Standard Chartered: Tokenization will be a game-changer for global trade

TechFlow Selected TechFlow Selected

Standard Chartered: Tokenization will be a game-changer for global trade

The overall demand for real-world asset tokenization is expected to reach $30.1 trillion by 2034.

Authors: Standard Chartered Bank, Synpulse

Translated by: Web3 Lawyer

This research report jointly authored by Standard Chartered Bank and Synpulse offers a comprehensive analysis of real-world asset tokenization in cross-border trade scenarios. The report details how tokenization will become a transformative force in global trade, converting trade assets into transferable instruments that provide investors with unprecedented liquidity, divisibility, and accessibility.

Unlike traditional financial assets that are highly volatile due to macroeconomic factors, trade assets differ significantly. While trade is closely linked to the economy, and economic downturns can impact bank lending, the massive trade finance gap still presents strong investment opportunities. Even during periods of economic slowdown, small and medium-sized enterprises (SMEs) continue to require substantial financing, creating consistent investment prospects. In this sense, trade assets demonstrate resilience against global economic recessions.

Moreover, due to their relatively short cycles, low default rates, and high funding demands, trade assets are particularly suitable as underlying assets for tokenization. Additionally, tokenizing trade assets brings numerous benefits to all participants and processes involved in complex global trade operations—specifically in 1) cross-border payment settlements, 2) financing needs among trading parties, and 3) leveraging smart contracts to enhance efficiency, reduce complexity, and increase transparency.

Standard Chartered forecasts that by 2034, total demand for real-world asset tokenization will reach $30.1 trillion, with trade assets ranking among the top three tokenized asset classes and accounting for 16% of the overall tokenized market within the next decade.

Therefore, we have translated this report to serve as a reference for market participants and investors. It explores the transformative power of trade asset tokenization and explains why now is the ideal time to adopt and scale it. The report also examines four key benefits of embracing tokenization and outlines actionable steps for investors, banks, governments, and regulators to seize this opportunity and shape the next chapter of finance.

Enjoy the read:

Real-World Asset Tokenization: A Game Changer for Global Trade

Over the past year, we have witnessed rapid advancements in tokenization, reflecting a significant shift toward more accessible, efficient, and inclusive financial systems. In particular, the tokenization of trade assets represents both a transformation in our understanding of value and ownership and a fundamental change in investment and exchange mechanisms.

Through Standard Chartered’s successful pilot under Project Guardian, led by the Monetary Authority of Singapore (MAS), the feasibility of an innovative "originate-to-distribute" structure using tokenization has been demonstrated, showcasing potential opportunities for investor participation in financing real-world economic activities.

Building on this vision, Standard Chartered pioneered an initial token offering platform for real-world assets. They successfully simulated the issuance of $500 million in asset-backed securities (ABS) tokens backed by trade finance assets on Ethereum’s public blockchain.

This pilot demonstrated how open and interoperable networks can practically facilitate access to decentralized applications, drive innovation, and promote growth within the digital asset ecosystem. It proved the real-world application potential of blockchain technology in finance—particularly in enhancing asset liquidity, reducing transaction costs, improving market access, and increasing transparency. Through tokenization, trade assets become more efficiently accessible and tradable by global investors, transforming them into transferable instruments and unlocking previously unimaginable levels of liquidity, divisibility, and accessibility. This not only offers investors new opportunities to balance portfolios with digitally represented assets tied to verifiable intrinsic value but also helps close the global $2.5 trillion trade finance gap.

1. What Is Asset Tokenization?

As the financial world undergoes rapid digitalization, digital assets stand at the forefront, revolutionizing how we perceive and exchange value. The integration of traditional finance with innovative blockchain technology is ushering in a new era of digital finance, fundamentally reshaping our concepts of value and ownership.

Prior to 2009, the idea of transferring value through digital assets was inconceivable. Digital value exchanges still relied heavily on intermediaries acting as gatekeepers, resulting in inefficient processes. Although there remains debate within the financial industry over the precise definition of digital assets, their pervasive presence in our technology-driven lives is undeniable. From information-rich digital files we use daily to content consumed on social media, they permeate every aspect of modern existence.

The introduction of blockchain technology changed the game entirely. It is revolutionizing financial markets. What once seemed impossible is now becoming reality, with tokenization emerging as a key driver expanding the digital asset market—from niche and experimental to widely accepted and mainstream.

At its core, “tokenization” refers to the process of issuing digital representations of traditional assets in the form of tokens on distributed ledgers.

