Reviewing the Gains and Losses of the 2024 Crypto Market: Where Is the Path Forward for 2025?

TechFlow Selected TechFlow Selected

Reviewing the Gains and Losses of the 2024 Crypto Market: Where Is the Path Forward for 2025?

New cycle, new direction, new applications.

By Tuoluo Finance

2024 has undoubtedly been a pivotal year in the history of crypto.

This year, centered around two major narratives—ETFs and the U.S. presidential election—and leveraging Bitcoin as the primary catalyst, the crypto industry achieved a breakthrough. Publicly traded companies, traditional financial institutions, and even national governments have all entered the space. Mainstream adoption and recognition surged significantly, while the regulatory environment shifted toward clarity and leniency with the incoming administration. The convergence of mainstream finance, path divergence, and regulatory evolution became the dominant themes of the year.

01 Reviewing 2024: Bitcoin Reaches New Heights, Ethereum Faces Challenges, MEME Casinos Draw Attention

Looking at the industry's key developments this year, Bitcoin was clearly the central narrative.

ETF approvals and national reserves propelled Bitcoin past $100,000, officially marking its transition beyond being just a cryptocurrency to becoming a globally recognized hard asset for inflation hedging and value storage. BTC is gradually evolving from digital gold into a potential supranational currency, signifying a milestone victory for Satoshi Nakamoto’s grand financial experiment. Meanwhile, the Bitcoin ecosystem expanded this year. Though inscriptions, runes, and L2s experienced extreme volatility between hype and collapse, a diversified Bitcoin ecosystem has begun to take shape. Applications such as BTCFi, NFTs, gaming, and social platforms continued developing. Bitcoin DeFi TVL skyrocketed from $300 million at the beginning of the year to $6.755 billion—a more than 20-fold increase. Among them, Babylon emerged as the largest protocol on Bitcoin, reaching a TVL of $5.564 billion by December 20—accounting for 82.37% of the total. Broadly defined BTCFi also performed exceptionally well this year. The explosive growth of spot Bitcoin ETF shares and MicroStrategy’s inclusion in the Nasdaq 100 made it a model widely emulated, highlighting Bitcoin’s overwhelming success in the CeFi domain.

In contrast, Ethereum—the leading smart contract platform—had a tougher year. It underperformed compared to other assets, with declining value capture and user activity, and its narrative weakened significantly. The "value thesis" put Ethereum under pressure. While the rallying cry for a DeFi revival gained consensus, beyond the recursive staking-driven TVL bubble, only Aave seemed to carry the burden. Real investment remained insufficient. However, the emergence of Hyperliquid, a dark horse in derivatives near year-end, not only disrupted half of CEX’s dominance but also sounded the counterattack for DeFi. On another front, after the Dencun upgrade, competition among Ethereum Layer 2s intensified, steadily capturing market share from the mainnet. This sparked widespread debate about Ethereum’s long-term mechanism, with growing skepticism—even rumors circulating that Ethereum’s future might belong to Coinbase given Base’s rapid rise.

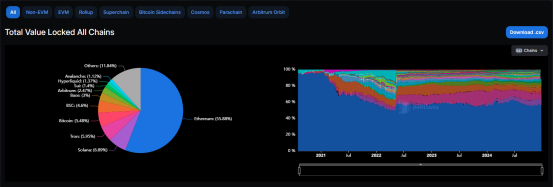

Solana’s strong ascent stood in stark contrast. In terms of TVL, Ethereum’s share among public blockchains dropped from 58.38% at the start of the year to 55.59%, while Solana surged from near obscurity to claim 6.9% by year-end, becoming the second-largest blockchain after Ethereum. SOL delivered miraculous growth, rising from $6 two years ago to $200 today—an over 100% gain within 2024 alone. From a recovery standpoint, Solana leveraged its unique advantages of low cost and high efficiency, targeting core liquidity needs. Fueled by Degen culture, it ascended as the undisputed king of MEMEs and became this year’s retail investor hub. Solana surpassed Ethereum multiple times in daily on-chain fees, and new developer growth outpaced Ethereum, signaling a clear trend of overtaking.

