Arthur Hayes' new article: My macroeconomic forecast accuracy in recent years has been only 25%, but my crypto investments are still profitable

TechFlow Selected TechFlow Selected

Arthur Hayes' new article: My macroeconomic forecast accuracy in recent years has been only 25%, but my crypto investments are still profitable

Despite experiencing many losing trades, I am still profitable overall.

Author: Arthur Hayes

Translation: TechFlow

(The views expressed in this article are solely those of the author and should not constitute the basis for investment decisions, nor should they be construed as recommendations or advice to engage in investment transactions.)

This week has been absolutely wild. If you missed Token2049 in Singapore last week, I truly feel sorry for you. Over 20,000 enthusiastic participants expressed their excitement in every imaginable way. I’ve attended almost every event since Singapore started hosting its night F1 race, but I’ve never seen the city so vibrant.

Attendance at Token2049 doubled compared to last year. I heard that some lesser-known projects paid as much as $650,000 just to speak on smaller stages.

The parties were packed. Marquee is a club that holds several thousand people. Imagine having to wait in line for over three hours just to get into one event. Each night, different crypto projects or companies booked out the entire venue. Booking Marquee costs $200,000—excluding drinks.

There was something for everyone. Iggy Azalea flew in a group of strippers from Los Angeles to create a pop-up "experience." Who would have thought these dancers could understand how to operate in volatile markets?

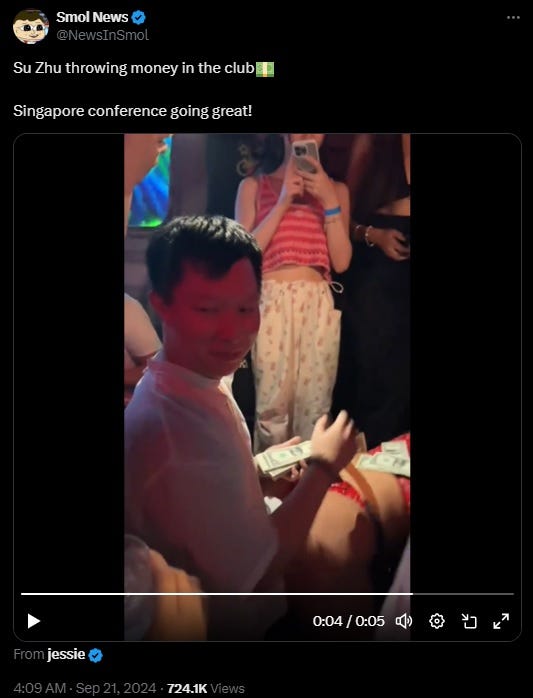

Even Su Zhu, known as the “Randall of crypto,” couldn’t resist wanting to “make money dance.” Randall, why do you look so uncomfortable in this video? Losing money is your specialty. Once you finally submit your assets to the British Virgin Islands bankruptcy court and settle all lawsuits, I’d be happy to take you to Magic City and teach you how it’s done.

I’m considering getting Branson Cognac and Le Chemin du Roi to sponsor my next party. As 50 Cent once said:

Every hotel was fully booked, even mid-tier restaurants were packed. When the 2024 data comes in, I suspect we’ll find that the crypto crowd brought more business to airlines, hotels, restaurants, conference venues, and nightclubs than any other event in Singapore’s history.

Thankfully, Singapore remains relatively geopolitically neutral. This means that as long as you believe in Satoshi, you can basically celebrate freely with your fellow crypto enthusiasts.

The energy and passion of crypto participants stand in stark contrast to the dullness and boredom of traditional finance conference attendees. The Milken Institute also held its conference that same week. If you walked around the Four Seasons—the conference venue—you’d see men and women dressed almost identically in bland business-casual or formal wear. Traditional finance deliberately keeps clothing and behavior calm and unchanging. They want the public to think, “There’s nothing to see here,” while in reality, they’re stealing human dignity through the inflation imposed by their institutions. Volatility is their enemy because when things start moving, ordinary people can see the true moral decay of their masters reflected in the mirror.

