts,” or creating “rat holes”

No. Qualified passive market makers remain neutral and do not actively engage in price manipulation or insider trading.

-

Providing liquidity equals volume washing

Exchange order books contain two types of orders: maker and taker. Passive market makers primarily place maker orders, with minimal taker activity. Even deep maker orders won’t boost volume unless matched by real takers. Self-trading (e.g., executing against your own orders) poses compliance risks—top exchanges actively monitor and penalize excessive self-trade ratios, which could result in warnings or suspension for both the market maker and the token.

-

So passive market makers seem useless?

They don’t directly control price or volume—but good liquidity is foundational. Small traders follow trends; large capital looks first at volume and depth. Healthy trading activity reflects product strength and marketing—and requires tight coordination with market makers. More importantly, top-tier CEXs rarely allow listing without professional MM support. Without pre-registered market makers, launch chaos is likely. So yes, partnering with passive market makers remains a necessary step for any project aiming for a major CEX listing.

-

Since market making is just placing orders, why not do it ourselves?

Yes and no. If you have an in-house trading team and sufficient scale, some tier-two exchanges may allow self-market-making. Otherwise, especially if building a new team, I recommend leaving it to professionals. The cost and risk of setting up a team often outweigh hiring a reliable MM. Plus, without experience, managing quotes during volatile conditions can lead to significant losses.

The Market Maker’s Role: Launch Liquidity Is the Most Valuable Resource

Now that we’ve covered the mechanics, let’s discuss the current landscape—to better contextualize everything.

What kind of market are we in during 2024–2025? From a liquidity perspective, here’s how I see it:

-

BTC marches independently upward, with abundant top-tier liquidity. Recent pullbacks haven’t shaken fundamentals. Miners’ break-even costs start at five or six figures—they’re happy. Traditional institutions rushing in are also pleased.

-

Tail-end PVP is intense, with relatively strong liquidity. Platforms like @pumpdotfun, @gmgnai, @solana, @base, and @BNBCHAIN keep retail gamblers hooked (I’ve contributed my share—damn it). Outliers and insiders profit handsomely.

-

Mid-tier liquidity is drying up. The Trump/Libra wave marked a peak, sucking mid-cap liquidity almost entirely out of the ecosystem—in a structural, irreversible shift from crypto-native to external capital. Tokens valued between hundreds of millions to billions now face awkward positioning. New listings on tier-one/two exchanges struggle to find buyers. Volume collapses within weeks. Most trading happens at launch. Prices quickly drop below VC entry levels. By VC unlock, losses are likely; by team token unlock, near-zero.

This cycle, mid-tier tokens seem to suffer the most. But here’s a harsh truth: over 90% of so-called “Web3 native” professionals—those paying salaries, attending conferences, building products, doing BD, marketing, development—are all operating within the mid-tier token economy. Funding rounds, product launches, promotions, farming, exchange listings—all revolve around these mid-tier, CEX-listed projects. Hence, this cycle, most insiders haven’t made money. Life’s tough for everyone.

Yet market makers hold the scarcest resource for mid-tier tokens: “launch liquidity.” Yes, liquidity alone isn’t enough—it must come early, at launch. Once a project dies, holding infinite tokens means nothing. At launch, say 15% of supply circulates—typically 1–2%, sometimes more, goes to market makers. This immediately unlocked launch liquidity is incredibly valuable in today’s environment. As a result, competition among market makers intensifies—not just from dedicated firms, but also VCs and project teams hastily assembling temporary MM squads. Some lack basic trading skills but think: “Grab the tokens anyway—ultimately it’ll go to zero, so delivery risk doesn’t matter.”

Dark Forest of Gresham’s Law: Honest Builders Lose to “Toxic Players”

Under these dynamics, a unique market maker ecosystem has emerged: increasing numbers of providers, with pricing so cutthroat it’s absurd; wildly varying service quality; frequent post-sale issues—most commonly, withdrawing liquidity or breaching contracts to dump. Let’s clarify: market makers aren’t forbidden from selling. In fact, if the price surges, algorithmic quoting naturally shifts toward selling, since they borrowed tokens and settle in USD (see the token loan + option section again if unclear). But a qualified passive market maker should quote fairly via algo—not aggressively sell as takers. Such actions severely harm the project.

Why do they do it? Recall the option discussion earlier: a market maker securing a token loan expects ~3% gain via proper delta hedging under flat conditions. But if they believe the token will be worthless at expiry, they can instead dump early and capture nearly 100% of the token’s current value—about 33x the legitimate profit. Of course, this is an oversimplified, extreme case. Real-world tactics are more nuanced. But the logic stands: short the token, sell high when price and liquidity are strong, buy back cheap at settlement.