These tokens function as digital certificates of ownership, enhancing operational efficiency and automation. Notably, tokenization is closely related to fractionalization—the ability to divide a single asset into smaller, transferable units. But the most revolutionary aspect lies in how tokenization expands access to new asset classes and improves financial market infrastructure, opening doors to innovative applications in decentralized finance (DeFi) and entirely new business models.

2. Evolution of Tokenization

The roots of tokenization trace back to the early 1990s. Real Estate Investment Trusts (REITs) and Exchange-Traded Funds (ETFs) were among the first vehicles enabling fractional ownership of physical assets, allowing investors to own portions of buildings or commodities.

Then came Bitcoin in 2009—a cryptocurrency that challenged the conventional role of third-party intermediaries. This sparked a revolution, followed by Ethereum's emergence in 2015. As a pioneering software platform powered by blockchain technology, Ethereum introduced smart contracts capable of supporting the tokenization of any asset. It laid the foundation for thousands of tokens representing various assets—including cryptocurrencies, utility tokens, security tokens, and even non-fungible tokens (NFTs)—demonstrating the vast possibilities of tokenization in representing both digital and physical items.

In subsequent years, new phenomena emerged: Initial Exchange Offerings (IEOs) and Initial Coin Offerings (ICOs). In 2018, the U.S. Securities and Exchange Commission (SEC) coined the term “Security Token Offering (STO),” paving the way for regulated tokenized offerings and driving the development of compliance-ready solutions.

These developments set the stage for real-world asset tokenization to take center stage. They continue to act as catalysts for transformation and technological advancement in financial services, enabling continuous innovation. Financial institutions are increasingly exploring the potential of tokenization, driven by client demand and the opportunities it presents for banks and the global digital economy. More and more financial firms are seeking ways to integrate digital assets into their service offerings.

A prime example is Project Guardian—an industry-wide collaboration between the Monetary Authority of Singapore (MAS) and leading industry players aimed at testing the feasibility of asset tokenization with DeFi applications. These industry pilots will further reveal the opportunities and risks brought about by rapid innovation in digital finance tokenization.

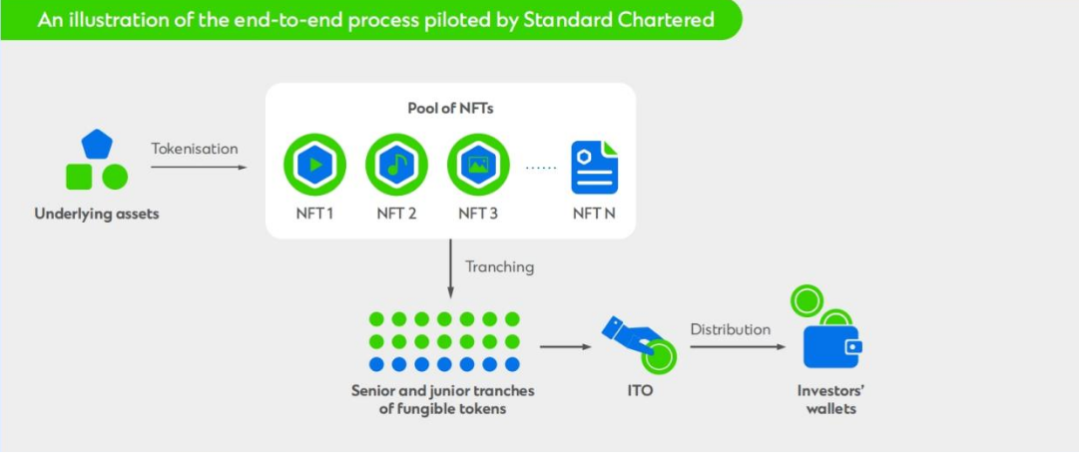

Case A: Project Guardian – Asset-Backed Securities (ABS) Tokenization Pilot

Standard Chartered demonstrated a bold vision in Project Guardian: advancing safer and more efficient financial networks using blockchain. This MAS-led initiative brought together industry leaders who conducted market case studies and designed blueprints for future market infrastructure harnessing the innovative potential of blockchain and DeFi.

Standard Chartered took this vision further by launching a token issuance platform for real-world assets, successfully simulating the issuance of $500 million in ABS tokens backed by trade finance assets on Ethereum’s public blockchain. Through this effort, the bank tested the end-to-end process from origination to distribution, including simulations of default scenarios.