Today, we’ll discuss volatility in crypto versus the lack of volatility in traditional finance. I want to explore how elites print money to create an illusion of economic stability. At the same time, I want to explain how Bitcoin serves as a release valve for the fiat currency printed to suppress volatility to unnatural levels. But first, I’d like to illustrate the key point that short-term macroeconomic predictions don’t matter much, by reviewing my track record from November 2023 to now.

Fifty-Fifty

Many readers and keyboard warriors in the crypto space often criticize me for being wrong. So how have I performed on major calls over the past year?

November 2023:

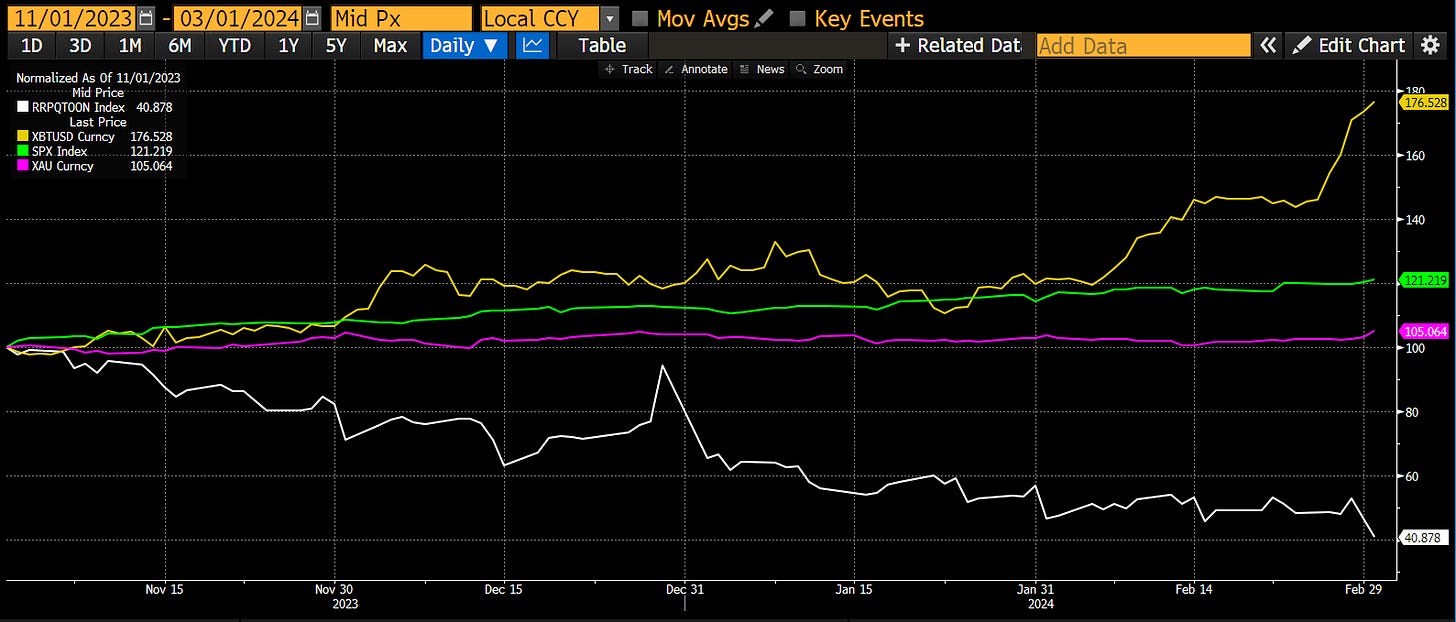

I wrote an article titled Bad Gurl. In it, I predicted that Treasury Secretary "bad girl" Yellen would issue more T-bills to drain funds from the Fed's Reverse Repo Program (RRP). The decline in RRP would inject liquidity into the market, driving up risk assets. I believed the market would soften in March 2024 when the Bank Term Funding Program (BTFP) expired.

From November 2023 to March 2024, the Reverse Repo Program (RRP, white) declined by 59%, Bitcoin (gold) rose 77%, the S&P 500 (green) increased by 21%, and gold (red) gained 5%. Each dataset is indexed to 100.