TON and SUI also broke through this year. Telegram, with 900 million users, single-handedly ignited the Web3 gaming sector, opening a new gateway for Web3 traffic and providing a strong stimulus to a previously stagnant market before September. Backed by such massive support, TON finally moved from prolonged anticipation into a fast-growth phase. According to Dune data, TON has accumulated over 38 million on-chain users and more than $2.1 billion in transaction volume. SUI impressed entirely through price performance. As a Move-language chain, it advanced rapidly with hardware innovation, protocol diversification, and strategic airdrops, painting a bright outlook. Compared to SUI’s price-driven momentum, Aptos—its peer chain—though weaker in price performance, attracted more traditional capital. This year, it successfully partnered with BlackRock, Franklin Templeton, and Libre. Its compliance-focused approach may position it well for upcoming cycles in RWA and BTCFi.

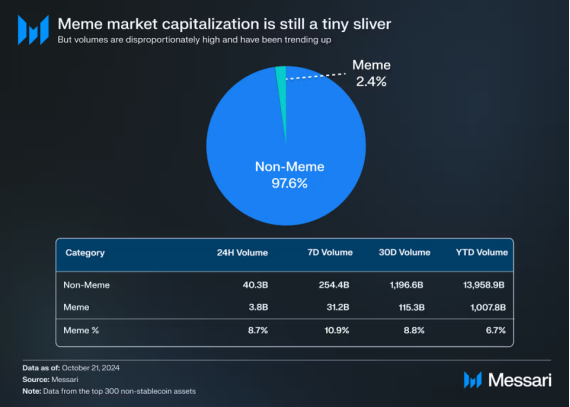

From an application perspective, MEMEs were the primary driver of this year’s market. In essence, the rise of MEMEs reflects a shift in the current market landscape—VC-backed tokens failed to gain traction, excess liquidity lacked viable targets, and ultimately poured into sectors offering greater fairness and profit-seeking opportunities. Within this, the concept of MEME itself has continuously expanded—from mere speculative assets to emblematic representations of cultural finance. 'Everything can be a MEME' is now becoming reality. Despite accounting for less than 3% of the top 300 cryptocurrencies (excluding stablecoins) by market cap, MEMEs consistently captured 6–7% of trading volume, peaking at 11% recently, making it one of the most liquid sectors. According to CoinGecko, MEMEs attracted 30.67% of investor attention this year—ranking first across all categories. Where attention goes, money follows. Indeed, this year’s MEME scene saw pre-sales, celebrity tokens, zoo-themed coins, PolitFi, and AI—all become major trends within the space.

Against this backdrop, infrastructure supporting MEMEs continued strengthening. Fair-launch platform Pump.fun emerged, reshaping the MEME landscape and becoming one of the most profitable and successful applications of the year. In November, Pump.fun became 'the first Solana protocol in history to generate over $100 million in monthly revenue.' According to Dune data, as of December 22, pump.fun had generated over $320 million in cumulative revenue, with approximately 4.93 million tokens deployed.

Of course, platform profits don’t necessarily mean retail gains. Considering the one-in-a-hundred-thousand chance of hitting a jackpot and only 3% of users profiting over $1,000 on Pump.fun, coupled with the increasingly evident institutionalization of MEMEs, retail investors remain vulnerable to being exploited regardless of how fair things appear. Perhaps because of this, adding fundamentals to MEME projects has become a new development model. Most longer-cycle projects like Desci and AIMEME adopt this approach. Yet for now, fleeting phenomena still dominate—'the faster you move, the better you survive' continues to gain credibility.

