ArkStream Capital: How PayFi Unlocks a New Chapter in Crypto Payments?

TechFlow Selected TechFlow Selected

ArkStream Capital: How PayFi Unlocks a New Chapter in Crypto Payments?

The PayFi sector has immense future potential, and as a composite innovation across multiple sectors, its market cap could surpass $10 billion.

Author: James Zhu

TL;DR

-

The stablecoin market continues to grow, but crypto payments will not fully replace traditional fiat systems.

-

The true significance of PayFi lies in driving the real-world application and innovation of crypto assets in practical scenarios.

-

Solana is not necessarily the only contender in the PayFi or crypto payment space—Ton Network and Sui, with their respective strengths, could potentially overtake it.

-

The future potential of the PayFi sector is enormous. As a composite innovation across multiple sectors, its potential market cap could exceed tens of billions of dollars.

In recent years, the crypto payments sector has continuously evolved—from early perceptions of crypto as a tool for gray-market transactions to mainstream fintech platforms like Stripe acquiring the stablecoin platform Bridge, and established giants such as PayPal and Visa entering the space. Combined with the emergence of the new concept of PayFi, this has sparked widespread attention.

To better understand the prospects of this sector, ArkStream has outlined the evolution of crypto payments, focusing on how PayFi iterates upon this space and helps us identify future development directions.

Crypto Payments Sector

Since Bitcoin’s inception in 2008, it has evolved from small-scale transactions among tech enthusiasts to a globally accepted commercial application, followed by regulatory oversight and compliance-driven growth, eventually forming a diversified, platform-based payment ecosystem. Today, with technological maturity and expanded use cases, crypto payments are gradually integrating into traditional financial systems, offering users more efficient, low-cost, transparent, and decentralized payment solutions—indicating a new wave of transformation in the fintech landscape.

Underpinning this revolution, stablecoins serve as a bridge between cryptocurrencies and fiat currencies, providing the foundation for broad adoption of crypto payments through stable value storage and efficient on-chain circulation. Studying the stablecoin market thus offers valuable insights into the broader market.