Win +1.

After closely reading the U.S. Treasury's Quarterly Refunding Announcement (QRA), I decided to increase my crypto exposure. Looking back, that was clearly the right move.

March 2024:

In my article Yellen or Talkin, I speculated that the BTFP would not be renewed due to its obvious inflationary nature. I argued that merely allowing banks to use the discount window wouldn't be enough to prevent another non-"Too Big To Fail" (TBTF) U.S. banking crisis.

The expiration of BTFP had no meaningful impact on the market.

Loss +1.

I lost some money on Bitcoin put options.

April 2024:

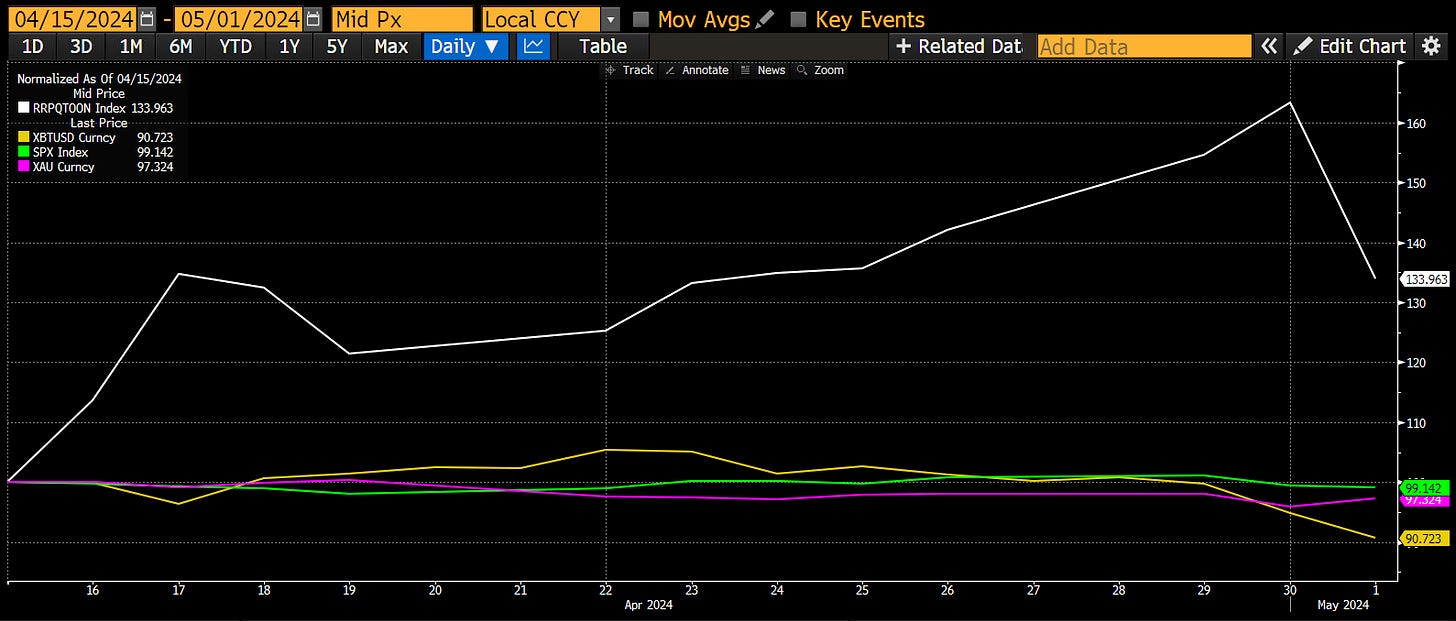

In my article Heatwave, I predicted that tax season in the U.S. would lead to a drop in crypto prices as dollar liquidity was drained. Specifically, I said I would pause adding any additional crypto risk between April 15 and May 1.

From April 15 to May 1, the RRP (white) rose by 33%, Bitcoin (gold) fell 9%, the S&P 500 (green) dropped 1%, and gold (magenta) declined by 3%. Each dataset is indexed to 100.