-

Tokenization: Trade finance receivables were tokenized in the form of non-fungible tokens (NFTs).

-

Risk-Based Allocation: These NFTs were structured into senior and junior tranches based on expected risk and return profiles, ensuring strict cash flow allocation.

-

Fungible Token Creation: Two types of fungible tokens (FTs) were created based on the underlying NFTs and structural design. Senior FTs offered fixed yields, while junior FTs provided excess spread.

-

Distribution and Access: Finally, these tokens were distributed to investors via an Initial Token Offering (ITO).

The success of the Project Guardian pilot demonstrated how open and interoperable blockchain networks can be used in practice to enable access to decentralized applications, stimulate innovation, and foster growth in the digital asset ecosystem. Use cases can expand to include tokenization of financial assets such as fixed income, foreign exchange, and asset management products, enabling seamless cross-border trading, distribution, and settlement.

Additionally, by tokenizing financing needs in cross-border trade scenarios, this new category of digital assets becomes accessible to a broader investor base, helping improve liquidity in the trade finance market.

3. Beyond Trade Asset Tokenization: What Else Can We See?

Tokenization is not merely about creating new ways to invest in digital assets or bringing much-needed transparency and efficiency to trade finance—it goes deeper, simplifying the complexities of supply chain finance.

Credit Transmission: Typically, trade finance is only available to established Tier-1 suppliers, leaving “deep-tier” suppliers—smaller SMEs often lacking scale—excluded. Through tokenization, SMEs can leverage the credit ratings of anchor buyers, thereby enhancing overall supply chain resilience and liquidity.

Liquidity Creation: Tokenization is frequently praised for its potential to unlock value, especially in inefficient and illiquid markets. There is growing consensus that investors prefer tokenized assets due to lower transaction costs and enhanced liquidity. For institutional providers, the appeal lies in accessing new capital pools, improving liquidity, and streamlining operational efficiency.

Beyond this, Standard Chartered believes the true transformative power of tokenization is far greater. The next three years will be pivotal for tokenization, with new asset classes rapidly being tokenized and trade finance assets taking center stage. Industry development is reaching a new level where shared utilities yield greater returns than isolated efforts.