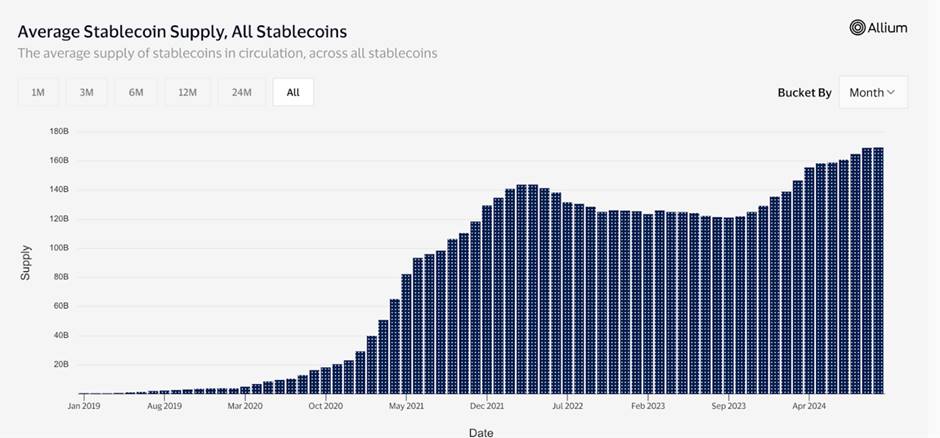

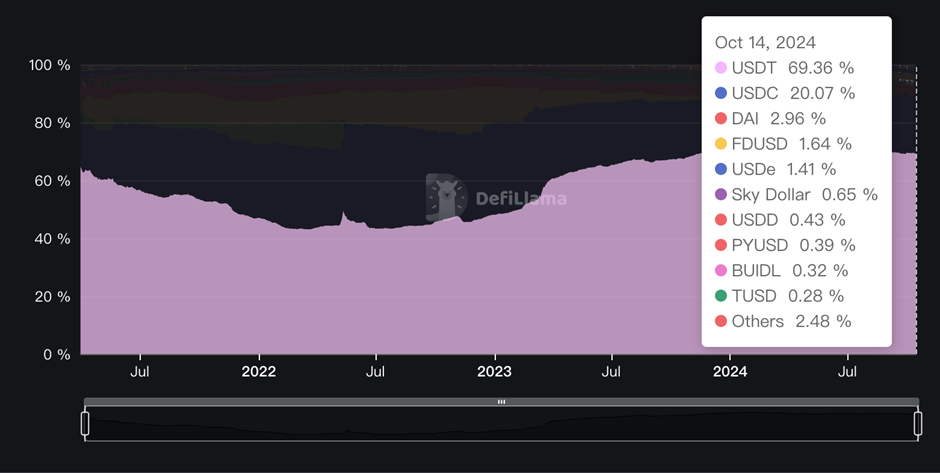

Overview of the Stablecoin Market

https://visaonchainanalytics.com/

https://defillama.com/stablecoins

Undeniably, the热度 of crypto payments is directly tied to the stablecoin market. These two charts (total stablecoin supply and market share by individual stablecoin) show long-term global growth in stablecoin issuance. USDT and USDC dominate the market with a combined 90%, with USDT leading at around 70% and showing steady, gradual growth.

We also examined the chain distribution of USDT and USDC. USDT is issued across 13 blockchains, with over 50% on Tron, followed by Ethereum and Solana. The top four chains account for nearly 99% of total issuance. In contrast, USDC is more centralized—nearly 92% is on Ethereum, followed by Solana, Tron, and Polygon.

It's clear that Ethereum and Solana remain dominant platforms for stablecoin applications. The sustained growth of the stablecoin market, coupled with major traditional payment players entering the space, demonstrates that the crypto payment sector has already developed a functional system capable of handling significant transaction volumes—proving market validation of stablecoin-based payments.

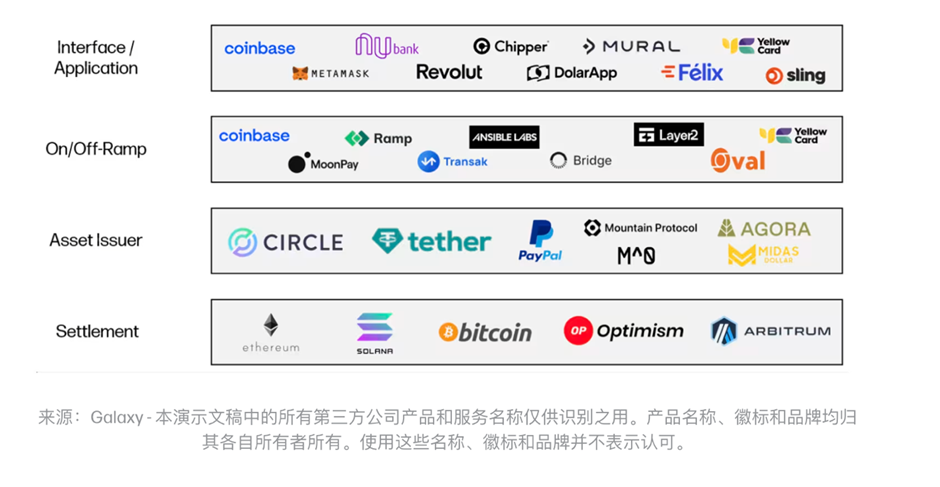

To better understand how crypto payments operate, we now examine the four-layer architecture of crypto payment solutions—an architectural framework ensuring security, scalability, and user experience.

Crypto Payment Solutions

A crypto payment solution consists of four layers, as shown in the diagram:

https://www.galaxy.com/insights/perspectives/the-future-of-payments/

-

Settlement Layer: The foundational blockchain infrastructure—including various Layer 1s and general-purpose Layer 2s like Optimism and Arbitrum—differ in speed, scalability, privacy, and security, essentially selling blockspace.

-

Asset Issuance Layer: Responsible for creating, maintaining, and redeeming stablecoins to maintain parity with fiat or a basket of underlying assets. Issuers earn yield by investing in stable-income assets like government bonds. Unlike traditional payment intermediaries, they do not charge fees on each transaction. Once issued, stablecoins can be self-custodied and transferred without additional costs to the issuer.

-

Fiat On/Off-Ramp Layer: Providers connecting blockchain and fiat systems, serving as technical bridges between stablecoins and bank accounts. Common models include B2C and C2C platforms.

-

Interface/Application Layer: Customer-facing software platforms supporting crypto payments, monetizing via traffic-driven fees from front-end transaction volume.

Current State of the Crypto Payments Sector

-

Traditional Payment Giants Enter Crypto

As the crypto market expands and ETFs gain approval, both traditional payment giants and native crypto projects are actively developing related services. As early as 2023, Visa extended USDC settlement to Solana, offering faster cross-border and real-time settlement.