Win +1.

May 2024:

Before heading off for my summer break in the Northern Hemisphere, I published Mayday, based on several macroeconomic factors. My predictions were:

-

Did Bitcoin hit a local low around $58,600 earlier this week? Yes.

-

What’s your price prediction? I expected Bitcoin to rise above $60,000, then trade between $60,000 and $70,000 until August.

Bitcoin dropped to a low of about $54,000 on August 5 due to unwinding of USD-JPY carry trades. My call was incorrect, missing by 8%.

Loss +1.

During this period, Bitcoin traded roughly between $54,000 and $71,000.

Loss +1.

During the summer slump, I did add some exposure to "altcoins." Some of the coins I bought are now trading below my entry price, others above.

June and July 2024:

When Japan’s fifth-largest bank admitted massive losses on foreign currency bonds, I wrote Shikata Ga Nai, discussing the importance of USD-JPY. I predicted the Bank of Japan (BOJ) wouldn’t hike rates, as it would endanger the banking system. However, this assumption proved overly naive. On July 31, the BOJ hiked rates by 0.15%, triggering a sharp unwind of USD-JPY carry trades. I followed up with the article Spirited Away, explaining the mechanics of the carry trade unwind.

While USD-JPY proved to be the most important macro variable, my judgment on BOJ policy was wrong. The policy response didn’t unfold as I predicted. Instead of providing dollars via central bank swap lines, the BOJ reassured markets it wouldn’t proceed with rate hikes or monetary tightening if they caused excessive volatility.

Loss +1.

August 2024:

Two major events occurred this month: the U.S. Treasury released the Q3 2024 QRA, and Powell pivoted on jobs data at Jackson Hole.

I predicted that Yellen’s reissuance of T-bills would provide dollar liquidity to markets. However, after Powell’s dovish turn confirmed a September rate cut, these two forces worked against each other. Initially, I thought net T-bill issuance would boost liquidity by pushing RRP to zero. But then T-bill yields fell below RRP rates, leading me to predict RRP balances would rise again, draining liquidity.

I didn’t anticipate Powell cutting rates before the election, risking an inflation explosion during voter decision-making.

Loss +1.

After Jackson Hole, RRP balances immediately increased, resuming an upward trend. Thus, I still believe this will slightly drain liquidity, as T-bill yields continue to fall and markets expect further Fed cuts in November.

The outcome is still uncertain; it’s too early to judge whether I’m ultimately correct.

September 2024:

As I left the Patagonian mountains, I wrote Boom Times … Delayed, and in speeches at Korea Blockchain Week and Singapore’s Token2049, I predicted that if the Fed cut rates, markets would react negatively. Specifically, I argued that narrowing USD-JPY interest rate differentials would cause further yen appreciation and reignite carry trade unwinds. This would trigger declines across global markets, including crypto, eventually requiring more money printing to put "Hamptons Dumpy" back together.

The Fed cut rates while the BOJ held steady, narrowing the spread—but the yen depreciated against the dollar, and risk markets performed strongly.

Loss +1.

Result:

2 correct predictions

6 incorrect predictions

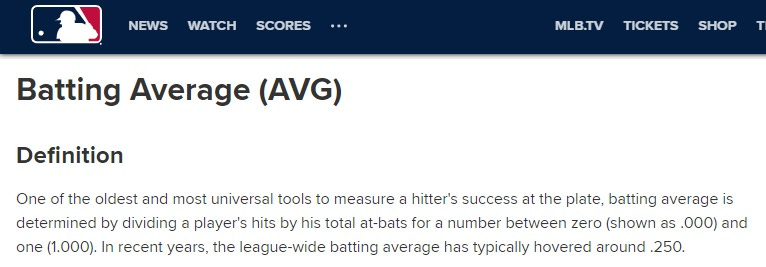

So my batting average is .250. That’s quite poor for an average person, but as the great Hank Aaron said: “My motto has always been keep swinging. Whether I’m in a slump, feeling bad, or having trouble off the field, the only thing to do is keep swinging.” Aaron’s career batting average was .305—he’s considered one of the greatest baseball players of all time.