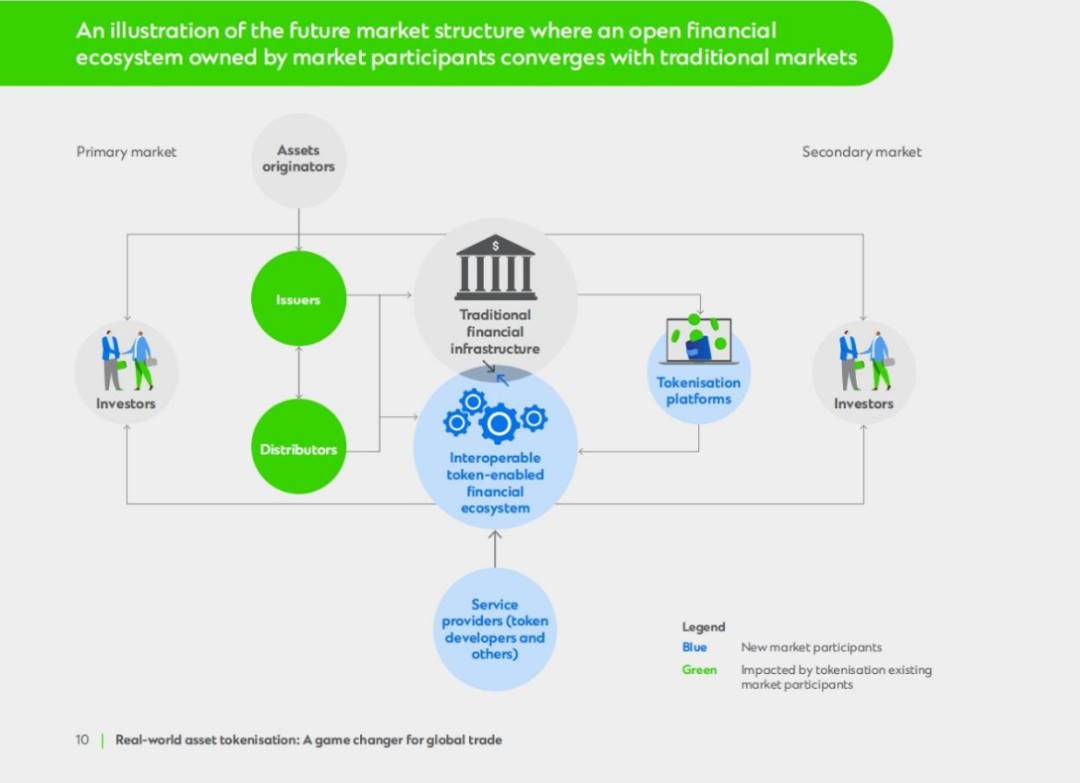

To provide access to new asset classes, banks play a crucial role in maintaining trust and bridging existing traditional financial markets with newer, more open, token-based market infrastructures. Maintaining trust involves verifying issuer and investor identities, conducting KYC/AML checks, and issuing credentials to participate in this new interoperable financial ecosystem.

Standard Chartered envisions a future where traditional and tokenized markets coexist and eventually converge, necessitating an open, permissioned, multi-asset, and multi-currency digital asset infrastructure to complement traditional markets. Compared to closed-loop systems of the past, ownership and utility would be shared among a wider range of market participants, balancing inclusivity with security. Such infrastructure could not only boost efficiency and innovation but also address current industry pain points like redundant investments and fragmented, siloed development that hinder growth and collaboration.

4. What Drives the Tokenization of Trade Assets?

Current macroeconomic and banking conditions serve as catalysts for adoption, as tokenization brings unprecedented liquidity, divisibility, and accessibility to asset classes long considered complex.

4.1 SMEs: Unlocking Trillions in Opportunities to Close the Trade Finance Gap

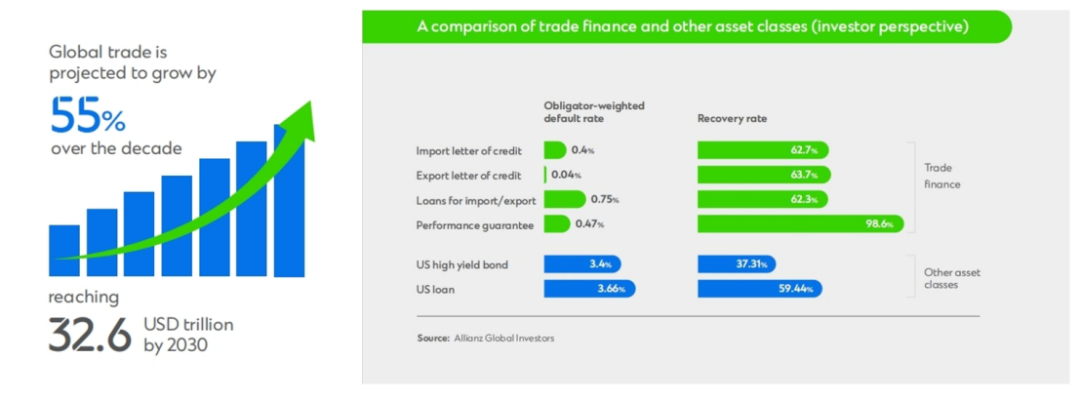

Standard Chartered projects global trade to grow 55% over the next decade, reaching $32.6 trillion by 2030. Digitization, expanding global trade, intensified competition, and improved inventory management are key drivers. However, a significant gap persists between trade finance demand and supply—especially for SMEs in developing countries.

The trade finance gap has surged—from $1.7 trillion in 2020 to $2.5 trillion in 2023, a 47% increase. This marks the largest single-period rise since the metric was introduced, driven by factors including COVID-19, economic hardship, and political instability, making it harder for banks to approve trade financing.

Furthermore, the International Finance Corporation (IFC) estimates that 65 million enterprises in developing countries—40% of formal micro, small, and medium-sized enterprises (MSMEs)—have unmet financing needs. While the challenges faced by SMEs are widely recognized, one critical segment remains overlooked: the “missing middle.”

The “missing middle” or mid-market enterprises (SMEs) fall between large investment-grade corporations and small retail businesses. These companies are particularly active across fast-growing regions like the Middle East, Asia, and Africa. They represent a vast, untapped market offering significant investment opportunities.

This investment opportunity is also recession-resilient. Although trade is closely tied to the economy, and recessions affect bank loans, the large trade finance gap presents excellent entry opportunities for investors. Even during economic slowdowns, SMEs continue to require substantial financing, generating sustained investment prospects.