Applying the four-layer model described earlier, Visa has built its crypto payment ecosystem through multi-layer partnerships:

-

Asset Issuance Layer: Partnering with Circle to use USDC ensures stable and compliant settlements.

-

Fiat On/Off-Ramp Layer: Collaboration with Crypto.com enables seamless fiat-to-crypto conversions.

-

Application Layer: Offering USDC settlement options to acquirers like Worldpay and Nuvei allows merchants greater flexibility.

-

Settlement Layer: Choosing Solana as its blockchain infrastructure leverages its high parallel processing, predictable low fees, and fast block finality for efficient on-chain settlement.

This integration allows Visa to bypass traditional banking rails—users can settle directly via USDC on the blockchain, eliminating intermediaries, shortening settlement times, and reducing costs. This move not only shows how crypto payments can innovate traditional finance but also offers a new vision for global payment networks.

PayPal also chose Solana as the new public chain for PYUSD this year, actively promoting blockchain-based payments. PayPal’s vice president has repeatedly highlighted Solana’s high throughput and low latency, making it an ideal infrastructure for crypto payments. While these traditional giants may lag behind Web3-native players in blockchain expertise, their massive user bases and industry resources enable rapid market entry and competitive positioning.

-

Native Crypto Projects

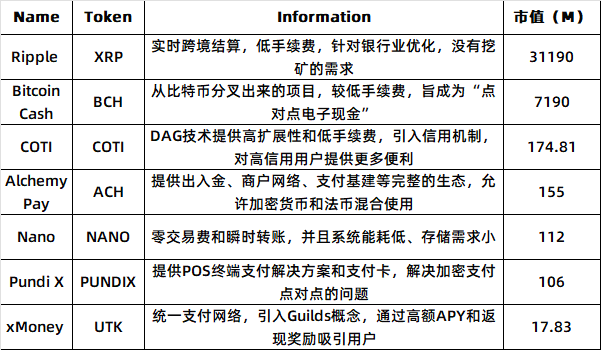

Compared to traditional giants, native crypto payment projects drive innovation through novel approaches. Below is a summary of crypto payment-related projects listed on Binance:

-

Ripple – Focused on B2B Cross-Border Transactions

Ripple has raised nearly $300 million in funding from prominent VCs including a16z, Pantera, Polychain, and IDE. It currently has nearly 6 million active accounts and over 300 partner institutions across 50 countries.

XRP is the native token of the Ripple Network, a Layer 1 blockchain focused on the B2B market, aiming to build a decentralized payment settlement and asset exchange platform in collaboration with central banks worldwide to support CBDC ecosystems.

Ripple uses the RPCA consensus algorithm and operates RippleNet atop the XRP Ledger, offering solutions like xCurrent, xVia, and xRapid to enhance cross-border liquidity and efficiency. It partners with traditional institutions like Bank of America and Credit Suisse. Compared to SWIFT, Ripple offers significantly faster and cheaper transactions—settling in seconds at less than 1% of traditional costs.

XRP processes around 150,000 payments daily, with over 10,000 daily active users. Its journey hasn’t been smooth—after years of SEC litigation alleging unregistered securities offerings—the case was recently dismissed by the SEC.

-

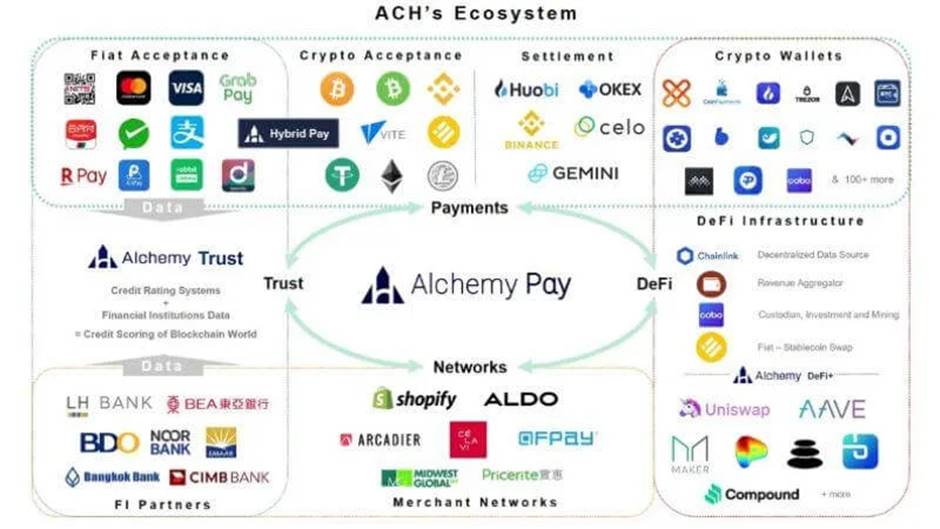

Alchemy Pay – Crypto Payment Specialist

Alchemy Pay has raised $10 million from investors like DWF and CGV. Recently, it gained renewed attention due to its virtual card integration with Samsung Pay.

