Crypto Apocalypse in February 2025: Power Law Growth, Retail-Driven Narratives, and Macroeconomic Reflections

TechFlow Selected TechFlow Selected

Crypto Apocalypse in February 2025: Power Law Growth, Retail-Driven Narratives, and Macroeconomic Reflections

The current crypto market has cooled down from its previous frenzy, with retail-driven narratives leading to increased volatility. However, this market correction could create opportunities for long-term investments and the emergence of new narratives.

By: Michael Dempsey

Translation: Baicai Blockchain

The crypto market is now in an interesting phase. It’s only been 8–12 weeks since the peak of market euphoria, yet we’re constantly hearing news that governments—once the most criticized entities by the crypto community—are now embracing this asset class and its underlying technology. Despite this, the market sentiment has sunk into a kind of lethargy I haven’t seen in a long time.

The old joke “developers, just do something” now rings hollow. Because “the developers”—in this case, policymakers—have actually acted. They’ve chosen to liberalize the market, removing many of the restrictions and hostilities previously imposed on crypto. So frankly, the future of this industry now rests entirely in our own hands.

So what exactly happened? Nobody knows for sure—but here are some thoughts I had this morning.

1. Macro Landscape

I won’t go into a detailed review of the crypto market over the past few months, but it's fascinating to observe how market psychology has shifted—and softened—in response to our president and other macro forces.

https://x.com/mhdempsey/status/1878788617004548287

In 2024, many profited from the so-called “Trump trade,” specifically betting that markets underestimated Trump’s chances of winning and the policy shifts that would follow. But now, both at the broader market level and within crypto, it appears the Trump trade was overbought. His election (and the immediate aftermath) may have been a classic “buy the rumor, sell the news” event. After all, Bitcoin surged from ~$70K to $106K following his victory, then entered a correction phase. As often happens in crypto, the market once again ran ahead of reality.

I won’t dwell too much on price action here, but I recommend following Smac and reading his recent posts on volatility and related topics. From a medium-term view, I’m slightly more bearish than Smac—but he might just be smarter than me, so definitely check out his take.

Now, let’s talk about something beyond just prices.

2. Stop Outsourcing Market Narratives to Retail

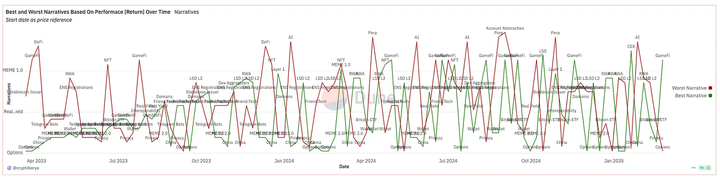

Crypto narrative Dune dashboard

This might sound odd, but I believe the crypto market has largely outsourced speculation and narrative creation to its smallest participants—retail investors—and those positioned at the furthest edge of the risk curve. This creates a feedback loop where less sophisticated, highly impressionable speculators end up driving market narratives. These stories spread through echo chambers like Crypto Twitter, trader group chats, and regional divides between Western and Asian markets, only reaching institutional players later—if at all. And some institutions themselves employ retail-like investment analysis, further amplifying the trend.

These narratives drive massive price swings and absorb significant capital, especially during periods when no new participants are entering the market. Capital rotation happens almost weekly, with tokens surging violently before crashing down 80% or more. Such dynamics neither support long-term investing nor attract fresh inflows into crypto (outside of BTC), nor do they foster sustainable industry development.

I think what’s truly needed is for projects to proactively shape how their products are positioned within the crypto ecosystem. In other words, teams should lead narrative creation instead of chasing existing ones.

Some might argue that the only thing that matters in crypto is gambling—switching tokens in hopes of making more money. Even within that framework, however, different narratives can still be built around that core mechanic.

Typically, large projects (L1s and L2s) chase prevailing narratives, hoping short-term TVL growth will translate into long-term success. The problem is that big projects move slower than small ones, so by the time they pivot toward a narrative, it’s often already dead. We recently saw this play out with the AI narrative: TAO captured most of the value early and successfully defined the story, while later “GPT wrapper” micro-projects diluted its impact.