Notably, according to Asian Development Bank data, the $2.5 trillion global trade finance gap accounts for 10% of all trade exports. With current trade finance covering 80% of global exports, another 10% may represent an additional, undisclosed financing gap—either because firms do not seek such funding or cannot access it. This suggests the total undiscovered trade finance gap could reach a potential $5 trillion opportunity.

4.2 An Underserved Market with Attractive Returns

Trade finance assets are attractive yet underinvested. They deliver strong risk-adjusted returns and possess unique characteristics:

-

Enables Risk Diversification: Trade assets typically have short maturities and are self-liquidating, making them low-risk investments with relatively low correlation to stock and bond markets. This makes them a more stable asset class while still delivering solid risk-adjusted returns.

-

Broad Investment Scope: A wide variety of trade assets are available to meet specific investor risk preferences. Combined with exposure to hard-to-reach emerging and frontier markets like Ghana, Côte d'Ivoire, Bangladesh, or Saudi Arabia, this asset class caters to diverse investor needs.

-

Low Default Risk and High Recovery Rates: Most importantly, trade finance assets boast an impressive track record. Compared to public credit, trade finance has lower default rates and higher recovery rates upon default, indicating superior risk-adjusted returns relative to other debt instruments.

Despite underinvestment due to lack of awareness, inconsistent pricing, opacity, and operational intensity, tokenization can help resolve these issues.

4.3 Banks Are Incentivized to Adopt Tokenization and Leverage Blockchain-Based Originate-to-Distribute Models to Unlock Capital in Frontier Markets

Basel IV is a comprehensive set of measures that will significantly impact how banks calculate risk-weighted assets. Although full implementation is expected by 2025, banks must already develop growth strategies under Basel IV by modernizing their distribution models.

Through blockchain-based originate-to-distribute models, banks can derecognize assets from their balance sheets, reducing regulatory capital requirements and promoting efficient asset origination. By distributing trade finance instruments to capital markets and emerging digital asset markets, banks can leverage tokenization. This “digital originate-to-distribute” strategy for trade finance assets enables banks to improve return on equity, diversify funding sources, and increase net interest income.

The global trade finance market is vast and well-positioned for tokenization. Most interbank trade finance assets can be tokenized and converted into digital tokens, enabling global investors seeking returns to participate directly.

4.4 Growing Demand Fuels Expansion

According to EY Parthenon, demand for tokenized investments will surge: by 2024, 69% of buy-side firms plan to invest in tokenized assets, up from just 10% in 2023. Moreover, investors intend to allocate 6% of their portfolios to tokenized assets in 2024, rising to 9% by 2027. Tokenization is not a passing trend—it reflects a fundamental shift in investor preferences.

However, market supply remains nascent. By early 2024, the total value of real-world asset tokenization (excluding stablecoins) stood at approximately $5 billion, primarily involving commodities, private credit, and U.S. Treasuries. In contrast, Synpulse estimates the accessible market size—including the trade finance gap—could reach $14 trillion.

Based on current trends, Standard Chartered forecasts that overall demand for real-world asset tokenization will reach $30.1 trillion by 2034. Trade finance assets will rank among the top three tokenized asset classes and account for 16% of the total tokenized market over the next decade. Given that demand is likely to outpace supply in the coming years, there is strong potential to help bridge the current $2.5 trillion trade finance gap.

5. Four Benefits of Embracing Tokenization

Asset tokenization has the potential to transform the financial landscape by increasing liquidity, transparency, and accessibility. While promising for all market participants, realizing its full potential requires collaborative efforts across stakeholders.

Trade finance drives the global economy, yet traditionally, these assets were mainly sold to banks. Tokenization opens doors to a broader investor base, ushering in a new era of growth and efficiency.

5.1 Improved Market Access

Today, institutional investors are eager to enter new, fast-growing markets. Emerging markets offer attractive diversification opportunities. However, lack of local expertise and effective distribution networks often prevents investors from fully capitalizing on these opportunities.

This is where tokenization shines. By distributing trade finance assets via digital tokens, banks can increase net interest income and optimize capital structures, while investors, businesses, and communities reliant on trade finance benefit from improved access. Examining Standard Chartered’s early collaboration with MAS on Project Guardian highlights the transformative power of tokenization. The pilot showed how open, interoperable digital asset networks can unlock market access, allowing investors from different ecosystems to participate in the tokenized economy and paving the way for more inclusive growth.

5.2 Simplifying Trade Complexity

Due to the involvement of multiple parties and cross-border nature of global capital and goods flows, trade finance is often seen as complex. This asset class lacks standardization—ticket sizes, timelines, and underlying commodities vary widely, making large-scale investment difficult.