Alchemy Pay combines Layer 1 protocols like the Lightning Network, state channels, and Raiden Network to create a hybrid on- and off-chain payment architecture. On-chain handles ledger management and data storage, while off-chain manages computation-heavy tasks like verification and reconciliation. This supports services including fiat on/off-ramps, NFT quick purchases, crypto credit cards, and customized crypto payment solutions.

https://alexablockchain.com/alchemy-pay-to-transform-crypto-payment-with-its-new-product/

According to third-party analysis of the ACH ecosystem, Alchemy Pay connects four core areas: payments, merchant networks, DeFi, and trusted assets. Partners include Binance, Shopify, Visa, and QFPay, highlighting its comprehensive footprint across the payment value chain.

Unlike XRP, ACH—the project’s token—is not used as a medium of exchange. Instead, it rewards users with cashback on payments, mimicking traditional credit card reward programs to boost loyalty and real-world usage.

ArkStream believes that whether traditional giants leverage their vast resources and global networks to enter crypto, or native projects push innovation via decentralization and tokenomics, both are advancing the sector. Traditional players bring market influence and compliance strength, while native projects excel in technical innovation and agility. With Stripe’s acquisition of Bridge—the largest deal in crypto history—we hope such collaborations will combine traditional scale and integration capabilities with crypto innovation to drive the payment industry toward digitalization, cost reduction, and efficiency gains.

-

Pain Points in the Crypto Payments Sector

1. Unstable Transaction Costs: Crypto payments aim to reduce intermediaries and transaction fees, but in practice, costs aren't always lower. During peak network congestion—especially on major L1s—fees can spike dramatically. In contrast, traditional payment tools like credit cards or third-party platforms offer more stable pricing, often absorbing fees (akin to "free shipping"), which reduces user friction.

2. Limited Processing Capacity: While decentralization and consensus mechanisms ensure transparency and security, they also constrain network throughput. Blockchains require global node consensus, limiting speed by block size and interval. Although Layer 2 solutions (e.g., Lightning Network), improved cross-chain communication, and sharding may help, even the highest-performing chains like Solana still fall short of Visa-level TPS. For high-frequency, low-value payments, current crypto networks face clear bottlenecks.

3. Lack of Application Scenarios: Despite enabling basic real-world use cases like daily spending, transfers, and cross-border payments, crypto payments remain absent in key financial domains such as lending, insurance, leasing, crowdfunding, and asset management—all still reliant on traditional finance.

ArkStream believes the root cause lies in prioritizing existing crypto users over broader market needs. Whether Alchemy Pay or Visa, focus remains on on/off-ramps, crypto debit cards, and P2P payments. To achieve mass adoption, projects must look beyond the crypto ecosystem, addressing external user demands—particularly unlocking new use cases—to build a full-fledged crypto payment ecosystem. Lily Liu, President of the Solana Foundation, recognized this gap and introduced the concept of “PayFi” at the Hong Kong Web3 Festival in April 2024, aiming to overcome these challenges and drive broader adoption.