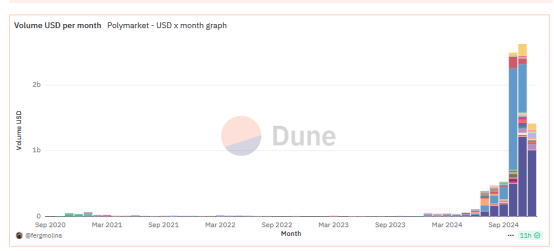

Meanwhile, influenced by the U.S. election, another legendary application surfaced. Polymarket surpassed all existing betting platforms, gaining fame in prediction markets with high accuracy. In October alone, Polymarket received 35 million website visits—twice that of popular sites like FanDuel—and monthly trading volume surged from $40 million in April to $2.5 billion. Broad user reach and real demand equate to clear value propositions—no wonder Vitalik praised it highly. The only regret is that it hasn’t yet achieved large-scale conversion of crypto users. Nevertheless, the new hybrid of media and gambling is clearly on its way.

As the year drew to a close, large models transitioned from technology to application, entering a fiercely competitive phase. After drifting through Web3 headlines for a year, AI finally re-emerged as the year’s dark horse. MEMEs led the charge—Truth Terminal brought quick wins with GOAT, ACT, and Fartcoin, reviving stories of hundredfold returns and sparking a frenzy around AI Agents, once a niche application. Currently, nearly all major institutions view AI Agents favorably, seeing them as the second breakout sector after DeFi. However, infrastructure remains immature, applications are mostly surface-level (MEMEs, bots), and deep integration between AI and blockchain is rare. But novelty means opportunity—cyber-style coin speculation awaits further observation.