Tokenization provides a platform to address this complexity.

Tokenization is more than just a new investment method; it is an enabler of deep-tier financing. Traditionally, trade finance is limited to mature Tier-1 suppliers, excluding “deep-tier” suppliers. Token-based deep-tier supply chain financing can eliminate this complexity.

Beyond bringing much-needed transparency and efficiency to trade finance, tokenization enhances overall supply chain resilience and liquidity by enabling SMEs to rely on the credit ratings of anchor buyers.

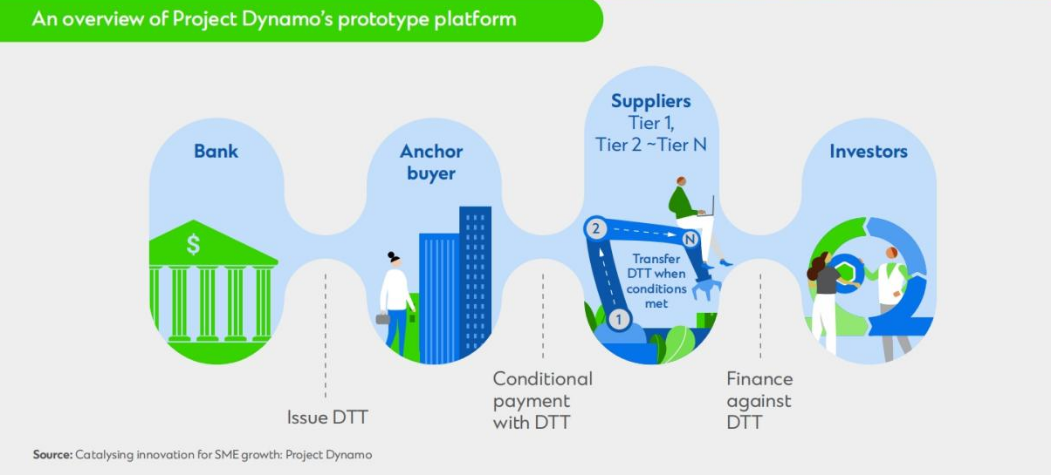

Case B: Project Dynamo – Using Digital Trade Tokens to Address Trade Complexity

Project Dynamo, a collaboration between Standard Chartered, the BIS Innovation Hub Hong Kong Centre, the Hong Kong Monetary Authority, and technology firms, exemplifies how digital trade tokens can simplify complex trade processes.

This joint effort developed a prototype platform where major buyers use tokens to make programmable payments to suppliers across their entire supply chain. Smart contract technology automatically executes and redeems these tokens based on specific events—such as triggering eBL or ESG conditions—enabling efficient and transparent trade workflows. Major buyers can also issue conditional payments to SME suppliers via tokens, which convert to cash only when predefined conditions (e.g., proof of delivery or electronic bill of lading) are met.

Token holders also have multiple options: they can hold, sell for financing, or use tokens as collateral for loans. Ownership transfer via tokenization gives deep-tier suppliers greater flexibility in managing capital efficiency.

The benefits extend beyond individual participants. Digital trade tokens are issued in “stablecoin” form, backed by dedicated bank funds or bank guarantees. Combined with the programmability and transferability enabled by blockchain infrastructure, institutional investors gain increased confidence in investing in SMEs and supply chain financing—areas previously deemed high-risk.

Project Dynamo is just the beginning. It lays out a blueprint to address the difficulties deep-tier suppliers face in accessing financing by offering more adaptive and efficient funding and payment mechanisms. Ultimately, it creates a new financing channel for those previously excluded from traditional financing options.