We’ve seen similar patterns across various “X + crypto” concepts, such as:

-

NFTs (art + crypto)

-

Investment DAOs (fund investing + crypto)

-

RWA (traditional finance + crypto)

-

OHM (greater fool theory + crypto)

More recently, we’ve witnessed the rise of memecoins at scale (“cultural” speculation + crypto, or meta-gaming narratives + crypto). And we’ll likely keep seeing similar cycles repeat in the future.

All crypto projects ultimately aim to build a core user base—what we usually call a “community”—aligned ideologically and economically with the project. With that in mind, if you're building a project, your goal should be to establish an early “propaganda arm.” As an organization, foundation, or well-funded group with far greater resources and reach than any individual retail investor (after all, you've launched a token or raised funds), your job is to create a narrative you genuinely believe in, and promote to the market why it matters—and why your project should lead it. Don’t try to compete for attention within an already-established narrative. Competition is a loser’s game, especially when fighting over existing stories.

Bet on the future you believe in, and become the Schelling Point Protocol for that vision.

3. Power Law & Compounders

As an investor spanning venture capital, crypto, and public equities, I’ve noticed vast differences in consensus across these markets. Many enjoy drawing parallels between public markets and crypto, but one key misunderstanding reveals a fundamental issue in today’s crypto landscape—and perhaps explains why some people (maybe just me) feel disillusioned.

Over the past 5 to 15 years, public market investors have increasingly embraced the concept of long-term compounding returns at the company level. Large companies have grown bigger than anyone expected, accumulating far more value than initially perceived. These firms often share traits like riding successive tech waves and starting with expansive visions. This investment thesis suggests that allocating capital to high-quality businesses capable of steady, predictable growth—with manageable drawdowns—is superior to betting on volatile companies that might surge but also collapse by 80% or more.

In public markets, this trend has made life harder for hedge funds. The “Mag7” (Microsoft, Apple, Google, Amazon, Meta, Tesla, NVIDIA) and other compounders have generated enormous momentum within major indices, making it difficult for hedge funds to outperform without taking on substantial risk. As a result, many fund managers have shifted toward concentrated, long-term holdings—often including a portion of Mag7 stocks—claiming they can achieve relatively low drawdowns even in brutal bear markets like 2022. (Though in reality, many still piled into speculative tech stocks and were ultimately wiped out.)

1) The Compounding Challenge in Crypto

Crypto hedge funds face similar pressures, particularly due to Bitcoin. Bitcoin (in my view) offers exceptional risk/reward and anchors multiple core narratives—“digital gold,” “inflation hedge,” and “crypto index.” It often serves as the benchmark for all liquid crypto strategies. Like traditional hedge funds, many crypto funds perform well during bull runs, primarily relying on leveraged long positions. But when the market turns, they suffer severe drawdowns and underperform Bitcoin significantly during risk-off periods, leading to long-term underperformance against the benchmark.

Historically, there have been almost no true “compounding” assets in crypto, except perhaps L1s like ETH and SOL. Infrastructure projects naturally lend themselves to horizontal scaling and sustained growth. Now, some teams are attempting to break this mold—but a critical question remains: Can existing token economic models support long-term compounding? Or would building a genuine compounding business require starting as a company from scratch, rather than launching a token too early? (This might be another strong reason why projects shouldn’t rush to issue tokens.)

2) The Future of Compounding Projects

We think deeply about this. Regardless, we believe this dynamic will shift in crypto. Founders are beginning to see their projects as potential compounding assets, with broader strategic visions than in previous cycles. This evolution could bring more rationality to the space and help establish a core set of benchmarks. Currently, crypto lacks a cohort of assets offering solid risk-adjusted returns, forcing participants into hyper-speculative “shitcoin” trading and constant capital rotation. If authentic compounding projects emerge, the entire investment logic of the market could transform.

4. Conclusion

As Bitcoin and the broader market slowly declined from ~$95K to $80K, I found myself reflecting on how to build lasting value in crypto—a somewhat idealistic, even utopian notion that feels ironically timed. This pullback has been one of the most orderly sell-offs I’ve seen recently. Yet, watching the industry retreat from pure “faith-based” investing, I believe this moment presents an opportunity: to build new investment frameworks, craft original narratives, and establish differentiated fundamental viewpoints amid the rubble left behind after low-conviction holders exit the market.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News