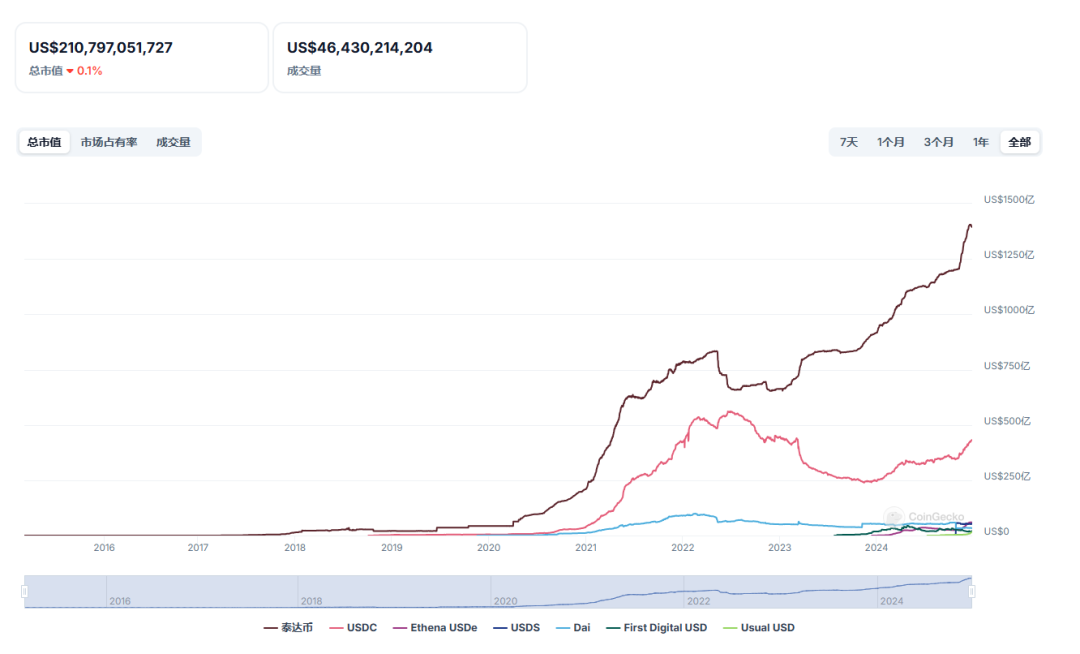

On another front, when examining core drivers behind this bull run, PayFi—seamlessly bridging traditional finance and Web3—stands out as paramount. Stablecoins and RWA are prime examples. This year, stablecoins began showing signs of the long-anticipated mass adoption—not only growing rapidly within crypto but also gaining ground in global payments and remittances. Regions such as Sub-Saharan Africa, Latin America, and Eastern Europe started bypassing traditional banking systems, adopting stablecoins directly for transactions, with scale increasing over 40% year-on-year. Circulating stablecoin value now exceeds $210 billion—significantly higher than the tens of billions in 2020. Over 20 million addresses transact in stablecoins monthly on public blockchains. In the first half of 2024 alone, stablecoin settlement value surpassed $2.6 trillion. Among new products, Ethena stood out as the brightest star in the stablecoin space this year, further fueling the yield-bearing stablecoin trend and becoming a key revenue driver for AAVE. RWA, meanwhile, exploded after BlackRock officially entered the space. Three years ago valued at under $2 billion, RWA reached $14 billion this year, spanning lending, real estate, stablecoins, and bonds.

In fact, PayFi’s development aligns perfectly with market dynamics. Precisely because internal market growth has hit a bottleneck, the institutional mainstream market—as a source of incremental growth—is now at the beginning of a new cycle. To seek new expansion, PayFi has thus entered a critical phase. Notably, due to its integration with traditional finance, this sector is also the most favored Web3 area by government bodies. For example, Hong Kong has already listed stablecoins and RWA as key development areas for next year.

Certainly, despite appearances of optimism, it cannot be denied that under nearly two years of macro tightening and industry downturn, the crypto space underwent an exceptionally harsh stress test. Innovation remained elusive, internal conflicts intensified, M&A activities surged, and reduced liquidity accelerated path divergence—leading to a Bitcoin-centric environment that continuously siphoned value from other cryptos. Altcoin markets spent much of the year in what felt like “garbage time.” Su Zhu’s saying, “This bull market has no alts,” was repeatedly proven and disproven—until a late-year rebound driven by Wall Street attention signaled the arrival of alt season. For now, path divergence will persist in the short term and likely intensify.

02 Outlook for 2025: New Cycle, New Applications, New Directions

As we turn our gaze to the present, the New Year’s bell is about to ring. Looking ahead to 2025, with the Trump administration ushering in a new era for crypto, well-capitalized institutions are eager to act. So far, over 15 institutions have released their market forecasts for next year.

Regarding price predictions, all institutions express bullish views on Bitcoin, with six forecasting peak prices between $150,000 and $200,000. VanEck and Dragonfly expect Bitcoin to reach $150,000, while Presto Research, Bitwise, and Bitcoin Suisse predict $200,000. Under strategic reserve scenarios, Unstoppable Domains and Bitwise even suggest figures up to $500,000 or higher. For other cryptos, VanEck, Bitwise, and Presto Research offered projections: ETH around $6,000–$7,000, Solana between $500–$750, and SUI potentially rising to $10. Presto and Forbes estimate total crypto market cap could reach $7.5–8 trillion, while Bitcoin Suisse believes altcoin market cap could grow fivefold.

These price forecasts come with solid reasoning. Almost all institutions believe the U.S. economy will achieve a soft landing next year, improving macro conditions, and that crypto regulation will loosen accordingly. Over five institutions hold positive views on Bitcoin strategic reserves, expecting at least one sovereign nation and numerous public companies to add Bitcoin to their reserves. All agree that increased ETF inflows will be an objective reality.

When it comes to specific sectors, stablecoins, tokenized assets, and AI are the top focuses for institutions. On stablecoins, VanEck predicts settlement volume will hit $300 billion next year, while Bitwise anticipates $400 billion driven by faster legislation, accelerating fintech adoption, and global settlement demand. Blockworks Mippo is even more optimistic, estimating $450 billion. A16z believes enterprises will increasingly accept stablecoins as payment, and Coinbase noted in its report that the next wave of true crypto adoption (the killer app) may stem from stablecoins and payments.

For tokenized assets, A16z, VanEck, Coinbase, Bitwise, Bitcoin Suisse, and Framework all express optimism. A16z suggests that as blockchain infrastructure costs decline, tokenization of non-traditional assets will become a new revenue stream, further driving decentralized economies. VanEck provides concrete numbers, predicting tokenized securities will exceed $50 billion—a figure aligned with Bitwise’s forecast. Messari offers a differentiated view based on practicality: as interest rates fall, tokenized government bonds may face headwinds, but idle on-chain funds could gain more traction, shifting focus from traditional financial assets to on-chain opportunities.