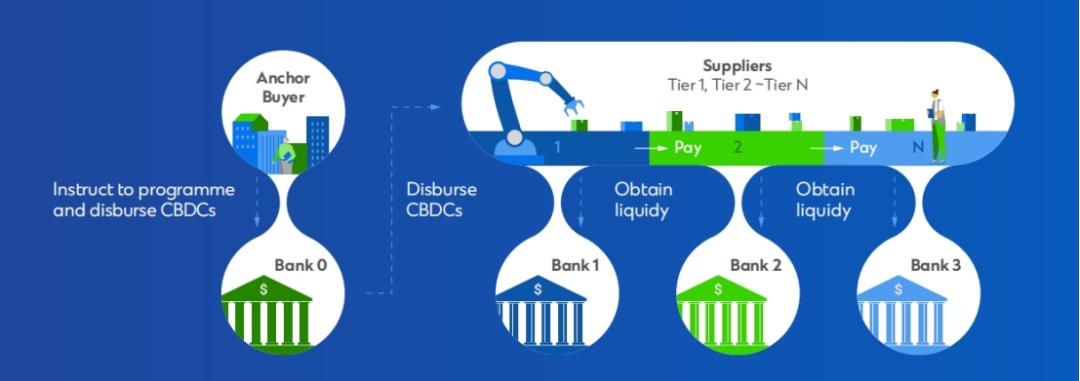

Case C: Optimizing Trade Processes and Financing Through Programmable CBDCs

While tokenization offers exciting possibilities for addressing trade ecosystem complexity, the programmability of central bank digital currencies (CBDCs) introduces another game-changing element. These digital versions of fiat currency, issued by central banks, can leverage smart contracts’ auto-execution capabilities to enable programmable transactions, further streamlining trade and supply chain financing.

Imagine a scenario: a large company with strong credit (an anchor buyer) operates a supplier network containing many SMEs with limited access to loans. With programmable CBDCs, the anchor buyer can instruct its bank to program future-payable CBDCs and distribute them directly to suppliers. Suppliers can then use these CBDCs to improve working capital efficiency or pay downstream suppliers.

This streamlined process brings multiple advantages to deep-tier supply chain financing:

-

Enhanced Flexibility: Deep-tier suppliers can use digital currency as collateral to borrow fiat, unlocking new financing options and improving operational flexibility.

-

Smoother Credit Assessment: Banks can leverage customer data collected through payment records to streamline SME credit assessments, reducing operational costs and risks associated with data collection.

-

Scalability and Transparency: CBDCs enhance scalability for SME operations, making it easier for all parties in the supply chain to report on ESG management and sustainability.

-

Stability and Confidence: On a broader scale, CBDCs strengthen stability and transparency across the entire supply chain.

In the above scenario, smart contracts play a critical role in automating payment and financing processes:

-

Pre-Defined Contract: Using smart contracts, CBDCs can be programmed to combine payment and trade information into a new trade finance instrument.

-

Purpose-Bound Payment: Deep-tier suppliers failing to meet credit criteria can use tokens as collateral to obtain financing tied to specific purposes.

-

Purpose-Bound Financing: Such CBDCs can be transferred by the anchor buyer to its suppliers, who can immediately use them to pay deep-tier suppliers.

-

Obligation Fulfilment: Once conditions in the smart contract are met, execution occurs automatically, and CBDC restrictions are lifted.

5.3 Digital Securitization

Traditional financial securitization of trade assets is effective but limited to a narrow subset of assets, such as working capital loans and import/export financing. Tokenization dramatically expands the universe of investable assets.

Given the short duration of trade assets, traditional processing is operationally inefficient. Managing trade assets requires comprehensive solutions to track underlying assets, assess performance, and determine funding and payments.

All of this can be addressed through the programmability of tokenization and smart contracts, combined with AI-driven automation to handle complexity and diversity. Automated workflows simplify and streamline data management. Each token is traceable, linked to corresponding receivables, aiding status monitoring, minimizing human error, enhancing transparency for all parties, and supporting evaluation of receivables and financing amounts.

Programmability also simplifies ownership transfer during transactions, boosting efficiency.

Since tokenization involves standardized representation of receivables, it creates a common language that makes cross-jurisdictional receivables management more straightforward.