Despite many losses, overall I am still profitable.

Why?

Big Assumptions

When writing these macro pieces, I try to predict specific events that might trigger policy responses from our corrupt rulers. We know—meaning both traditional finance puppets and believers in Satoshi—that they cannot handle any form of financial market volatility due to the extreme leverage built into the post-1971 Bretton Woods global trade and financial system. We all agree that when things go south, they’ll hit the “Brrrr” button. That’s always their policy response.

If I can predict the trigger ahead of time, I feel good about myself and maybe gain extra profit by positioning early. But as long as my portfolio benefits from fiat printing designed to suppress the natural volatility of human civilization, it doesn’t really matter if every single event-driven prediction I make turns out wrong—as long as the policy reaction unfolds as expected.

I’ll show you two charts to help you understand the enormous amount of fiat required to suppress volatility at historically low levels.

Volatility

Starting in the late 19th century, the elite who control global governments made a deal with the masses. If ordinary people surrendered more and more freedom, the “smart” people running nations would create a calm universe by suppressing entropy, chaos, and volatility. As decades passed, government involvement in every citizen’s life grew increasingly significant. Maintaining the appearance of rising order became extremely expensive, as our collective knowledge expanded and the world grew more complex.

Previously, a few authors’ books were treated as authoritative sources on how the universe works. They killed or exiled anyone practicing science. But as we broke free from organized religion and began thinking critically about the cosmos, we realized we knew nothing—and things were far more complicated than simply believing what’s written in books like the Bible, Torah, or Quran. People then turned to politicians (mostly men, a few women), who replaced priests, rabbis, and imams (always men), offering frameworks promising safe living and understanding of how the universe operates. Yet whenever volatility spiked, the response was always money printing—to mask the myriad problems in the world and avoid admitting nobody knows what’s coming next.

It’s like holding an inflated ball underwater—the deeper you push it down, the more energy it takes to keep it submerged. Global distortions are so extreme, especially under American hegemony, that the amount of money printing required to maintain the status quo grows faster each year. That’s why I can confidently say the quantity of fiat needed from now until the final system reset will vastly exceed the total printed since 1971. It’s simply math and physics.