PayFi: A New Chapter in Web3 Payments

Introduction to PayFi

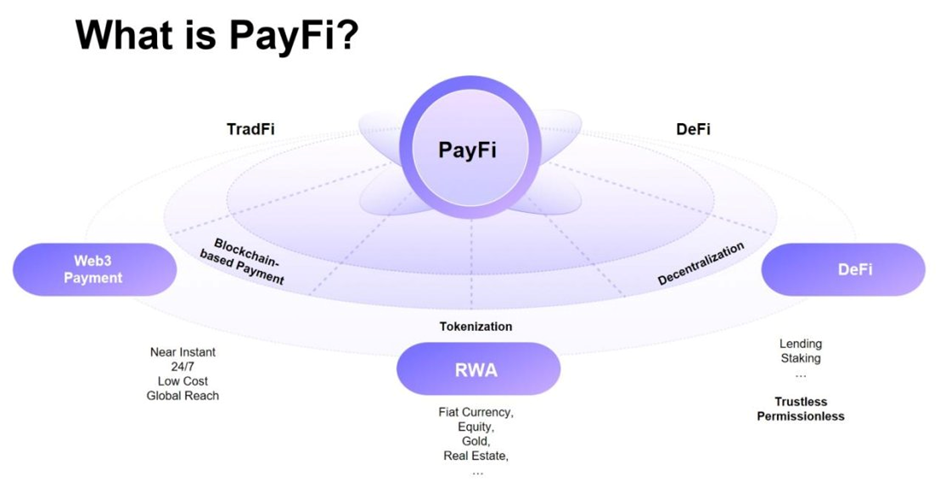

First, what is PayFi?

PayFi is not a standalone concept, but an innovative integration of Web3 payments, DeFi, and RWA.

-

RWA tokens represent real-world assets on-chain, enabling 1:1 value transfer via smart contracts;

-

DeFi focuses on reinventing traditional financial products in a decentralized, on-chain economy—AMMs, flash loans, liquidity mining—with trading as the primary goal;

-

Web3 Payments use crypto as a medium for transactions, improving efficiency in remittances and crypto cards.

PayFi is not simply RWA, Web3 Payments, or DeFi. ArkStream believes its true value lies in promoting digital asset applications in real-world scenarios. More precisely, PayFi builds on the foundations laid by RWA and Web3 Payments, extending DeFi’s innovations into tangible use cases.

https://www.feixiaohao.com/news/12951184.html

PayFi centers on two core concepts:

-

Tokenization of Real-World Assets: Since most transactions occur in real life, PayFi requires moving traditional payment scenarios on-chain via tokenization. Starting with stable, low-risk assets, PayFi leverages DeFi for transparent, liquid, flexible, and high-yield capital use, while RWA provides diverse asset classes and stable yield sources.

-

Unlocking Time Value of Money: Another key PayFi concept is using smart contracts and blockchain’s decentralized nature to efficiently unlock the time value of money at minimal cost. For example, users can manage and invest funds without intermediaries—via on-chain credit markets, installment systems, or automated investment strategies—reducing opportunity costs and enabling rapid reinvestment.

We illustrate PayFi’s value through a simple mathematical model measuring opportunity cost based on fund yields:

Let P = prepaid amount, r = interest rate. Assume traditional cross-border payments take 3 days, while crypto payments take 3 minutes. The opportunity costs are:

Opportunity Cost (Traditional) = P × r × 3

Opportunity Cost (Crypto) = P × r × (3/1440)

The difference equals roughly 3 days of interest. Our analysis shows this gap widens with larger prepayments and higher interest rates. Thus, this efficiency gain is especially impactful in high-frequency, large-value, or high-interest-rate environments.

Blockchain Selection for PayFi

Currently, many crypto payment projects are building on Solana. PYUSD is primarily hosted on Solana, capturing 64% market share versus Ethereum’s 36%. MiCA-compliant stablecoins like EUROC and EURC are also launching on Solana.

Why do both traditional and native crypto projects prefer Solana? We analyzed several key factors: high-performance infrastructure, capital liquidity, and developer talent.

-

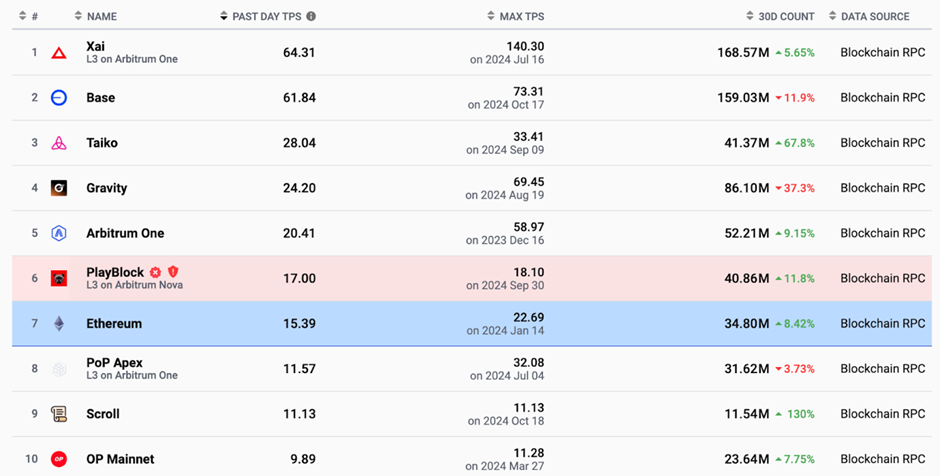

High-Performance Blockchain: Solana’s performance is its core advantage, consistently ranking among the highest TPS blockchains. Its consensus mechanism and low gas fees outperform most L2 solutions.