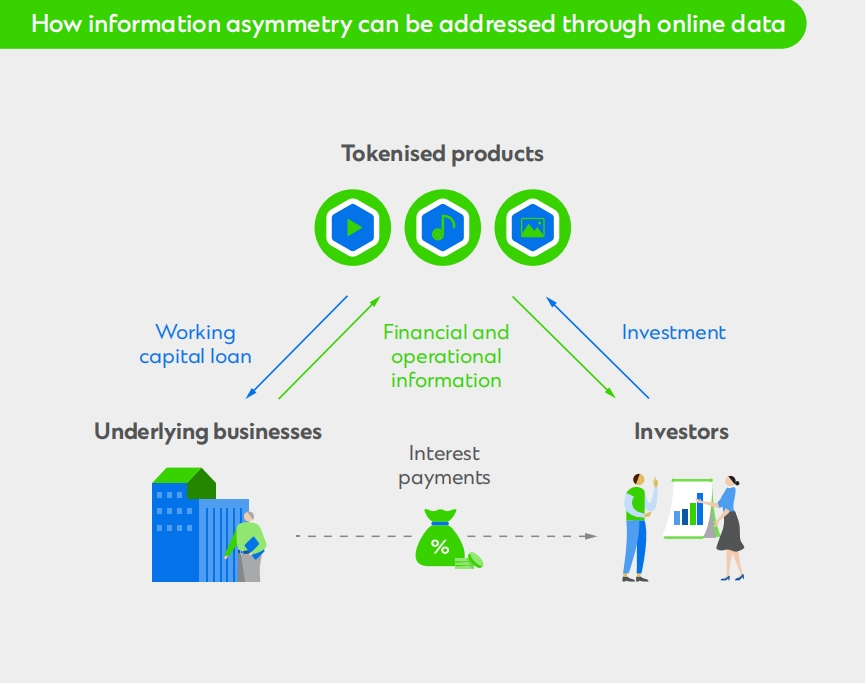

5.4 Reducing Information Asymmetry

Leveraging blockchain to trace underlying assets helps reduce information asymmetry between issuers and investors, thereby strengthening investor confidence.

Establishing listing frameworks for tokenized assets is a crucial step in encouraging adoption and building investor trust. Public disclosure of offering documents makes due diligence information more accessible to investors. Listed tokens ensure issuers maintain a certain level of transparency and meet regulatory disclosure requirements—critical for many institutional investors.

Today’s investors are more sophisticated, demanding greater transparency and control. We will soon see tokenized products emerge as a new tool to reduce information asymmetry. Beyond representing underlying assets, tokens can embed additional functionalities, such as providing online access to operational and strategic data from those assets. For example, in the tokenization of working capital loans, investors could access operational metrics of the underlying business, such as profit margins or lead counts in sales pipelines. This model has the potential to boost investment returns and elevate transparency to a new level.

6. How to Participate in the Tokenized Market?

Asset tokenization has the potential to reshape the financial landscape, offering higher liquidity, transparency, and accessibility. While it holds promise for all market participants, unlocking its full potential requires collective action from all stakeholders.

6.1 Adoption

For institutional investors seeking exposure to new asset classes or enhanced returns, tokenization offers more targeted and differentiated solutions tailored to clients’ specific risk-return profiles and liquidity preferences.

Family offices and high-net-worth individuals (HNWIs) can benefit from more effective wealth growth through diversified and transparent product structures, unlocking previously inaccessible opportunities.

To capture these investment opportunities, investors should start with a solid foundation. As this is an emerging and evolving field, understanding new risks is essential—begin with education to build expertise.

For instance, participating in pilot programs allows investors and asset managers to experiment and build confidence in allocating to tokenized assets.

6.2 Collaboration

The industry stands at a turning point toward full acceptance of asset tokenization. Market-wide collaboration is essential to realize its benefits. Overcoming distribution challenges and achieving better capital efficiency require joint efforts. Banks and financial institutions can expand reach through collaborative models—for example, by developing tokenized industry utilities. Similarly, intermediaries like insurers can act as alternative distribution channels, broadening market access. Recognizing the transformative impact of tokenization on capital and operational efficiency, the industry must unite to harness the power of shared infrastructure.

Beyond financial institutions, the broader ecosystem—including technology providers and other participants—must collaborate to create a supportive environment. Achieving interoperability, legal compliance, and efficient platform operations through standardized processes and protocols is critical.

Current tokenization efforts remain fragmented and nascent. There is an urgent need for industry-wide cooperation to address these key issues, combining the robustness of traditional finance (TradFi) with the innovation and agility of DeFi. This strategic convergence will pave the way for a more stable, unified, and mature digital asset ecosystem, balancing technological progress with regulatory alignment and market stability.

6.3 Facilitation

Finally, governments and regulators—not just market participants—play a vital role in fostering responsible growth in the digital asset industry. By implementing policies that support global trade and communities (e.g., job creation), they can promote industry development while mitigating risks.

Clear, balanced regulatory frameworks can encourage innovation while avoiding pitfalls seen in the crypto space.

Public-private partnerships with banks and other financial institutions are equally important. Such collaborations can accelerate industry development by promoting responsible and sustainable growth.

Through these efforts, regulators can ensure that the growth of the digital asset industry benefits the economy, enhances global financial integration, creates jobs, and upholds market integrity and investor protection.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News