Four Decades of Fed Monetary Policy: "Volcker's Inflation Fight" — "Greenspan's Miracle" — "Bernanke's QE" — What Will Powell Leave Behind?

TechFlow Selected TechFlow Selected

Four Decades of Fed Monetary Policy: "Volcker's Inflation Fight" — "Greenspan's Miracle" — "Bernanke's QE" — What Will Powell Leave Behind?

Today, the Federal Reserve is facing the most complex global economic situation in history.

Author: Zhang Yaqi, Wall Street Insights

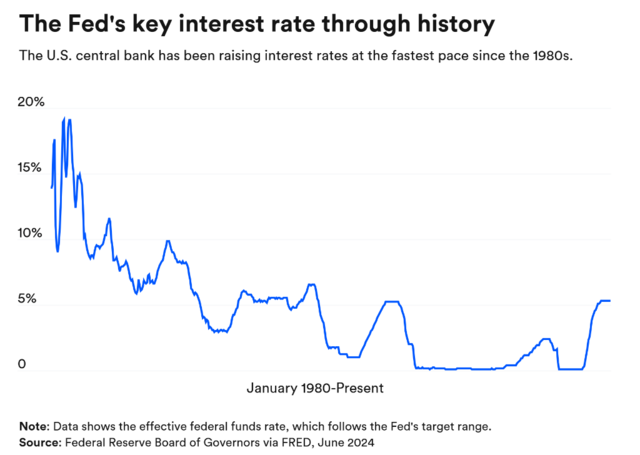

Over the past four decades, U.S. monetary policy has been shaped by multiple Federal Reserve chairs, each navigating the unique challenges of their era.

From Volcker's aggressive rate hikes to tame inflation, to Greenspan guiding America through an era of economic prosperity, followed by Bernanke's quantitative easing reshaping the post-crisis economy and Yellen ushering in a new hiking cycle—today, the Fed faces one of the most complex global economic environments in history.

This Thursday, Powell made a historic announcement cutting rates by 50 basis points, marking the start of a new easing cycle. Can he replicate the successes of his predecessors and steer the U.S. economy toward a soft landing? And what legacy will he leave behind?

"The Volcker Moment": Resolutely Controlling Inflation, Even at the Cost of Recession

In the late 1970s, the United States was mired in stagflation, with persistently high inflation. In response to this crisis, then-Fed Chair Paul Volcker implemented unprecedentedly aggressive interest rate hikes.

Between 1981 and 1990, the federal funds rate soared to a historic peak of 19–20%. While this successfully brought inflation under control, it also triggered a recession, pushing unemployment to nearly 11%—the highest since the Great Depression.

Meanwhile, Fed rates fluctuated frequently: on November 2, 1981, rates sharply declined to a target range of 13–14%, rose again to 15% during the first four months of 1982, then dropped to 11.5–12% on July 20, 1982. Records show that over this decade, the "effective" federal funds rate averaged 9.97%. After November 1984, the rate never exceeded 10% again.

Unlike today’s approach of directly adjusting interest rates to manage inflation, Volcker’s policy centered on constraining money supply growth. Though heavily criticized at the time, his strategy ultimately brought inflation below 2% by 1986.

Alan Greenspan: Successfully Steering the U.S. Economy to a Soft Landing

During his tenure as Fed Chair (1987–2006), Alan Greenspan played a pivotal role in shaping U.S. monetary policy, economic management, and global financial affairs.

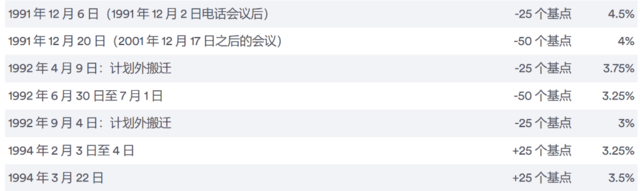

In August 1990, the U.S. economy entered an eight-month recession. Under Greenspan’s leadership, the Fed responded effectively, eventually raising the federal funds rate to a record high of 6.5% by May 2000. In contrast, the rate had dipped to 3% in September 1992—the lowest level in a decade.

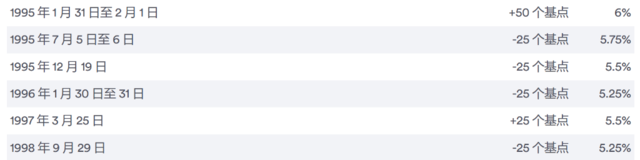

In 1995, Greenspan successfully guided the U.S. economy to a soft landing, paving the way for a subsequent period of economic boom.

In 1994, the Fed aggressively raised rates to combat inflationary pressures. By 1995, the labor market had clearly cooled, and in May 1995, monthly job growth turned negative.