On AI, A16z—which has heavily invested in the field—remains highly optimistic about the convergence of AI and crypto. It believes AI agents will gain significant autonomy, capable of owning dedicated wallets and acting as independent entities, with decentralized autonomous chatbots becoming the first truly autonomous high-value network participants. Coinbase agrees, stating that AI agents equipped with crypto wallets represent the frontier of disruption. VanEck expects over 1 million on-chain activities by AI agents, while Robot Ventures forecasts at least a fivefold increase in market cap for AI agent-related tokens. Dragonfly acknowledges token appreciation but maintains a relatively conservative stance on real-world applications, suggesting underlying protocols may see limited use.

Bitwise and Defiprime highlighted core use cases: Bitwise believes AI Agents will drive the next MEME explosion, while Defiprime sees DeFi as the ideal integration scenario.Messari outlines three specific directions for AI-crypto synergy: first, novel AI casinos like Bittensor and Dynamic TAO; second, blockchain technology applied to fine-tuning small and specialized AI models; third, the fusion of AI agents with MEMEs.

Other predictions vary: YBB believes DeFi revival will be the 2025 theme, Robot Ventures expects consolidation in the app-chain and L2 space, Messari forecasts ZK technology adoption across nearly all infrastructure protocols by 2025, DEPIN could generate eight- to nine-digit revenues by then, VanEck and Bitcoin Suisse anticipate NFTs making a comeback, and so on. Given space constraints, we won’t list every detail here.

03 Conclusion: Where Should Investors Go?

Although viewpoints differ slightly and nuances exist across sub-sectors, it’s clear that all institutions hold optimistic and positive expectations for next year—whether in price appreciation, ecosystem expansion, or mainstream adoption, all are expected to scale new heights in 2025.

Clearly, from a pricing perspective, upward movement in major cryptocurrencies is inevitable, especially in Q1 2025, which will likely be packed with policy tailwinds. Altcoin markets will continue diverging—compliant altcoins influenced by ETF narratives will attract capital inflows and sustain narratives, while others slowly contract. If macro liquidity tightens, risks for altcoins will become increasingly pronounced.

From an industry standpoint, dominant Layer 1 chains still hold ecological advantages, but challenges from emerging blockchains are unavoidable. Ethereum’s value capture and narrative will continue evolving, though optimism lies in external capital inflows possibly alleviating pressure. Technological scaling and broader adoption of account abstraction will be key breakthroughs for Ethereum in 2025. Solana retains growth momentum backed by capital influence, but its heavy reliance on MEMEs poses hidden risks. Competition with Base will intensify. Additionally, new entrants like Monad and Berachain are expected to join the race.

The shift from infrastructure to applications defines the future trajectory. Consumer-facing apps will be the focus in coming years, with app-chains and chain abstraction likely becoming primary methods for DApp development. Across sectors, DeFi revival is now consensus—but currently concentrated on AAVE. On the centralized side, payments remain the focal point, with Hyperliquid and Ethena warranting close attention.

The speculative wave around MEMEs will likely persist in the short term, albeit at a slower pace, particularly amid alt season. However, thematic areas like Politifi still offer longer narratives. That said, MEME-related infrastructure is expected to mature, enhancing user experience, lowering barriers, and accelerating institutionalization. Notably, innovative token launch mechanisms will always spark new waves of excitement.

Given that incremental markets come from institutions, sectors favored by institutional players—stablecoins, AI, RWA, DePin—are poised to accelerate. Moreover, in times of tight liquidity, any on-chain liquidity tools or protocols enabling leverage will likely gain favor.

A new cycle is approaching. For investors, letting go of the old and embracing the new—identifying the cycle, adapting to it, conducting deep research, and actively participating—is the only viable path forward.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News