Beyond ethics and compliance, this approach carries risks: inability to meet liquidity KPIs during the contract (due to insufficient inventory); catastrophic losses if the bet is wrong, leading to failed settlement.

Why Is This So Common?

-

The industry remains in its early stages regarding compliance. While market makers provide daily/weekly reports, dashboards, and third-party monitoring tools exist, what happens inside their accounts remains a black box. Only centralized exchanges have definitive proof of every trade a market maker executes. Yet many market makers are VIP clients (V8/V9) of these exchanges, generating tens of millions in fees and deposits annually. Exchanges have a duty to protect client privacy—how could they possibly disclose detailed trade data to help projects seek justice? That’s why I deeply respect @heyibinance and @cz_binance for taking swift action—I recall this was the first time precise transaction records were fully disclosed, down to the minute, including operation details and cash-out amounts. Whether such transparency should become standard is debatable—but the intent was undoubtedly positive.

-

Project teams and the broader industry still lack understanding of market makers. I’m often shocked: many top-tier VCs, founders who’ve raised millions, even exchange staff—don’t truly understand this role. That’s precisely why I wrote this piece. Most projects are “first-timers”; market makers are battle-hardened “toxic players.” As a frontline operator, I sometimes wonder: should I match competitors’ outrageous terms just to close deals? In this dark forest of market making, integrity is hard. The slick, mysterious “bad boy” always attracts more attention than the honest, diligent worker. Only when collective industry knowledge improves can we prevent bad actors from driving out the good.

How to Choose Your Market Maker

Some key questions and tips I recommend:

-

Should you never consider active market makers?

When asked, I don’t outright say no. Setting aside compliance, it’s debatable. Some projects achieve better charts, higher volume, bigger exits through tight collaboration with active MMs—though failures far outnumber successes. My view: whoever can pump your token for real will also ruthlessly dump it. With finite market liquidity, you and your active MM are ultimately counter-parties—money flows to either you or them.

-

Token loan vs retainer—how to decide?

Token loan remains dominant, but retainer adoption is slowly rising. It depends on your preferences. Projects wanting full control over supply may avoid external large-scale liquidity. Others may prefer transparency and reduced counterparty risk.

-

Avoid relying on just one passive market maker

Don’t put all eggs in one basket. Use 2–4 market makers: compare terms, ensure redundancy if one fails. To win your business, each may offer extra value-adds—more partners mean more support. But to avoid the “three monks, no water” problem, assign different exchanges to each MM. Mixing them increases monitoring complexity dramatically.

-

Don’t choose your market maker solely based on investment

You can accept investment from a market maker—extra runway is always welcome. But understand: MM investment plays a different game than VC investment. Controlling significant launch liquidity, MMs can hedge or lock in prices for their invested (yet locked) tokens. So while receiving investment seems beneficial, combining token loans with large invested positions isn’t necessarily ideal for the project.

-

Don’t select based purely on liquidity KPIs

KPIs are hard to verify precisely in practice. Don’t choose based solely on impressive-sounding metrics—what matters is execution. Before lending tokens, you’re in control; once tokens are sent, you become dependent. There are many ways MMs can deceive you.

-

Shift your mindset: become the “toxic player”

Remember—you’re the client. Compare terms thoroughly. Discuss monitoring mechanisms, safeguards against breaches, and choose the strategy best aligned with your project’s goals. Use one MM’s offer to pressure another. Negotiate clearly—no vague clauses. If anything is unclear, ask directly.

A Few Final Thoughts

I’m a newcomer, but grateful for the chance to deeply engage with this industry. I often feel its dirtiness and chaos—yet also sense its vitality and promise. I don’t consider myself among the brightest, but I see many talented young peers quickly finding their path. Still, far more young people feel lost—with few alternatives outside Web3 for upward mobility.

I’m lucky to have an exceptionally principled boss and a highly skilled trading team backing me. Our stable asset management business means we don’t rely on market making to sustain operations—we use it to build relationships. I’ve moved at my own pace, prioritizing friendship over short-term gains. I’ve missed deals, sure—but also closed a few I’m proud of. Some projects didn’t work out commercially, but became real friendships.

I’ve written a lot. Publishing this felt difficult. Partly because I worry my limited expertise or poor phrasing might mislead readers. Partly because market makers have long operated in silence—I feared crossing invisible lines or threatening someone’s interests.

But I truly believe that as the industry evolves and compliance becomes standard, the role of market makers will eventually shed its dark reputation and step into the light. Maybe this article can help—even just a little.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News