The Fed then cut rates three times by 25 basis points each during 1995 and early 1996, achieving success. By mid-1996, average monthly job creation rebounded to around 250,000, and inflation ceased to be a major concern for the U.S. economy for many years thereafter.

Greenspan served longer than any other Fed chair. He earned the nickname “Maestro” for steering the U.S. through the longest economic expansion in its history. Under his leadership, the Fed also informally established a 2% inflation target—a decision that profoundly influenced modern monetary policy.

Ben Bernanke: The Architect of QE

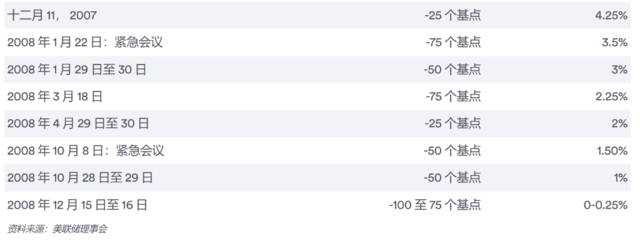

Amid the catastrophic 2008 financial crisis, Ben Bernanke led the Federal Reserve in launching quantitative easing (QE) and cutting interest rates to near zero, rescuing the U.S. economy from collapse.

Prior to the crisis, rates had reached a high of 5.25%. After the subprime mortgage crisis erupted, the Fed slashed rates by 100 basis points, bringing them close to zero.

During this period, the Federal Reserve implemented quantitative easing—large-scale asset purchases (LSAP)—aimed at lowering long-term interest rates and stimulating economic growth. This caused the Fed’s balance sheet to balloon dramatically, surging from $870 billion to $4.5 trillion.

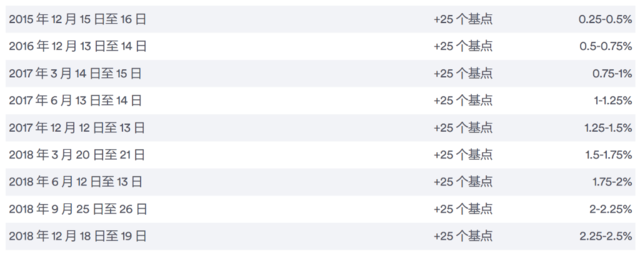

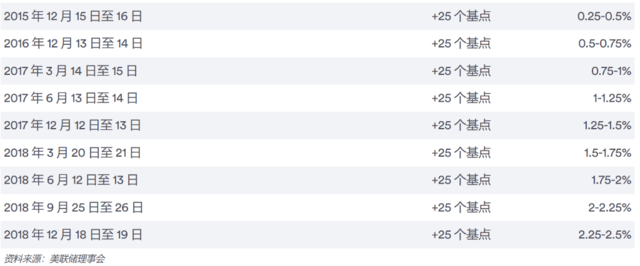

Not until after 2015 did the Fed begin raising rates by 25 basis points at a time, eventually reaching a range of 2.25–2.5% by 2018.

Yellen: From Exiting QE to Raising Rates

In February 2014, Janet Yellen succeeded Bernanke as Chair of the Federal Reserve, guiding the economy through the recovery from the Great Recession.

Starting in December 2015, the Fed raised rates by just 25 basis points per year. In 2017, it hiked three times; in 2018, four times. The federal funds rate peaked at 2.25–2.5%.

Powell Takes the Helm: Where Is the U.S. Economy Headed?

In February 2018, current Fed Chair Jerome Powell took office.

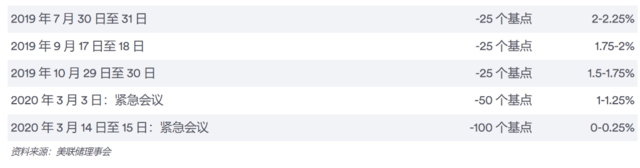

Facing tepid inflation and slowing growth, the Fed decided in 2019 to cut rates three times to reinvigorate the economy—similar to Greenspan’s “insurance cuts” in the 1990s.

Then came the COVID-19 pandemic, marking the dawn of a new era. In two emergency meetings within 13 days, the Fed slashed interest rates to zero.

After the crisis, inflation once again emerged as the top threat to the U.S. economy. In March 2022, the Fed raised rates by 25 basis points for the first time, and over the following year-plus, stepped on the gas relentlessly, lifting the benchmark rate to a high of 5.25–5.5%.

This week, the Fed delivered its first rate cut since April 2022, holding the benchmark rate at 4.75–5.0%.

"Central banks tend to focus on winning the last war," said Scott Sumner, Mercatus Center’s emeritus scholar in monetary policy at George Mason University:

"If inflation is high, they take a tougher stance. If inflation falls below target, the Fed thinks, 'Well, maybe we should pursue more expansionary policies.' When Powell took office, he was determined that if another recession hit, they’d adopt more aggressive policies. I think that strategy worked relatively well at first—but was pushed too far."

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News