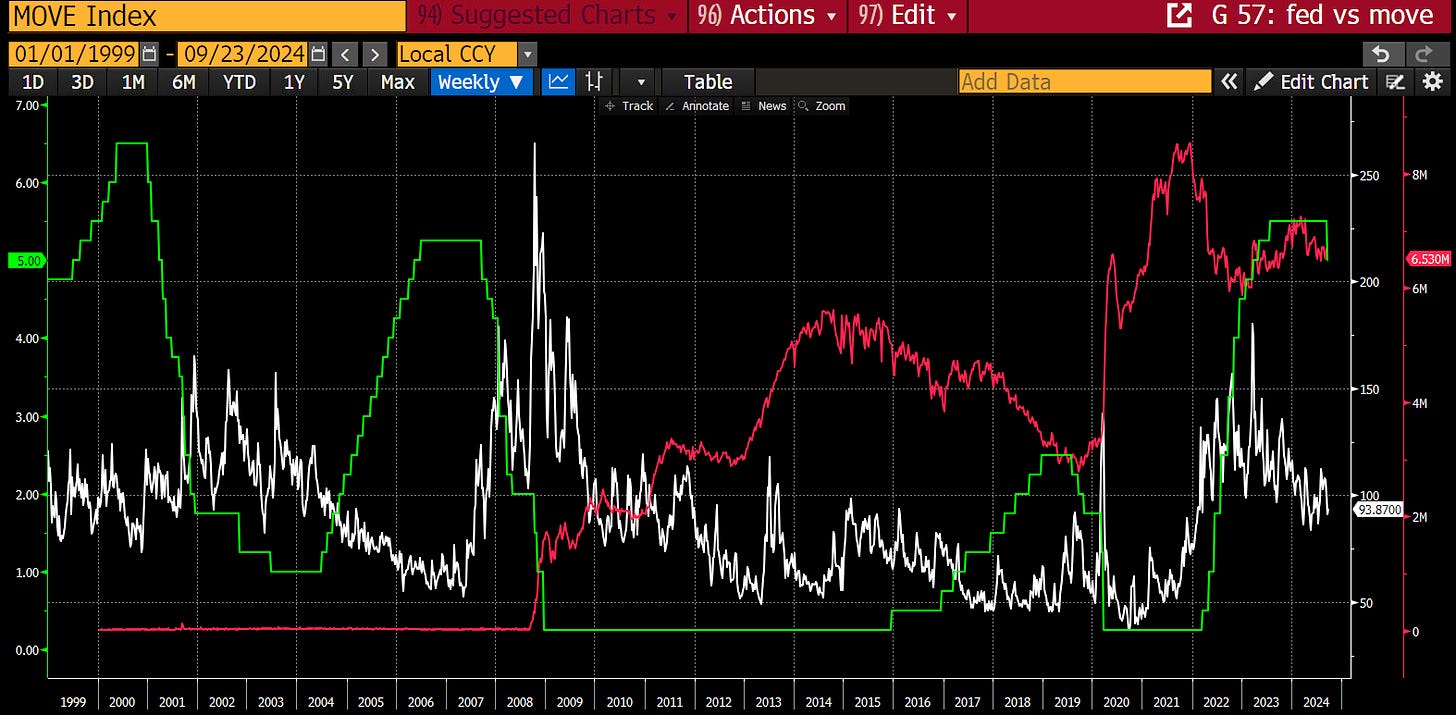

The first chart I’ll show is the MOVE Index (white), measuring volatility in the U.S. bond market against the upper bound of the Federal Funds Rate (green). As you know, I believe quantity matters more than price, but in this case, price paints a very clear picture.

You probably remember the rise and collapse of the tech bubble around 2000. As you can see, the Fed raised rates to burst the bubble—until things went wrong. After 9/11 in 2000 and 2001, bond market volatility surged. Once volatility spiked, the Fed cut rates. After volatility subsided, the Fed normalized rates—only to burst the subprime housing market, leading to the 2008 Global Financial Crisis (GFC). Rates were quickly slashed to zero and stayed there for nearly seven years to suppress volatility. Then came another attempt at normalization, followed by COVID, which caused a bond market crash and volatility spike. The Fed cut rates to zero again. Inflation ignited by COVID stimulus began heating up the bond market from 2021, increasing volatility. The Fed raised rates to combat inflation but had to stop in March 2023 during the non-TBTF banking crisis. Finally, the current Fed easing cycle occurs amid heightened bond market volatility. If we consider 2008–2020 “normal,” today’s bond market volatility is nearly twice our comfort level.

Now let’s introduce a measure of dollar quantity. The red line approximates total bank credit, composed of excess bank reserves held by the Fed plus Other Deposits and Liabilities (ODL)—a solid indicator of commercial bank lending growth. Recall from Econ 101: the banking system creates money by extending credit. As the Fed conducts QE, excess reserves rise; as banks lend more, ODL increases.

As you can see, 2008 was a turning point. The financial crisis was so massive that the flood of credit dwarfed what happened after the tech bubble burst in 2000. No wonder our Lord and Savior Satoshi created Bitcoin in 2009. Since then, total bank credit has never fully contracted. This fiat credit cannot be destroyed—or the system would collapse under its own weight. Moreover, in every crisis, banks must create ever-larger amounts of credit to suppress volatility.

I could show similar charts linking FX volatility—USD/CNY, USD/JPY, EUR/JPY—to government debt levels, central bank balance sheets, and bank credit growth. But none are as clear as the one I just showed. American hegemony cares about bond market volatility because it underpins the global reserve currency—the dollar. Allies, vassals, and enemies alike watch volatility between their currencies and the dollar, as it affects their ability to trade with the world.

