Is the Federal Reserve prohibited from owning Bitcoin?

TechFlow Selected TechFlow Selected

Is the Federal Reserve prohibited from owning Bitcoin?

Rate cut implemented, yet U.S. major indices and crypto market all see sharp pullbacks.

By Liu Jiaolian

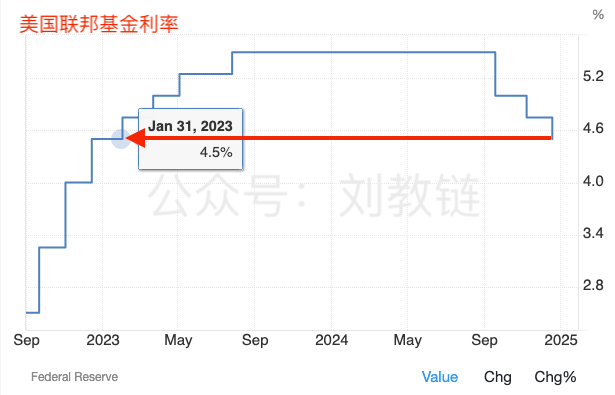

Overnight into this morning, the Federal Reserve concluded its December monetary policy meeting as scheduled. The outcome was in line with market expectations: another 25 basis point rate cut. This result surprised some who had speculated that the Fed might pause its easing cycle. Thus far, since the second half of 2024, the Fed has cut interest rates three times cumulatively, lowering the federal funds rate by 100 basis points—or 1%—from 5.5% down to 4.5%.

This brings U.S. interest rates back to the level seen at the beginning of 2023.

Rate cuts implemented. Yet both Wall Street’s three major indices and the crypto market saw sharp pullbacks. Why? Because an expected rate cut had already been priced in well ahead of time. What followed was a classic case of “sell the news”—a fleeting moment of triumph, like red sunsets against enduring green mountains.

Of course, the pullback was also partly due to the Fed Chair's comment that policy adjustments next year may proceed with greater caution. This tempered some investors’ more aggressive hopes for rapid and continuous rate cuts in 2025.

In this era of global radicalism during a Kondratiev winter, any deviation from extremism is often labeled as conservatism. In such a climate, not cutting rates aggressively enough is perceived as not cutting them at all.

If you stand as a moderate in the center, those on your right will accuse you of being too far left, while those on your left will condemn you for being too far right. You end up pleasing no one.

Why does Chinese philosophy emphasize the Doctrine of the Mean? It’s precisely because societies tend toward "M-shaped" polarization—the middle ground is where true courage lies. Only the brave dare to stand in the center; only the strong can survive there without being torn apart.

Black or white, left or right, heaven or hell—one thought turns Buddha into demon. Today it's blockchain revolution, tomorrow tulip mania.

Pretending to be divine is easy. To become a truly upright person, standing tall between heaven and earth, is hard. Mindlessly pandering to public sentiment through blind praise or trashing is easy. Objectively and impartially recognizing new phenomena and seizing historical opportunities is difficult.

You don’t appreciate her value simply because you haven't spent real time with her. Once you do—and especially once you've done so for long—you'll understand what makes her special.

A segment of Powell’s Q&A session at the early-morning press conference went viral.

A reporter asked about the possibility of a national Bitcoin (BTC) strategic reserve in the United States.

Powell responded: "The Federal Reserve is not permitted to own Bitcoin. We are not seeking changes to that law."

His statement accurately reflects the current legal reality.

But the remark is broad, general, and vague. Let's unpack it carefully.

First, how does Powell view the nature of BTC?

Recall from Jiaolian Insight’s article dated December 5, 2024, "Bitcoin Surge Breaks $100K", where Powell previously stated publicly that, in his view, BTC resembles gold more than anything else. He said, "It is not a competitor to the dollar, but rather a competitor to gold."

In other words, he sees BTC as a physical asset.

Can the Federal Reserve directly "own" physical assets? Clearly not.

Take gold, for example. The U.S. gold reserves are legally owned by the U.S. Department of the Treasury. Actual storage and custody are distributed across various depositories within the country (such as the Federal Reserve Bank of New York). Under the Gold Reserve Act of 1934, the Treasury issues gold certificates to represent the value of its gold holdings. These gold certificates, issued by the U.S. Treasury, serve as the legal proof of gold reserves.

Can the Federal Reserve own physical gold? No. The Fed can only hold gold certificates as financial assets.

Even holding gold certificates requires acting within legal boundaries. The key lies in properly recording the financial value of these assets on the Fed’s balance sheet.

According to the Federal Reserve Act of 1913, the Fed may include gold certificates on its balance sheet as part of its reserve assets. On the Fed’s books, gold certificates are recorded at face value, representing the Treasury’s pledged gold worth.

Accounting-wise, the valuation of gold reserves follows the International Monetary Fund Agreement Act of 1973, which fixes the price at $42.22 per ounce—regardless of market prices. Jiaolian discussed this pricing mechanism in detail in the November 14, 2023 article "How Much Gold Does the U.S. Really Hold?", so we won’t repeat it here.

However, this method isn’t set in stone. For instance, China’s central bank revalues its gold holdings based on market prices. See Jiaolian’s October 31, 2023 article "The PBOC’s ‘Secret’" for details.

With this background, we now need to examine two critical questions:

First: Can the incoming U.S. president, using executive authority alone, authorize the Treasury to hold BTC (‘big cake’) and issue “cake vouchers” (analogous to gold certificates)?