-

Capital Liquidity: Solana’s ecosystem has attracted $61 billion in staked capital. Investments from top-tier VCs like a16z and Polychain Capital further strengthen market confidence.

-

Rich Application Ecosystem: Consumer-facing apps—like Sanctum debit cards, Helium SIM cards, and the official Solana phone—surpass those of other blockchains.

Many L2 projects (Optimism, zkSync, Lightning Network) and L1s (Polygon, Monad, Aptos) claim superior TPS and scalability. Yet, according to available data, most fail to reach even a fraction of Solana’s peak TPS.

https://l2beat.com/scaling/activity

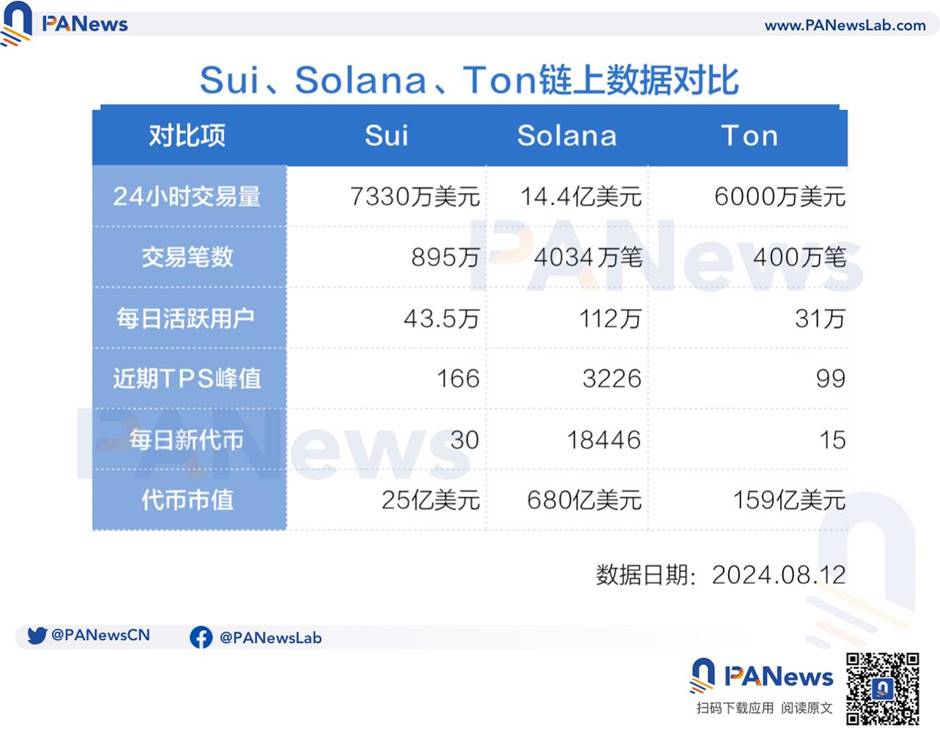

Despite Solana’s mainnet suffering multiple outages since 2020, ArkStream believes no chain can fundamentally replace it in the near term. However, emerging blockchains like Sui and TON are showing unique advantages, offering alternative paths for future crypto payment development.

Sui: Parallel Processing + Innovative Ecosystem

Sui, a next-gen blockchain, uses DAG architecture and parallel execution. Unlike Solana’s focus on high-frequency trading and DeFi, Sui aims to solve network bottlenecks in large-scale user interactions—making it ideal for GameFi and complex smart contracts.

Although Sui hasn’t attracted Solana-level capital and its peak TPS is less than half of Solana’s, its team brings deep expertise in payments and decentralized app development. This could attract innovative projects. For PayFi, Sui’s parallel processing may shine in highly interactive applications.

TON: Community + Payment Bridge

TON originated from Telegram, optimized for large communities and frequent microtransactions. Unlike Sui and Solana, TON emphasizes low latency and high scalability through sharding, already integrated into Telegram’s ecosystem.