Reaction

All this fiat money has to go somewhere—Bitcoin and crypto are the release valves. Fiat printed to suppress volatility will flow into crypto. Assuming Bitcoin’s blockchain technology remains sound, Bitcoin will always benefit from elites continuing to defy the laws of physics. There must be a balancing mechanism—you can’t create something from nothing. In this modern digital world, Bitcoin happens to be the most technologically reliable way to counterbalance the reckless behavior of ruling elites.

As investors, traders, and speculators, your goal is to acquire Bitcoin at the lowest possible cost. This might mean pricing your hourly labor in Bitcoin, using excess cheap energy to mine Bitcoin, borrowing fiat at low rates to buy Bitcoin (call Michael Saylor), or allocating part of your fiat savings to Bitcoin. The volatility between Bitcoin and fiat is your asset—don’t waste it by using leverage to buy Bitcoin you plan to hold long-term.

Are there risks?

Profitable speculation based on short-term price moves is extremely difficult. As you saw from my record, I’m 2 for 6. If I had gone all-in or all-out on every call, Maelstrom would likely be bankrupt by now. Randall and Kyle Davies were right—there is indeed a supercycle in elites suppressing volatility. But they lacked patience, borrowing fiat to buy more Bitcoin. When fiat funding costs changed—as they always do—they got squeezed and lost everything. Not all of them—I’ve seen photos of Randall throwing lavish parties at his mansion in Singapore. But don’t worry—it’s in his kids’ names, protecting it from bankruptcy courts.

Assuming you don’t abuse fiat leverage, the real risk lies in when elites can no longer suppress volatility, and it returns to its natural level. Then the system resets. Will it be a revolution like Bolshevik Russia, where the bourgeoisie are completely wiped out? Or the more common scenario—corrupt elites replaced by another corrupt group, with people’s suffering continuing under a new “ism”? Either way, everything falls—and Bitcoin falls less relative to the ultimate asset: energy. Though your total wealth shrinks, you’ll still outperform. Sorry, nothing in the universe is risk-free. Safety is an illusion sold by fraudsters who want your vote on Election Day.

Trading Strategy

United States

Based on the Fed’s historical response to “high volatility,” we know that once they start cutting rates, they typically keep cutting until rates approach 0%. Additionally, bank credit growth must accelerate alongside rate cuts. I don’t care how “strong” the economy is, how low unemployment goes, or how high inflation rises—the Fed will keep cutting, and the banking system will unleash more dollars. Regardless of who wins the U.S. presidential election, the government will keep borrowing as much as possible to appease the masses, indefinitely into the future.

European Union

The unelected bureaucrats of the EU are suicidally destroying their economy by rejecting cheap, abundant Russian energy and dismantling domestic energy production under slogans like “climate change,” “global warming,” “ESG,” or other nonsense. Economic depression will be countered by the European Central Bank lowering euro interest rates. Governments will also force banks to lend more to local businesses, enabling job creation and rebuilding deteriorating infrastructure.

China

As the Fed cuts and U.S. banks extend more credit, the dollar will depreciate. This allows China to ramp up credit growth while maintaining stability in the USD/CNY exchange rate. The Chinese president’s main concern with accelerating bank credit is depreciation pressure on the yuan versus the dollar. But if the Fed prints, the PBOC can print too. This week, the PBOC rolled out a series of interest rate cuts across the monetary system. This is just the beginning—the real “big bazooka” comes when banks extend significantly more credit.

Japan

If other major economies are now loosening policy, pressure on the Bank of Japan (BOJ) to rapidly hike rates diminishes. BOJ Governor Ueda clearly stated he intends to normalize rates. But since other countries’ rates are now falling toward his low level, he doesn’t need to rush to catch up.

The moral of the story: global elites are once again suppressing volatility in their nations or economic blocs by lowering the price of money and increasing its supply. If you’re already fully invested in crypto, sit back, relax, and watch your portfolio’s fiat value rise. If you have spare fiat, hurry and deploy it into crypto. As for Maelstrom, we’ll push projects that delayed token launches due to poor market conditions to accelerate. We hope to find green candlestick charts in our Christmas stockings. And the fund brothers are hoping for a nice 2024 bonus—so please help them out!

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News