Second: Can the Federal Reserve, without amending the Federal Reserve Act of 1913, exercise emergency discretion to include such “cake vouchers” on its balance sheet?

Regarding the first question, U.S. President John F. Kennedy, the 35th president, provided a precedent.

On June 4, 1963, President Kennedy signed Executive Order 11110. This order delegated to the U.S. Treasury the authority under the Silver Purchase Act of 1920 to issue silver certificates backed by the Treasury’s silver reserves, in the Treasury’s own name.

Fundamentally, silver certificates were a form of U.S. currency exchangeable for physical silver at par value.

On November 22, 1963, President Kennedy was assassinated. See Jiaolian Insight’s November 8, 2024 article "Fed Cuts Rates as Expected, Powell Rejects Resignation".

The radio seems to play a female singer’s voice:

“Dare you dare / To love me the way you once said? /

Dare you dare / To go crazy for love like I do?

Dare you dare / To love me the way you once said? /

To go crazy for love like I do— / What would you say?”

As for the second question, the Federal Reserve itself has already demonstrated a path forward.

During the 2008 financial crisis, the Fed implemented a series of unconventional monetary policies, including purchasing MBS and other financial assets to inject liquidity and support the economy. This policy became known as Quantitative Easing (QE).

Section 14(2) of the Federal Reserve Act of 1913 allows the Fed to buy government bonds (like U.S. Treasuries) to manage money supply and stabilize the economy. However, the Act does not explicitly authorize the purchase of private-sector assets unrelated to the government, such as mortgage-backed securities (MBS).

The core issue is: Is the Fed’s power public or private?

Public authority operates under the principle that “what is not permitted is forbidden.” If the law doesn’t clearly allow the Fed to directly purchase MBS, then doing so could be considered illegal.

Yet the Federal Reserve, serving as America’s central bank and effectively the world’s central banker, exists as a unique anomaly. In reality, the Fed is a private institution, not a public agency. And for private rights, the principle is “what is not prohibited is allowed.”

Hence, legal interpretation becomes flexible.

The usual justification goes like this:

One, the Federal Reserve Act of 1913 does not explicitly prohibit the Fed from buying certain types of assets.

Two, the Fed invoked other laws to justify its emergency actions, including the Emergency Banking Act of 1932 and the Financial Stability Act of 2008. These statutes empowered the Fed to take extraordinary monetary measures under specific emergency conditions, providing a legal basis for MBS purchases during the crisis.

In sum, the Fed argued that buying MBS was necessary for monetary policy and financial stability, justified as an emergency response to a systemic crisis. Therefore, although these actions didn’t strictly comply with the letter of the 1913 Act, subsequent legislative backing provided a de facto legal foundation.

In practice, U.S. courts have never ruled definitively that these actions violated the Federal Reserve Act of 1913, largely treating them as legitimate crisis responses.

Thus, despite existing in a legal gray area, these measures were not deemed outright violations of the 1913 Act.

As repeatedly noted in Jiaolian Insider reports from May 5, 2024, "Insider Report 5.5: Accidentally Sent Away 1,155 Bitcoins", and July 1, 2024, "Insider Report 7.1: The Unstoppable Rebound", the Fed has quietly been replacing its “gray” MBS positions with clean, legal U.S. Treasury holdings.

They’ve been wiping this mess since 2008—and still aren’t finished.

So even without formally changing laws, the Fed can flexibly interpret its own powers to justify what it does or doesn’t do.

Finally, TechFlow notes that central banks around the world belong to an international coordination body called the BIS (Bank for International Settlements), a pillar of the post-WWII financial order.

BIS membership consists primarily of global central banks, currently totaling around 60 members, including key institutions like the U.S. Federal Reserve, the European Central Bank, and China’s People’s Bank of China. Founded in 1930 and headquartered in Basel, Switzerland, it is often called “the central bank of central banks.”

In 1974, the BIS established the Basel Committee on Banking Supervision (BCBS), tasked with setting international regulatory standards and guidelines for the banking sector.

The BCBS focuses on establishing global norms related to bank capital adequacy, risk management, and supervision—especially regulations concerning capital ratios, liquidity requirements, and risk-weighted assets. It regularly issues standards and recommendations for adoption by national regulators worldwide, aiming to ensure the health and stability of the global banking system.

In 1988, the Basel Committee introduced Basel I, the first global standardization of bank capital requirements.

In 2004, it released Basel II, further refining and expanding Basel I.

In 2010, following the global financial crisis, the committee launched Basel III, designed to improve the quality of bank capital and strengthen systemic resilience during crises.

Clearly, the BIS and the Basel Committee play pivotal roles in global banking regulation. The Committee, operating under the BIS, develops international standards, while the Basel Accords (I, II, III) embody those standards in practice.

Central banks globally—including the Fed—typically must work through the BIS and the Basel framework to establish standards before incorporating new asset classes onto their balance sheets—that is, before taking any risk exposure to a given asset.

The Basel Accords are called “accords,” not laws, because compliance relies on member self-discipline rather than enforcement by coercive state apparatus.

Interestingly, as early as December 2022, the BIS published a report indicating that "Central Banks Will Be Allowed to Allocate Up to 2% of Bitcoin Starting in 2025" (Jiaolian article, December 17, 2023).

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News