TON’s greatest strength is its massive user base—900 million monthly active users—and embedded mini-app functionality. As a bridge between Web2 and Web3, TON offers PayFi projects instant access to a vast ready-made market via social and micro-payments.

https://www.techflowpost.com/article/detail_19707.html

While Solana leads today in crypto payments and PayFi due to proven performance, rich DeFi ecosystem, and capital strength, the future may see multi-chain coexistence. Sui’s parallel computing and novel use cases, along with TON’s dominance in social payments, could disrupt the current landscape.

Whether PayFi projects choose Sui or TON will depend on product needs, market positioning, and GTM strategy. But undoubtedly, multi-chain diversity and expanding use cases offer abundant opportunities for PayFi innovation.

Business Models and Real-World Applications

PayFi was first introduced in April 2024, so there are few projects so far. We categorize current PayFi initiatives into two main application areas: cross-border trade and credit finance.

Huma Finance

Product Overview: Huma Finance is a focal point in the PayFi space, targeting PayFi applications for consumers and SMEs. Its recent acquisition of Arf addresses liquidity issues related to prepaid capital in cross-border payments.

Arf aims to solve liquidity and timing issues in cross-border prepayments. Through Arf, trust between buyers and sellers is established without requiring bank prepayments or letters of credit. Arf provides a P2P service and an on-chain liquidity network, advancing stablecoins to enterprises and eliminating the need for upfront payments. Businesses pay a fee and repay Arf within an agreed timeframe.

https://x.com/arf_one

Huma Finance’s core offering aligns with Lily Liu’s “Buy Now, Pay Never” vision. Users can pledge upcoming receivables as collateral. Huma tokenizes these receivables via its protocol, allowing users to borrow from a lending pool, with enforcement handled automatically by smart contracts. Potential use cases include trade finance, SME lending, and international tuition payments.

Technical Architecture: Huma’s PayFi Stack comprises six layers—Transaction, Currency, Custody, Financing, Compliance, and Application—covering every aspect from transaction processing to asset management and compliance. This full-stack design enables the entire borrowing, valuation, funding, and payment process to occur within one ecosystem. By combining automation, decentralization, and layered integration, PayFi drastically simplifies complex lending and payment workflows, boosting efficiency and lowering costs.

Data: To date, Huma has facilitated $1 billion in total loan volume with zero defaults. As a leader in the PayFi space, it has raised $38 million in funding.

Future Market for PayFi

After reviewing PayFi projects, we’ve considered their geographic applicability. ArkStream believes PayFi has undeniable global mass adoption potential. Initial use cases may not be limited to developed economies (U.S., Singapore, Europe); emerging markets also hold vast promise.

-

Strategy in Developed Markets: In advanced economies, PayFi can complement existing digital payment systems by integrating DeFi innovations. Clearer regulations and policy support (e.g., USDC, PYUSD, EUROC) have enabled wide adoption. Strategic partnerships with retailers, e-commerce platforms, and cross-border financial services could accelerate PayFi adoption by offering lower-cost, higher-efficiency crypto payment channels.

-

Opportunities in Emerging Markets: In regions underserved by traditional finance, PayFi can offer crypto microloans, flash loans, and other services. The decentralized and borderless nature of crypto payments can provide financial access to the unbanked. Examples include Africa, Southeast Asia, Latin America, and high-inflation countries like Nigeria and Argentina. Due to the lack of robust traditional financial infrastructure, PayFi products may scale faster here than in developed nations.

Therefore, ArkStream concludes that PayFi should pursue a dual-track strategy: in developed markets, focus on enhancing existing use cases and building partnerships; in developing countries, prioritize deployment of crypto payments, PayFi applications, and penetration into remittance markets.

Outlook

Though the PayFi concept is new and real-world projects remain scarce, ArkStream believes PayFi holds significant promise. Both internal developments in crypto payments and external macroeconomic trends strongly favor PayFi’s growth.

In recent years, rising U.S. interest rates have driven demand for fixed-income products. Many crypto users have shifted funds into tokenized bond markets, attracted by stable underlying assets and relatively high, liquid returns.

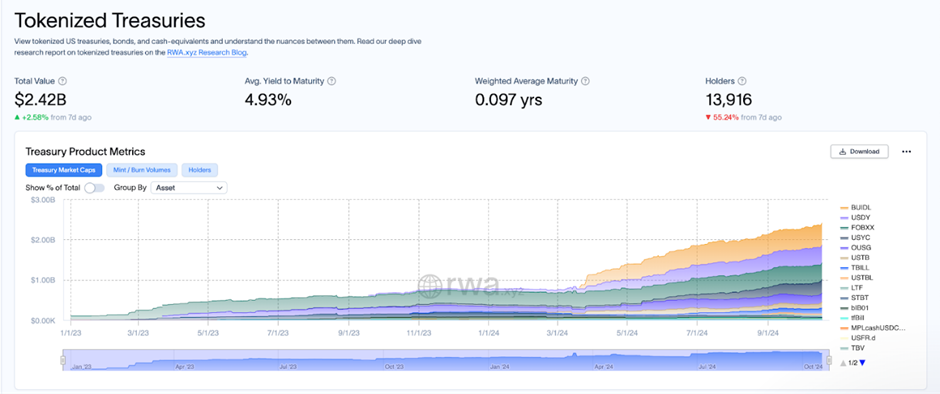

According to RWA.XYZ, the tokenized U.S. Treasury market has grown from $770 million in early 2024 to $1.916 billion by August 1, 2024—a 248% increase.

https://app.rwa.xyz/

With the U.S. signaling rate cuts and declining Treasury yields, investor reliance on Treasuries is weakening, prompting capital to seek new destinations. Investors are turning to assets offering sustainable value and stable returns.

The rise of PayFi combined with RWA perfectly fills this gap. The RWA sector now has over $6 billion in TVL and continues to grow. RWA involves tokenizing real-world assets (bonds, receivables, supply chain finance) onto the blockchain, offering diversified, highly liquid investment options.

Here are three promising RWA examples:

-

MakerDAO RWA offers tokenized real estate and receivables, linked to DAI stablecoin, effectively bridging off-chain funding needs with on-chain liquidity. It’s currently the top RWA protocol by TVL;

-

Tether Gold offers gold-backed tokens, enabling crypto-native gold investment without physical ownership;

-

Ondo Finance offers risk-tiered on-chain exposure to real financial assets like government and corporate bonds. As Treasury yields fall, Ondo’s corporate loan RWA products may better meet investor demand.

Conclusion

Currently, PayFi projects are extremely limited and mostly in early stages. Therefore, we focus on the innovativeness of PayFi solutions.

From a business model perspective, PayFi integrates elements from multiple sectors: crypto payments (e.g., Ripple, Stellar), DeFi lending (e.g., Aave, Compound), and RWA (e.g., MakerDAO RWA, Ondo Finance). These sectors have already validated their feasibility, proving market demand and growth potential. By referencing the market caps of leaders in these fields—ranging from billions to tens of billions of dollars—we can reasonably expect PayFi, as a composite innovation, to surpass them. As use cases like cross-border payments, supply chain finance, and corporate lending expand and compound, the overall market cap of the PayFi sector could exceed current benchmarks.

From a product standpoint, future PayFi development should target specific payment scenarios, optimizing efficiency and user experience. Undoubtedly, PayFi remains one of the few untapped blue oceans—but it lacks sufficient applications. We call on more developers to leverage existing crypto payment technologies, focus on global markets, and innovate based on real-world needs.

For instance, at Token2049 this year, we observed TADA Taxi partnering with the Ton Network, using crypto payments and shared incentives to reduce commission rates, differentiating itself in a crowded ride-hailing market. Similarly, Ether.Fi is launching a crypto payment card whose Cash feature not only supports standard crypto spending but also allows users to repay expenses using yield from liquid staking.

Such real-world breakthroughs exemplify PayFi’s vast global potential. Projects should not merely seek the next high-yield “reservoir” for on-chain capital, but instead focus on delivering tangible benefits—convenience, cost savings, usability—to traditional users, thereby increasing crypto’s market penetration.

We can envision entirely new financial products that traditional finance cannot easily offer, such as:

-

Instant Loans: Users can collateralize crypto assets on PayFi platforms to obtain loans with better terms than traditional channels;

-

Advance Consumption & Investment: Without debt, users can spend or invest before receiving future income;

-

High-Yield Liquid Funds: Using staking and liquid staking, users can earn over 10% yield while maintaining liquidity;

-

Prepayment of Interest on Term Financial Products: Users can use accrued interest as working capital before product maturity.

These innovations embody the principle that “time is money,” maximizing the time value of capital. We recognize clearly that PayFi is neither speculative nor an “insider’s party.” From both practicality and innovation, PayFi is steadily bridging crypto and traditional finance. As long-term investors, ArkStream sees PayFi’s immense potential—even foreseeing a future without traditional banks.

These innovative applications, blending DeFi with real-world needs, further validate PayFi’s huge potential in unlocking capital efficiency. ArkStream believes the long-term prospects of PayFi are limitless.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News